5 Hidden Medicare Costs That Blindside First‑Time Enrollees (Agents Explain How to Dodge Them)

")

-

Last Updated July 22, 2026

Why So Many First-Time Medicare Enrollees Get Blindsided by Hidden Costs

Even after doing their homework, many first-time Medicare enrollees are shocked to find out that their new plan doesn’t cover everything. Some expenses aren’t obvious at sign-up, while others get lost in the fine print, until it’s too late.

To uncover what catches people off guard the most, Medicare Agents Hub, the internet’s largest directory of Medicare insurance agents, asked dozens of experienced professionals the following question:

“What’s one hidden Medicare expense that people don’t think about until it’s too late?”

The responses poured in from licensed agents across the country. These aren’t hypothetical worries, they’re real-world issues clients face every day. Below, we’ve grouped their answers into five key categories. Whether you’re new to Medicare or helping someone else navigate it, this list could save you thousands in avoidable costs.

1. Skilled Nursing & Long-Term Care Gaps

Why short-term coverage ends fast, and how ongoing needs become costly

One of the most commonly overlooked Medicare expenses is the limited coverage for skilled nursing and long-term care. Many enrollees assume that Medicare will step in fully if they ever need extended care in a facility or at home, but the reality is far more restrictive.

Traditional Medicare only covers the first 20 days of a skilled nursing facility stay in full. From days 21 to 100, patients are responsible for a daily co-pay, and after 100 days, Medicare stops paying altogether. One agent highlighted how this leaves patients vulnerable:

“Skilled Nursing Facility Costs. Days 1-20, Medicare pays 100%. Days 21-100, the member pays a daily co-pay. After 100 days, Medicare no longer covers expenses.”

Another added that even with Medicare Advantage plans, skilled nursing coverage can be limited or unclear, and few people prepare for what comes next.

Long-term care is another major blind spot. Many seniors mistakenly believe Medicare will cover long-term custodial care, such as a nursing home stay for dementia or assistance with daily activities over the long haul. It doesn’t. Without a separate long-term care insurance policy or substantial savings, this becomes a massive out-of-pocket burden.

“No one thinks about the possibility of having to have a caregiver or even staying in a facility. It's a HUGE problem and regular Medical Insurance does not cover it.”

Agents across the board stressed that families are often blindsided by these limitations, especially after a serious illness or fall. Planning ahead for long-term care or looking into supplemental insurance that covers skilled nursing gaps is critical to avoiding this hidden cost.

2. Out-of-Pocket Maximums, Deductibles & Co-Pays

The high price tags that sneak in under “coverage”

Another major hidden cost that blindsides first-time Medicare enrollees is the accumulation of out-of-pocket expenses, especially under Medicare Advantage plans. These include deductibles, hospital co-pays, and the out-of-pocket maximum (MOOP) that can amount to thousands of dollars annually.

One agent noted that in 2025, the federal government sets the MOOP limit for Medicare Advantage plans at $9,350, but not all beneficiaries realize that’s even a possibility:

“They do not understand the Medicare Advantage MOOP limits… You may be expected to pay this maximum out-of-pocket cost annually for the covered services.”

Even though Medicare Advantage plans often appear “affordable” on the surface, people are sometimes surprised when they receive a hospital bill after a stay. One agent pointed out that hospital co-pays can catch people off guard. The bill shows up after discharge, when it's least expected.

“Hospital co-pays that the clients don't realize that they have until they leave the hospital and receive their bill.”

In Original Medicare, Part B coinsurance (typically 20% of the service cost) is another area where enrollees may underestimate their exposure. One agent recalled a retiree who had dropped her supplement plan due to good health, only to face a major bill following a heart attack:

“Under Part B of Original Medicare, she is responsible for her Part B deductible… plus 20% of the cost. A heart attack can easily cost $5k or more with just Part A and Part B.”

Several agents also warned about annual rate increases on Medigap (Medicare Supplement) plans, which many don’t expect but can add up over time. And across all types of coverage, underestimating deductibles and co-pays is a consistent theme. As one agent put it, many clients don’t realize what’s coming until it’s too late:

“Sometimes people don't think about the deductibles and out-of-pocket maximum until it's too late.”

This category of hidden expenses underscores the importance of fully understanding your plan’s cost structure: not just premiums, but what you may pay if and when something happens.

What Agents Say About Medicare Decisions People Regret

What's one Medicare decision that too many people regret later?

I would say that the one i here most is: Regretting choosing a Medicare Advantage plan based on low premiums without realizing it restricts doctor networks and requires prior authorization for care. Many regret not opting for Original Medicare with a Medigap plan, which allows nationwide access to any doctor who accepts Medicare.Other regretted decisions include:

Restricted Networks: Switching to a Medicare Advantage plan and realizing their preferred specialists are out-of-network, leading to higher costs or inability to see them.

Forgoing Medigap Initial Enrollment: Skipping a Medicare Supplement (Medigap) plan at 65. If you do not buy one during your Initial Enrollment Period, you may have to pass medical underwriting later, meaning you can be denied coverage due to pre-existing conditions.

Assuming Medicare Covers Everything: Assuming standard Medicare covers long-term care, dental, or vision, leading to unexpected, massive out-of-pocket expenses.

Missing Part B Enrollment: Failing to enroll in Part B when first eligible, resulting in lifetime late-enrollment penalties and coverage gaps.

"Set it and Forget it" Drug Coverage: Not re-evaluating Part D drug plans annually,

3. The High Cost of Medications

When drug coverage gaps and deductibles catch you off guard

Prescription drug expenses are another area where Medicare beneficiaries are often caught off guard, especially those who assume medications are automatically included in their plan. For those enrolled in Original Medicare (Parts A & B), prescription drug coverage is not included by default, which means you need to enroll in a Part D plan or risk going without coverage altogether.

One agent emphasized that this gap is still widely misunderstood:

“Original Medicare Part A & B usually doesn't include prescription drug coverage. Make sure it's part of your package.”

Even when a Part D or Medicare Advantage plan includes drug coverage, deductibles and formulary limitations can lead to unexpectedly high costs, particularly early in the year or for higher-tier medications. One agent flagged prescription drug deductibles as a major blindside, especially under Medicare Advantage:

“The biggest expenses that often creep up on folks are… prescription drug deductibles on a Medicare Advantage plan.”

Another agent added that not only are drug costs a concern, but provider networks can further complicate access. If your doctor isn’t in-network, you may face high out-of-pocket charges just to get a prescription authorized or filled:

“Prescription drug costs. And that their doctor may not be in network and they may have to pay out of pocket to see them.”

Choosing the right drug plan requires more than just looking at the premium. Enrollees need to consider which medications they take, whether those drugs are covered, what tier they’re on, and what deductible applies. Failing to do this upfront often results in sticker shock at the pharmacy counter. In the video below, Scottsdale-based Medicare agent Steve Brauer provides a brief explanation of the different tiers within Medicare Part D prescription drug plans.

4. Dental Expenses Aren’t Covered

Why ignoring dental benefits leads to big bills later

Many first-time Medicare enrollees are surprised to learn that routine dental care is not covered under Original Medicare. Services like cleanings, fillings, root canals, dentures, and oral surgery typically require separate coverage, and failing to plan for this can result in expensive out-of-pocket bills.

One agent pointed out that seniors often assume dental care is part of their plan, only to discover too late that even basic services are excluded unless they’ve enrolled in a Medicare Advantage plan that includes limited dental benefits:

“Dental is an expense that traditional Medicare does not cover and that can be very expensive to cover depending on what is required.”

Another agent reminded enrollees that as we age, dental care becomes more essential, not less, which makes this particular gap in coverage even more financially risky:

“Dental insurance too is a needed coverage as we get older.”

Some Medicare Advantage plans may offer partial dental coverage, but the scope and quality of that coverage can vary widely. Without the right plan or a standalone dental policy, many retirees end up paying out of pocket for routine and emergency care, often when their income is most fixed.

This overlooked gap reinforces the importance of reviewing all healthcare needs, not just medical, when choosing a Medicare plan. Factoring in dental from the start can prevent hundreds or even thousands of dollars in surprise expenses.

5. Penalties & Premium Surprises

Late fees, IRMAA charges, and supplement premium hikes

Some of the most financially painful surprises come not from services rendered, but from timing mistakes and income-based penalties that Medicare enforces, often without much warning.

One such surprise is the late enrollment penalty for Part B and Part D. If you delay enrollment and don’t have other creditable coverage, you can be penalized for life, even if the delay was accidental. One agent emphasized how commonly this is overlooked:

“Late enrollment penalties are often overlooked. Medicare Part B and Part D both have a late enrollment penalty if you go without creditable coverage for a period of time.”

Agents Explain Why Lifelong Penalties Happen

Why do some seniors end up paying lifelong penalties for Medicare Part B or Part D?

Social Security expects a new Medicare beneficiary to enroll in their Part B as well as a Part D prescription drug plan (PDP).When turning 65, you'll have a 7-month window (3mo ahead before your birth month, your birth month, and 3 months thereafter) to enroll in your Medicare Part B. If not, a Late Enrollment Penalty (LEP) would apply. If one goes longer term without having enrolled in their Part B, they'll eventually pay an additional 10% for each year without coverage above the current standard rate at the time of issue.

If one is retiring and losing employer/group coverage, they'll have the opportunity to enroll in their Part B without penalty, so long as creditable coverage has been verified.

Social Security also "expects" one to have a qualified PDP. If one doesn't enroll in a PDP plan, nothing happens until there is enrollment into a plan; either a standalone PDP or a Medicare Advantage Plan w/PDP. The LEP here is a % of the current standard rate for a PDP at the time of issue, multiplied by a % factor to establish the LEP.

Unfortunately, in either circumstance where an LEP is applied, this penalty is for life. Thus, it's always wise to make sure there's adequate research before becoming Medicare eligible or simply contact a credible agent.

Steven A James, MBD

Contact me.

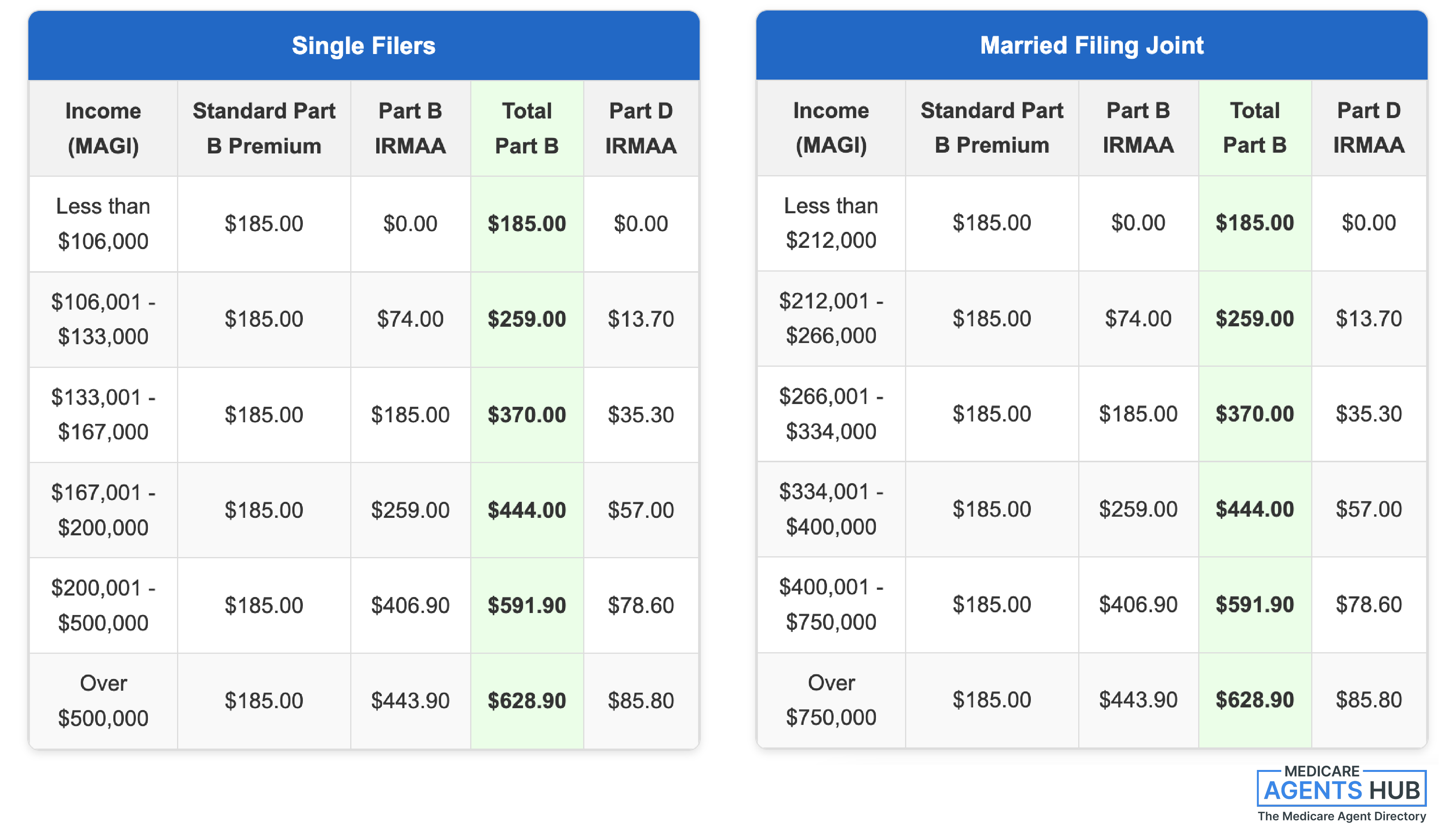

Another blindside for higher-income beneficiaries is IRMAA (Income-Related Monthly Adjustment Amount), which increases the monthly cost of both Part B and Part D based on your income. Many people don’t expect this added premium and are shocked by the increase, especially if their income is just slightly over the threshold.

“No matter what plan you’re on, if your income is on the high side, an IRMAA Part B and Part D can be a huge shock.”

What Agents Say About IRMAA

I've heard about IRMAA affecting my Medicare premiums. How can I find out if it applies to me, and how does it work?

IRMAA is always (NOT) a fun surprise and many folks don’t see it coming. It stands for Income-Related Monthly Adjustment Amount, but really, it just means Medicare is charging you more because you “made too much” two years ago. Yay, right?Medicare looks at your income from two years back - so in 2025, they’re using your 2023 tax return. If your income was over a certain amount, you’ll pay extra for Part B and Part D. And no, it’s not always a small bump - it can be a few hundred bucks more per month depending on your income level.

You’ll get a letter from Social Security if IRMAA applies. The timing of that letter? Let’s just say it's government issued and doesn’t always conveniently show up BEFORE you’ve already picked your plans and thought you had your costs locked in.

If you’re not working with someone who brings this up ahead of time, that Social Security letter is not a fun one to open. That’s why it helps to trust your advisor who’s actually looking ahead - not just plugging in plan info or letting you go at it alone.

The good news? If your income has gone down if you just retired, sold a business, or lost a spouse - you can appeal it using form SSA-44 to get those premiums adjusted.

If your 2023 income was over $103,000 (single) or $206,000 (married filing jointly), it’s worth looking into. If not, you’re probably good. Either way, the key is catching it before you’re stuck wondering why your Medicare bill just jumped.

Lastly, those who opt for a Medicare Supplement (Medigap) plan are often surprised to find that the premiums increase over time. While these plans can offer excellent coverage, they are subject to pricing changes by private insurers, and those hikes aren’t always anticipated when people enroll.

“The drawback with these types of plans is… insurance carriers underwrite these Medigap plans and have the right to increase monthly premiums.”

Altogether, these three sources of hidden costs: penalties, income-based surcharges, and rising premiums, can quietly add hundreds or thousands to your annual Medicare expenses if you’re not prepared. Working with a knowledgeable agent who explains these scenarios upfront can make all the difference.

How to Avoid These Hidden Medicare Costs Before They Drain Your Budget

Medicare is often marketed as comprehensive, but the reality is more complicated, and more costly, than most first-time enrollees expect. From limited nursing care coverage to out-of-pocket surprises, drug plan gaps, missing dental, and unexpected penalties, there are multiple ways your health expenses can balloon if you’re not fully informed. Many of these pain points are problems agents have been pushing to change for years.

Fortunately, these pitfalls are avoidable, if you know where to look.

The insights shared here come directly from licensed Medicare agents who work with real clients every day. Their advice is based on hard-earned experience, not theory. And the takeaway is clear: the more proactive you are in understanding what’s not covered, the better positioned you’ll be to protect yourself financially.

If you’re approaching Medicare enrollment, or helping someone who is, use this list as a guide to ask better questions, compare plans more carefully, and plan ahead for the unexpected. And if you’re not sure where to begin, consider browsing Medicare Agents Hub, the internet’s largest directory of licensed Medicare insurance agents, to find someone who can walk you through it all, without the guesswork.

Because when it comes to Medicare, what you don’t know really can cost you.