When Can I Change My Current Medicare Plan?

-

Last Updated July 21, 2026

Written by John Billetdoux

Medicare Broker Licensed in NJ, DE, FL, NC, PA & SC

If you’ve been on Medicare for some time, then you’re likely aware that things in Medicare are always changing. If you have a supplemental plan, then you’re already aware that your premium is always changing from one year to the next, and sometimes those increases can be pretty steep.

If you’ve got a Medicare Advantage Plan, then you may also experience fluctuations in your premium, as well as changes in co-pays, deductibles, benefits, etc.

It’s important to understand exactly what your rights and entitlements are under Medicare, and how specific changes can be implemented.

Changing Your Supplemental/Medigap Plan

We often get called by people whose supplemental/medigap premiums have skyrocketed and have become difficult to contain. So they want to know how they can change to a different supplemental plan, perhaps one that is less expensive.

It’s important to first know that supplemental/medigap plans are created and standardized by the federal government, so all G Plans will be the same, regardless of carriers you go through, the same applies for N and for all other supplemental plans. It’s important to realize that you may change your supplemental/medigap plan, 12 months out of the year. You are not bound by the Annual Enrollment Period in the fall, if you’re looking to move from one supplemental plan to another, for example moving from an Aetna G Plan to a Cigna G Plan. This is a move that can be made at any time of the year, however there is an underwriting requirement. In order to move from one supplemental plan to another, you must remember that you’ll have to pass through the underwriting phase. This means the potentially new carrier is allowed to ask you health questions, if they are not satisfied with the answers they receive, they can decline the application or possibly charge you a higher premium than you’d normally be paying. It’s not uncommon for people to move to cheaper medigap plans when their current plan gets burdensome in terms of its monthly premium, it’s just important to remember the underwriting.

The Annual Enrollment Period Myth

One common mistake that people have is that they can simply attempt this move during the Annual Enrollment Period, and no health questions would apply. This is 100% incorrect, as it makes no difference at all when you attempt to make a move such as this, you will ALWAYS have to answer health questions (so long as you are outside your initial 6 month Initial Enrollment into Part B). The fact that it may be Annual Enrollment Period, gives you no special considerations whatsoever, and it’s very important to remember this fact.

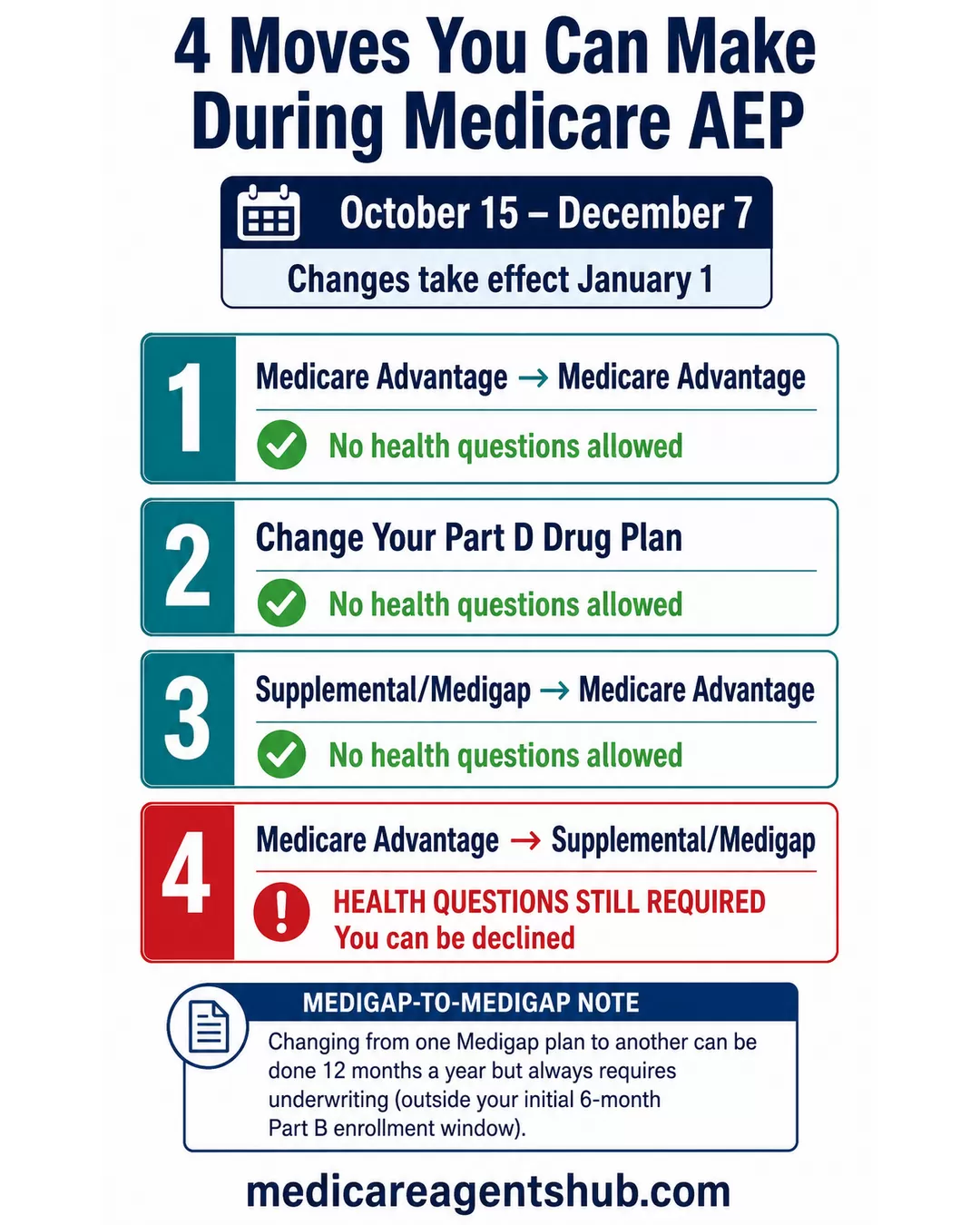

The 4 Moves You Can Make During the Annual Enrollment Period

The Annual Enrollment Period falls between October 15 and December 7 each year. Any changes that are made will go into effect January 1st. There are 4 moves that you can make during the AEP (Annual Enrollment Period). Those changes are as follows:

1. Medicare Advantage to Medicare Advantage

This is essentially a lateral move. It could be based on premium changes, co-pay changes, network changes. But it’s a very common move, and MedAdvantage Plans are NEVER allowed to ask health questions, so there are no concerns nor questions about your health.

2. Drug Plan Changes

This is a move that can be made during the AEP as well, and the same basic theme applies, maybe you’ve been diagnosed a new medication, or perhaps your premium has changed. This would be reason enough to seek out a new drug plan, and this move can be made during the AEP season.

3. Supplemental/Medigap to Medicare Advantage

This move is one that is often made by people who may feel they’re paying too much for their supplemental plan. It’s imperative that you consult with someone to make sure of the significant differences between a Supplemental plan and a MedAdvantage Plan… They are in no way remotely alike and so the benefits are significantly different, and the wrong move could be costly here. It’s one you’ll definitely want to review with a professional to make sure it’s the right one for you. Again, MedAdvantage Plans CANNOT ask you health questions, so this will be a smooth transition.

4. Medicare Advantage to Supplemental/Medigap

This is the most commonly misunderstood move of all of them. The reason for this is because people ASSUME that due to the fact it’s Annual Enrollment Season, they can simply do whatever they please in terms of movement, NOT TRUE. Many people assume they’ll sign up for the less expensive MedAdvantage Plan and then upgrade when their health goes south…..this is a TERRIBLE strategy and they always find out the hard way, that this isn’t how it works. If you are attempting to make this move during the Annual Enrollment Period, you will STILL HAVE TO ANSWER HEALTH QUESTIONS….and if you do not answer them to the carrier’s liking, they will decline you. Most people are surprised because they didn’t completely understand the rules of the Annual Enrollment Period, and are shocked to find that they are unable to move to a supplemental plan because of some health issue they may have.

Can I switch from a Medicare Advantage plan to a Supplemental/Medigap plan during the Annual Enrollment Period without answering health questions?

If you are attempting to make this move during the Annual Enrollment Period, you will STILL HAVE TO ANSWER HEALTH QUESTIONS….and if you do not answer them to the carrier’s liking, they will decline you.Why This Matters Before You Go on Medicare

This is why it’s important to understand these PRIOR to going onto Medicare. If you have a serious medical condition, then you’re absolutely going to want to consult with a professional because that health issue may prevent you from being able to change plans down the road, at least on the supplemental side of the fence (remember that a MedAdvantage Plan is NEVER allowed to ask health questions).

Why You Need a Medicare Broker

A Medicare broker works with a variety of carriers and plans, both on the supplemental/medigap side of the fence and on the MedAdvantage side of the fence. A plan that works for your neighbor, may not necessarily work for you, because everyone’s needs are different. You’re not likely to have the same health status, nor take the same medications… This is where it becomes individualized and you’ll want someone to guide and direct you into a plan that best meets your specific and individual needs, which is exactly what a Medicare Broker like JBA Insurance Brokers, does. We are trained professionals who are contracted with a variety of plans and carriers to ensure that you find the best plan for you, and we remain with you so that in the event your needs change at some point, we can reassess your situation and adjust accordingly.

Feel free to reach out to John Billetdoux of JBA Insurance Brokers through his Agent Listing here: John Billetdoux, Medicare Broker