The $0 Extras Trap: Why Veteran Agents Beg You Not to Pick a Medicare Advantage Plan for SilverSneakers, Life Alert, or a Grocery Card

-

June 10, 2026

Every fall during Annual Enrollment, Medicare agents across the country hear some version of the same question: "Which plan gives me SilverSneakers?" or "I want the one with the grocery card." It sounds reasonable. These benefits are marketed aggressively, they cost nothing extra, and who wouldn't want a free gym membership or $50 a quarter for groceries?

The problem, according to the agents who help seniors navigate these decisions for a living, is that chasing extras is one of the most reliable ways to end up in a plan that fails you when it matters. Not because the extras themselves are bad, but because they distract from the things that actually determine whether your plan protects you financially and medically.

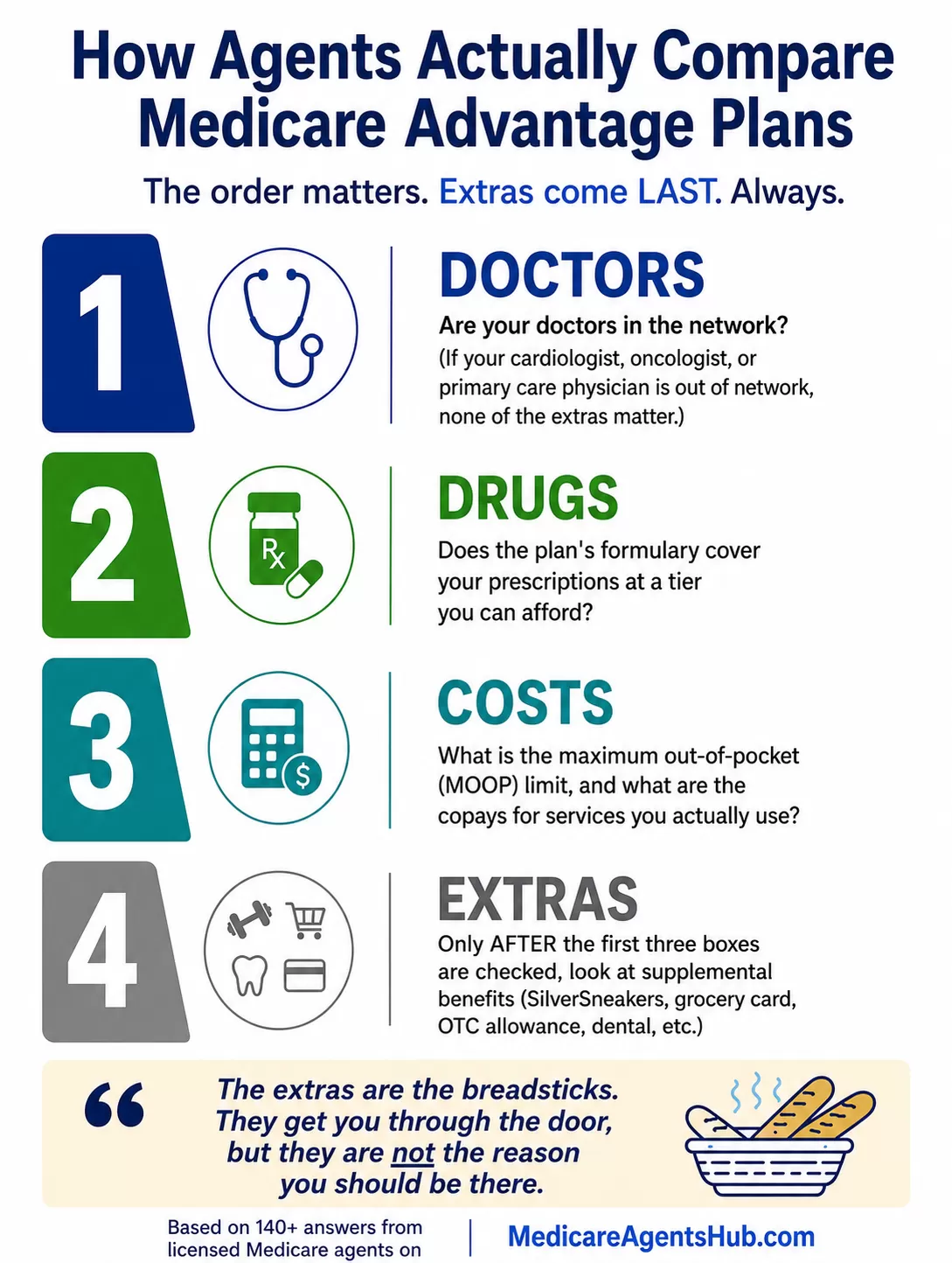

The Decision Order Agents Actually Teach

Ask a veteran Medicare agent how to compare plans and you will hear some version of the same framework, repeated so often it might as well be an industry catechism. The extras come last. Always.

Agents describe a clear hierarchy when walking clients through their options. First: are your doctors in the network? If your cardiologist, your oncologist, or even your primary care physician is out of network, none of the extras matter. Second: does the plan's formulary cover your prescriptions at a tier you can afford? Third: what is the maximum out-of-pocket (MOOP) limit, and what are the copays for the services you actually use? Only after those three boxes are checked do agents suggest looking at supplemental benefits.

What are the most overhyped benefits of Medicare Advantage plans that seniors should be wary of?

I always tell my clients to focus on the core benefits of the Advantage plan, in this order:1. Are all your "must-have" Dr's on the plan?

2. What are the co-pays and max out-of-pocket

3. Does the plan have a monthly premium, if so how much?

The ancillary benefits of dental, vision, OTC allowance, etc., are of least importance, unless #'s 1, 2 and 3 are equal, then the other benefits can be compared.

That sequence is not arbitrary. It reflects what agents see go wrong year after year: a client picks the plan with dental and a gym membership, then discovers in February that their blood pressure medication jumped from $15 to $90 because the new plan placed it on a higher tier. Or they find out their orthopedic surgeon is out of network and they need prior authorization to see anyone at all.

Why "Free" Benefits Cost More Than You Think

The extras that draw the most attention during enrollment season share a common trait: they feel like pure upside. SilverSneakers is free. The OTC allowance is free. The grocery card is free. But agents point out that nothing about a Medicare Advantage plan exists in isolation. Benefits generally draw from the same overall plan funding, and plans marketed as "free" still carry real costs that show up in copays, narrower networks, or higher out-of-pocket maximums.

Several agents compare the situation to choosing a restaurant based on the free breadsticks instead of the quality of the food. The extras are the breadsticks. They get you through the door, but they are not the reason you should be there.

What are the most overhyped benefits of Medicare Advantage plans that seniors should be wary of?

Food cards: due to a limited number of people qualifying for them, but agents are marketing them like crazy. OTC cards: Unless you really need help buying diabetes test strips, pain relievers, band-aids, etc., this shouldn't be a priority when deciding on a health plan. Part B Giveback: A lot of plans advertise this, however, common issues are $.60 - $1.00/month "Givebacks", OR the company offers more ($66 - $120), but a lot of times, it isn't paid, is overinflated, or you have to fight to get it--and it's likely going to be a contributing factor in that plan leaving the market the following year. Also, read the fine details on the dental, vision, and hearing benefits in the Summary of Benefits. I have many clients who were sold Medicare Advantage plans and had to purchase a standalone dental plan because the coverage wasn't what they were expecting--nor was it effective for their needs.Get insurance for what it's made to do best. Who's got better meatballs: Golden Corral, or the small Italian restaurant down the street that's been open since the '70's? My point: There is no magic insurance plan that does everything well all in one package (unless you have TRICARE or Medicaid, but that's not the focus); make sure you can see your doctors. Make sure you can afford the co-pays and deductibles. Physical therapy is a common situation where people overlook how quickly those $40 - $55 copays add up. Make sure you're covered at a price you can afford, at doctors you are comfortable seeing. Then move on and get a dental plan... in network with your dentist, covering what YOU need. Supplemental or Cancer/Heart/Stroke coverage is an affordable option to add to help with MA copays, hospitalizations, outpatient surgeries, and catastrophic health situations. Get creative and ask questions, but don't buy insurance because you're going to get $35 to use at CVS every quarter. Buy insurance plans that make you feel genuinely protected.

That analogy lands because it captures what agents see in practice: clients who enrolled for a quarterly grocery allowance and then spent thousands more than necessary on specialist visits or prescription copays. The math almost never works in favor of the extras. A $50-per-quarter grocery benefit adds up to $200 a year. A single specialist visit at an out-of-network rate, or a tier bump on a specialty medication, can erase that savings in a single claim.

The SilverSneakers Question

SilverSneakers is the single most asked-about extra benefit in Medicare Advantage. Agents field questions about it constantly, and many acknowledge it is a genuinely valuable program for seniors who use it. Regular exercise reduces falls, improves cardiovascular health, and supports mental wellbeing. Nobody disputes that.

What agents push back on is making SilverSneakers the deciding factor. The program gives you access to participating gyms and fitness classes at no additional cost, but your Medicare Advantage plan's core medical coverage determines far more about your financial exposure. Multiple agents note that many gyms offer senior discounts or low-cost memberships in the $20-30/month range. If the plan with SilverSneakers has a $4,000 higher MOOP than the plan without it, you would need to use that gym for over a decade to break even.

My friend gets SilverSneakers with her plan and I don't-how are we both paying for Medicare and getting such different stuff?

Extra benefits are going to depend on the type of plan you have and your carrier. Medicare supplement and advantage have numerous different options. While “extras” are great benefits to explore, your agent should be working with you first to verify your medications and providers are covered and in-network with your plan.Once you’ve verified plans that cover your specific situation, you’ll then want to see what extra benefits those plans will provide.

The better approach, as agents consistently describe it, is to narrow your options based on medical needs first, then check which of the remaining plans include fitness benefits. If two plans are otherwise identical in network, formulary, and cost structure, SilverSneakers can absolutely be the tiebreaker. But it should never be the starting point.

If you are already feeling unsure about how to weigh these trade-offs, you are not alone. A licensed Medicare agent in your area can walk you through the plans available where you live and help you compare what actually matters before you get to the extras.

Medical Alert Systems and Life Alert: The Coverage Gap Nobody Mentions

Life Alert and personal emergency response systems (PERS) represent a different flavor of the extras trap. Some Medicare Advantage plans do include a medical alert device as a supplemental benefit, but the coverage is far more limited than most people expect.

Agents who deal with these questions regularly report that clients come in believing Medicare will provide Life Alert the same way it provides a hospital bed or a wheelchair. It does not. Even on plans that include some form of PERS coverage, the benefit is often restricted to a basic pendant or wristband with limited monitoring. The full Life Alert system with its 24/7 monitoring, fall detection, and wall-mounted help buttons typically costs $50-80 per month out of pocket, and most of that is not covered by any Medicare Advantage plan.

Does Medicare pay for medical alert systems?

The majority of the time, the answer is "NO". There may be something with certain Medicare Advantage plans that could offer some cash back towards it, but where do you sacrifice other care in order to get that slight benefit? Putting some thought into it before you go in that direction is advisable.That question cuts to the heart of the extras trap. Every benefit in a Medicare Advantage plan represents a trade-off. The plan's total funding is finite, and dollars allocated to alert system subsidies or grocery cards are dollars not allocated to lower copays, broader networks, or more generous prescription coverage. Agents are not telling you these extras are worthless. They are telling you to understand what you might be giving up to get them.

When Extras Actually Can Tip the Decision

Agents are not uniformly anti-extras. The experienced ones are careful to distinguish between chasing extras as a primary strategy (bad) and using extras as a legitimate differentiator between otherwise comparable plans (smart).

There are specific situations where supplemental benefits genuinely matter more. Dual-eligible seniors (those qualifying for both Medicare and Medicaid) often have access to D-SNP plans that include substantial food allowances, transportation benefits, and OTC cards. For someone on a fixed income who qualifies for these specialized plans, those extras can meaningfully improve quality of life. Similarly, C-SNP plans designed for chronic conditions like diabetes or heart failure may include benefits specifically tailored to managing that condition.

I've had a change in my health condition. How does this affect my current Medicare plan, and should I reconsider my coverage?

Your Medicare plan could be greatly affected by your health. There are specialized plans tailored to chronic conditions in certain counties that are greatly beneficial.A Chronic Condition Special Needs Plan is a Medicare Advantage plan designed for people who have a chronic or disabling condition.

Benefits of a C-SNP can include specialized care, transportation, meal delivery services, access to specialists, telehealth services, and more.

If you need help signing up for a C-SNP, a Medicare Advisor can assist. Contact us or schedule a time to chat.

So, whether your health condition has improved or declined, an Advisor can help you understand your options better, even if you already have a C-SNP.

Healthy seniors with minimal medication needs and no strong doctor preferences represent another exception. If your medical exposure is genuinely low, the core coverage differences between plans shrink, and supplemental benefits carry more relative weight. But agents caution that this only applies if you are honest about your health profile. "I'm healthy" at 67 is a very different statement than "I'm healthy" at 77, and the plan you pick today is the plan that will cover you when something changes.

Some agents also highlight lesser-known benefits that deliver more tangible value than the headline grabbers: meal delivery after a hospital discharge, transportation to medical appointments, telehealth access, and expanded hearing or vision coverage. These tend to be more directly tied to medical outcomes than a gym membership or a grocery card, and they are worth investigating once the core coverage questions are settled.

The Grocery Card Reality Check

Grocery cards and OTC allowances became a flashpoint in Medicare Advantage marketing over the past few years. Agents report that the landscape around grocery cards shifted dramatically as CMS tightened rules on what qualifies as a supplemental benefit. Many of the generous food allowances that were advertised in 2024 and 2025 have been scaled back or eliminated entirely.

Even when grocery benefits are available, agents consistently describe them as misunderstood. The allowance is typically loaded onto a plan-specific debit card that can only be used at participating retailers for approved items. It is not cash. It is not flexible. And the quarterly amounts ($25-$75 in most cases) rarely move the needle on actual grocery spending.

The bigger issue is what these benefits signal about a plan's priorities. Plans that lean heavily on marketing extras tend to be the same plans with tighter networks, more aggressive prior authorization requirements, and higher copays for specialist visits. That pattern is not a coincidence. Marketing budgets and benefit design compete for the same resources, and plans that invest heavily in attracting enrollees through extras often have less room for generous core coverage.

Isn't it suspicious that Medicare Advantage plans offer gift cards and incentives to enroll?

It is a fair question, and the skepticism is understandable, but the extra benefits you see advertised with Medicare Advantage plans like grocery allowances, over-the-counter cards, and utility credits are actually funded by the government rebate dollars that carriers receive when they operate efficiently. That said, the marketing around these benefits has gotten aggressive and sometimes misleading, which is why CMS has cracked down on how carriers can advertise them. The most important thing to remember is that a flashy benefit should never be the main reason you choose a plan, because a $50 monthly grocery card means very little if the plan has a narrow network, high out-of-pocket maximums, or does not cover your medications well. Always look at the full picture of the plan before enrolling.What Agents Wish You Would Ask Instead

Rather than asking which plan has the best extras, agents wish more seniors would walk in with questions like:

- Are all my current doctors in this plan's network?

- What tier are my specific medications on, and what will I pay at the pharmacy each month?

- What is the maximum out-of-pocket if something serious happens?

- Does this plan require prior authorization for the specialists I see?

- What happens to my coverage if I need care outside the plan's service area?

Those five questions will tell you more about how a plan performs in the real world than any list of supplemental benefits. The extras are a bonus. They should feel like a bonus, not like the reason you chose the plan. When a $35 quarterly OTC allowance is the most compelling thing about your Medicare coverage, that is worth examining carefully.

The agents who answered these questions are not trying to take anything away from you. They are trying to make sure you do not give something away, specifically the medical and financial protection that is the entire point of Medicare, in exchange for benefits that look good on a brochure but fall apart under scrutiny. Talk to a licensed agent in your area before your next enrollment period. Bring your medication list, your doctor names, and your questions about coverage. The extras will sort themselves out once the important stuff is handled.

Frequently Asked Questions

Should I choose a Medicare Advantage plan because it has SilverSneakers?

Not as the primary reason. SilverSneakers is a valuable fitness benefit, but agents consistently recommend checking your doctors, medications, and out-of-pocket costs first. If two plans are equal on those fronts, SilverSneakers can be a great tiebreaker.

Does Medicare cover Life Alert?

Original Medicare does not cover Life Alert or similar personal emergency response systems. Some Medicare Advantage plans include a basic medical alert device as a supplemental benefit, but it is typically a limited pendant or wristband, not the full Life Alert system with 24/7 monitoring and fall detection.

Are Medicare grocery cards real?

Yes, some Medicare Advantage plans offer a grocery or food allowance loaded onto a plan-specific debit card. However, the amounts are usually modest ($25-$75 per quarter), they can only be used at participating retailers for approved items, and CMS rule changes have reduced their availability in recent years.

What should I compare before looking at Medicare Advantage extras?

Agents recommend this order: (1) confirm your doctors are in the plan's network, (2) check that your prescriptions are covered at affordable tiers, (3) compare the maximum out-of-pocket limit and copays for services you use, and (4) review prior authorization requirements. Only after those boxes are checked should extras enter the conversation.