10 Things Agents Want You to Know About Medicare and Prior Authorization

-

Last Updated July 20, 2026

You scheduled the surgery. Your doctor said it was necessary. And then someone from your insurance company called and said, "Not so fast... we need to approve this first."

If that sounds familiar, you've just run into prior authorization, one of the most common and least understood parts of Medicare coverage. It catches people off guard because they assume "covered" means "automatically approved." It doesn't always work that way.

We asked licensed Medicare agents across the country to share what they wish every beneficiary understood about prior authorization before the surprise hits. Here are the 10 things they want you to know.

1. Prior Authorization Is Standard, Not a Red Flag About Your Plan

This is the single most important thing agents want you to understand: needing prior authorization does not mean your plan is bad. It's a standard process used by insurance companies to confirm that a procedure or treatment is medically necessary before they agree to pay for it.

Think of it as your insurer saying, "We'll cover this. We just need your doctor to confirm it's the right course of action." For high-cost procedures like knee replacements, hip surgeries, and certain imaging scans, prior authorization is nearly universal across Medicare Advantage plans.

Your doctor's office typically handles the paperwork. In most cases, the approval comes through within a few days. It's not a denial; it's a checkpoint.

I called to ask about a knee replacement and suddenly they said I need prior authorization. I thought my plan was supposed to be good-what's going on?

Even if your plan covers it, many insurers require prior authorization to confirm the surgery is necessary, with an approved provider, and costs will be covered. It’s a standard step, not a problem with your plan.2. The Big Dividing Line: Advantage Plans Require It, Supplements Generally Don't

This is the distinction that shapes nearly every conversation about prior authorization. If you're on a Medicare Advantage plan (Part C), prior authorization is part of the deal. These are managed care plans run by private insurers, and they use PA as a tool to manage costs and utilization.

If you're on Original Medicare with a Medicare Supplement (Medigap), prior authorization is rarely required. Your doctor recommends the treatment, Medicare evaluates whether it's covered, and your Supplement pays its share. There's no insurance company in the middle saying "hold on, let us review this first."

This is one of the core trade-offs that come with Medicare Advantage. The premiums are often lower (sometimes $0), but you're trading that savings for managed care features like prior authorization, network restrictions, and referral requirements. Medicare Supplement plans cost more monthly but give you more freedom and fewer administrative hurdles.

Neither option is inherently better. They work differently, and the right choice depends on your health situation, your budget, and how much you value flexibility. Understanding how prior authorization fits into that equation is critical when comparing HMOs, PPOs, and other plan types.

Who will make medical decisions as to what is necessary to me: my Doctor or the insurance company?

Your doctor is the one who decides what care you medically need, tests, treatments, medications, and follow‑ups. That part is purely clinical.Your insurance company doesn’t make medical decisions, but they do decide what it will pay for based on your plan rules, prior authorization requirements, and Medicare guidelines.

So the doctor determines the care, and the insurance company determines the coverage.

3. Your Doctor Makes the Medical Call, But Your Plan Has the Last Word on Payment

One of the biggest sources of frustration around prior authorization is the feeling that an insurance company is overriding your doctor. Agents want to be clear about how this actually works:

- Your doctor decides what care you need. That's a clinical decision based on your health, your history, and their medical expertise.

- Your insurance plan decides what it will pay for. That's a coverage decision based on Medicare coverage rules, CMS guidance, and whether the treatment meets the plan's medical necessity criteria (not arbitrary cost decisions).

These are two separate decisions. Prior authorization is the mechanism your plan uses to make that second decision before the procedure happens, rather than after. When your doctor and your insurer agree, the process is smooth. When they don't, that's where appeals come in (more on that below).

If you're on a Medicare Advantage plan, learning how to talk to your doctor about coverage limits can help you navigate this dynamic more effectively. The more your doctor understands about your specific plan's requirements, the faster they can submit the right documentation.

4. Switching Plans Can Trigger Prior Authorization Surprises Overnight

This is where prior authorization blindsides people the hardest, especially with prescription drug coverage.

Every Part D plan has its own formulary (a list of covered medications with its own rules about which drugs need prior authorization). Medicare spells out the underlying Part D coverage rules that every plan has to follow, but the specifics vary plan to plan. When you switch plans, you're moving from one set of rules to a completely different set. A medication that was covered automatically under your old plan might suddenly require PA under the new one.

This doesn't just apply to obscure specialty drugs. Agents report seeing it happen with common maintenance medications like blood pressure drugs, cholesterol medications, even diabetes treatments. The drug is still "covered" by the new plan, but the coverage now comes with a prior authorization requirement that your old plan didn't have.

The worst part? Many plan comparison tools focus on whether a drug is covered and what it costs, but don't clearly flag PA requirements. That's why agents emphasize checking the formulary details, not just the coverage summary, before making any switch. This is one of the most common enrollment mistakes beneficiaries make.

I switched to a new Part D plan and now half my meds require prior authorization. Why didn't anyone warn me this could happen?

Switching to a new Medicare Part D plan can sometimes come with surprise like medications suddenly requiring prior authorization. Each plan has its own formulary (drug list) and coverage rules, which can include prior authorizations, step therapy, or quantity limits. Even if your medications were covered without issue before, a new plan may handle them differently.Many plan comparisons focus on cost and whether a drug is covered, but not always how it’s covered. That’s why this can catch people off guard.

The good news is there are solutions. Your doctor can usually submit a prior authorization, and in some cases request an exception if the medication is medically necessary. Many plans will also allow a temporary supply while this is being reviewed.

The important thing to remember when reviewing Part D plans is look beyond coverage and cost so you understand any restrictions that may apply so there are fewer surprises later.

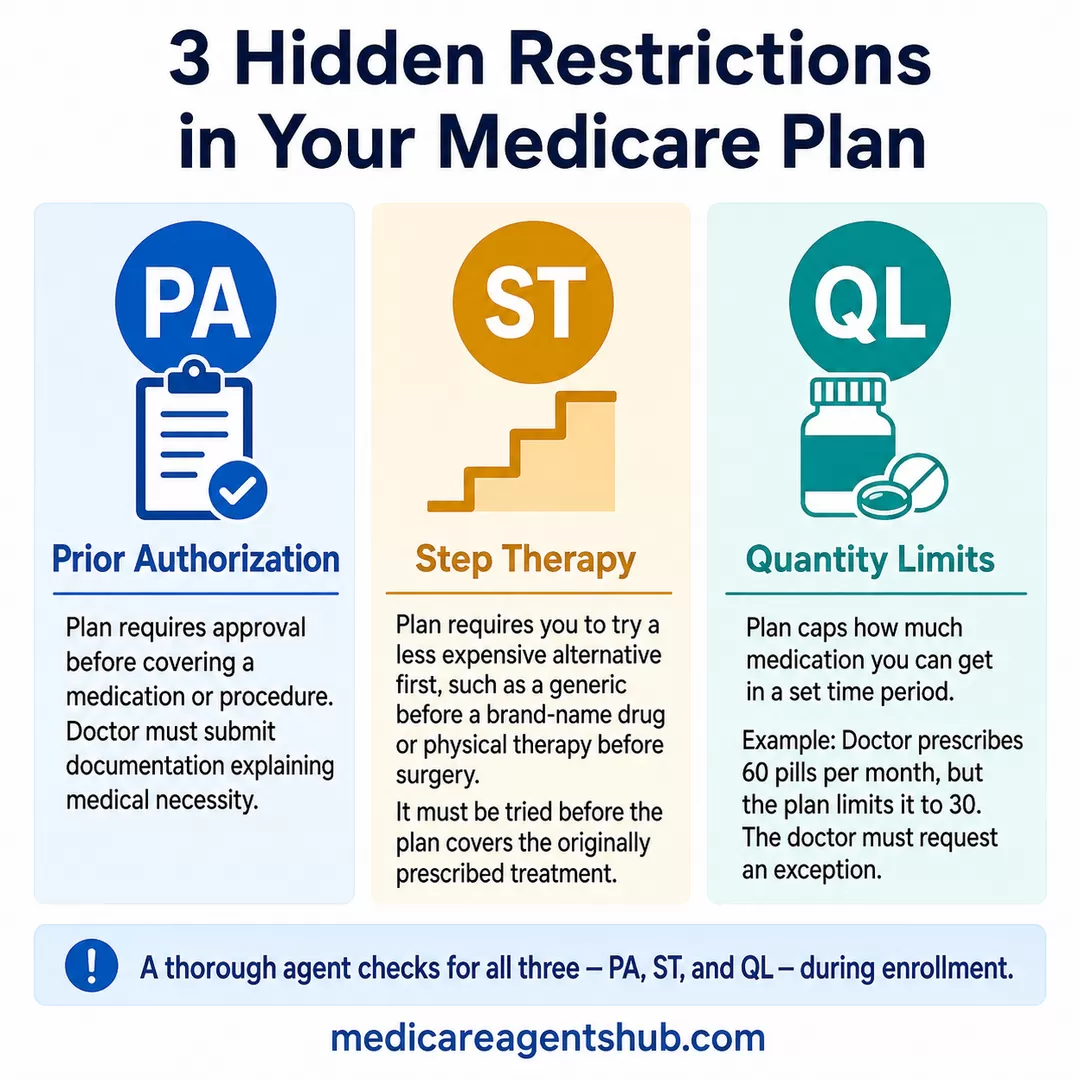

5. Three Hidden Restrictions Hiding in Your Plan: PA, Step Therapy, and Quantity Limits

Prior authorization is actually just one of three utilization management tools that plans use to control costs. The other two catch people off guard just as often:

Prior Authorization (PA)

Your plan requires approval before covering a medication or procedure. Your doctor submits documentation explaining why it's medically necessary.

Step Therapy (ST)

Your plan requires you to try a less expensive alternative first before it will cover the drug your doctor originally prescribed. For example, you might need to try a generic version before the plan will approve the brand-name drug, or try physical therapy before approving surgery.

Quantity Limits (QL)

Your plan caps how much of a medication you can get in a given time period. If your doctor prescribes 60 pills per month but your plan limits it to 30, you'll need your doctor to request an exception.

When agents review your medications during enrollment, they're not just checking whether each drug is on the formulary. They're checking for all three of these restrictions (PA, ST, and QL) because any one of them can disrupt your access to medication if you're not prepared. This is an essential part of choosing the right prescription drug plan.

6. You're Entitled to a Transition Fill While PA Gets Sorted Out

Here's a right that many beneficiaries don't know they have: if you switch to a new Part D plan and suddenly need prior authorization for a medication you were already taking, you're entitled to a transition fill.

A transition fill is typically a one-time 30-day supply of your medication that the new plan must provide while your doctor works through the prior authorization process. It's designed to prevent a gap in your treatment during the transition period. For certain drug classes like opioids or specialty medications, the supply length may be shorter, so ask your pharmacy exactly what the plan will cover.

How to use it:

- Contact your new plan's member services or your pharmacy and specifically ask for a "transition refill"

- Reach out to your prescribing doctor immediately so they can begin the prior authorization process with your new plan

- Don't wait. The transition fill is temporary, and the clock starts ticking from your plan's effective date

This safety net exists because Medicare recognizes that plan switches shouldn't leave people without critical medications. But it only works if you know to ask for it.

Can a drug plan drop one of my medications during the middle of the year?

Yes, a drug plan can drop a medication mid-year. It can also change the tier of the medication and the rules regarding its requirements for prior authorization. However, if you are currently taking a medication the plan must continue to cover it for the remainder of the year. This gives you time to either find a new plan for the next year or find an alternative medication if your doctor approves it.7. Prior Authorization Rules Change Every Single Year

A procedure that didn't require prior authorization this year might require it next year, even if you stay on the exact same plan. Medicare Advantage and Part D plans update their rules, formularies, and authorization requirements annually.

This is why annual Medicare plan reviews are so important. Your plan sends you an Annual Notice of Change (ANOC) each fall, outlining what's different for the coming year. Most people toss it in a pile of junk mail. Agents say you should read it carefully, or better yet, review it with someone who knows what to look for.

The prior authorization requirements for your specific medications and potential procedures should be part of every annual enrollment conversation. What worked last year is not guaranteed to work the same way next year.

If I’m in a Medicare Advantage plan, will I still need prior authorization for procedures next year?

You will likely still need prior authorization for many procedures next year (2026) and possibly in the years ahead If you’re enrolled in a Medicare Advantage plan. MA plans almost always require prior authorization for certain services before they’ll agree to cover them (especially higher-cost items like hospital stays, chemotherapy, durable medical equipment, etc.). This requirement will continue into 2026 and likely future years because Medicare Advantage insurers use prior authorization as a tool to manage costs and utilization. Starting in 2026, new federal rules are meant to make prior authorization easier by setting firm deadlines for insurer decisions and requiring clearer explanations when coverage is denied.8. New Federal Rules Are Speeding Up the PA Process, But Not Eliminating It

If you've been frustrated by prior authorization delays, there is some good news. The Centers for Medicare & Medicaid Services (CMS) has been rolling out new rules designed to make the process faster and more transparent.

Starting in 2026, Medicare Advantage plans face stricter deadlines for prior authorization decisions and must provide clearer explanations when coverage is denied. The goal is to reduce the "black box" problem where beneficiaries wait for weeks without understanding what's happening with their request.

But here's what agents want you to understand: these reforms are about making prior authorization faster and fairer, not about getting rid of it. Prior authorization is built into the structure of managed care. As long as Medicare Advantage plans exist in their current form, PA will be part of the package.

For beneficiaries who want to avoid prior authorization entirely, the path is Original Medicare with a Medigap plan, which comes with higher monthly premiums but virtually eliminates the PA process for medically necessary care.

9. If You're Denied, You Have the Right to Appeal

A prior authorization denial is not the end of the road. You have legal rights to appeal, and agents say many people who appeal end up getting the care they need covered.

Here's how the process works:

- Ask for the denial in writing. Your plan is required to explain why the request was denied and what criteria weren't met.

- Work with your doctor. The most successful appeals include detailed medical documentation from your provider explaining why the treatment is necessary for your specific situation.

- File the appeal. Start with your plan's internal appeal process. If that's denied, you can escalate to an independent review.

- Know the timeline. For standard appeals, plans must respond within 30 days. For expedited appeals (when your health is at risk), the deadline is 72 hours.

Don't give up at the first "no." The appeals process exists specifically because initial denials aren't always correct. Medicare publishes an overview of your claims and appeals rights, and for a detailed walkthrough, read our guide on how to appeal a Medicare denial and fight back.

I need home health care after my surgery, but Medicare denied coverage. What are my appeal rights?

You can always appeal. According to the Medicare Rights Center, 80 percent of Medicare Part A appeals and 92 percent of Part B appeals result in coverage for the beneficiary.10. A Good Agent Catches PA Issues Before You Enroll

This is the theme that came up more than any other when we asked agents about prior authorization: most PA surprises are preventable.

A thorough enrollment process with an experienced agent includes:

- Reviewing every medication against the plan's formulary, not just checking if it's covered, but checking for PA, step therapy, and quantity limit requirements

- Asking about upcoming procedures — if you know you'll need a surgery or specialist care in the coming year, that should factor into which plan you choose

- Explaining the PA landscape of each plan option so you can make an informed decision about whether the trade-off is worth it for your situation

- Flagging potential problems before enrollment locks you in for the year

The agents who answered questions about PA surprises after switching plans were nearly unanimous: this should have been caught during the enrollment conversation. When it wasn't, it usually meant the beneficiary either enrolled on their own without professional guidance, or worked with someone who didn't do a thorough medication review.

If prior authorization is a concern for you, and especially if you take multiple medications or anticipate needing procedures, working with a licensed Medicare agent in your area is one of the most effective ways to avoid surprises. The service is free to you, and a good agent will walk through every restriction in your plan before you sign anything.

How do you approach educating clients who are new to Medicare versus those who are considering switching plans?

There is no distinction. Most of the people I sit with who have had Medicare for years do not know how it works and do not know what things are not covered by Medicare. I explain it the same way and answer questions. People who are turning 65 are able to decide if they would like to start with a supplement and prescription drug plan or an advantage plan. I go over their health, doctors and prescriptions; What is most important for the client to get out of their plan and finally we go over the top plans available to them in their area (zip code).The Bottom Line

Prior authorization isn't going away. It's a permanent feature of managed care, and it's expanding, not shrinking. But it doesn't have to be a crisis if you understand how it works, know which plans require it, and have someone in your corner who checks the details before enrollment day.

The agents who shared their expertise for this article have seen hundreds of beneficiaries blindsided by prior authorization. Their collective advice boils down to this: the best time to deal with prior authorization is before you enroll, not after you're standing at the pharmacy counter or sitting in your surgeon's waiting room.