How Medicare Part B Really Works

Medicare Part B is medical insurance. It helps pay for doctor services, outpatient care, preventive services, and certain medical supplies. While Part B is a critical part of Medicare coverage, it does not work like employer insurance—and misunderstanding it is one of the biggest reasons people end up with unexpected medical bills.

Let’s walk through how it actually works.

What is one of the the most common misconceptions people have about Medicare?

I would have to say the most common misconception for Medicare is that the open enrollment period at the end of the year applies to Medicare Supplements.It is very shocking to some that they may not get to choose another carrier "EVER" because of their health issues.

William Gray

Contact me.

What Medicare Part B Does Cover

Medicare Part B generally covers medically necessary services such as:

- Doctor visits (primary care physicians and specialists)

- Outpatient medical services

- Preventive care (annual wellness visits, screenings, lab work)

- Durable medical equipment (walkers, wheelchairs, oxygen, etc.)

- Outpatient mental health services

- Ambulance services (when medically necessary)

- Some home health services

- Certain hospital services when you are considered outpatient or under observation status

Important note: Medicare Part B is not limited to a doctor’s office. Depending on how your care is billed, Part B can apply even while you are physically in the hospital.

What Medicare Part B Does Not Cover

Medicare Part B does not cover everything. Common exclusions include:

- Prescription drugs you take at home (covered under Part D)

- Routine dental care (cleanings, fillings, dentures)

- Routine vision exams and eyeglasses (though Part B does cover medically necessary eye care such as cataract surgery)

- Hearing exams and hearing aids

- Long-term custodial care (such as nursing home stays)

- Cosmetic procedures (note: medically necessary dermatology is covered under Part B)

- Most care received outside the United States

Because of these gaps, many people choose to add a Medigap plan or a Medicare Advantage plan.

The Medicare Part B Deductible

Before Medicare starts paying its share, you must meet the annual Medicare Part B deductible, which is $283 this year.

- You pay 100% of Medicare-approved services until the deductible is met

- The deductible resets every calendar year

Once the deductible is satisfied, Medicare begins sharing costs with you.

The 80/20 Coinsurance Rule

After the deductible is met:

- Medicare pays 80%

- You pay 20%

This 20% coinsurance applies to most Part B services, including doctor visits, outpatient procedures, imaging, and lab work.

There is no maximum out-of-pocket limit with Original Medicare alone, meaning that 20% responsibility can continue indefinitely.

I picked the plan with the lowest premium, but now every doctor visit feels like a surprise bill. Should I have gone with a higher premium instead?

You have not provided enough information.If you have original Medicare and chose a plan like the HDG - or the N plan or K / L there will be copays and deductibles. Medicare will pay after the deductible of 257$ 80/20. These plans all have different variations of copays so it will likely cost you different copays when you go to the dr.

If you chose a Medicare Advantage plan you have replaced original Medicare with this plan and therefore you will have to read that plans summary of benefits to determine your copays and out of pocket costs.

You can reach out to me if you need help understanding what you have and what costs you can expect.

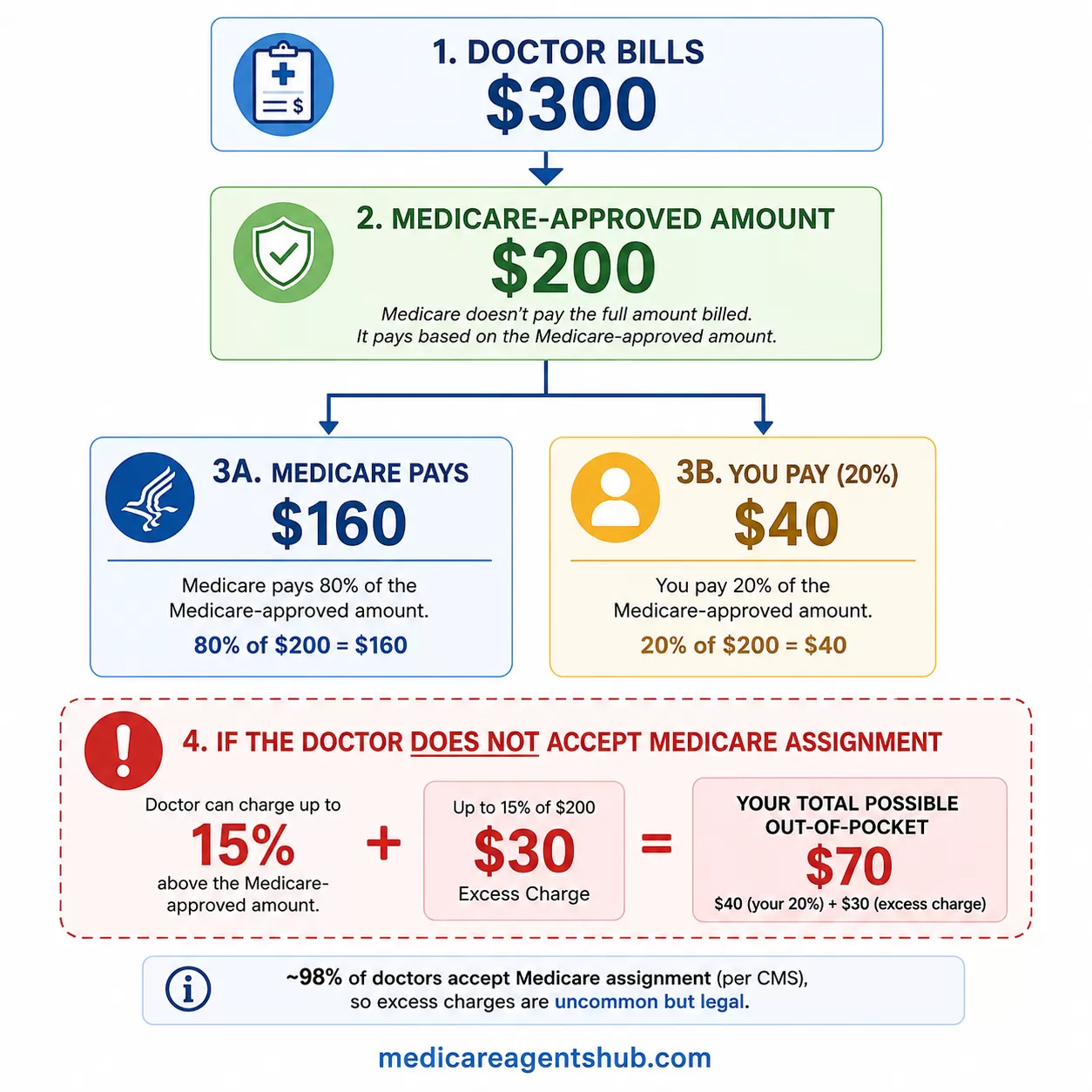

Billed Amount vs. Medicare-Approved Amount

This is one of the most misunderstood parts of Medicare.

- The billed amount is what a provider charges

- The Medicare-approved amount is what Medicare says the service is worth

Medicare bases payment only on the approved amount—not what the provider bills.

Example:

- Doctor bills: $300

- Medicare-approved amount: $200

- Medicare pays 80% of $200 = $160

- You pay 20% of $200 = $40

The difference between what was billed and what Medicare approved is where additional costs may come into play.

What Are Medicare Excess Charges?

Some doctors do not accept Medicare assignment.

When this happens, Medicare allows the provider to bill up to 15% more than the Medicare-approved amount. This additional amount is known as a Medicare excess charge.

According to CMS, approximately 98% of doctors nationwide accept Medicare assignment, meaning they agree to Medicare’s approved amount and do not charge excess charges. While excess charges are relatively uncommon, they are still allowed under Medicare rules and can apply in certain situations.

Key points to understand:

- Excess charges are legal under Medicare rules

- Medicare does not pay excess charges

- You are responsible for them unless you have coverage that pays them

Example:

- Medicare-approved amount: $200

- Maximum excess charge (15%): $30

- You could owe:

- $40 (20% coinsurance)

- Plus $30 (excess charge)

- Total out of pocket: $70

I'm on Medigap Plan G, and I'm curious how my upcoming knee replacement surgery will be billed. Does the plan cover it all after my deductible?

Medicare plan G is the most comprehensive Medicare Supplement available today.Once you meet the 257$ deductible for part B your medicare supplement will cover your remaining cost of care at 100%.

This is assuming you are on the G and not the HDG (the HDG has a 2870) then its 100% covered.

Why You May See Part B Bills from a Hospital

You may receive Part B charges even when services are provided in a hospital setting. This commonly happens with:

- Emergency room visits

- Observation stays

- Outpatient procedures

- Lab work, imaging, and physician services provided during a hospital visit

In these situations, Medicare Part B applies based on how the service is classified, not the building you are in.

After a surgery, should I expect out-of-pocket costs?

You have a bunch of variables.Do you have Original Medicare A&B?

Do you have Orginal Medicare and a Supplement?

* No, then yes you can expect to pay 20% of the entire amount approved by medicare and the part B deductible assuming you were not hospitalized overnight.

* Yes, What supplement do you Have?

A, B, D, G, J, K, L, M, N ( some or no longer available.

* Does your plan have a deductible? HDG/ HDF

Are you on a Medicare Advantage?

If so forget everything i just said and look at your ANOC. There will definatley be out of pocket costs.

Honestly it's best to speak to a Medicare Speciliast usually the Broker who sold you your plan.

William Gray

"The Medicare Dude" Daytona Beach Fl, 32117

Why Understanding These Gaps Matters

Medicare Part B provides essential medical coverage—but it leaves gaps:

- A $283 annual deductible

- Ongoing 20% coinsurance with no out-of-pocket cap

- Potential excess charges (even if uncommon)

- No routine dental, vision, hearing, or prescription drug coverage

Understanding these gaps is critical to avoiding surprise medical bills and choosing the right supplemental coverage.

About the Author: William Gray, otherwise known as “The Medicare Dude,” has nearly 30 years of experience helping individuals understand Medicare and make informed, confident coverage decisions. His focus is simple: explain Medicare in plain English and help people avoid costly mistakes.