Medicare is Your Insurance Vehicle

As we know, Medicare is a federal program that pays for healthcare for persons over the age of 65 and for disabilities under the age of 65 or anybody who has been diagnosed with permanent kidney failure. However, Medicare does not pay for long term care services, it helps for short term hospitalization and skilled nursing services, as well as hospice care and home health care. Let's face it, Medicare is an insurance resource we paid for in our employment years. Though it has financial limitations in funding our health needs, it could cover intrinsic needs for skilled nursing facilities and services such as for the first 20 days financial deductible for $0.00 and from the 21st day to the 100th day of hospital confinement, coinsurance is $217.00 per day. Imagine how it will look like without Medicare insurance, a semi-private room now costs $315.00 per day, and a private room at $370.00 per day.

Social Security and FICA: How Medicare Gets Funded

Social Security benefits program is thought by many to be a complicated and confusing matter. Well, it is not really the way it seems. Remember the FICA (Federal Insurance Contribution Act), an entry into the W2 pay stub indicating your contribution to Social Security and Medicaid. And for the self-employed, remember your form 1040 SE (Self Employment form), where taxes are paid in full being for business owners, being yourself as your own boss. These tax payments are pooled into a trust fund invested in various investment vehicles that make the fund grow. The FICA is the law allowing Social Security taxes, including Medicare taxes, to be deducted from the paystubs.

Can you get Medicare without Social Security?

Yes, you can absolutely get Medicare without receiving Social Security benefits. In fact, many people delay Social Security until age 70 to maximize their monthly checks while still enrolling in Medicare at 65 to ensure they have health coverage.Who Runs Medicare?

The Health Care Financing Administration, now known as Center for Medicare and Medicaid Services or CMS, part of the United States Department of Health and Human Service, administers Medicare. Medicare is the nation's largest health insurance program, covering over 68.5 million individuals. There are three parts to Medicare: Hospital stays and Skilled Nursing facilities and services (Part A – Hospital Insurance), Doctor visits and outpatient care (Part B – Medical Insurance), and medicines (Part D – Prescription Drug Coverage Insurance). You might wonder if there is a 'Part C'? Well, its called Medicare Advantage, it is an 'all-in-one' alternative to Medicare 'the Original Medicare'.

Medicare Advantage: The Part C Alternative

When you join a Part C plan, you still have Medicare, but you get your Part A (Hospital Insurance) and Part B (Medical Insurance) coverage from the Medicare Advantage Plan, not Original Medicare. Instead of the government managing your care, you choose a private insurance company (like UnitedHealthcare, Humana, or Aetna) to provide your Medicare benefits. The government pays these companies a fixed amount to cover your care (recall your FICA), and the companies, in turn, manage your doctors, tests, and hospital visits.

Medicare Advantage hook clients from the Original Medicare Insurance through extra coverage, such as Vision (exams and glasses), Dental (cleanings and X-rays), Hearing (exams and hearing aids), Fitness memberships (like Silver Sneakers) and over the counter (OTC) allowances for pharmacy items.

Can I be turned down for a Medicare Advantage plan because of my health?

Under the Affordable Care Act and subsequent updates, Medicare Advantage plans are guaranteed issue. They cannot deny you coverage based on your medical history. They cannot charge you a higher premium because you are sick. They must cover your pre-existing conditions from day one (no waiting periods).Part D: Prescription Drug Coverage Gets a Makeover

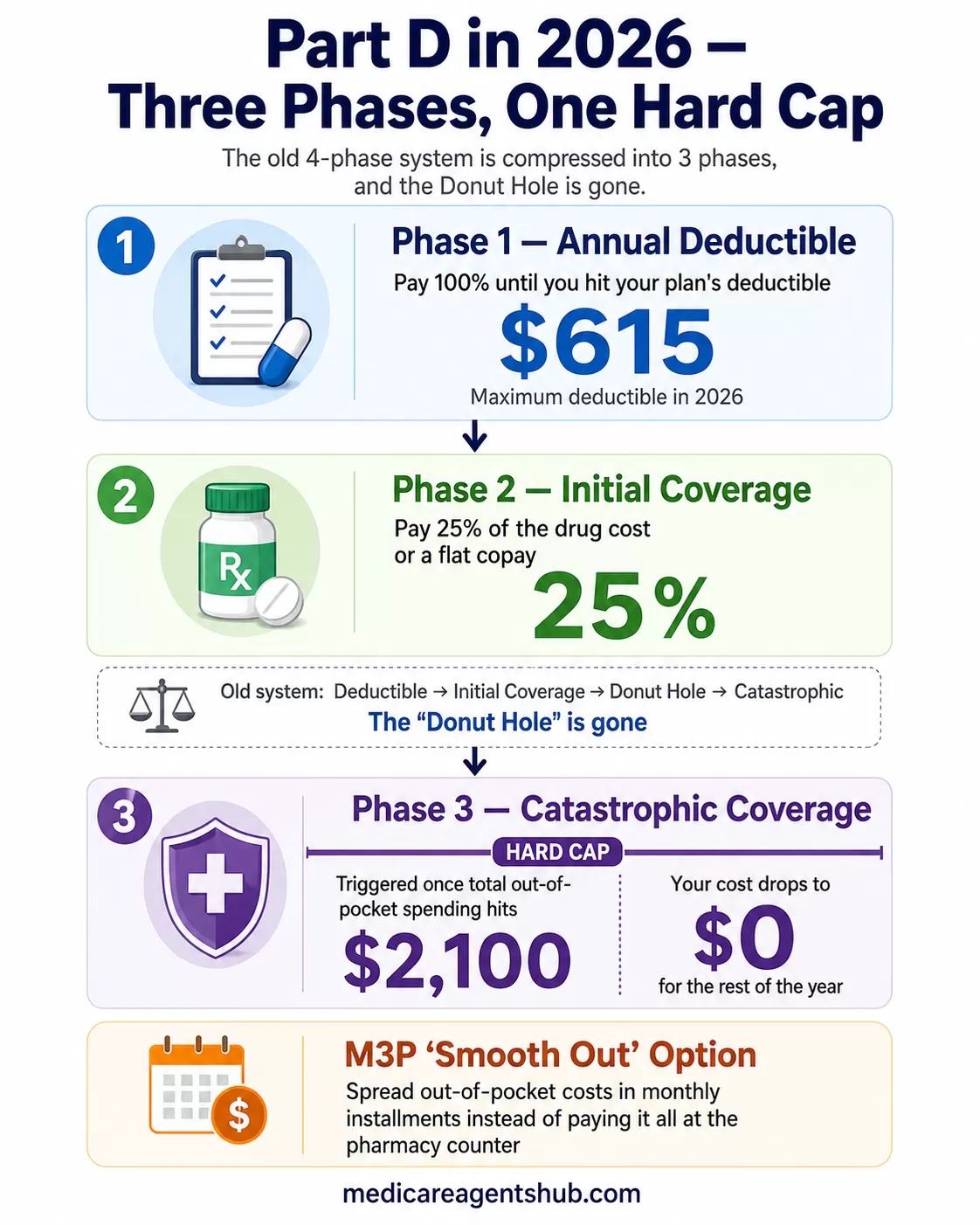

What happened to Part D – Prescription Drug Coverage Insurance? "Part D" hasn't gone anywhere, but it just underwent the most significant makeover in its 20-year history. If you remember the old "Donut Hole" (the coverage gap where you suddenly had to pay more for your meds), that is officially a thing of the past. As of 2026, the program has been simplified and capped to protect seniors from high drug costs. Here are the three major changes:

1. The $2,100 Out-of-Pocket Cap

This is the "headline" change. In the past, there was essentially no limit to how much a senior could spend on expensive medications. But now: Once you spend $2,100 out-of-pocket on covered drugs in 2026, you hit the "Catastrophic Phase." The result: For the rest of the year, your cost-sharing drops to $0. You pay nothing for your covered prescriptions for the remainder of the calendar year.

2. Death of the "Donut Hole"

The confusing four-phase system (Deductible → Initial Coverage → Donut Hole → Catastrophic) has been compressed into just three phases:

- Annual Deductible: You pay 100% until you hit your plan's deductible (maximum $615 in 2026).

- Initial Coverage: You pay 25% of the drug cost (or a flat copay).

- Catastrophic Coverage: Triggered once your total out-of-pocket spending hits $2,100. Your cost is $0.

3. The "Smooth Out" Option (M3P)

The government introduced the Medicare Prescription Payment Plan (M3P). If you have a very expensive prescription in January, you no longer must pay the full $2,100 at the pharmacy counter all at once. You can opt-in to "smooth" those costs, allowing you to pay your out-of-pocket expenses in monthly installments throughout the year, like a utility bill.

The Bottom Line: Part D is still here, but it's much more "insurance-like" now, with a hard ceiling on how much it can cost you.

How do I compare Part D plans to minimize costs for a mix of generic and specialty drugs?

Ask about the Medicare Prescription Payment Plan. This is a new feature that allows you to spread your out-of-pocket costs (like that $2,100 cap) into monthly installments throughout the year instead of paying a massive sum the first time you fill your specialty drug in January.Make the Most of Your Medicare

These are the ABC of Medicare, and I hope you've learned something from this newsletter. Remember, Medicare is an insurance vehicle you paid for during your employment years. Thus, make most out of it in life.