Why Your GoodRx Card Might Be Costing You More Than It Saves on Medicare

-

April 26, 2026

A GoodRx card feels like free money. You hand it to the pharmacist, the price drops, and you walk out spending less than your plan's copay. So why do Medicare agents keep telling their clients to stop using it?

Because that "savings" might be quietly preventing you from reaching the one number that actually matters: your $2,100 Part D out-of-pocket cap. Every dollar you spend through a discount card is a dollar that doesn't count toward the threshold where your prescription costs drop to $0 for the rest of the year.

Here's how the math actually works, and when using GoodRx still makes sense.

The $2,100 Cap: How Part D Drug Costs Work in 2026

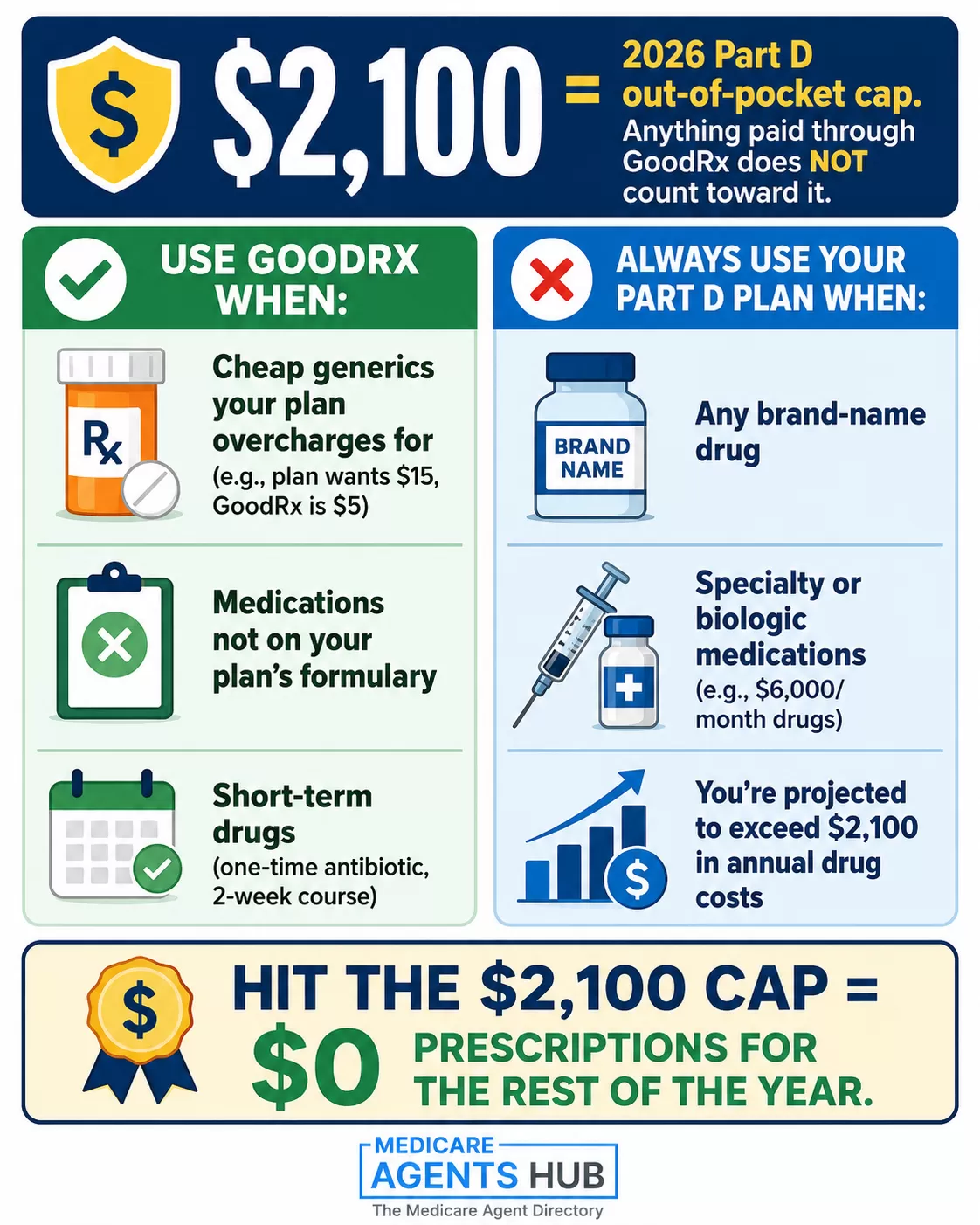

Before 2025, Medicare Part D had no true ceiling on prescription costs. Seniors on expensive medications could spend $7,000 or $8,000 a year, grinding through a coverage gap (the infamous "donut hole") before reaching catastrophic coverage. The Inflation Reduction Act changed that, first capping annual out-of-pocket spending at $2,000 in 2025, then adjusting to $2,100 for 2026.

The mechanics are straightforward. Your Part D deductible, copays, and coinsurance all accumulate toward that $2,100 threshold. Medicare tracks this number (called your True Out-of-Pocket cost, or TrOOP) automatically. Once you hit it, you enter the catastrophic coverage phase and pay $0 for every covered prescription for the rest of the calendar year.

For someone taking only cheap generics, this cap may never come into play. But for anyone on a brand-name medication, a specialty drug, or even a couple of Tier 3 prescriptions, reaching that cap can mean the difference between thousands in annual drug costs and a hard stop at $2,100.

Why is the new $2,000 out-of-pocket maximum for drug costs important?

Because it did away with the Coverge Gap, also called the Donut Hole. Basically the Coverage Gap caused you to pay a lot more for your drugs, for instance after the combined spending on your covered drugs reached a certain dollar amount (several thousand dollars) you then had to pay up to 25% of the drug manufacturers cost of the drug until that combined total reached closer to $8,000, then your copays would go back down, and that was called the catastrophic stage.So, with now having a “cap” called a maximum out of pocket dollar amount, it can save you money, especially if you take a lot of named brand drugs.

In 2026 that cap will be $2,100, it is currently $2,000 in 2025, and Medicare determines that cap amount annually. If you ever reach the “cap” dollar amount (includes the deductible and your copays, but not any of the premiums) you pay zero for your medications, the plan you have has to cover that over and above costs, this is still called the catastrophic stage.

Why Discount Card Purchases Don't Count

Here's the catch that trips up millions of Medicare beneficiaries every year: you cannot use a discount card and your Part D plan at the same time. At the pharmacy counter, it's one or the other. If the pharmacist runs your prescription through GoodRx, SingleCare, or any other discount card, that transaction happens completely outside your Medicare plan.

That means the amount you paid:

- Does not count toward your Part D deductible

- Does not count toward your $2,100 out-of-pocket cap

- Does not move you closer to catastrophic coverage

You saved $8 on today's prescription. But you also pushed back the date when all your prescriptions become free. For someone on multiple medications, that tradeoff can cost hundreds or even thousands over the course of a year.

How do discount cards and resources affect my Medicare Prescription Drug plan?

Good question! Here’s a simple answer. It’s one or the other. If you pay for a prescription using your Medicare Prescription drug plan card Then you work towards Medicare‘s catastrophic coverage (in 2025 that amount is $2K), Meaning that whatever you spend towards covered medication’s, gets you closer to hitting your $2000 out-of-pocket maximum a.k.a. catastrophic coverage. once you hit $2000 out-of-pocket you no longer pay a penny for any covered medication’s. Using your Medicare prescription drug coverage will typically give you a pretty big discount on your medication‘s as it is a pre-negotiated discounted rate between the drug company and the insurance company.If you were to use something like goodRX, you may get a discounted medication but there is no cap to what you may pay throughout the year. Everyone’s situation is different, so for some folks, I’m a huge fan of good RX but for others I strongly encourage sticking to using your Medicare prescription drug plan.

The Tier Problem Nobody Talks About

Part D plans organize drugs into tiers, typically five of them. Tier 1 and Tier 2 are usually generics with low copays ($0 to $10 on many plans). Tiers 3 through 5 cover preferred brands, non-preferred brands, and specialty medications, with progressively higher cost-sharing.

The problem is that the same drug can land on a completely different tier depending on which plan you're on. A medication that's Tier 2 on one plan might be Tier 4 on another. This means your copay for the exact same pill, at the exact same pharmacy, could be $3 on one plan and $95 on another.

This is where discount cards get their foothold. When your plan places a common generic on Tier 3 (triggering a higher copay or a deductible), GoodRx might offer a price that looks much better. But that's a signal to review your Part D plan, not to abandon it for a discount card.

What are some ways to save on prescription drug costs?

Checking your drugs versus available plans is the first thing. Sometimes, different plans will put different medications in higher tiers on their formulary versus another plan. There are some independent tools out there like GoodRX or Optum Perks that allow you to price medicine without running these through any insurance plan at major retailers. If you price your medications and notice 1 or 2 that are causing your price to increase, it might make sense to compare the cost of those medications versus your ability to use one of these tools independently of your insurance.When You Should (and Shouldn't) Use GoodRx

Discount cards aren't always the wrong call. The key is knowing when they help and when they quietly work against you.

When GoodRx Makes Sense

- Cheap generics your plan overcharges for. If your Part D plan places an inexpensive generic (think $4 to $10 retail) on Tier 3 and requires you to pay a deductible first, the discount card price might be $5 while your plan wants $15. On a drug that cheap, the TrOOP impact is minimal.

- Non-covered medications. If a drug isn't on your plan's formulary, it doesn't count toward your cap anyway. A discount card is your best option here.

- Drugs you take short-term. A one-time antibiotic or a two-week course of something won't meaningfully affect your annual TrOOP trajectory.

When You Should Always Use Your Part D Plan

- Any brand-name drug. These are expensive enough that the copay accumulates toward your cap quickly. Using a discount card slows that accumulation.

- Specialty and biologic medications. If you're on a $6,000-per-month medication, you'll blow through the $2,100 cap in your first fill. Every dollar needs to go through your plan.

- When you're on track to hit the cap. If your projected annual drug costs exceed $2,100, every prescription should run through Part D so you reach $0 prescriptions as fast as possible.

What are some ways to save on prescription drug costs?

First, make sure you have the plan providing lowest cost coverage for your formulary needs. Next make sure you use preferred plan pharmacies. Create a price sheet comparing plan co-pays/coinsurance vs Single Care, GoodRx, CostPlusDrugs, or other discount programs. I have one blood pressure med I pay approx. 23% for 90 days versus plan pricing.Note: If you use a non-plan option, have your prescriber note that on your chart for audit purposes.

Some tablets can be split in half, others not - you may be able to pay a similar price for double strength tablet and half it. Just make sure your doctor knows and approves for your needs.

What About Expensive Medications and Biologics?

For beneficiaries taking high-cost medications like biologics for rheumatoid arthritis, cancer treatments, or specialty drugs, the Part D cap is transformative. A drug that costs $6,000 per month means you'll hit the $2,100 ceiling almost immediately. After that first fill, every subsequent fill for the rest of the year costs $0.

One critical detail: this only applies to Part D drugs (prescriptions you pick up at a pharmacy). If your biologic is administered in a doctor's office or infusion center, it's typically billed under Medicare Part B, which has its own cost structure and no equivalent annual cap. Ask your doctor whether your medication can be self-administered at home. That single question could save you thousands.

I have severe rheumatoid arthritis and my biologic medication costs $6,000 per month. How will the 2025 Medicare Part D changes affect someone in my situation?

The biggest change:There is now a $2,000 annual out-of-pocket cap on Part D drugs

That includes:

Deductible

Copays/coinsurance

All covered prescriptions (including expensive biologics)

What this means for YOU:

Before 2025 → you could pay thousands all year long (no true cap)

In 2025 → once you hit $2,000 total for the year… you pay $0 for covered drugs after that

A couple important details:

This only applies to Part D drugs (pharmacy meds)

If your biologic is given in a doctor’s office (Part B), this cap does not apply

The drug must be on your plan’s formulary

Bottom line:

Your costs go from potentially tens of thousands per year → capped at ~$2,000.

For someone in your situation, this is one of the biggest Medicare improvements in years.

The Payment Plan Most People Don't Know About

If the thought of paying $2,100 upfront sounds rough, there's a program specifically designed to smooth it out. The Medicare Prescription Payment Plan (M3P) lets you spread your projected annual drug costs into equal monthly installments. Instead of a $590 deductible hit in January followed by large copays, you'd pay roughly $175 per month, spread evenly across the year.

This is a voluntary program. You have to call your Part D plan and ask to enroll. It doesn't reduce what you owe. It just prevents the front-loaded financial shock that drives some people to reach for a discount card in January when the bills are highest.

If you've been using GoodRx specifically because those first-of-the-year costs feel unmanageable, the M3P program is the better answer. Your money still counts toward the cap, you still reach catastrophic coverage, and you get the predictability of a flat monthly payment.

What to Do Before Your Next Pharmacy Visit

If you've been using a discount card alongside your Part D plan, take these steps:

- Ask the pharmacist to price it both ways. For each medication, get the Part D copay and the discount card price. Write them down.

- Add up your projected annual Part D costs. If the total exceeds $2,100, you should be running everything through your plan. Those copays are buying you $0 prescriptions later.

- Check if you qualify for Extra Help. This federal program can reduce your Part D costs dramatically, and it works with your plan rather than outside it.

- Review your plan during Annual Enrollment. If your current plan places cheap generics on expensive tiers, that's a plan problem. A local Medicare agent can compare formularies across every plan in your area and find one that covers your specific drugs at the lowest cost-sharing.

What are some ways patients can reduce medication costs while on Medicare?

There are a couple ways that people can reduce medication costs while on Medicare. First being if they find their medication to be expensive, they can also ask the pharmacist to run the prescription under good rx, which in some cases is more cost effective than their Part D coverage. Another way is to apply for extra help through social security. I've had quite a few clients qualify for this due to their income. Most of my clients had no idea. The program existed, or they thought they made too much, and they still qualified so it's good to check. Give me a call today if you'd like to see if you qualify.The bottom line: GoodRx and similar discount cards are tools, not strategies. They save money on individual prescriptions. But Medicare Part D is a system designed to protect you over an entire year. If you're pulling prescriptions out of that system to save $5 or $10 at a time, you may be paying for it later when you never reach the catastrophic coverage phase that would have made every prescription free.

Talk to your pharmacist. Talk to a Medicare agent who understands drug plans. And run the numbers before you hand over that discount card.