Medicare Decisions in an Age of Confusion: How Beneficiaries Can Make Better Coverage Choices

For millions of Americans approaching retirement age, few decisions feel as overwhelming as choosing Medicare coverage. Television advertisements, mailers, social media promotions, friends, family opinions, and countless insurance options can create confusion long before a person enrolls.

The challenge is not simply choosing coverage. It is understanding what Medicare actually is, what it is not, and how different options may impact healthcare access, finances, and long-term planning.

As enrollment into Medicare continues to grow, understanding the fundamentals has become increasingly important.

Understanding Medicare: More Than a Single Program

Many people mistakenly believe Medicare is one insurance plan. In reality, Medicare is a collection of different components that work together.

Original Medicare generally consists of:

- Part A: Hospital insurance

- Part B: Medical insurance

Beyond these components, beneficiaries may add prescription coverage, supplemental insurance, or choose private plan alternatives.

Because Medicare can be assembled in multiple ways, two people of the same age may have dramatically different healthcare experiences depending on the choices they make.

This complexity is one reason many beneficiaries report feeling uncertain during enrollment periods.

Why Medicare Choices Feel Difficult

One major source of confusion is that Medicare decisions frequently involve tradeoffs.

Some individuals prioritize:

- Lower monthly costs

- Predictable expenses

- Maximum provider flexibility

- Prescription coverage

- Additional benefits

- Travel considerations

- Long-term healthcare risks

These priorities do not always align.

For example, lower monthly premiums may sometimes result in higher out-of-pocket exposure later. Conversely, higher monthly expenses may provide greater predictability or broader provider access.

The "best" Medicare choice often depends less on the product itself and more on the person selecting it.

The Growing Importance of Healthcare Planning

Modern retirement planning increasingly includes healthcare strategy.

Individuals may spend years planning:

- Investments

- Retirement income

- Housing

- Estate planning

Yet many spend comparatively little time preparing for healthcare costs in retirement.

Healthcare planning involves asking practical questions:

- Do my doctors participate?

- What prescriptions do I take?

- How often do I travel?

- What happens if my health changes?

- How much financial risk am I comfortable assuming?

These questions become increasingly important because healthcare needs rarely remain static.

A healthy sixty-five-year-old may have very different needs ten years later.

Common Misconceptions About Medicare

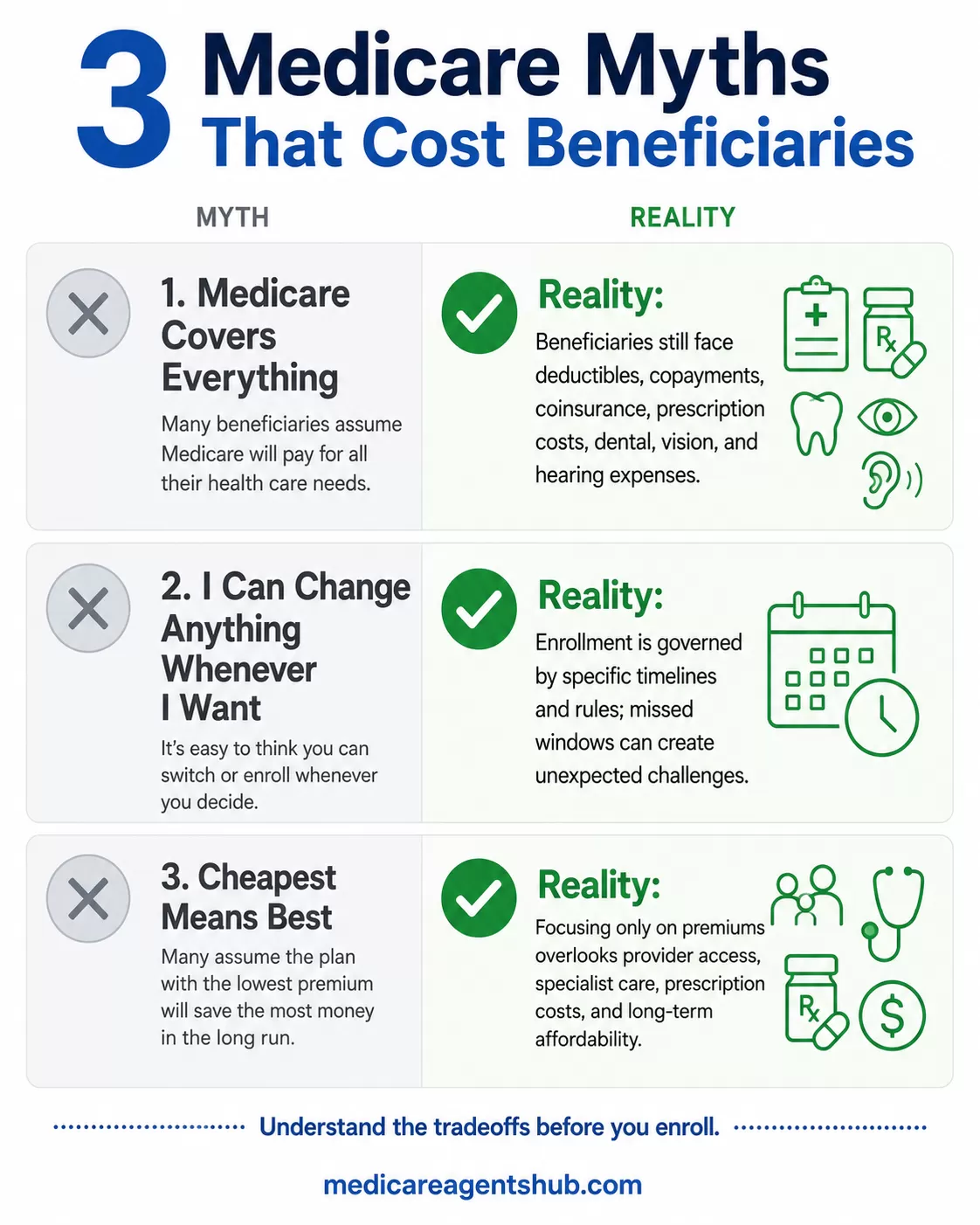

"Medicare Covers Everything"

Medicare provides significant protection but generally does not cover every healthcare expense.

Beneficiaries may still encounter:

- Deductibles

- Copayments

- Coinsurance

- Prescription costs

- Dental expenses

- Vision expenses

- Hearing-related costs

Understanding these gaps helps prevent financial surprises. Knowing what Original Medicare does not cover is an important first step.

"I Can Change Anything Whenever I Want"

Enrollment opportunities exist, but they are often governed by specific timelines and rules.

Waiting too long to make changes or assuming changes can occur anytime may create unexpected challenges. Understanding Medicare enrollment periods and key dates can help avoid missed windows.

I'm worried about choosing the wrong plan and being stuck with it. How often can I change my Medicare coverage?

You may have more opportunities to change your Medicare coverage than you realize, depending on the type of coverage you have and your situation.If You Have Medicare Advantage (Part C):

You can usually make changes during these periods:

* Annual Enrollment Period (October 15 – December 7):

You can join, switch, or leave a Medicare Advantage plan or change your prescription drug coverage. Changes generally take effect January 1.

* Medicare Advantage Open Enrollment (January 1 – March 31):

If you already have a Medicare Advantage plan, you can switch to another Medicare Advantage plan or return to Original Medicare (and possibly add a prescription drug plan).

If You Have Original Medicare:

* You can generally join, switch, or drop a prescription drug plan during the Annual Enrollment Period.

* You may also have opportunities to change coverage if you qualify for certain special circumstances.

Special Enrollment Periods (SEPs)

You may qualify for additional enrollment opportunities if certain life events happen, such as:

* Moving to a new area

* Losing employer coverage

* Qualifying for Extra Help or Medicaid

* Moving into or out of a nursing facility

* Other qualifying circumstances

Important Note About Medicare Supplement (Medigap):

If you want to switch your Medicare Supplement plan later, you may have to answer health questions depending on your state and situation, so timing can matter.

Simple Answer:

You are usually not permanently “stuck” with a Medicare plan, but when and how you can change depends on your current coverage and circumstances.

"Cheapest Means Best"

Focusing exclusively on premiums can overlook important considerations such as provider access, specialist care, prescription costs, and long-term affordability.

The lowest-cost option upfront does not always produce the lowest overall healthcare spending.

The Role of Insurance Professionals

Insurance professionals often serve an important educational role.

Many beneficiaries rely on agents or advisors because Medicare rules, enrollment periods, and plan structures can feel overwhelming.

However, beneficiaries should remain active participants in their decisions.

Questions consumers should consider asking include:

- Why are you recommending this option?

- What are the disadvantages?

- What alternatives exist?

- What happens if my health changes?

- How will this impact my future flexibility?

Healthcare decisions typically produce better outcomes when beneficiaries understand both advantages and tradeoffs.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

This is a fair question, and the answer is: sometimes there are legitimate reasons, and sometimes financial incentives influence recommendations. You should not automatically be skeptical — but you should ask questions.Why Some Agents Recommend Medicare Advantage

Some agents recommend Medicare Advantage because:

* Lower upfront cost: Many plans have low or $0 monthly premiums beyond your Part B premium

* Extra benefits: May include dental, vision, hearing, fitness benefits, transportation, etc.

* Maximum out-of-pocket protection: Original Medicare by itself does not have a spending cap

* Local network options: Some plans work well in certain areas

Why Some Agents Recommend Medigap

Many agents recommend Medigap because:

* Greater flexibility to see providers that accept Medicare nationwide

* Less concern about networks and referrals (depending on plan type)

* More predictable healthcare costs

* Often preferred by people who travel frequently or want broader access

Agents can be compensated differently depending on the product and carrier. That does not automatically mean bad advice, but it does mean you should ask:

✅ “Why are you recommending this plan specifically?”

✅ “What are the disadvantages?”

✅ “What happens if my health changes later?”

✅ “Show me alternative options.”

Be cautious if someone:

* Pressures you to enroll immediately

* Says “everyone should get this plan”

* Avoids discussing disadvantages

* Refuses to compare alternatives

* Talks mostly about benefits but not costs, networks, or risks

The Better Question Is: “Which option best fits my health needs, budget, travel habits, doctors, prescriptions, and risk tolerance?”

For example:

* Someone healthy who wants lower premiums may prefer Medicare Advantage

* Someone who wants maximum provider flexibility may prefer Medigap

* Someone who travels frequently may value nationwide access differently

Beware of agents who start with product selections instead of a needs analysis

Why Medicare Conversations Are Changing

The Medicare landscape continues evolving.

Several factors contribute to increasing complexity:

- Rising healthcare costs

- Longer life expectancy

- Greater plan variety

- Changing provider networks

- More prescription options

- Increased consumer advertising

As these factors evolve, education becomes increasingly valuable.

Consumers who understand basic Medicare principles often feel more confident navigating future changes.

Practical Steps for Better Medicare Decisions

1. Start Earlier Than You Think

Waiting until enrollment deadlines approach often increases stress and reduces preparation time.

2. Review Coverage Annually

Healthcare needs, prescriptions, and provider participation may change. Annual plan reviews help ensure your coverage still fits.

3. Focus on Total Costs

Monthly premiums represent only one portion of healthcare spending.

4. Verify Providers and Prescriptions

Coverage that appears attractive on paper may work differently in practice.

5. Ask Questions

Consumers should never feel uncomfortable requesting explanations.

Understanding coverage is more important than enrolling quickly.

Final Thoughts

Medicare decisions rarely involve perfect answers.

Instead, beneficiaries are often choosing among different sets of tradeoffs involving cost, access, flexibility, and future uncertainty.

The goal should not necessarily be finding a "perfect" plan.

The goal is making informed decisions based on personal needs, financial circumstances, and healthcare priorities.

As Medicare continues evolving, education remains one of the most valuable tools available to beneficiaries.

About the Author: Hudson Albert is an insurance sales agent and coach with more than 20 years of experience in the insurance industry, specializing in Medicare and final expense insurance. He is also a veteran of the United States Marine Corps and has spent years helping individuals better understand insurance concepts and coverage decisions.