Understanding Medicare: The Basics Explained Simply

-

Last Updated July 22, 2026

Written by Alyssa Gonzales

Medicare Broker Licensed in CO, IA, IN & 5 other states

I am a licensed Medicare agent and I help folks turning 65 or already on Medicare understand their options and feel confident about their healthcare choices. Medicare can be confusing, but I believe in explaining things clearly, without jargon or pressure. My mission is to help you make the best decision for your personal situation. Whether that’s Original Medicare, a Medicare Advantage plan, or something in between. When I’m not helping clients, I’m probably sipping coffee, watching college softball, or tinkering with new tech gadgets! Let’s Get Started Shall We!

Part A (Hospital Insurance)

Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. You can think of this like “Room and Board.” Most people don’t pay a premium for Part A because they or their spouse paid Medicare taxes while working. This is sometimes referred to as “premium-free Part A.”

However, while the monthly premium may be free, Part A still comes with costs like deductibles and coinsurance. For example, in 2026, the Part A deductible is $1,736 per benefit period. After that, you may pay daily coinsurance amounts depending on the length of your hospital stay.

Part B (Medical Insurance)

Part B covers outpatient care like doctor visits, preventive services (such as mammos and colonoscopy….yay), mental health services, durable medical equipment (like walkers or wheelchairs, and diabetic equipment), and some home health care. Unlike Part A, most people pay a monthly premium for Part B. In 2026, the standard premium is $202.90, although it may be higher depending on your income.

Part B also comes with an annual deductible ($283 in 2026), and after that, you typically pay 20% of the Medicare-approved amount for services.

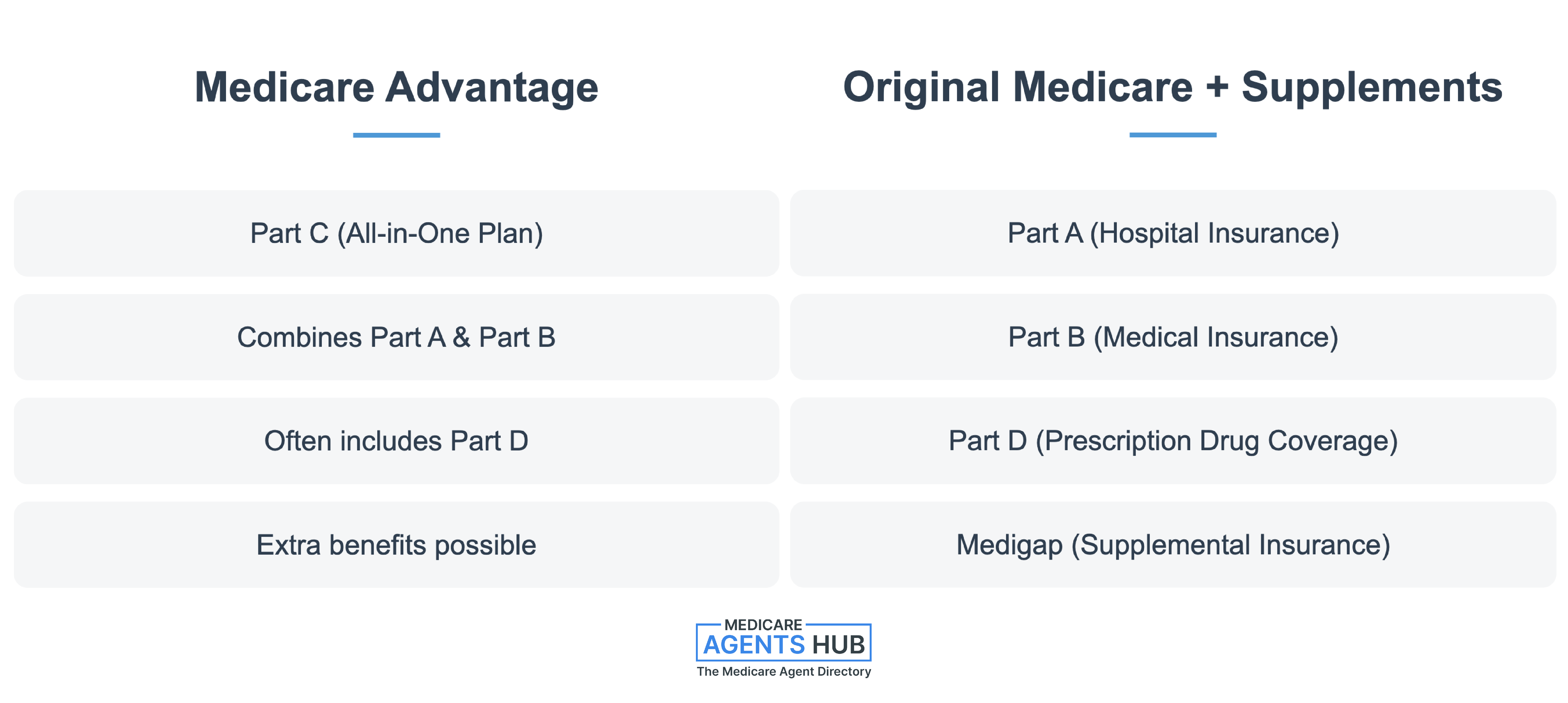

Together, Part A and Part B are known as Original Medicare or Traditional Medicare. While they cover a broad range of services, they don’t cover everything, most notably, they don’t cover prescription drugs, vision, dental, hearing aids, or long-term care. This leads many people to consider additional coverage.

What does Medicare Part B cover? Is it enough?

Well, it’s a solid start.... but it doesn’t cover everything, so most folks end up pairing it with a Medigap plan or Medicare Advantage to fill in the gaps (and avoid surprise bills). Medicare Part B covers doctor visits, outpatient care, preventive services, lab work, durable medical equipment, and things like physical or occupational therapy.Part C (Medicare Advantage)

Part C, also known as Medicare Advantage, is an alternative to Original Medicare. These are private insurance plans approved by Medicare that bundle Part A and Part B coverage and often include additional benefits like dental, vision, hearing, fitness programs, and most importantly—prescription drug coverage (Part D). Medicare Advantage plans are offered by private insurance companies and vary by county and ZIP code. Premiums, copays, provider networks, and out-of-pocket costs can differ significantly between plans, so it’s important to compare carefully.

One key difference between Original Medicare and Medicare Advantage is that Advantage plans typically operate with provider networks think HMOs or PPOs aka Managed Care Plans, so your choice of doctors and hospitals may be more limited.

As a senior, what should I know about the differences between Original Medicare and Medicare Advantage before I choose?

Original Medicare is going to be Part A and Part B as your primary insurance. So that's that red, white, and blue card that says Part A and Part B. Normally, you will have a Medicare supplement, also known as a Medigap plan, as a secondary, sort of like a backup. So they're gonna build your primary, which is original Medicare, then build your secondary. And that's usually the way it goes in terms of creating a holistic hospital and medical plan, a primary and secondary.

Now, because you have original Medicare as your primary, you're not working within the confines of an actual insurance company. You don't have networks. You don't have the things like you would have on the Medicare Advantage side, right? So this is the opposite side of the road. Medicare Advantage does replace original Medicare, so you will be working from a company's HMO or PPO plan. It's just another managed care plan that follows the Medicare rule book.

I can go in-depth about this, but to keep it short, that is the difference. Medicare Advantage, also known as Part C, is a managed care plan that comes in the form of HMO or PPO plans. And then you've got original Medicare, which is Part A and Part B, normally served up with a Medicare supplement as a secondary. Good luck!

Part D (Prescription Drug Coverage)

Part D helps cover the cost of prescription medications and is offered through private insurance companies. If you have Original Medicare and want drug coverage, you’ll need to enroll in a standalone Part D plan. If you choose a Medicare Advantage plan, it may include Part D coverage as part of the package. Each Part D plan has its own list of covered drugs (called a formulary), which is divided into tiers that affect your cost. It’s important to review whether your medications are covered under the plan you’re considering. Part D plans also come with premiums, deductibles, and copays or coinsurance.

If you don’t sign up for Part D when you’re first eligible and you don’t have other creditable drug coverage, you may face a permanent late enrollment penalty.

So I heard something about Medicare drug costs being capped at $2,000 in 2025. Is that really happening or just talk?

Yup ..... it's real talk! Starting January 1, 2025, anyone with a Medicare Part D plan (or Medicare Advantage with drug coverage) will pay no more than $2,000 in out‑of‑pocket costs per calendar year for covered prescriptions this includes deductible, copays, and coinsurance. Once you hit that cap, you’ll have catastrophic coverage and pay $0 for the rest of the year.Supplementing Your Medicare Coverage (Medigap)

Another important part of the Medicare conversation is Medicare Supplement Insurance, also known as Medigap. These are additional policies sold by private companies to help pay some of the costs not covered by Original Medicare, like copayments, coinsurance, and deductibles.

Medigap plans work only with Original Medicare and give you the flexibility to see any doctor who accepts Medicare nationwide. There are different types of Medigap plans (labeled Plan A, Plan G, Plan N, etc.), each offering a standardized set of benefits.

While Medigap plans can help reduce your out-of-pocket costs, you must also enroll in a standalone Part D plan to cover prescriptions.

How the Parts Work Together

Here are a few common combinations people choose:

- Original Medicare (Part A + Part B) + Part D + Medigap: Offers the most flexibility with providers and lowers out-of-pocket costs, but comes with multiple premiums.

- Medicare Advantage (Part C): Offers all-in-one convenience, often with extra benefits, but may require you to stay within a provider network.

It’s essential to evaluate your health needs, budget, and preferences before deciding which path to take.

What Medicare Doesn’t Cover

It’s also important to be aware of what Medicare does not cover, so you can plan accordingly. Original Medicare does not cover:

- Routine dental care

- Vision care (like eye exams or glasses)

- Hearing aids and exams

- Long-term care (such as assisted living or nursing home care beyond short-term rehab)

- Most care received outside of the U.S.

Some Medicare Advantage plans offer coverage for some of these services, so they may be worth exploring if these benefits are important to you. For a closer look at simplifying Medicare for seniors, we have a helpful guide that breaks things down even further.

Tips for Getting Started

- Start early: Begin researching your Medicare options at least 3-6 months before your 65th birthday.

- Make a list: Write down your preferred doctors, prescriptions, and healthcare priorities.

- Use tools: Medicare.gov has a great Plan Finder tool to compare plans in your area.

- Talk to someone: A licensed Medicare agent can help you navigate the options and avoid costly mistakes.

- Separate fact from fiction: There are many misconceptions floating around, so take a look at these common Medicare myths debunked before making any decisions.

Finding Your Best Fit with Medicare Coverage

Understanding Medicare’s structure is the first step in making an informed decision. Each part plays a unique role, and depending on your personal circumstances, you may need one part, several parts, or a combination of parts. Whether you choose Original Medicare, add a Medigap and Part D plan, or go with a Medicare Advantage plan, the key is choosing the coverage that aligns with your healthcare needs, preferences, and financial situation. Taking the time to learn your options now will save you time, money, and stress later on.

About the Author: Alyssa Gonzales of The Gonzales Agency is Medicare Broker Licensed in TN, CO, IA, IN, KS, LA, ME, ND, OR, TX, WA and WI.