The Importance of Annual Medicare Plan Reviews

-

Last Updated July 22, 2026

Medicare beneficiaries have the crucial task of evaluating their Medicare plans annually, particularly during the Annual Enrollment Period (AEP) from October 15 to December 7. This period is the prime opportunity to review and adjust your Medicare coverage to better suit your healthcare needs and financial situation. Here’s an in-depth look at why annual reviews are essential and how to effectively conduct them.

Key Takeaways

- Read your Annual Notice of Change (ANOC) as soon as it arrives in September.

- Confirm your prescriptions are still on the formulary and your doctors are still in-network.

- Compare plans using the Medicare Plan Finder every year, even if you’re happy with your current coverage.

- Make changes between October 15 and December 7 for coverage that starts January 1.

- Talk to a licensed agent if any part of the process feels overwhelming.

Reasons to Review Your Medicare Coverage Every Year

1. Plan Premiums and Coverage Can Change

Every year, Medicare plans, including Medicare Advantage and Prescription Drug Plans, undergo changes in premiums, coverage, and out-of-pocket costs. These adjustments can significantly impact your budget and access to healthcare services. A plan that was affordable last year might have increased costs this year, or vice versa. By reviewing your plan, you ensure it still fits your budget and healthcare needs. For instance, a plan that once covered all your prescriptions might now exclude some, leading to unexpected expenses.

2. Personal Health Changes

Your healthcare needs can evolve over time due to new diagnoses, changes in medication, or the need for additional healthcare services. An annual review of your Medicare plan ensures that it still meets your current health needs. For example, if you’ve been diagnosed with a chronic condition that requires regular specialist visits, you’ll need a plan that provides comprehensive coverage for specialist care and any associated treatments or medications. If you’re an adult child reviewing plans on behalf of a parent, having the right questions ready for your Medicare agent can make the review process more productive.

I started taking a new prescription this year. Do I need to change my Medicare plan?

Starting a new prescription doesn’t always mean you have to change your Medicare plan—but it’s a good reason to review your coverage.• Every Medicare Advantage and Part D drug plan has its own formulary (list of covered drugs).

• If your new prescription is covered and affordable under your current plan, you may not need to make any changes.

• If it’s not covered, requires high copays, or has restrictions (like prior authorization), then reviewing other plan options could save you money.

3. Access to New Benefits

Each year, new Medicare plans and benefits are introduced, which might offer better coverage or more benefits than your current plan. For example, some Medicare Advantage plans now include additional services like dental, vision, and hearing coverage, which are not typically covered by Original Medicare. Medigap (Medicare Supplement) plans don’t add these extras either — they only help pay for costs that Original Medicare already covers. Reviewing your options annually can help you access benefits that were previously unavailable to you, ensuring comprehensive coverage.

Do Medicare Advantage plans include dental coverage?

Most, but not all, Medicare Advantage Plans offer dental coverage. When you are signing up for a plan make sure to ask if dental coverage is included and ask for the coverage amount. This will be available to you in the plan's Summary of Benefits.Keep in mind that since Advantage Plans are run by private companies, the dental benefits will not be the same. Some may have different coverage dollar amounts. Some plans may offer preventative services like two cleanings per year, x-rays, orl exams and flouride treatments. Others may offer additional coverage through a dental rider. This means that for an additional fee you can purchase more coverage for dental work.

4. Network Changes

If you have a Medicare Advantage plan, the network of doctors, hospitals, and pharmacies can change each year. This can impact your access to preferred healthcare providers and facilities. It’s crucial to ensure that your current healthcare providers remain in-network to avoid higher out-of-pocket costs and maintain continuity of care. Switching plans might be necessary if your preferred providers are no longer covered. Compare Medicare Advantage vs. Medicare Supplement to understand your options under your existing plan.

Understanding Medicare Advantage Plan Annual Reviews

If you’re on a Medicare Advantage plan, the yearly review carries extra weight. Your plan’s provider network, drug formulary, supplemental benefits (dental, vision, hearing, over-the-counter allowances), and Maximum Out-of-Pocket limit can all shift from one plan year to the next. The Annual Notice of Change you receive in September lists these adjustments, but reading it alongside the current Evidence of Coverage is the only way to see the full picture. If your primary care doctor drops out of network in January, or your Tier 2 drugs jump to Tier 4, waiting until spring to notice will cost you real money. Reviewing your Advantage plan every AEP — not just when something feels wrong — is the difference between staying ahead of these changes and reacting to them.

5. Potential Cost Savings

Reviewing your Medicare plan annually can lead to significant cost savings. You might discover a plan that offers the same or better coverage at a lower cost. Medicare choice errors, such as selecting inappropriate coverages or missing enrollment deadlines, can be unnecessarily costly. For instance, economists have found that Medicare beneficiaries often overspend by more than $1,000 per year due to suboptimal plan choices. By taking the time to review your options, you can avoid these errors and save money.

Questions to Consider During Your Review

To effectively review your Medicare plan, consider the following questions:

- Has your medical status changed in the past year? Assess any new health conditions, treatments, or prescriptions you need.

- Have your co-pays or premiums changed? Compare your current out-of-pocket costs with other available plans.

- Are your prescriptions still covered? Check if your medications are still included in your plan’s formulary.

- Have you moved or are you planning to move? Ensure your plan covers services in your new location.

- Does your plan still meet your needs? Evaluate whether your current plan still aligns with your healthcare and financial needs.

The Process of Reviewing and Changing Your Medicare Plan

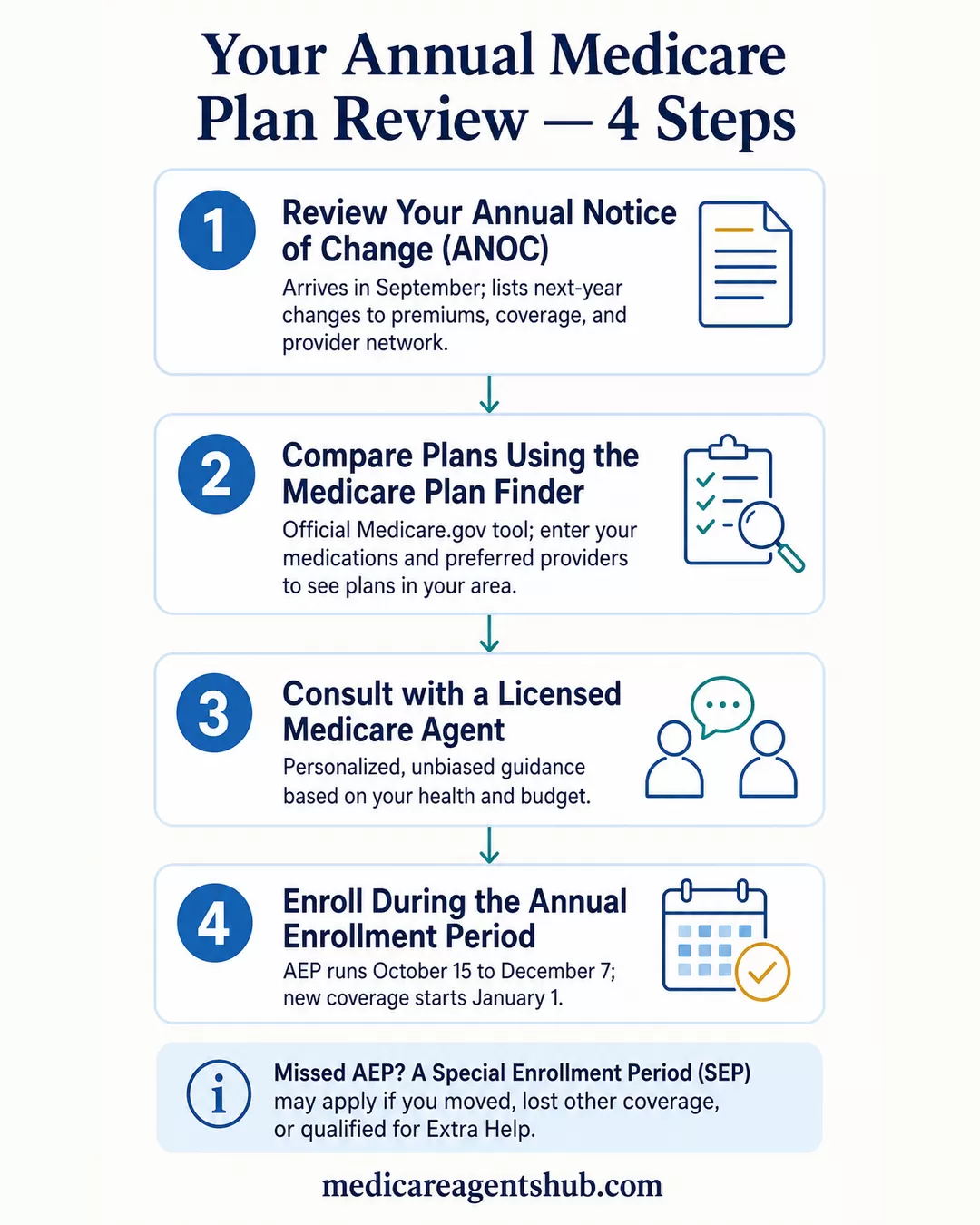

Step 1: Review Your Annual Notice of Change (ANOC)

Before the AEP, you will receive an ANOC from your Medicare plan. This document outlines any changes to your current plan for the upcoming year, including alterations in premiums, coverage, and provider networks. Learn more about what an ANOC is and why it matters. Reviewing this document carefully is the first step in understanding how your plan will change and identifying any areas of concern.

Step 2: Compare Plans Using the Medicare Plan Finder

The Medicare Plan Finder tool on the official Medicare website is an invaluable resource for comparing different plans available in your area. By entering your specific details, such as your medications and preferred providers, you can find plans that best meet your needs. Consider the coverage, costs, and network of providers for each plan to ensure you choose the best option.

Step 3: Consult with a Licensed Medicare Agent

A licensed Medicare agent can provide personalized advice based on your unique healthcare needs and financial situation. They can help you understand your options and guide you through the process of selecting a new plan if necessary. Licensed agents meet rigorous standards to provide unbiased and comprehensive Medicare information, ensuring you make informed decisions.

Step 4: Enroll During the Annual Enrollment Period

If you decide to change your plan, make sure to do so during the AEP from October 15 to December 7. This is the period when you can make changes that will take effect on January 1 of the following year. During this time, you can switch from Original Medicare to a Medicare Advantage plan, change from one Medicare Advantage plan to another, join a Medicare Part D drug plan, or drop your Medicare drug coverage entirely.

Special Enrollment Periods (SEPs)

In addition to the AEP, there are Special Enrollment Periods (SEPs) that allow you to make changes to your Medicare plan outside of the regular enrollment periods. SEPs can be triggered by specific life events such as moving to a new location, losing other insurance coverage, or qualifying for Extra Help with Medicare prescription drug costs. Understanding SEPs can provide additional opportunities to adjust your coverage as needed.

Common Mistakes and How to Avoid Them

1. Ignoring the Annual Notice of Change

One of the most common mistakes beneficiaries make is ignoring the ANOC. This document contains vital information about changes to your plan that could affect your coverage and costs. Make it a priority to review the ANOC as soon as you receive it.

2. Not Comparing Plans

Another common mistake is sticking with the same plan without comparing it to other available options. Plans can vary significantly in terms of coverage, costs, and provider networks. By comparing plans annually, you can ensure you’re getting the best value and coverage for your needs.

3. Overlooking Prescription Drug Coverage

Prescription drug coverage can change each year, and failing to review your Part D or Medicare Advantage plan’s formulary can result in higher costs or lack of coverage for necessary medications. Make sure to review the list of covered drugs each year and consider alternative plans if your medications are no longer covered.

4. Missing Enrollment Deadlines

Failing to make changes during the AEP or a relevant SEP can result in being stuck with a suboptimal plan for the following year. Mark your calendar for important dates and set reminders to review and make any necessary changes to your Medicare coverage.

5. Not Seeking Professional Help

Navigating Medicare can be complex, and not seeking professional help can lead to costly mistakes. Licensed Medicare agents can provide valuable guidance and help you understand your options. Their expertise can ensure you make informed decisions that align with your healthcare needs and financial situation.

Case Study: The High Cost of Medicare Choice Errors

Ari Parker, a Medicare expert, provides a real-world example in his book “It's Not That Complicated: The Three Medicare Decisions to Protect Your Health and Money.” A 72-year-old woman named Diane attended a Medicare presentation, assuming she could delay Medicare enrollment because she had employer-provided coverage. However, she learned that because her employer had fewer than 20 employees, she wasn’t eligible for a Special Enrollment Period. This mistake resulted in a 70% late enrollment penalty on her Medicare Part B premium for the rest of her life. Per Medicare.gov’s guidance on avoiding penalties, the Part B late enrollment penalty adds 10% to your premium for every full 12-month period you were eligible but didn’t enroll — and it sticks with you for life. This cautionary tale highlights the importance of understanding Medicare rules and reviewing your plan annually to avoid costly errors.

Conclusion

Annual Medicare plan reviews are essential for maintaining appropriate coverage and managing healthcare costs. By reassessing your plan each year, you can ensure it continues to meet your needs and take advantage of any new benefits or cost savings. Start your review early, ask the right questions, and consult with a Medicare expert to make informed decisions about your healthcare coverage. Taking these steps can help you avoid costly mistakes, ensure you have the best coverage, and give you peace of mind regarding your healthcare needs.