Are Hospital Indemnity, Critical Illness, and Cancer Plans Smart Add-Ons or Upsells?

-

April 22, 2026

The Supplemental Insurance Debate

If you have Medicare Advantage, you've probably been offered a hospital indemnity plan, a critical illness policy, or a cancer plan at some point. Maybe your agent recommended one. Maybe a mailer showed up. Maybe a friend swears by theirs.

Here's what most of that marketing won't tell you: Medicare agents themselves don't agree on whether these products are worth buying. Some consider them a near-necessity for anyone on an Advantage plan. Others think they're redundant, especially if you have Medigap coverage. And a third group says the answer depends entirely on your health history and savings.

We gathered answers from dozens of licensed agents across the country to lay out each side honestly. No sales pitch. Just the arguments, the math, and the trade-offs so you can decide what makes sense for your situation.

Side A: Why Many Agents Recommend Hospital Indemnity Plans

The most common argument in favor of hospital indemnity plans centers on Medicare Advantage copays for inpatient hospital stays. Most MA plans charge a daily copay for the first several days of each hospitalization. Those copays are not small.

To see how the math works, consider a plan that charges $490 per day for Days 1 through 5 of a hospital stay. That single admission costs $2,450 out of pocket. A hospital indemnity plan running $30 to $40 per month could offset most or all of that bill.

The compounding risk is what concerns agents most. MA plans charge copays per admission, and those copays reset with each new hospital stay. Two hospitalizations in the same year could run $3,000 to $5,000 in copays alone, depending on the plan and length of stay.

Several agents pointed out that hospital indemnity plans pay you directly in cash, not the hospital. You can use that money for copays, but also for transportation, groceries, help around the house, or anything else. For people used to seeing medical bills pile up, getting a check in the mail instead is a welcome change.

Do I need a Hospital Indemnity Plan if I have Medicare Advantage? What if I am hospitalized twice in the same year?

With a Medicare Advantage Plan if you have a stay in the hospital, you will have a hospital copay usually days 1-5. These copays can be very costly as much as $350 a day depending on the plan.A hospital indemnity plan can help mitigate some of the risk by cutting you a check for your hospital stay. You can get a high plan or a low plan depending on your desired benefit amount. High plan around $50 a month and low plan around $30 a month.

Depending on the plan there may be a 60 day requirement before the plan will pay twice. This means staying out of the hospital for at least 60 days.

But, if its been a bad year health wise and you have already met your "MOOP" maximum out of pocket for your advantage plan. You are going to pocket that indemnity plan check, and actually make a profit.

The "Hybrid Medigap" Strategy

A growing number of agents describe the combination of a $0-premium Medicare Advantage plan plus a hospital indemnity plan as a budget-friendly alternative to Medigap. Some call it a "hybrid Medigap" approach: pairing an Advantage plan with hospital indemnity, cancer, and lump-sum benefits for roughly a third of what a traditional Medigap policy would cost.

One agent who carries this combination personally reported paying $88 per month for hospital indemnity, cancer coverage, and heart attack lump-sum benefits bundled together - far less than a standalone Medigap premium.

For seniors who can't afford Medigap premiums (which can run $150 to $300+ per month depending on age and location), this combination offers a middle ground. It won't cover everything a Medigap plan covers, but it addresses the single biggest out-of-pocket risk on most Advantage plans: hospital stays.

Side B: Why Some Agents Say These Plans Are Unnecessary

Not every agent is a fan. The strongest pushback comes from agents who believe Medigap coverage already handles the problem these plans claim to solve, and from agents who think the MOOP (Maximum Out-of-Pocket) cap on Advantage plans provides sufficient protection.

The Medigap Argument

If you're on Original Medicare with a Medicare Supplement plan, several agents said supplemental indemnity coverage is largely pointless. With a Plan G, you're only on the hook for the annual Part B deductible ($257 in 2025). Hospital stays, coinsurance, excess charges - it's all covered. A hospital indemnity plan on top of that is essentially paying for protection you already have.

Plan G covers the Part A deductible (currently $1,736 in 2026), hospital coinsurance, and Part B excess charges. There's very little left for a hospital indemnity plan to cover.

On the critical illness side, agents acknowledged that a good Supplement or even a strong Advantage plan may already provide sufficient medical coverage. A CI rider might come in handy if something serious happens, but only if the premium is reasonable for your situation.

Is paying for a high-end Medicare Supplement plan really worth it, or is it overkill?

I believe buying the best Medicare Supplement plan available is the smart move. It costs more upfront, but the lower financial exposure and stronger benefits outweigh the savings from cheaper plans with weaker coverage. Most clients I’ve guided find the trade-off worth it when they need serious care. You’re not overpaying—you’re securing peace of mind.The MOOP Cap Argument

Medicare Advantage plans have a Maximum Out-of-Pocket limit that caps your total spending for the year. Once you hit it, the plan pays 100% of covered services for the rest of the calendar year.

The practical argument is straightforward: your total out-of-pocket spending is what matters, not the number of hospital visits. Even without an indemnity plan, there's a ceiling on what you'll pay each year.

Some agents lean toward "no" in most cases, but stop short of a blanket dismissal. They frame it as a personal cost-benefit calculation: does the monthly premium justify the potential payout based on your health and financial situation?

With the supplements being so expensive in climbing in price every year, what is your take on hospital indemnity policies added with advantage policies?

I think hospital indemnity plans can make sense for some people on Medicare Advantage, especially if they want extra protection against inpatient copays and like having more predictable costs. That said, they are not a replacement for good core coverage, so I usually look at whether the Advantage plan already has reasonable hospital cost-sharing before adding another premium.Side C: It Depends on Your Health and Your Savings

The largest group of agents landed somewhere in the middle. Their consistent message: these products aren't universally good or bad. They're tools that make sense for some people and not others.

Family History Matters

Multiple agents pointed to family history as the deciding factor for critical illness and cancer plans. Their consistent advice: only you can assess that risk. If your parents or siblings have dealt with cancer, heart disease, or stroke, a CI plan becomes a much stronger consideration.

The statistics reinforce the point: roughly 1 in 2 men and 1 in 3 women will face some form of cancer in their lifetime. Heart disease and kidney failure are common as well. For people with family histories in these areas, the odds of eventually needing the coverage are substantial.

One agent compared the decision to investing: even without a family history, everyone has a risk tolerance. Can you absorb a large unexpected bill, or would you rather hedge with a modest monthly premium?

Do I need extra protection like Critical Illness Insurance if I am on Medicare?

It really depends on which way you go Medicare Advantage or Medicare Supplemental. On the Medicare Advantage plans, one of the main reasons that people hit their MOOP (max out of pocket), is because they are dealing with a Critical Illness. If you have a Medicare Supplemental, depending on the plan, you may see very little out of pocket costs for critical illnesses, except for your prescriptions. But now with the Inflation Reduction Act in full effect, if your prescription is approved by Medicare and on formulary, then the most you will pay in a year for your prescriptions will be $2000. So going back to the original question, I would recommend a Critical Illness policy to go with your Medicare Advantage plan if you go the Advantage route. If I was going into Medicare right now, I would go with a Medicare Supplemental plan. This way I will limit my exposure to any large medical bills, and that's a good feeling when people are on a fixed income!The Savings Test

Several agents offered a simple way to evaluate the decision: add up your inpatient copays for a week-long hospital stay. If that total is more than your budget or savings can comfortably absorb, an indemnity plan is worth considering.

A similar framework works for evaluating your overall risk: check your MA plan's Maximum Out-of-Pocket limit. If you couldn't handle that amount hitting all at once, a hospital indemnity plan provides a cushion.

This is the clearest way to think about it. If your MA plan's MOOP is $5,000 and you have $5,000 in savings you could access without hardship, an indemnity plan is optional. If that $5,000 bill would put you in a difficult spot, the $30 to $50 monthly premium starts looking like cheap insurance against a real risk.

What About Critical Illness and Cancer Plans Specifically?

Hospital indemnity gets the most attention, but critical illness and cancer plans work differently. Instead of paying a daily benefit during a hospital stay, these plans typically pay a lump sum when you're diagnosed with a qualifying condition like cancer, heart attack, or stroke.

These plans are purchased separately and pay directly to you upon diagnosis. The money is yours to use however you need, with no coordination of benefits with your medical coverage. They're designed specifically for the non-medical and out-of-pocket costs that pile up around a serious diagnosis: travel to treatment centers, lodging, missed time from work, experimental treatments.

The Gap Medicare Doesn't Fill

This is the angle that gets overlooked in most conversations about supplemental coverage. Medicare (whether Original or Advantage) covers the medical bills. But a serious diagnosis creates costs that go beyond hospital bills.

Agents mentioned these non-medical costs repeatedly:

- Travel to treatment centers (especially for specialized cancer care)

- Lodging near hospitals for extended treatment

- Lost income for a spouse or family member who takes time off to help

- Home modifications or hiring help during recovery

- Groceries, utilities, and everyday bills that don't stop because you're sick

Agents consistently made the point that Medicare simply does not cover these non-medical costs. Lost income, travel, home modifications, out-of-network specialist care - none of it. That gap exists regardless of which type of Medicare coverage you have, and it's the specific gap CI policies are built to fill.

One veteran agent with over 20 years in the business broke it down by coverage type. On Medicare Advantage, a CI policy provides a financial buffer against the plan's cost-sharing on top of covering non-medical expenses. On a Supplement, your medical costs are already predictable and capped, but the non-medical burden remains: airfare to a cancer center, hotel stays during treatment, hiring help at home. Either way, CI covers the indirect costs that no Medicare plan touches.

Can you help me understand Maximum Out-of-Pocket (MOOP) limits in Medicare plans, from your experience as an agent?

The maximum out of pocket is your threshold for copayments and deductibles. After it is met, you go to 100% coverage for the year. My experience as an agent is that shockingly few people ever reach the maximum out of pocket. The reason is because many plans do not have a deductible and the copays are very low. Even hospitalization is not going to be all that high. As a result, the only people I ever see reach it is people that go through very serious chronic conditions like cancer, kidney failure, and others that require so many specialist and high dollar treatments.The Math: When Does a Hospital Indemnity Plan Pay for Itself?

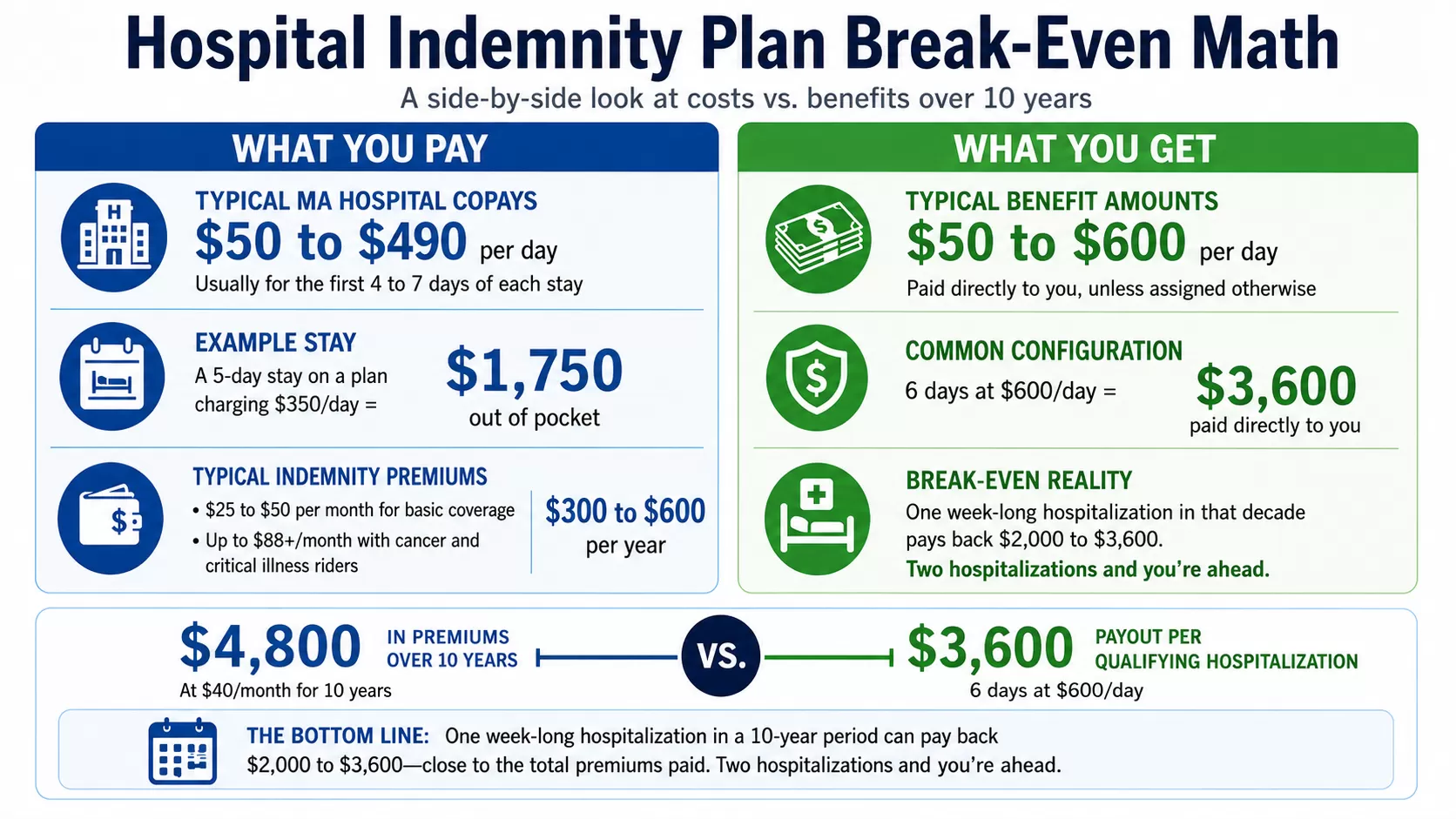

Several agents shared specific numbers that help illustrate the break-even calculation.

Typical MA hospital copays: $50 to $490 per day, usually for the first 4 to 7 days of each stay. A 5-day stay on a plan charging $350 per day costs $1,750 out of pocket.

Typical indemnity plan premiums: $25 to $50 per month for basic coverage, up to $88 or more for plans that include cancer and critical illness riders. That's $300 to $600 per year in premiums.

Benefit amounts: $50 to $600 per day depending on the plan, with most people choosing coverage that aligns with their MA plan's copay structure. A common configuration is 6 days of coverage at $600 per day, paying out $3,600 directly to the policyholder - essentially 5 days to cover hospitalization and 1 day to cover the annual premium.

It's worth zooming out to a longer time horizon. Hospital stays are relatively rare events, so agents recommend running the numbers over a 10-year window rather than a single year. At $40 per month, you'd pay $4,800 over 10 years. If you're hospitalized once in that decade for a week, a good indemnity plan would pay back $2,000 to $3,600. Twice, and you're ahead.

Do I need a Hospital Indemnity Plan if I have Medicare Advantage? What if I am hospitalized twice in the same year?

If you have a Medicare Advantage plan, you may still consider a Hospital Indemnity plan because most MA plans charge a per-day copay for inpatient hospital stays. That means if you’re admitted, you’ll owe the daily copay amount outlined in your plan’s Summary of Benefits. If you are hospitalized twice in the same year, you would typically pay that copay structure twice, since each admission is treated separately. A Hospital Indemnity plan pays you a fixed cash benefit per day (or per stay), which you can use to offset those out-of-pocket costs. It isn’t required, and it really comes down to whether you could comfortably absorb multiple hospital copays in a year. If those costs would create financial strain, an indemnity plan can provide a cushion.The trade-offs that come with Medicare Advantage extend beyond just copays. Network restrictions, prior authorization requirements, and varying coverage levels all factor into whether additional protection makes sense.

What Agents Don't Always Tell You

A few agents raised points that often get buried in the sales conversation:

Hospital indemnity doesn't cover everything. These plans cover hospital stays, not the full range of MA plan costs. Physical therapy is a common blind spot: 20+ PT visits at your specialist copay rate after a surgery add up fast, and the indemnity plan won't help there. The same goes for chemotherapy or radiation treatments billed as outpatient services.

Observation status is a gap. Even if you spend the night in a hospital bed, you might be classified as an outpatient rather than formally admitted. Hospital indemnity plans typically require an inpatient admission to trigger benefits, so observation stays may not be covered. Always confirm your admission status with hospital staff.

Benefit reset periods vary. Most plans require 60 days between hospital stays before the full benefit resets. Some are 30 days, some are longer. If you're readmitted quickly for the same condition, the plan may not pay full benefits on the second stay.

Premiums can be locked in. On the upside, unlike Medigap premiums, which tend to climb year after year, many indemnity plan premiums lock in at the age you enroll. That price stability is part of the appeal for people on fixed incomes.

With the supplements being so expensive in climbing in price every year, what is your take on hospital indemnity policies added with advantage policies?

I think that Hospital Indemnity Policies are a great idea in combination with Medicare Advantage. But please understand that the HIP will not cover every expense that you are exposed to in your Medicare Advantage plan. A good example is Physical Therapy. You may need 20+ PT visits at your specialist copay amount after a surgery or injury, and that really adds up. Another example would be chemotherapy / radiation treatments or yet another would be Skilled Nursing Care. These items would not necessarily be covered by a HIP but could cause you substantial out-of-pocket expense. Always talk to a licensed agent to learn what options are best for your needs before you purchase a policy.How to Decide: A Quick Framework

Based on what agents across the country said, here's a straightforward way to think through this decision:

You probably don't need these plans if:

- You have a Medigap plan (especially Plan G or Plan F) that already covers hospital costs

- You have enough savings to comfortably absorb your MA plan's MOOP

- You're healthy with no significant family history of cancer, heart disease, or stroke

These plans deserve a serious look if:

- You're on Medicare Advantage with hospital copays of $200+ per day

- A $3,000 to $8,000 unexpected bill would strain your finances

- You have a family history of cancer, heart attack, or stroke

- You switched from Medigap to MA to save on premiums and want to recapture some protection

- You're on a fixed income and prefer predictable monthly costs over unpredictable large bills

The hidden costs that blindside first-time enrollees often include exactly the type of expenses these supplemental plans are designed to cover. Knowing your plan's copay structure before you need it is the first step.

The Bottom Line from Agents

One thing was clear across every answer we reviewed: no agent said these plans are a scam. The disagreement is about who needs them, not whether they work. The strongest advocates pair them with Advantage plans as standard practice. The skeptics recommend them selectively, or not at all for Medigap holders.

The most practical advice came from agents who emphasized doing the math for your specific situation. Add up your plan's hospital copays for a week-long stay. Compare that number to the annual premium of an indemnity plan. Then ask yourself whether you could absorb that bill without help.

If the answer is no, and especially if your family history puts you at higher risk for hospitalization, these plans do exactly what they promise. If the answer is yes, your money might be better spent elsewhere. Either way, the decision is worth a conversation with a licensed agent who can review your specific plan and help you weigh the numbers.