Does Medicare Cover Repatha? Costs, Coverage, and Ways to Save in 2026

-

May 25, 2026

Sources checked: CMS 2026 Part D redesign guidance, Medicare & You 2026, Amgen pricing announcement, FDA Repatha prescribing information, Medicare.gov Plan Finder.

This article explains Medicare coverage and costs. It is not medical advice. Ask your cardiologist whether Repatha, Praluent, Leqvio, ezetimibe, bempedoic acid, or another treatment is appropriate for you.

If your doctor prescribed Repatha (evolocumab) to lower your LDL cholesterol, the first question is usually the same: will Medicare actually pay for it, and how much will it cost me? The short answer is yes, most Medicare Part D plans cover Repatha, but it typically sits on a higher formulary tier and almost always requires prior authorization. The longer answer involves which plan you have, what step therapy your insurer demands, and how the $2,100 out-of-pocket cap changes the math in 2026.

This guide walks through how Repatha is covered, what you can expect to pay, and the steps that actually move the bill down.

Does Medicare Part D Cover Repatha?

Repatha is a PCSK9 inhibitor used to lower LDL cholesterol in adults who can't reach their target on statins alone, or who have heart disease or familial hypercholesterolemia. Because it's a self-injected biologic you administer at home, it falls under Medicare Part D, not Part B. (Drugs administered in a doctor's office, like infusions, are the ones that typically go through Part B.)

The large majority of standalone Part D plans and Medicare Advantage prescription drug plans include Repatha on their formulary in 2026. Licensed agents who regularly run formulary checks report coverage in roughly 95% of plans, though this varies by region. The catch is that coverage and affordability aren't the same thing. Repatha is on the formulary, but it's rarely on a low-cost tier, and your plan will likely require prior authorization before paying its share.

It's worth noting that a small number of carriers don't cover Repatha at all. This varies by region and by plan. In states like Florida, for example, some carriers exclude it from their formulary entirely, which means you'd pay full price out of pocket. Always verify that Repatha is on the formulary of any plan you're considering before you enroll.

If you're new to Part D or trying to figure out how to compare plans for a specific medication, our breakdown of how to choose the right Medicare Part D plan covers the basics.

Does Medicare Part D cover Repatha?

Yes — Medicare Part D can cover Repatha. But not every Part D plan does, which is where people often get tripped up.Repatha is an expensive medication, so it’s essential to verify that it’s listed on the formulary of any Part D plan you’re considering. Never assume — always confirm.

When it is covered, Repatha is most commonly placed on a Tier 3 (Preferred Brand) tier. That usually means you’ll pay the full retail cost until the plan’s annual deductible is met (and with Repatha, you tend to meet that deductible quickly). After that, you’ll move into the plan’s Tier 3 copay or coinsurance structure.

Bottom line: Part D coverage for Repatha absolutely exists — but choosing the right plan makes a significant difference in what you’ll actually pay out of pocket.

What Tier Is Repatha on Most Part D Formularies?

Part D plans organize covered drugs into tiers, and your copay or coinsurance depends on which tier the drug sits in. Repatha lands on different tiers depending on the plan: many agents report seeing it on Tier 3 (preferred brand), while other plans place it on Tier 4 or 5 (specialty). That tier placement directly determines what you pay.

| Tier | Typical Drugs | What You Usually Pay |

|---|---|---|

| Tier 1 | Preferred generics | $0–$5 copay |

| Tier 2 | Generics | $5–$15 copay |

| Tier 3 | Preferred brand-name | $40–$50 copay |

| Tier 4 | Non-preferred brand | 40–50% coinsurance |

| Tier 5 (Specialty) | Biologics, some PCSK9 inhibitors | 25–33% coinsurance |

That's why the same prescription can carry wildly different costs from one plan to the next, even in the same ZIP code. Agents who work with Repatha patients regularly report that the difference between a Tier 3 placement and a Tier 5 placement can mean hundreds of dollars in savings per year. One detail that often gets overlooked: whether the Part D deductible applies to that tier. Some plans waive the deductible for Tier 3 drugs but not for Tier 5, which changes your first-month cost dramatically.

What tier is Repatha on Medicare Part D formularies?

Repatha may be on different tiers depending on the plan and carrier. I find it mostly on Tier 3 on the formularies. I have a few clients on Repatha so I will say that you should look into the cost carefully when comparing plans as it can differentiate by quite a bit depending on the cost of the Tier 3, the Part D drug deductible and if the Deductible applies to tier 3 or not.Prior Authorization and Step Therapy Requirements

Before your plan pays anything toward Repatha, it almost certainly wants two things:

- Prior authorization (PA): Your doctor has to submit clinical documentation showing why you need Repatha specifically.

- Step therapy: Many plans require documentation of prior statin therapy, intolerance or inadequate LDL response, and/or use of ezetimibe before they'll cover a PCSK9 inhibitor. The specific requirements vary by plan.

If you have a documented diagnosis of clinical atherosclerotic cardiovascular disease (ASCVD) or heterozygous familial hypercholesterolemia, the PA process tends to move faster. If your prescription is for primary prevention, expect more friction. If you're still getting up to speed on how Medicare drug coverage works in general, our plain-language Medicare overview covers the foundation before you tackle formulary details.

One thing worth understanding: PA requirements on specialty drugs like Repatha have been increasing since the $2,000 out-of-pocket cap took effect in 2025. Plans are now absorbing a larger share of high-cost drug expenses once patients hit the cap, so they're using prior authorization and step therapy more aggressively to control which patients access expensive medications. If you're switching Part D plans, check the new plan's prior authorization requirements before you enroll. PA rules that applied to your old plan don't carry over.

When your plan denies the request, you have appeal rights, and they're worth using. Denials are sometimes overturned when the prescribing physician submits stronger documentation or a detailed letter of medical necessity. If you're switching plans or facing a new formulary restriction, ask your plan or pharmacy whether you qualify for a transition fill. It may help avoid an immediate interruption, but don't wait until you are out of medication to start the process.

I switched to a new Part D plan and now half my meds require prior authorization. Why didn't anyone warn me this could happen?

Part D plans are private, and each creates its own unique "formulary" (drug list) and utilization rules. When you switch plans, your new insurer may impose prior authorization (PA) requirements on drugs that were previously covered automatically. These rules manage costs, ensure safety, or verify medical necessity for expensive or specialized medications. You are often entitled to a one-time "transition refill" (typically a 30-day supply) while your doctor works to obtain the necessary authorizations.Immediate Steps to Take

Request a Transition Fill: Contact your pharmacy or plan immediately and ask for a "transition refill." This provides a temporary supply while your provider navigates the authorization process.

Contact Your Prescriber: Your doctor’s office is responsible for submitting the prior authorization request. Contact them today to provide the plan's specific requirements, which you can find by calling the member services number on your new insurance card.

Ask About "Step Therapy" and Limits: When speaking with your plan, ask if the PA is due to "step therapy" (requiring you to try a cheaper alternative first) or "quantity limits" (caps on dosage or supply). Knowing this helps your doctor submit the correct paperwork the first time.

Appeal if Denied: If a prior authorization request is denied, you have the right to file an appeal. Start with the internal appeal process directly through your plan.

Plans rarely notify members individually about specific changes to how their current medications are covered prior to enrollment, which is why it is essential to review the "Evidence of Coverage" or use the Medicare.gov plan finder tool to check your specific drug list before switching. Keep in mind that authorizations often need to be renewed annually, so diarize this date to avoid future interruptions.

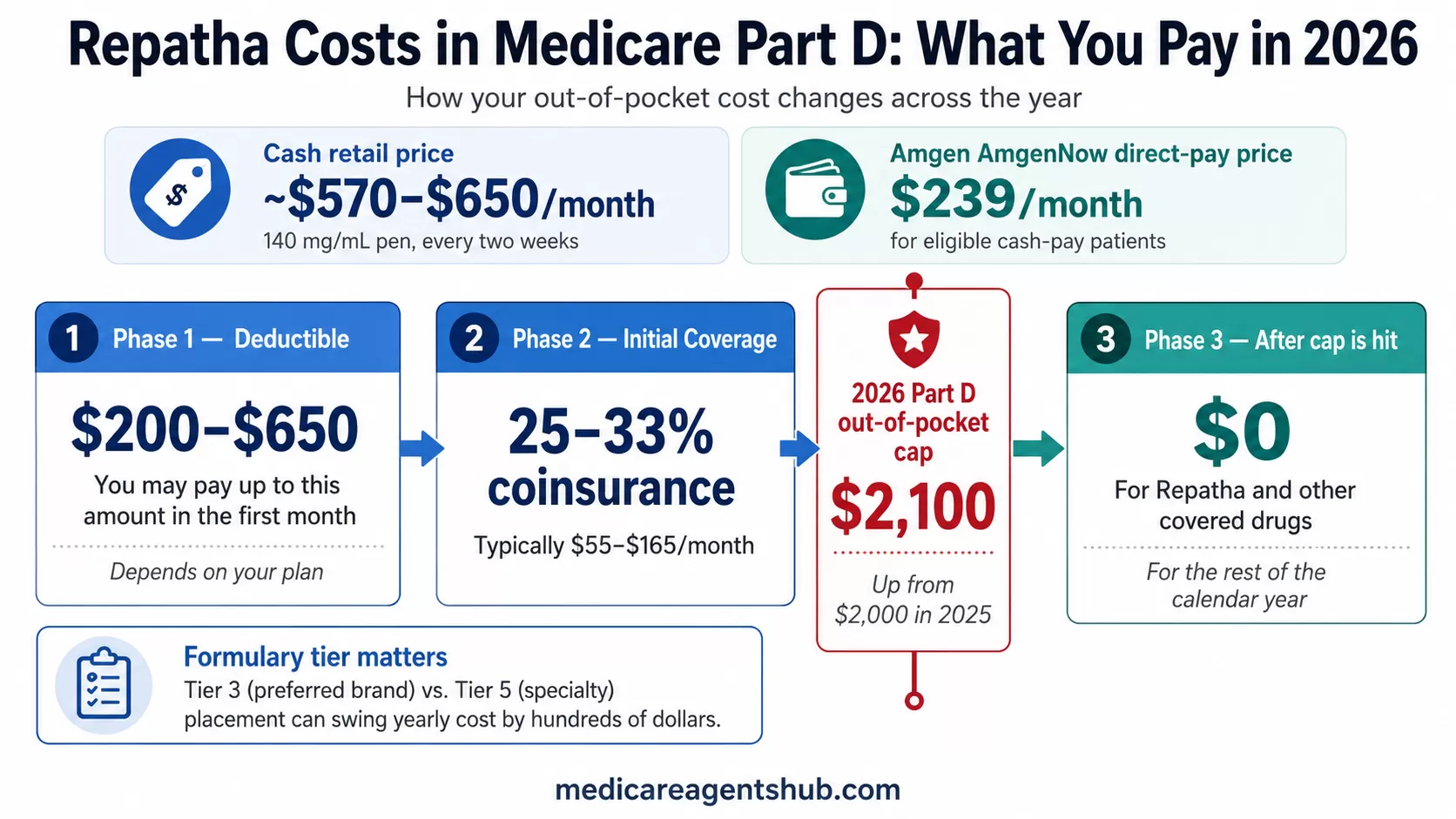

What You'll Actually Pay for Repatha in 2026

Repatha's retail price can vary by pharmacy and dosage form, but many cash prices fall in the roughly $570–$650/month range for the standard 140 mg/mL pen used every two weeks. Amgen's direct-pay AmgenNow program lists Repatha at $239/month for eligible cash-pay patients, and that lower price flows through to some Medicare plans as well.

Under a typical specialty-tier 25% coinsurance, what you'd pay in 2026 looks something like this:

- Deductible phase: Up to the full negotiated price, often $200–$650 the first month depending on your plan.

- Initial coverage phase: 25–33% of the drug's cost, usually $55–$165 per month.

- After you hit $2,100 out-of-pocket: $0 for Repatha and every other covered drug for the rest of the calendar year.

For most Repatha patients, the out-of-pocket cap is the difference between an affordable year and a financially brutal one. Many Repatha patients may reach the cap within the first several months, especially if they have deductible exposure or other expensive medications.

Your first-month cost swings more than most people realize based on which plan you're in. A low-premium plan ($5–$10/month) may charge you $650+ at the pharmacy in January because it applies a full deductible to brand-name drugs. A higher-premium plan ($80–$100/month) might drop that first fill to $200–$300 because it waives or reduces the deductible. Over the full year, the higher-premium plan can cost less in total when you add up premium plus drug costs. This is why running a full-year cost comparison matters more than looking at monthly premium alone.

Paying too much for Repatha on your current plan?

A licensed Medicare agent can run a full-year cost comparison with Repatha pre-loaded and show you which plans in your county cost less.

Find a Local Medicare Agent

How do drug tiers work in Medicare Part D?

Prescription drug plans (PDP's) and Medicare Advantage Prescription Drug plans (MAPD's) structure the drug portion of the plans based on tiers, prior authorizations and step thereapy protocols. The tiers are typically for the following:Tier 1 - preferred generics - you will see medications that are frequently prescribed in this tier. Most blood pressure and cholesterol medicines fall in this category, but not all.

Tier 2 - generic

Tier 3 - preferred brand

Tier 4 - non-preferred brand - typically these are medications that you will see advertised on TV because they are new.

Tier 5 - specialty medication - medicines used for transplants, etc.

This is just a sample, they can change according to company. The tiers can have copays of $0 or more and can also be percentages based on the cost of the medication which can change as the medicine prices change.

Keep in mind that for 2026, the max out of pocket that you may pay is $2100 for eligible medications.

The $2,100 Out-of-Pocket Cap and Medicare Prescription Payment Plan

The Part D out-of-pocket cap was set at $2,000 when it launched in 2025 and has increased to $2,100 for 2026. Once you spend that much (deductible + copays + coinsurance), your plan pays 100% of covered drugs for the rest of the year.

For Repatha patients, this is the single biggest cost-control change in the program's history. Before 2025, hitting the catastrophic coverage phase still left you paying 5% of drug costs indefinitely, which on a $7,800/year drug was $400+ a year with no endpoint. That's gone.

The companion change is the Medicare Prescription Payment Plan (M3P). Instead of paying $650 the first month and then dropping to lower amounts, you can opt in to spread your annual out-of-pocket costs across the remaining months of the year. If you opt in early and your projected Part D costs are high enough to reach the cap, the program can make costs more predictable. Your actual monthly bill depends on when you enroll and when claims occur, so it won't always divide evenly, but it avoids the front-loaded shock of a $650 pharmacy bill in January. For a deeper look at how the Part D changes affect specialty drug patients, see our full breakdown.

I'm on an expensive specialty medication. Will the 2025 Part D changes help someone in my situation?

Yes, the 2025 Part D changes will help with expensive specialty medications, primarily due to the new $2,000 out-of-pocket (OOP) cap and the option to use a Medicare Prescription Payment Plan. The OOP cap means you won't have to pay more after your total yearly drug costs reach $2,000, and the payment plan allows you to spread your costs out over 12 months instead of paying large amounts at the pharmacy.In 2026, the Max Out of Pocket (MOOP) for covered medications will be $2,100.

It's important to check the cost of your specific medications each year. I highly recommend working with a local, trusted, Medicare agent that can assist with review and can provide you with the estimated cost of your medications for the year and what to expect for out of pocket costs starting with your first fill in January.

You can also visit the Medicare.gov website and enter you medications. However, there have been some inaccuracies with the website this year and may require entering the medication on the site and then cross walking them with the 2026 formulary for your plan.

Ways to Lower Your Repatha Costs

The biggest savings come from picking the right plan during Annual Enrollment, not from manufacturer coupons (most copay cards are blocked for Medicare beneficiaries). Here's what actually works:

- Run a plan comparison every fall. Use the Medicare Plan Finder at Medicare.gov, enter Repatha as a drug, and rank plans by total annual cost. The cheapest plan for a Repatha patient is often not the cheapest plan for a non-Repatha patient. Pay attention to total annual cost (premium + deductible + coinsurance), not just the monthly premium.

- Check Extra Help (LIS) eligibility. The income limits expanded in 2024, and many seniors who didn't qualify before now do. Extra Help can take your specialty drug copay down to a few dollars. In 2025, qualifying individuals paid no more than $4.90 for generic drugs and $12.15 for brand-name drugs.

- Ask about Amgen's AmgenNow program. Amgen now offers Repatha at $239/month through its direct-to-patient program; some Part D plans use this lower-priced version, which reduces your coinsurance proportionally. Even if you qualify for AmgenNow, keep your Part D plan active. It covers your other medications and counts spending toward the $2,100 cap.

- Use the M3P. Spreading your out-of-pocket costs across the year through the Medicare Prescription Payment Plan avoids the front-loaded pharmacy bill shock, especially in January and February when deductibles hit.

- Appeal tier-placement denials. If your doctor documents that a lower-tier alternative won't work, plans can move Repatha to a lower tier for you specifically (a tiering exception).

Be cautious with discount card programs like GoodRx for medications also covered by your Part D plan. Our guide on why GoodRx might cost you more on Medicare explains how using a discount card can prevent spending from counting toward your out-of-pocket cap. For a fuller list of strategies, see our guides on saving money on prescriptions with Medicare and using Extra Help and savings programs to lower Medicare costs.

I'm on a fixed income and struggling to afford my medications. What's this Extra Help program I've heard about for Medicare Part D?

Extra Help, also know as Low Income Subsidy is a program from Social Security that helps eligible individuals with the cost of there Medications. It works with any Medicare Prescription drug plan( stand alone plans and Medicare Advantage plans with Prescription Drug coverage). To qualify in 2025 your income must be below $1,903 a month and you must have less than $9.660 in countable assets.If you qualify you will not pay more than $4.90 for any covered Generic medication or $12.15 for any covered Brand medication. The Extra Help program will cover all cost above these copays. In addition the Extra Help program may cover a portion of your plans monthly premium.

Repatha vs. Praluent and Other Cholesterol Options

Repatha isn't the only PCSK9 inhibitor. Praluent (alirocumab) is the other major one, and the newer drug Leqvio (inclisiran) is a twice-yearly injection administered in a doctor's office, which means it's billed under Part B rather than Part D.

If your Part D coverage for Repatha is poor, ask your cardiologist whether Leqvio is appropriate. Because it's a Part B drug, it doesn't count toward your $2,100 Part D cap, but it's covered at 80% by Original Medicare (or fully by a Medigap plan), and there's no formulary tier to worry about.

Because Repatha is commonly self-administered, it is usually handled through Part D. Do not assume an in-office injection will automatically make it payable under Part B. CMS generally covers drugs under Part B only when they are not usually self-administered, and Repatha's label describes self-injection as the standard method. If you're considering this route, ask the prescribing office and your plan how the claim would be billed before relying on it.

For non-PCSK9 alternatives, bempedoic acid (Nexletol) and ezetimibe sit on much lower tiers and may be appropriate for patients who don't need the aggressive LDL reduction Repatha provides.

Before You Enroll: Plan-Check Checklist

- Repatha is on the plan's formulary

- Which tier Repatha is placed on (Tier 3 vs. Tier 5 makes a big cost difference)

- Whether the plan's deductible applies to that tier

- Prior authorization and step therapy requirements

- Preferred pharmacy networks (costs may differ at preferred vs. standard pharmacies)

- Total estimated annual cost (premium + deductible + coinsurance), not just monthly premium

- Whether your other medications are also covered on the same plan

When to Talk to a Medicare Agent

Licensed agents who work with Repatha patients consistently report that costs vary widely by plan because formularies, tiers, deductibles, and prior authorization rules differ even within the same state. Repatha is one of those drugs where the right plan saves you thousands and the wrong plan costs you thousands.

If you're already on Repatha or your cardiologist is about to start you, an independent Medicare agent can run plan comparisons in your county with Repatha pre-loaded as a drug, so you can see total annual cost (premium + deductible + coinsurance) for every available plan before AEP closes.

You can find a licensed local agent through our directory at Medicare Agents Hub. The service is free, and independent agents represent multiple carriers, so you'll see honest comparisons rather than a pitch for one company's plan.

If you're managing other chronic conditions or expensive medications alongside Repatha, our guide on how Part D covers high-cost conditions like diabetes walks through the same plan-selection math for insulin, which has a similar tier structure and a separate cost cap.

The Bottom Line on Repatha and Medicare

Yes, Medicare Part D covers Repatha in the large majority of plans, but coverage doesn't mean cheap. Expect it on a higher formulary tier with prior authorization and step therapy. Expect to pay $55–$165/month during the initial coverage phase, reach the $2,100 cap within several months depending on your plan's tier and deductible structure, and pay $0 for the rest of the year. The plan you pick during Annual Enrollment matters more than any coupon, and Extra Help can cut your cost dramatically if you qualify.

Pull up Plan Finder during AEP, enter Repatha as a drug, and compare total annual cost across every plan available in your county. That single step does more to lower your Repatha bill than anything else.

Frequently Asked Questions

Does Medicare Part D cover Repatha in 2026?

Yes. The large majority of Part D plans include Repatha on their formulary, though a small number of carriers in certain regions do not. Always confirm coverage in the specific plan you're considering by checking the formulary on Medicare.gov or with a licensed agent.

What tier is Repatha usually on?

It varies by plan. Agents commonly report Repatha on Tier 3 (preferred brand) or Tier 4/5 (specialty). The tier determines whether you pay a flat copay or a percentage of the drug cost, so this matters a lot for your bottom line.

Does Repatha count toward the $2,100 Part D cap?

Yes. Your deductible payments, copays, and coinsurance for Repatha all count toward the annual $2,100 out-of-pocket maximum. Once you reach it, you pay $0 for all covered Part D drugs for the rest of the calendar year.

Can I use a manufacturer coupon with Medicare?

Most manufacturer copay cards are not available to Medicare beneficiaries. However, Amgen's AmgenNow direct-to-patient program offers Repatha at $239/month for eligible cash-pay patients, and some Part D plans negotiate based on that lower price.

Is Repatha Part B or Part D?

Because Repatha is typically self-administered at home, it is covered under Part D. Leqvio is a different cholesterol-lowering injectable given in a doctor's office and is generally billed under Part B.

What should I do if my plan denies Repatha?

File an appeal. Have your prescribing physician submit a letter of medical necessity with clinical documentation of your diagnosis, statin history, and LDL levels. Denials are sometimes overturned with stronger supporting evidence.