Medicare Advantage Is More Than Free Groceries and $0 Premiums

Every day, thousands of Americans become eligible for Medicare, and many quickly discover that enrolling isn't as simple as they expected. Television commercials, online advertisements, and stacks of mail promise everything from "$0 monthly premiums" to dental benefits, hearing aids, vision coverage, grocery allowances, and gym memberships. While these advertisements certainly grab attention, they often leave beneficiaries with more questions than answers.

Choosing a Medicare plan is one of the most important healthcare decisions a person will make after turning 65 or becoming eligible through disability. The right choice can provide financial protection, convenient access to physicians, and peace of mind. The wrong choice may result in unexpected costs, limited provider access, or prescription drug challenges.

Understanding how Medicare Advantage works and knowing what questions to ask before enrolling can help beneficiaries make informed decisions that fit both their healthcare needs and their budget.

What Is Medicare Advantage?

Medicare Advantage, also called Medicare Part C, is an alternative way to receive Original Medicare benefits through private insurance companies that contract with the Centers for Medicare & Medicaid Services (CMS).

Every Medicare Advantage plan must provide the same Medicare Part A (hospital insurance) and Part B (medical insurance) benefits covered by Original Medicare. Most plans also include prescription drug coverage (Part D), although not every Medicare Advantage plan does. In addition, many plans offer supplemental benefits that Original Medicare does not cover.

These may include:

- Routine dental care

- Vision exams and eyeglasses

- Hearing exams and hearing aid benefits

- Fitness memberships

- Transportation assistance

- Meal benefits following qualifying hospitalizations

- Over-the-counter product allowances

- Telehealth services

These additional benefits have made Medicare Advantage increasingly popular among Medicare beneficiaries across the United States.

Looking Beyond the Extra Benefits

Many beneficiaries naturally focus on the extra benefits advertised on television. While these benefits can provide meaningful value, they should never be the primary reason for selecting a Medicare Advantage plan.

A grocery allowance may save hundreds of dollars each year, but choosing a plan that doesn't include your physician or hospital could cost far more in inconvenience and healthcare expenses.

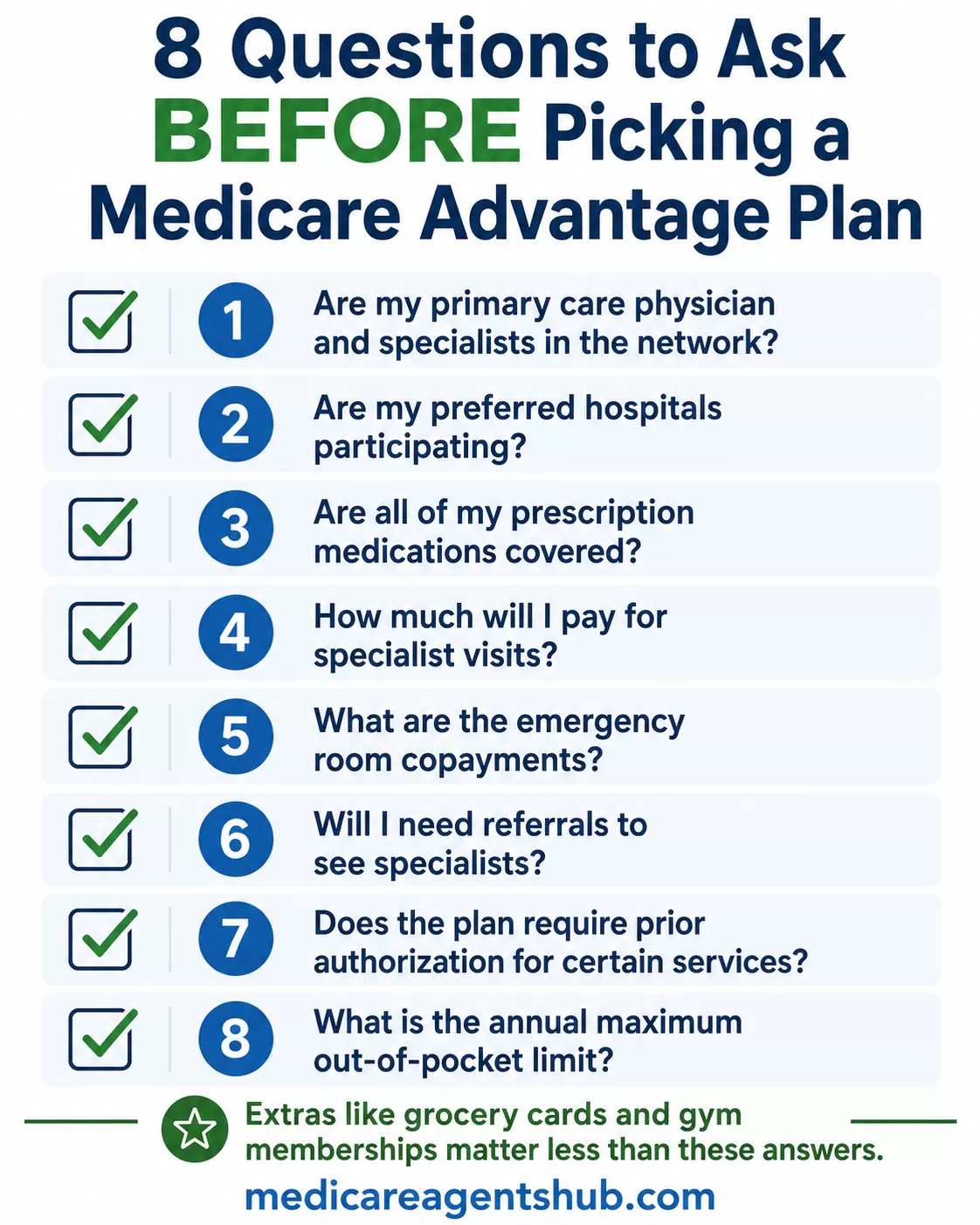

Before enrolling, beneficiaries should carefully evaluate several important questions:

- Are my primary care physician and specialists in the network?

- Are my preferred hospitals participating?

- Are all of my prescription medications covered?

- How much will I pay for specialist visits?

- What are the emergency room copayments?

- Will I need referrals to see specialists?

- Does the plan require prior authorization for certain services?

- What is the annual maximum out-of-pocket limit?

These questions often have a much greater impact on a beneficiary's overall healthcare experience than supplemental benefits alone.

The Importance of Coordinated Care

One of Medicare Advantage's greatest strengths is its emphasis on coordinated healthcare.

Many plans encourage members to establish an ongoing relationship with a primary care physician who helps coordinate preventive care, referrals, specialist appointments, laboratory testing, and chronic disease management.

This coordinated approach allows healthcare providers to communicate more effectively while helping patients avoid duplicate testing, medication conflicts, and unnecessary hospitalizations.

For beneficiaries managing diabetes, hypertension, heart disease, chronic lung disease, or multiple medical conditions, coordinated care can improve both convenience and long-term health outcomes.

Preventive Care Saves Lives

One of Medicare's most valuable goals is preventing illness before it becomes serious.

Most Medicare Advantage plans cover numerous preventive services with little or no additional cost when provided by participating healthcare professionals.

These services commonly include:

- Annual wellness visits

- Influenza and pneumonia vaccinations

- Cancer screenings

- Diabetes screenings

- Cardiovascular evaluations

- Bone density testing

- Depression screenings

- Smoking cessation counseling

Preventive care helps identify medical conditions early, when treatment is often simpler, less expensive, and more effective.

Understanding Costs

One question I hear often is, "If my premium is $0, does that mean I won't have any medical bills?" The answer is no. A $0 premium simply means there isn't an additional monthly plan premium beyond your Medicare Part B premium.

In reality, beneficiaries may still be responsible for deductibles, copayments, and coinsurance depending on the services they receive.

One important financial protection Medicare Advantage provides is an annual maximum out-of-pocket limit for Medicare-covered services. Once a beneficiary reaches that limit, the plan pays 100% of covered medical expenses for the remainder of the calendar year.

This protection does not exist under Original Medicare alone, making it one of Medicare Advantage's most valuable features.

Understanding these costs before enrolling allows beneficiaries to avoid unexpected financial surprises later.

Medicare Is Not One-Size-Fits-All

I've never believed there's a "best" Medicare Advantage plan. The right plan for a healthy 67-year-old who sees a doctor twice a year may be completely different from the right plan for someone managing diabetes, heart disease, or several prescription medications.

Someone who rarely visits physicians may value lower monthly costs and preventive benefits.

Another individual living with multiple chronic conditions may prioritize broad provider networks, specialist access, prescription drug coverage, and lower out-of-pocket medical expenses.

Healthcare needs are personal, and Medicare coverage should reflect those individual circumstances rather than advertising alone.

Why Reviewing Your Plan Every Year Matters

Healthcare needs change. Doctors retire. Hospitals enter or leave provider networks. Prescription formularies change. Benefits are added, modified, or removed.

For these reasons, beneficiaries should review their Medicare coverage every year during the Annual Enrollment Period rather than automatically renewing their existing plan.

Even if a current plan has worked well in the past, another option may better fit changing medical or financial needs.

An annual review allows beneficiaries to compare available plans, verify physician participation, confirm prescription drug coverage, and understand any changes before the next plan year begins.

Working with a Licensed Medicare Professional

Medicare rules, enrollment periods, provider networks, and prescription drug coverage can be overwhelming for beneficiaries navigating the system for the first time.

A knowledgeable, licensed Medicare professional serves as an educational resource by helping individuals understand their available options, compare plans objectively, verify provider participation, explain enrollment timelines, and answer questions in clear, understandable language.

The goal should never be to simply enroll someone in a plan. Instead, it should be to educate beneficiaries so they can confidently choose coverage that best supports their healthcare needs and financial goals.

Final Thoughts

Medicare Advantage has transformed healthcare coverage for millions of Americans by combining comprehensive medical benefits with innovative supplemental services and coordinated care.

However, the best Medicare Advantage plan isn't necessarily the one offering the most television commercials, the largest grocery allowance, or the longest list of extra benefits.

The best plan is the one that matches a beneficiary's physicians, hospitals, medications, healthcare priorities, and financial situation.

By understanding how Medicare Advantage works, asking the right questions, reviewing coverage annually, and making informed decisions, beneficiaries can maximize both their healthcare and their peace of mind.

About the Author: Will Carias is a bilingual Medicare insurance professional with a background in nursing, patient education, and healthcare. His experience in both clinical care and Medicare education has given him firsthand insight into the questions and concerns beneficiaries face when choosing health coverage. He is passionate about simplifying complex Medicare topics into practical, easy-to-understand information that empowers individuals to make informed decisions with clarity and confidence. Will believes that educated consumers make better healthcare decisions and is committed to helping beneficiaries confidently navigate both Original Medicare and Medicare Advantage.