Medicare Part D: Choosing the Right Prescription Drug Plan

-

Last Updated July 24, 2026

Introduction to Medicare Part D

Importance of Medicare Part D

If you take prescription medications, Medicare Part D is one of the most important coverage decisions you'll make. Medicare Part D is a federal program designed to subsidize the costs of prescription drugs for Medicare beneficiaries. Introduced in 2006, this program has become a vital component of healthcare for seniors and individuals with disabilities. A licensed Medicare agent who specializes in prescription drug coverage can help you navigate the options. Without Medicare Part D, many seniors would struggle to afford their medications, leading to poorer health outcomes and increased hospitalizations.

The significance of Medicare Part D cannot be overstated. It provides a safety net for those on a fixed income, ensuring they can access necessary medications without depleting their savings. The program also promotes preventive care by making medications for chronic conditions more affordable, thereby reducing the need for more expensive medical interventions down the line. (Note: Part D covers prescription medications but does not cover over-the-counter supplements, herbs, or homeopathic remedies.)

Purpose of this Article

Navigating the complexities of Medicare Part D can be daunting, especially with the numerous plans available and the varying coverage options. This article aims to demystify Medicare Part D and provide a clear, comprehensive guide to help you choose the right prescription drug plan. Whether you are new to Medicare or looking to switch plans during the open enrollment period, understanding the intricacies of Part D will empower you to make informed decisions about your healthcare.

In the following sections, we will delve into the details of Medicare Part D, starting with an overview of what it is and how it works. We will then explore the different types of plans available, the factors you should consider when selecting a plan, and the tools and resources that can aid in your decision-making process. Additionally, we will highlight common pitfalls to avoid and special considerations for those who may qualify for additional assistance.

By the end of this article, you will have a thorough understanding of Medicare Part D and the confidence to choose a prescription drug plan that best meets your needs. Let's get started on this journey to ensure you have the right coverage for your medications and peace of mind for your health.

Overview of Medicare Part D

Definition and Purpose

Medicare Part D is a federal program established under the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. It was implemented on January 1, 2006, to help Medicare beneficiaries pay for prescription drugs. Part D provides coverage for a wide range of medications, including those needed for chronic conditions, acute illnesses, and preventive care. The program is designed to make prescription drugs more affordable for seniors and individuals with disabilities, thereby improving their overall health and quality of life.

The purpose of Medicare Part D is to fill a significant gap in Medicare's original coverage. While Medicare Parts A and B cover hospital and medical services, they do not typically include outpatient prescription drugs. Part D addresses this gap by offering insurance for medication costs, reducing out-of-pocket expenses for beneficiaries.

Eligibility and Enrollment

To be eligible for Medicare Part D, individuals must first be enrolled in Medicare Part A and/or Part B. Generally, eligibility for Medicare begins at age 65, although younger individuals with certain disabilities or conditions such as End-Stage Renal Disease (ESRD) may also qualify.

Enrollment in Medicare Part D is not automatic; beneficiaries must actively enroll in a Part D plan during designated enrollment periods. These periods include:

- Initial Enrollment Period (IEP): This is a seven-month period that begins three months before the month you turn 65, includes your birth month, and extends three months after. During this time, you can sign up for a Part D plan without penalty.

- Annual Enrollment Period (AEP): From October 15 to December 7 each year, beneficiaries can enroll in a Part D plan, switch plans, or drop coverage. Changes made during AEP take effect on January 1 of the following year.

- Special Enrollment Period (SEP): Certain life events, such as moving to a new area or losing other credible prescription drug coverage, may qualify you for a SEP, allowing you to enroll in or change your Part D plan outside of the standard enrollment periods.

Costs Associated with Part D

Medicare Part D costs can vary significantly depending on the specific plan you choose and your medication needs. Key cost components include:

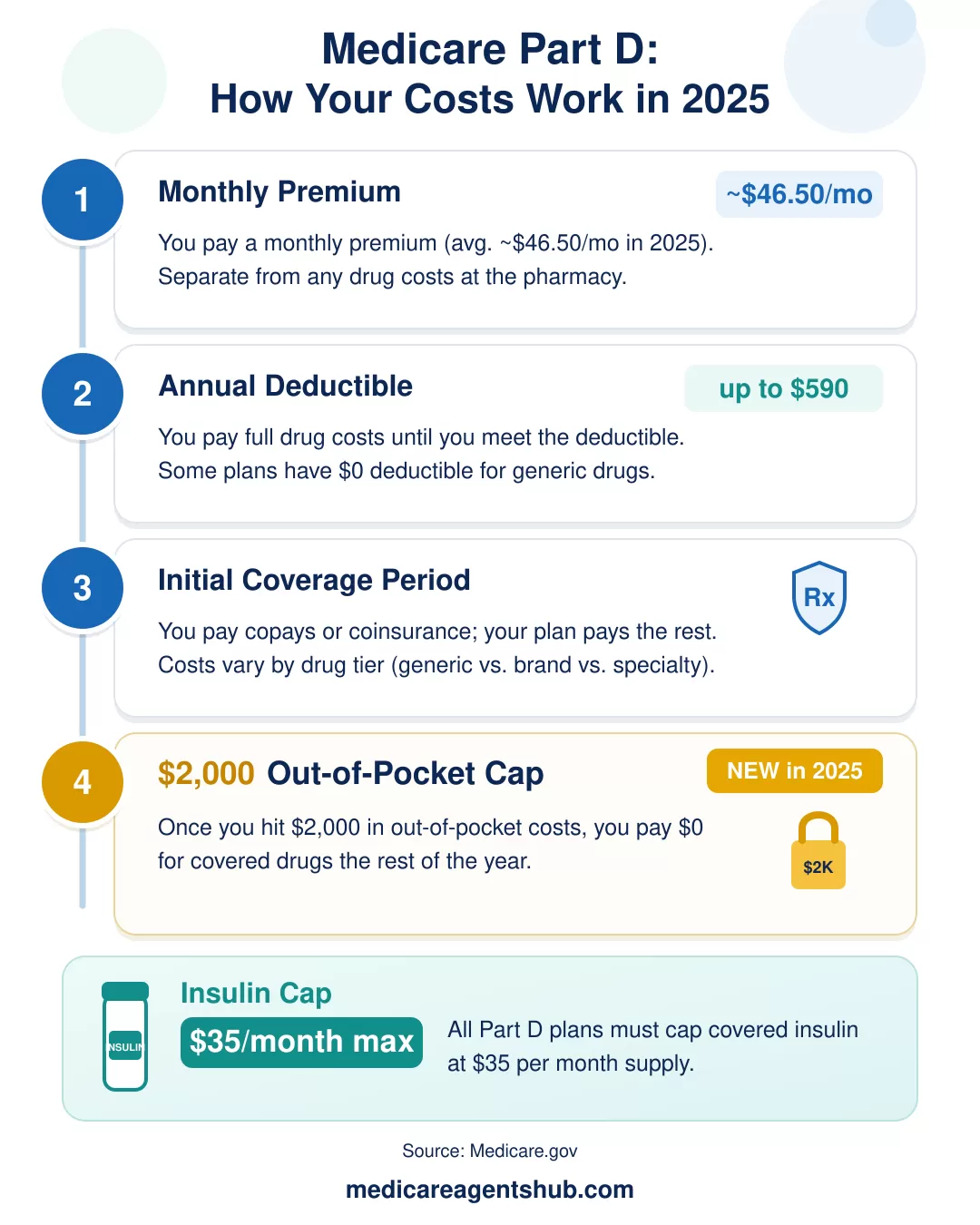

- Monthly Premiums: Each Part D plan charges a monthly premium, which varies by plan and provider. In 2025, the average basic Part D premium is approximately $46.50 per month, but premiums can be higher or lower depending on the plan's coverage and benefits.

- Annual Deductibles: Before your Part D plan starts paying its share, you may need to meet an annual deductible. The deductible amount can vary but cannot exceed a certain limit set by Medicare each year. For 2025, the maximum deductible is $590.

- Copayments and Coinsurance: After meeting the deductible, you will typically pay a portion of the cost of your medications through copayments or coinsurance. Copayments are fixed amounts you pay for each prescription, while coinsurance is a percentage of the drug's cost. Understand why generic drug prices sometimes increase so you can plan accordingly.

- Annual Out-of-Pocket Cap: Thanks to the Inflation Reduction Act, starting in 2025 your total out-of-pocket spending on Part D drugs is capped at $2,000 per year. This replaces the old "donut hole" coverage gap, which previously left beneficiaries paying 25% of drug costs between certain thresholds. Once you hit $2,000, you pay nothing more for covered prescriptions for the rest of the year.

- $35 Insulin Cap: Part D plans now cap the cost of a month's supply of covered insulin at $35, regardless of which coverage phase you're in. This applies to all insulin products covered by the plan and can save hundreds of dollars per year for beneficiaries managing diabetes.

Understanding these costs is crucial for budgeting and selecting a Part D plan that aligns with your financial and healthcare needs.

How will the new 2025 Medicare Part D out-of-pocket cap impact seniors and prescription drug costs?

The $2,000 out-of-pocket cap on Medicare Part D drug costs that took effect in 2025 is one of the most significant improvements to Medicare drug coverage since Part D launched in 2006. Before this change there was effectively no ceiling on what a beneficiary could spend on prescriptions in a given year, which left people on high-cost specialty medications in a really difficult financial position. Now once you hit $2,000 in out-of-pocket drug costs your cost sharing drops to zero for the rest of the calendar year, making prescription costs far more predictable. The cap also pairs with the new Medicare Prescription Payment Plan, which lets you spread that potential out-of-pocket cost across monthly installments rather than absorbing large expenses early in the year. That said, premiums and formularies vary across plans, so running a plan comparison each fall during Annual Enrollment is the best way to make sure you are getting the most out of these new protections.Medicare Part D is a vital part of the Medicare program, providing essential prescription drug coverage to millions of Americans. By understanding the basics of Part D, eligibility requirements, and associated costs, you can make informed decisions about your prescription drug coverage and ensure you have access to the medications you need.

Types of Medicare Part D Plans

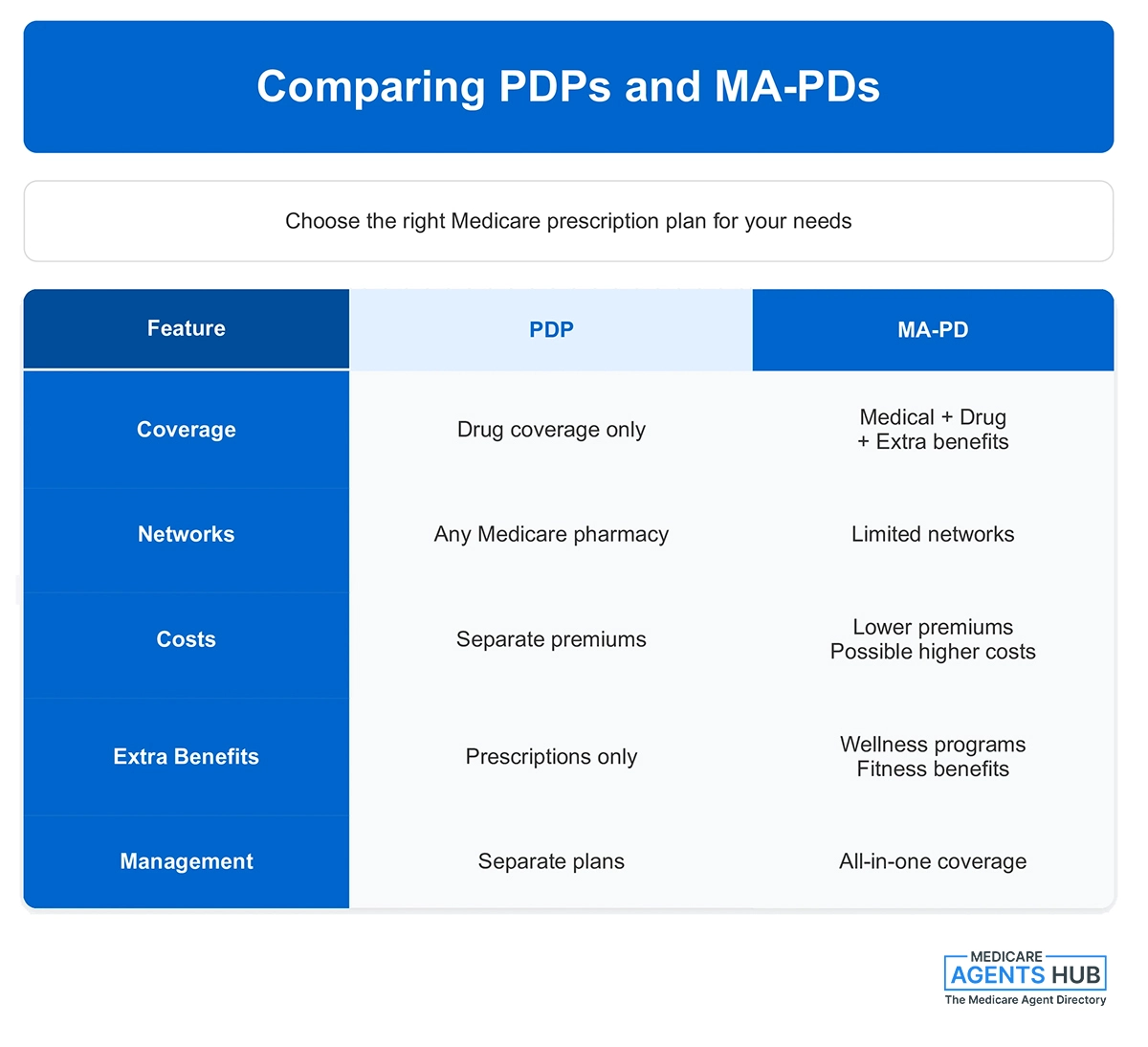

When it comes to Medicare Part D, there are two main types of plans that provide prescription drug coverage: Stand-Alone Prescription Drug Plans (PDPs) and Medicare Advantage Plans with Prescription Drug Coverage (MA-PDs). Understanding the differences between these plan types is crucial for choosing the one that best meets your needs. View a list of the most popular medications among Medicare beneficiaries.

Stand-Alone Prescription Drug Plans (PDPs)

Stand-Alone Prescription Drug Plans (PDPs) are designed to add drug coverage to your Original Medicare (Part A and Part B). These plans are ideal for individuals who want to keep their Original Medicare coverage and add prescription drug benefits separately.

Key Features of PDPs:

- Independent Coverage: PDPs are separate from your Original Medicare coverage. They exclusively cover prescription drugs and do not include medical services.

- Wide Availability: PDPs are available nationwide, with numerous plans to choose from, allowing beneficiaries to select a plan that fits their specific medication needs.

- Formulary and Network: Each PDP has its own formulary (list of covered drugs) and pharmacy network. This is especially important for newer medications like GLP-1 drugs for diabetes and weight management, which may not appear on every formulary. It’s essential to ensure your medications are included in the plan’s formulary and that your preferred pharmacy is in the network.

- Cost Structure: PDPs have varying premiums, deductibles, and copayments/coinsurance. Comparing these costs across plans is vital for finding the most cost-effective option.

Who Should Consider a PDP?

- Individuals who are satisfied with their Original Medicare coverage but need prescription drug coverage.

- Those who want the flexibility to choose a drug plan that specifically meets their medication requirements.

Medicare Advantage Plans with Prescription Drug Coverage (MA-PDs)

Medicare Advantage Plans (Part C) are an alternative to Original Medicare, offered by private insurance companies approved by Medicare. Many Medicare Advantage Plans include prescription drug coverage, known as Medicare Advantage Prescription Drug plans (MA-PDs).

Key Features of MA-PDs:

- Comprehensive Coverage: MA-PDs provide all-in-one coverage, including Medicare Part A, Part B, and Part D benefits. They often include additional services such as dental, vision, and hearing care.

- Network-Based: MA-PDs typically require you to use a network of doctors, hospitals, and pharmacies. There are different types of Medicare Advantage plans, such as Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs), which have varying rules about network usage.

- Extra Benefits: Many MA-PDs offer additional benefits not covered by Original Medicare, such as wellness programs, gym memberships, and transportation to medical appointments.

- Cost Structure: MA-PDs often have lower monthly premiums than standalone PDPs, but you may pay higher out-of-pocket costs for services. These plans also have an annual out-of-pocket maximum, which can provide financial protection against high medical costs.

Who Should Consider an MA-PD?

- Individuals who prefer an all-in-one plan that includes medical and prescription drug coverage.

- Those who want additional benefits beyond what Original Medicare offers.

- Beneficiaries who are comfortable using a network of providers and pharmacies.

Comparing PDPs and MA-PDs

Choosing between a PDP and an MA-PD involves considering various factors, including your healthcare needs, budget, and lifestyle preferences. Here are some key points to help you compare the two types of plans:

- Coverage Scope: If you want comprehensive coverage, including additional benefits like dental and vision care, an MA-PD might be more suitable. If you prefer to keep your Original Medicare and only need drug coverage, a PDP is the way to go.

- Provider and Pharmacy Networks: MA-PDs require you to use a network of providers and pharmacies, which can limit your choices. PDPs offer more flexibility, allowing you to use any pharmacy that accepts Medicare.

- Costs: Compare the premiums, deductibles, copayments, and out-of-pocket maximums for both plan types. While MA-PDs may have lower premiums, consider the potential for higher costs for medical services.

- Extra Benefits: Consider whether the additional benefits offered by MA-PDs are valuable to you. These can include fitness programs, preventive care services, and wellness incentives.

- Convenience: An MA-PD offers the convenience of having all your Medicare benefits under one plan, which can simplify managing your healthcare. A PDP, combined with Original Medicare, may involve dealing with separate entities for medical and drug coverage.

Understanding the types of Medicare Part D plans available and their respective features is the first step in making an informed decision about your prescription drug coverage. Whether you choose a PDP or an MA-PD, the goal is to ensure you have access to the medications you need at a cost you can afford.

My diabetes medication is super expensive, and I've heard horror stories about Part D not covering what people need. Should I go standalone Part D or get it through a Medicare Advantage plan?

The right answer depends on your exact medications, not the plan type.Both standalone Part D and Medicare Advantage plans can either cover your drugs well or poorly—it varies by plan formulary, dosage, and pharmacy.

For diabetes specifically, some plans cover insulin well but don’t cover newer or brand-name drugs as favorably.

Best approach: work though a broker and run your exact medication list through both options and compare total annual cost (premiums + copays). That’s how you avoid the “horror stories.”

Factors to Consider When Choosing a Part D Plan

Selecting the right Medicare Part D plan requires careful consideration of several factors to ensure the plan meets your medication needs and budget. Here are the key aspects to evaluate:

Formulary (Drug List)

The formulary is a list of prescription drugs covered by a Part D plan. Understanding the formulary is crucial because not all plans cover all medications.

- Check Your Medications: Ensure that your current prescriptions are included in the plan's formulary. If a medication is not covered, you may have to pay for it out-of-pocket or switch to an alternative drug.

- Drug Tiers: Formulary drugs are typically categorized into tiers, with different cost-sharing amounts. Lower-tier drugs generally have lower copayments, while higher-tier drugs have higher out-of-pocket costs. Be aware of which tier your medications fall into.

- Restrictions and Requirements: Some plans impose restrictions such as prior authorization, step therapy, or quantity limits. Prior authorization requires approval before the plan covers the drug. Step therapy mandates trying a less expensive drug first. Quantity limits restrict the amount of medication covered.

I'm confused about the different tiers in Medicare Part D plans. How do they affect what I pay for my medications?

The tiers on your part D plan can be thought of as "copay levels" that each of your medications is assigned to. Many plans have 5 tiers. In general, the higher the tier, the higher the copay you pay at the pharmacy. So, medications assigned to tiers 1 and 2 are usually lower cost medications such as generics. Tiers 3 through 5 are usually more expensive brand name medications. Note that you may have to pay the full cost of your medication until you have met your plan's deductible before you pay the copay corresponding to a particular medication's assigned tier.Pharmacy Network

Part D plans have networks of pharmacies where you can fill your prescriptions. Using an in-network pharmacy can significantly reduce your costs.

- Preferred vs. Standard Pharmacies: Some plans offer lower copayments at preferred pharmacies compared to standard ones. Ensure your preferred pharmacy is in the plan’s network and check if it is a preferred or standard option.

- Mail-Order Options: Many plans offer mail-order services, which can be convenient for maintenance medications and may provide cost savings. Verify if the plan offers mail-order and consider using it for your long-term prescriptions.

Costs and Coverage

Understanding the costs associated with a Part D plan helps you budget for your medications and avoid unexpected expenses.

- Monthly Premiums: Compare the monthly premiums of different plans. While lower premiums might seem attractive, ensure the plan adequately covers your medications.

- Annual Deductibles: The deductible is the amount you pay out-of-pocket before the plan begins to share the cost. Some plans have no deductible, while others have deductibles up to a limit set by Medicare. In 2025, the maximum deductible is $590.

- Copayments and Coinsurance: After meeting the deductible, you will pay either a copayment (a fixed amount) or coinsurance (a percentage of the drug cost) for your medications. Compare these costs across plans for the medications you take.

- Out-of-Pocket Cap: Starting in 2025, your annual out-of-pocket drug costs are capped at $2,000. Once you reach this limit, your plan covers 100% of your prescription costs for the rest of the year. This replaced the old "donut hole" coverage gap.

- Post-Cap Coverage: After reaching the $2,000 out-of-pocket cap, you pay $0 for covered prescriptions for the remainder of the year. This is a major improvement from the old system where beneficiaries still owed copayments even in catastrophic coverage.

Plan Ratings and Reviews

Medicare assigns star ratings to Part D plans based on various performance metrics. These ratings range from one to five stars, with five being the highest.

- Medicare Star Ratings: Review the plan’s star rating, which reflects customer satisfaction, drug safety, and customer service. A higher-rated plan generally indicates better quality and reliability.

- Customer Reviews: Look for reviews from current or past enrollees to gain insights into the plan’s performance, customer service, and any issues they might have encountered. Online forums and review sites can be helpful.

Extra Considerations

- Special Needs Plans (SNPs): If you have specific health conditions or circumstances, such as chronic illnesses or being dual-eligible for Medicare and Medicaid, consider a Special Needs Plan tailored to your situation. For example, if you need coverage for cancer treatment, a plan designed for chronic conditions can simplify access to chemotherapy drugs and specialist care.

- State Pharmaceutical Assistance Programs (SPAPs): Some states offer assistance programs that help pay for Part D premiums and other costs. Check if you qualify for additional support from your state.

- Low-Income Subsidy (LIS): Also known as Extra Help, this federal program helps low-income individuals with Part D costs. If you qualify, you can receive assistance with premiums, deductibles, and copayments. Eligibility depends on income and resources, and you can apply through the Social Security Administration.

Choosing the right Medicare Part D plan involves balancing cost, coverage, and convenience to find the best fit for your needs. By carefully evaluating the formulary, pharmacy network, costs, plan ratings, and additional considerations, you can make an informed decision that ensures access to necessary medications without undue financial burden.

How to Compare Medicare Part D Plans

Choosing the right Medicare Part D plan can be challenging, but using the right tools and understanding the comparison process can simplify the task. Here’s a step-by-step guide to help you compare plans effectively:

Using the Medicare Plan Finder Tool

The Medicare Plan Finder tool is a powerful resource provided by Medicare to help beneficiaries compare Part D plans based on their specific needs. Here’s how to use it:

- Access the Tool: Visit the official Medicare website and navigate to the Medicare Plan Finder tool.

- Enter Personal Information: Input your ZIP code to view plans available in your area. You can also create an account or log in to save your information and view personalized recommendations.

- Enter Medications: List all your current medications, including the dosage and frequency. This step ensures the tool can accurately compare the costs of different plans based on your medication needs.

- Choose Pharmacies: Select your preferred pharmacies. The tool will show you the costs at these pharmacies and help you determine if they are in-network for the plans you are considering.

- Review Plan Options: The tool will display a list of plans available in your area, sorted by the lowest estimated annual retail drug costs. Review the details of each plan, including premiums, deductibles, copayments, and formulary coverage.

- Compare Side-by-Side: Use the tool’s side-by-side comparison feature to directly compare up to three plans. Pay attention to key factors such as total estimated annual cost, coverage for your specific medications, and any plan restrictions.

- Consider Plan Ratings: Review the star ratings for each plan, which reflect the plan’s overall performance and customer satisfaction. Higher-rated plans generally offer better service and reliability.

How do I compare Part D plans to minimize costs for a mix of generic and specialty drugs?

The most effective way is to compare plans using your exact medication list, including dosage and preferred pharmacies. Enter everything into Medicare’s Plan Finder to see total annual cost, not just premiums, since specialty drugs can significantly impact costs. Pay close attention to each plan’s formulary, drug tiers, prior authorization rules, and preferred pharmacy pricing. Also review how the plan performs across the year, especially with the $2,000 out-of-pocket cap, to understand when you’ll hit higher or lower costs. The best plan is the one with the lowest total yearly cost for your specific drugs, not necessarily the lowest premium.Consulting with a Medicare Agent

Working with a licensed Medicare agent can provide additional support - for free - and personalized advice. Here’s how a Medicare agent can help:

- Personalized Recommendations: Agents can provide tailored recommendations based on your specific health needs, financial situation, and preferences.

- Expert Knowledge: Agents have in-depth knowledge of Medicare Part D plans and can explain the nuances of different plan options, formularies, and costs.

- Enrollment Assistance: Agents can assist with the enrollment process, ensuring you understand each step and complete it accurately.

- Ongoing Support: Many agents offer ongoing support, helping you review your plan annually and make changes during open enrollment if necessary. With the declining support available for Part D plan selection, having an agent in your corner is more valuable than ever.

Evaluating Costs and Coverage

When comparing plans, it’s essential to evaluate the costs and coverage details carefully. Here’s what to focus on:

- Monthly Premiums: While a lower premium may seem attractive, it’s crucial to consider the overall cost, including deductibles and out-of-pocket expenses.

- Annual Deductibles: Check if the plan has a deductible and how it impacts your initial out-of-pocket costs.

- Copayments and Coinsurance: Review the copayments or coinsurance amounts for your medications. These costs can vary significantly between plans, especially for higher-tier drugs.

- Coverage Gap: Understand the plan’s coverage in the donut hole. Some plans offer additional coverage in this phase, which can reduce your out-of-pocket costs.

- Zero-Cost Coverage After Cap: Once you hit the $2,000 out-of-pocket cap, your plan covers all remaining prescription costs. This applies to all Part D plans, so focus your comparison on costs during the earlier coverage phases.

Considering Additional Benefits and Features

Some Part D plans offer additional benefits and features that can enhance your coverage and convenience:

- Medication Therapy Management (MTM): Some plans offer MTM programs to help you manage your medications, optimize therapeutic outcomes, and reduce the risk of adverse effects.

- Pharmacy Networks: Evaluate the plan’s pharmacy network, including preferred and standard pharmacies, as well as mail-order options. Using in-network pharmacies can significantly reduce your costs.

- Extra Services: Consider any extra services or perks offered by the plan, such as discounts on over-the-counter medications, health and wellness programs, or access to specialized care.

Reviewing Plan Changes Annually

Medicare Part D plans can change their costs and coverage each year. It’s crucial to review your plan annually during the Open Enrollment Period (October 15 to December 7) to ensure it still meets your needs:

- Annual Notice of Change (ANOC): Review the ANOC sent by your current plan, which outlines any changes in coverage, costs, and formulary for the upcoming year.

- Re-evaluate Your Needs: Consider any changes in your health, medications, or financial situation that might affect your plan choice.

- Compare New Plans: Use the Medicare Plan Finder tool or consult with a Medicare agent to compare new plans available in your area.

By following these steps and considering all relevant factors, you can make an informed decision when choosing a Medicare Part D plan that best suits your needs and budget.

Common Pitfalls and How to Avoid Them

Navigating Medicare Part D can be complex, and there are several common pitfalls that beneficiaries might encounter. Understanding these pitfalls and how to avoid them can help ensure you select the best plan for your needs and avoid unnecessary costs or disruptions in your medication coverage.

Failing to Review Annual Changes

Medicare Part D plans can change their costs, coverage, and formulary every year. One of the most common mistakes is failing to review these annual changes, which can lead to unexpected costs or loss of coverage for specific medications.

- Annual Notice of Change (ANOC): Each fall, your Part D plan will send an ANOC that details changes to the plan’s benefits and costs for the upcoming year. Carefully review this document to understand how your plan will change.

- Open Enrollment Period: From October 15 to December 7, you can compare your current plan with other available plans. Use this period to ensure your plan still meets your needs. If significant changes affect your coverage or costs, consider switching plans.

- Proactive Review: Regularly reviewing your plan details and costs, even outside the open enrollment period, helps you stay informed and prepared for any necessary adjustments.

Ignoring the Formulary

The formulary, or drug list, varies by plan and can change annually. Ignoring the formulary can result in higher out-of-pocket costs or lack of coverage for essential medications.

- Check Your Medications: Always ensure that your current medications are covered by the plan’s formulary. If a drug you take regularly is not covered, it can significantly impact your costs.

- Understand Drug Tiers: Medications are categorized into tiers, each with different cost-sharing requirements. Verify which tier your drugs fall into, as higher-tier drugs typically have higher copayments or coinsurance.

- Formulary Updates: Plans can update their formularies throughout the year. Stay informed about any changes by regularly checking your plan’s formulary online or through communications from your plan.

Overlooking Additional Costs

Many beneficiaries focus solely on monthly premiums, overlooking other costs such as deductibles, copayments, and coinsurance. These additional costs can add up and significantly impact your overall expenses.

- Total Cost Evaluation: When comparing plans, consider all costs, including premiums, deductibles, copayments, and coinsurance. The plan with the lowest premium may not always be the most cost-effective when all factors are considered.

- Deductibles: Some plans have high deductibles that must be met before coverage begins. Ensure you understand how much you’ll need to pay out-of-pocket before the plan starts to cover your medications.

- Copayments and Coinsurance: Pay attention to the cost-sharing structure for your medications. Higher copayments and coinsurance rates can lead to higher out-of-pocket costs, especially for expensive or high-tier drugs.

Not Understanding the New $2,000 Out-of-Pocket Cap

The old "donut hole" coverage gap has been replaced by a $2,000 annual out-of-pocket cap starting in 2025. While this is great news, many beneficiaries are still confused about how the new system works, which can lead to missed savings opportunities.

- The $2,000 Out-of-Pocket Cap: Starting in 2025, the old donut hole has been replaced by a hard $2,000 annual cap on out-of-pocket drug spending. Once you reach this cap, you pay nothing for covered prescriptions the rest of the year.

- Medicare Prescription Payment Plan: To help manage costs before reaching the cap, Medicare now offers a payment plan option that spreads your out-of-pocket drug costs evenly across the year in monthly installments. Ask your plan about this option.

- Track Your Spending: Even with the $2,000 cap, it’s important to track your drug spending throughout the year so you know when you’re approaching the cap. Your plan’s Explanation of Benefits (EOB) statements will show your running total.

I'm worried about the 'donut hole' in my Part D plan. How do I manage my medication costs once I enter it?

The donut hole no longer exist. It was ended in 2025. Drugs are capped in 2025 at $2,000 for the year and that cost goes up to a max of $2,100 for 2026. There is also a monthly payment plan set up now that you can enroll in if you choose that breaks that down monthly so you don’t have to come up with high out of pocket costs until you hit the max out of pocket.Not Utilizing Available Assistance Programs

Many beneficiaries are unaware of assistance programs that can help reduce Part D costs. Failing to utilize these programs can result in higher out-of-pocket expenses.

- Low-Income Subsidy (LIS) or Extra Help: This federal program helps low-income beneficiaries with Part D costs, including premiums, deductibles, and copayments. Eligibility is based on income and resources. Apply through the Social Security Administration if you think you might qualify.

- State Pharmaceutical Assistance Programs (SPAPs): Some states offer programs to assist with Part D costs. Check if your state has an SPAP and if you qualify for assistance.

- Manufacturer Assistance Programs: Some pharmaceutical manufacturers offer programs to help with the cost of specific medications. These programs can provide significant savings for high-cost drugs.

Delaying Enrollment

Delaying enrollment in a Part D plan can result in late enrollment penalties, which are added to your monthly premium and continue for as long as you have Part D coverage.

- Initial Enrollment Period (IEP): Enroll during your IEP, which starts three months before your 65th birthday, includes your birth month, and ends three months after.

- Special Enrollment Periods (SEPs): Certain life events, such as losing other credible prescription drug coverage, can qualify you for a SEP to enroll without penalty.

- Avoiding Penalties: If you don’t enroll in a Part D plan when first eligible and don’t have other credible drug coverage, you may face a late enrollment penalty when you do sign up. This penalty is calculated based on the number of months you were eligible but didn’t enroll and can add significantly to your premiums.

By understanding these common pitfalls and taking proactive steps to avoid them, you can make more informed decisions about your Medicare Part D coverage, ensuring that you have access to the medications you need without unexpected costs or disruptions.

What's the biggest mistake seniors make when choosing a Medicare Part D plan?

Without a doubt the BIGGEST and the MOST COSTLY mistake Sr's make when they are eligible for Part D is to NOT take it "because I don't take any medications". When opting out of this you are setting yourself up for "forever" LEP (Late Enrollment Penalty) down the road. The Medicare Part D LEP is calculated at a 1% penalty for every month you were eligible for Part D and you DID NOT enroll. This 1%/per month is based on the national average cost of a Part D drug plan and a.) stays with you forever b.) recalculates every January to new "national average".The second biggest error is enrolling in a plan when turning 65 and having the monthly premium deducted from your monthly SS check. Over time, both plan premiums and member drug needs change and this is something that needs to be reviewed every year during AEP.

Most areas in the country will have $0 to low cost stand-alone PDP plans so do yourself a favor and don't bypass this when you are first eligible.

Special Considerations

When choosing a Medicare Part D plan, there are several special considerations that can significantly impact your coverage and costs. These considerations include programs and options for individuals with specific needs or circumstances, such as those with limited income or chronic health conditions. Understanding these special considerations can help you maximize your benefits and minimize your out-of-pocket expenses.

Low-Income Subsidy (LIS)

The Low-Income Subsidy (LIS), also known as Extra Help, is a federal program designed to assist beneficiaries with limited income and resources in paying for Medicare Part D costs. This subsidy can significantly reduce your prescription drug costs, including premiums, deductibles, and copayments.

- Eligibility: To qualify for Extra Help, your income must be at or below 150% of the federal poverty level, and your resources must fall under set limits. In 2025 that worked out to roughly $23,475 in annual income for an individual and $31,725 for a married couple, with resource limits of about $17,600 (individual) and $35,130 (couple). These thresholds are adjusted each year, so check the Social Security Administration for the current figures. Resource limits include savings, investments, and real estate, but exclude your primary residence, personal possessions, and one vehicle.

- Benefits: If you qualify for Extra Help, prescription copays are capped at just a few dollars for generics and around $12 for brand-name drugs, and you may have reduced or no premiums and deductibles.

- Application: You can apply for Extra Help through the Social Security Administration (SSA) online, by phone, or at your local SSA office. Additionally, some individuals are automatically enrolled if they receive Medicaid, Supplemental Security Income (SSI), or other assistance from their state.

I'm on a fixed income and struggling to afford my medications. What's this Extra Help program I've heard about for Medicare Part D?

The Extra Help program is a Medicare program that helps people with limited income and resources pay for their Part D prescription drug costs. It can lower or even cover your monthly premiums, deductibles, and copayments, making your medications much more affordable.You can apply through the Social Security Administration, and if you qualify, the help is automatic every year — so it’s worth checking to see if you’re eligible, especially if you’re on a fixed income.

State Pharmaceutical Assistance Programs (SPAPs)

Some states offer Pharmaceutical Assistance Programs (SPAPs) to help residents with prescription drug costs. These programs vary by state and can provide significant financial assistance for Medicare Part D enrollees.

- Eligibility and Benefits: Each state has its own eligibility criteria, which typically include income limits and residency requirements. Benefits may include assistance with premiums, deductibles, copayments, and coverage during the coverage gap (donut hole).

- How to Apply: To find out if your state offers an SPAP and how to apply, contact your State Health Insurance Assistance Program (SHIP) or visit your state’s health department website.

Special Needs Plans (SNPs)

Special Needs Plans (SNPs) are a type of Medicare Advantage plan tailored to meet the specific needs of certain groups of people, including those with chronic conditions, those institutionalized, and dual eligibles (those eligible for both Medicare and Medicaid).

- Chronic Condition SNPs (C-SNPs): These plans are designed for individuals with specific chronic or disabling conditions, such as diabetes, chronic heart failure, or HIV/AIDS. C-SNPs provide specialized care and coverage tailored to manage these conditions effectively.

- Institutional SNPs (I-SNPs): I-SNPs are for individuals who live in institutions like nursing homes or require nursing care at home. These plans focus on providing coordinated care to meet the complex health needs of these individuals.

- Dual Eligible SNPs (D-SNPs): D-SNPs are for people who are eligible for both Medicare and Medicaid. These plans offer integrated benefits to simplify access to healthcare services and reduce out-of-pocket costs.

- Eligibility and Enrollment: To enroll in an SNP, you must meet the specific eligibility criteria for that type of plan. Enrollment is typically available year-round for SNPs, unlike other Medicare Advantage plans that have specific enrollment periods.

Employer and Union Coverage

Some individuals have prescription drug coverage through an employer or union plan. It’s important to understand how this coverage works with Medicare Part D.

- Creditable Coverage: Employer or union health plans that provide prescription drug coverage must notify you each year if their coverage is considered “creditable.” Creditable coverage means that the plan is expected to pay, on average, at least as much as Medicare’s standard prescription drug coverage.

- Maintaining Coverage: If you have creditable coverage, you can delay enrolling in a Medicare Part D plan without incurring a late enrollment penalty. However, if you lose your employer or union coverage, you’ll have a Special Enrollment Period (SEP) to join a Part D plan.

- Coordination of Benefits: If you have both Medicare Part D and employer or union coverage, it’s important to understand how the two plans will work together to pay for your prescriptions. Contact your employer or union benefits administrator for details.

Veterans Affairs (VA) Benefits

Veterans who are eligible for healthcare benefits through the Department of Veterans Affairs (VA) may also consider their prescription drug coverage options.

- VA Coverage: The VA offers comprehensive prescription drug coverage, which is often as good as or better than Medicare Part D. If you have VA coverage, you are not required to enroll in a Part D plan, but you may choose to do so if it provides additional benefits.

- Dual Enrollment: Veterans can have both VA and Medicare Part D coverage. This can provide more flexibility in choosing where to get your medications. However, VA and Part D plans do not coordinate benefits, meaning you cannot use both plans for the same prescription.

By understanding and utilizing these special considerations, you can ensure that you maximize your Medicare Part D benefits and minimize your out-of-pocket expenses. Whether through federal assistance programs, state initiatives, specialized plans, or coordinating with other coverage, these options can provide significant support in managing your prescription drug costs.

Conclusion

Recap of Key Points

Choosing the right Medicare Part D plan is a critical decision that can significantly impact your health and financial well-being. This comprehensive guide has covered several essential aspects to help you navigate the process. We started by explaining the basics of Medicare Part D, including its purpose and the eligibility requirements. Understanding these fundamentals is the first step toward making an informed decision.

We then delved into the different types of Part D plans available: Stand-Alone Prescription Drug Plans (PDPs) and Medicare Advantage Plans with Prescription Drug Coverage (MA-PDs). Each type of plan offers unique benefits and considerations, and choosing the right one depends on your specific healthcare needs and preferences.

Next, we discussed the key factors to consider when selecting a Part D plan, such as the formulary, pharmacy network, and overall costs. These elements play a crucial role in determining how well a plan will meet your needs. We also highlighted the importance of using tools like the Medicare Plan Finder and consulting with a Medicare agent to compare plans effectively.

We addressed common pitfalls that can arise when choosing a Part D plan, such as failing to review annual changes, ignoring the formulary, and misunderstanding the coverage gap. By being aware of these potential issues and taking proactive steps to avoid them, you can ensure smoother, more cost-effective coverage.

Special considerations, such as the Low-Income Subsidy (LIS), State Pharmaceutical Assistance Programs (SPAPs), Special Needs Plans (SNPs), and employer or union coverage, were also explored. These programs and options can provide significant financial assistance and tailored coverage for individuals with specific needs or circumstances.

Take Action Now & Get Informed

Now that you have a thorough understanding of Medicare Part D, it's time to take action. Whether you are new to Medicare or considering switching plans during the open enrollment period, use the information and tools provided in this guide to make an informed decision. Start by listing your medications, evaluating your pharmacy preferences, and estimating your budget for prescription drugs.

Don’t hesitate to seek help from a licensed Medicare agent who can provide personalized advice and assist you in navigating the complexities of Medicare Part D. Remember, the goal is to find a plan that offers the best combination of coverage, convenience, and cost-effectiveness for your specific needs.

Ready to speak with a local expert?

A licensed Medicare agent can review your medications, compare plans in your area, and help you enroll at no cost to you.

Find a licensed Medicare agent near youReview your plan annually to ensure it continues to meet your needs and make any necessary changes during the open enrollment period. Staying informed and proactive will help you avoid potential pitfalls and maximize your benefits.

Resources for Further Assistance

To further assist you in your journey, here are some valuable resources:

- Medicare Plan Finder: The official Medicare Plan Finder tool (available at www.medicare.gov) is an excellent resource for comparing Part D plans based on your specific needs and location.

- State Health Insurance Assistance Program (SHIP): SHIP offers free, unbiased counseling on Medicare options. Visit www.shiptacenter.org to find your local SHIP.

- Social Security Administration (SSA): For information and applications for the Low-Income Subsidy (Extra Help) program, visit www.ssa.gov or call 1-800-772-1213.

- Pharmaceutical Assistance Programs: Check with your state’s health department or visit https://www.cms.gov/medicare/coordination-benefits-recovery/prescription-drug-assistance-programs for information on state-specific assistance programs.

- Medicare Rights Center: This nonprofit organization provides education and advocacy for Medicare beneficiaries. Visit www.medicarerights.org or call their helpline at 1-800-333-4114 for support.

By utilizing these resources, you can gain additional insights and support as you navigate your Medicare Part D options. Taking the time to thoroughly research and compare plans will pay off in the long run, ensuring you have the coverage you need at a price you can afford.

In conclusion, selecting the right Medicare Part D plan is a crucial aspect of managing your healthcare. With the right information and tools, you can make informed decisions that provide peace of mind and ensure access to necessary medications. Agents do not charge for their services, and can help walk you through your drug coverage. Empower yourself with knowledge, seek professional advice when needed, and stay proactive in reviewing and adjusting your plan to meet your evolving needs.