CMS-L564 Form Explained: What It Is, How to Fill It Out, and Why It Matters

-

June 21, 2026

Most people who delay Medicare Part B because they're still working never hear about the CMS-L564 form until Social Security asks for it. By then, the clock on a late enrollment penalty may already be running.

Quick answer: CMS-L564 is the Medicare "Request for Employment Information" form used to prove that you delayed Part B because you had group health coverage based on current employment. It is usually submitted with CMS-40B when enrolling in Part B after age 65. COBRA and retiree coverage generally do not extend the Part B Special Enrollment Period, and missing the window can lead to a lifetime Part B penalty.

What the CMS-L564 Form Actually Is

The CMS-L564, officially titled Request for Employment Information, is a one-page form that gives Social Security written proof that you (or your spouse) had health coverage through a current employer after you turned 65. That proof is what unlocks a Part B Special Enrollment Period (SEP) and waives the late enrollment penalty that normally kicks in for anyone who signs up after their Initial Enrollment Period ends.

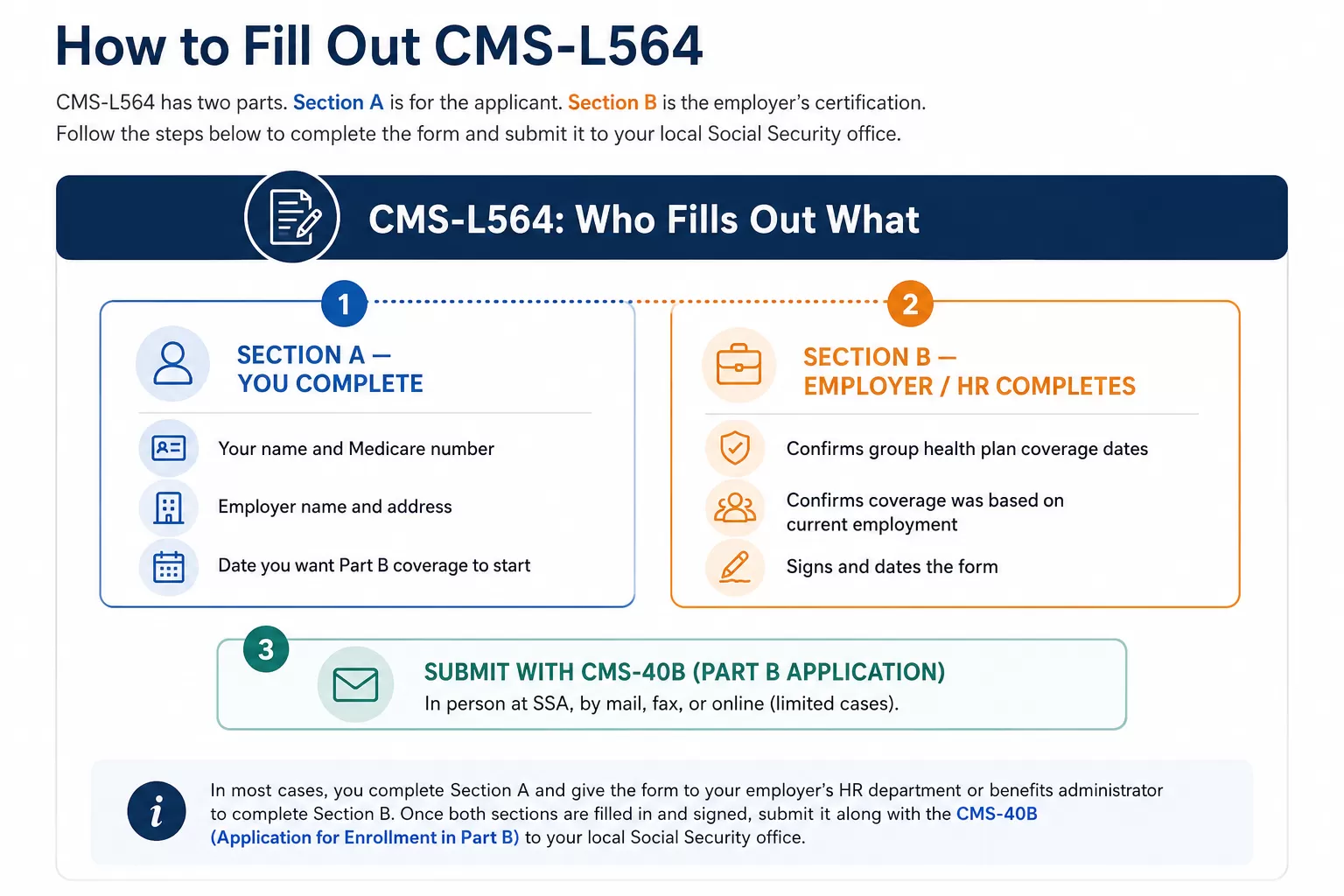

Two sections. You complete Section A: name, Medicare number, employer info. Your employer's HR or benefits administrator completes Section B, confirming the dates you were covered under their group health plan and that the coverage was based on current employment, not retirement or COBRA.

The form proves two things at once: you had coverage, and that coverage came from active employment. Agents say to keep two kinds of proof on file starting now. First, your annual Part D creditable drug coverage notice from the plan administrator. Second, separate proof that your medical coverage comes from active employment: a completed CMS-L564, an employer letter confirming group health plan dates, pay stubs, W-2s, insurance cards with effective dates, or EOBs. A Part D creditable coverage letter does not prove group health plan coverage for a Part B Special Enrollment Period. SSA is explicit about that distinction (SSA POMS HI 00805.295).

What is the CMS-L564 form and when do I need it for Medicare enrollment?

If you decide to work past the age of 65, you will need to fill out the L-564 form and submit it to Social Security when you apply for your Part B. The L-564 form is filled out by your employer and shows that you've had "creditable coverage" by your employer since you turned 65. This is a very important document to submit because it will keep you from having to pay a late penalty.How to Fill Out CMS-L564

Section A is for the applicant: your name, Medicare number (or Social Security number), and contact information. Section B is the employer's certification, where HR fills in the dates you were covered under the group health plan, the employer's name, and the employer's signature confirming the information.

In most cases, you complete Section A and hand the form to your employer's HR department or benefits administrator to complete Section B. Once both sections are filled in and signed, you submit it alongside the CMS-40B (Application for Enrollment in Part B) to your local Social Security office. You can file in person, by mail, by fax, or in some cases online through ssa.gov.

If the employer can no longer fill out Section B (because the company closed, HR can't be reached, or records are unavailable), you can complete Section B as best as possible without signing the employer line and submit it with supporting proof: W-2s showing employer-paid premiums, insurance cards, pay stubs, or Explanations of Benefits. Medicare's enrollment guidance outlines the alternative documentation SSA will accept.

When You Need It (and When You Don't)

You need the L564 if all three of these are true:

- You're 65 or older and eligible for Medicare

- You delayed Part B enrollment because you were covered under a current employer's group health plan (yours or your spouse's)

- You're now ready to enroll in Part B, usually because the job is ending, the coverage is ending, or you're switching off the group plan

You do not need it if you're enrolling during your Initial Enrollment Period at 65, if you never had employer coverage past 65, or if your only coverage was COBRA or retiree health benefits. Neither COBRA nor retiree coverage counts as "current employment" coverage for SEP purposes, a detail that catches a surprising number of people.

The form also has rules around employer size. If the employer has fewer than 20 employees, Medicare typically becomes primary at 65, and delaying Part B may not have been the right move in the first place. The L564 alone won't fix that situation. How the handoff from employer coverage to Medicare actually works covers the 20-employee rule in depth.

I'm turning 65 in three months but still working with employer coverage. Do I need to sign up for Medicare right now or can I wait?

You can wait as long as you are maintaining employer coverage. Medicare part A will still get assigned to you but (as long as you are not receiving SS benefits) not part B. When you do choose to leave employer coverage make sure you visit SSA.gov and “apply for Medicare part B only”. Keep in mind this may take at least a few weeks and you may have to collect some signatures from your employers HR dept so start this process at least a month before you plan on quitting/ leaving employer coverage.The Part B Special Enrollment Period: Why This Form Matters

The SEP gives you up to 8 months after employer coverage ends (or after employment ends, whichever comes first) to enroll in Part B without a late penalty. The L564 is how Social Security verifies you qualify.

Miss that 8-month window and you lose the SEP entirely, get pushed into the General Enrollment Period (January 1 through March 31), and pick up a penalty that never goes away.

| Penalty Type | How It's Calculated | Duration | Impact Example (2-Year Delay) |

|---|---|---|---|

| Part B | +10% added to your monthly premium for every full 12 months you were eligible but didn't enroll, without creditable coverage | Permanent (lifetime) | Base premium jumps from $202.90 to about $243.50/mo |

In 2026, the standard Part B premium is $202.90. A two-year delay adds a 20% penalty, raising the monthly cost to about $243.50 for as long as you have Part B. Three years would mean 30%, pushing it past $264. That penalty shows up on every premium statement for the rest of your life. Real stories from seniors who ended up with lifelong penalties show that most of them came down to one form, one phone call, or one missed deadline.

Where to Get the Form

Three places to get the L564:

- Online: Download directly from CMS.gov as a PDF

- Social Security: Pick one up at your local SSA office or request one by phone

- Your HR department: Many benefits administrators keep copies on hand because the request comes up regularly for employees over 65

You'll also need the CMS-40B, the actual application for Part B. The L564 is the supporting document; CMS-40B is what tells Social Security you want to enroll.

The HR Problem Nobody Warns You About

The biggest holdup with the L564 isn't the form itself. It's getting Section B back from an HR department. Some employers handle it the same day. Others sit on it for weeks, especially if the company is small, if the benefits administrator is offsite, or if the former employee left on bad terms.

A few things that help:

- Ask early. Don't wait until your coverage ends. Start the conversation 60 to 90 days before you plan to enroll in Part B.

- Send the form pre-filled. Complete Section A yourself and email or hand-deliver the form so HR only has to fill in their part.

- If the employer refuses or can't be reached, Social Security will sometimes accept alternate proof: pay stubs showing health insurance deductions, a letter from the insurance carrier, or other documentation. Talk to SSA before assuming you're stuck.

What happens if I am unable to provide creditable coverage?

If you cannot show proof of creditable coverage for a period when you were eligible for Medicare but did not enroll, you face permanent premium penalties that never go away. The Part B penalty adds 10 percent to your premium for every 12 months you went without coverage, and the Part D penalty is calculated on how long you went without creditable drug coverage and gets tacked onto your monthly premium for life. Not all insurance qualifies, so never assume your retiree coverage or other plan meets the standard without verifying it first. If you have a gap or are unsure where you stand, talk to a Medicare agent or your local SHIP counselor before your enrollment deadlines, because fixing this before you enroll is always easier than dealing with penalties after the fact.What If the Employer Is Out of Business?

Companies close. Records get destroyed. People retire from places that no longer exist. Agents handle this scenario more often than you'd expect, and the playbook looks like this:

- Reach out to the plan administrator, not the employer. If the group plan was through a major carrier, that carrier still has enrollment records even when the employer is gone. Call the carrier's group benefits line and ask for a Certificate of Creditable Coverage covering the dates you were insured.

- Pull your old W-2s. If the employer offered group health, your W-2s from those years will show the employer-paid premium in Box 12, code DD. That's not a Notice of Creditable Coverage, but Social Security has accepted it as supporting evidence in cases where the L564 is impossible to obtain.

- Get a SHIP counselor involved. Every state has a free State Health Insurance Assistance Program that can submit an equitable relief request on your behalf. These requests are reviewed case by case, and a clean paper trail showing you tried in good faith is what usually wins them.

- Document everything in writing. Email beats phone calls here. If you have to argue an appeal later, you'll want timestamps and the names of every person you spoke to.

SSA accepts alternative evidence when the L564 can't be completed. Pay stubs, W-2s, insurance cards, and EOBs can all serve as supporting proof of group health plan coverage. The full list of acceptable documentation is outlined in SSA POMS HI 00805.295.

If You're Delaying Part A Too, Read This First

The L564 covers Part B enrollment. Part A is a different conversation. Most people qualify for premium-free Part A at 65 and just take it, even while still on employer coverage. There's usually no cost and no downside.

The exception: Health Savings Accounts. The moment you enroll in any part of Medicare, including premium-free Part A, you lose eligibility to contribute to an HSA. Worse, Part A can be backdated up to 6 months when you enroll later, which can retroactively disqualify HSA contributions you already made. The HSA six-month retroactive rule walks through the trap in detail.

If you're still contributing to an HSA past 65, talk to a tax advisor and a Medicare agent before signing up for Part A. Once it's done, it can't be undone without giving up Social Security entirely. What an HSA can and can't pay for once you're on Medicare covers the spending rules after enrollment.

Can I use a health savings account (HSA) to pay Medicare premiums after I retire?

It’s important to note that once you’re enrolled in in Medicare, you CANNOT make any new contributions to your HSA or you may incur IRS penalties. If you’re enrolling past age 65, your enrollment could be retroactive up to 6 months so one needs to plan carefully. You also CANNOT use HSA funds to pay a Medigap Premium (like plan G or plan F).You can use the EXISTING money to pay for Medicare premiums (A, B and D), deductibles, copays, and coinsurances and other qualified medical expenses like dental, vision or hearing. It requires some careful navigation but EXISTING HSA funds can be a big help in managing the cost of healthcare in retirement.

Common Mistakes That Cost People the Penalty Waiver

Counting COBRA as creditable employer coverage. It isn't, at least not for Part B SEP purposes. The day your active employment coverage ends, your SEP clock starts, even if COBRA picks up the same medical coverage.

Waiting past the 8-month SEP window. The window is shorter than people think. Once it closes, the next chance to enroll is the General Enrollment Period (January 1 through March 31), with coverage starting the month after you enroll and a permanent penalty attached.

Assuming a small employer counts. If the employer has fewer than 20 employees, the SEP rules don't protect you the same way. Medicare expects to be primary, and skipping Part B in that situation can mean both a coverage gap and a penalty. Understanding what actually qualifies as creditable coverage is worth reading before you make the decision to delay.

Filing without Section B completed. Social Security can't process a half-finished L564. If you can't get HR to fill it out, contact SSA before submitting. There are alternate paths, but you need to set them up in advance.

When to Loop In a Local Medicare Agent

The L564 itself is simple. The mistakes that surround it (small employer rules, HSA timing, COBRA confusion, SEP deadlines) are where things get expensive. A licensed Medicare agent in your area can walk through your specific employer situation, confirm you actually qualify for the SEP, and help with the paperwork at no cost to you.

The form is one page. The penalty for getting it wrong lasts forever. Worth the 20 minutes to get it right.

Don't guess on your creditable coverage status. If you're approaching 65 or helping a parent who is, find a licensed Medicare agent in your area who can review your employer plan details and flag any gaps before they become a permanent line item on your premium.