Switching from Medicare Advantage Back to Original Medicare: How It Works, When You Can, and the Medigap Trap to Avoid

-

March 13, 2026

You picked a Medicare Advantage plan, and now something's off. Maybe your doctor dropped the network. Maybe the prior authorizations are piling up. Maybe the "$0 premium" stopped looking like a deal once the out-of-pocket costs started landing. Whatever brought you here, the question is simple: can you go back to Original Medicare, and what's it actually going to cost you?

The short answer is yes, you can switch back. The longer answer is that when you switch matters enormously, and the real risk isn't a penalty from Medicare itself. It's getting denied for a Medigap policy on the way out. This guide walks through the windows, the rules, and the one decision most people get wrong.

Yes, You Can Switch Back

The fear of a "penalty" stops a lot of people from even looking at their options. Medicare does not charge you a fee for leaving a Medicare Advantage plan and returning to Original Medicare. There is no disenrollment fee, no clawback, no black mark on your record.

The penalties people worry about are actually two specific, separate issues:

- The Part D late enrollment penalty — if you drop an Advantage plan that includes drug coverage and don't pick up a standalone Part D plan (or other creditable drug coverage) within the allowed window, you can be hit with a permanent monthly surcharge on future drug coverage.

- Medigap medical underwriting — this is the big one. Outside of a few protected windows, insurance companies can ask health questions and deny you a Medicare Supplement (Medigap) policy based on your medical history. More on that below.

So the switch itself is free. What costs money is switching at the wrong time.

If we choose a Medicare Advantage plan and later regret it, can we go back to Original Medicare without penalties?

Yes.You can switch back to Original Medicare from a Medicare Advantage plan, and there is no penalty for the switch itself.

However, you must enroll in a separate Part D prescription drug plan, or be fined if you decide down the road to switch back to an Advantage plan. You may face new challenges in obtaining a Medigap (supplemental) plan due to potential medical underwriting.

You can make this switch during specific enrollment periods, such as the Annual Enrollment Period (October 15–December 7) or the Medicare Advantage Open Enrollment Period (January 1–March 31).

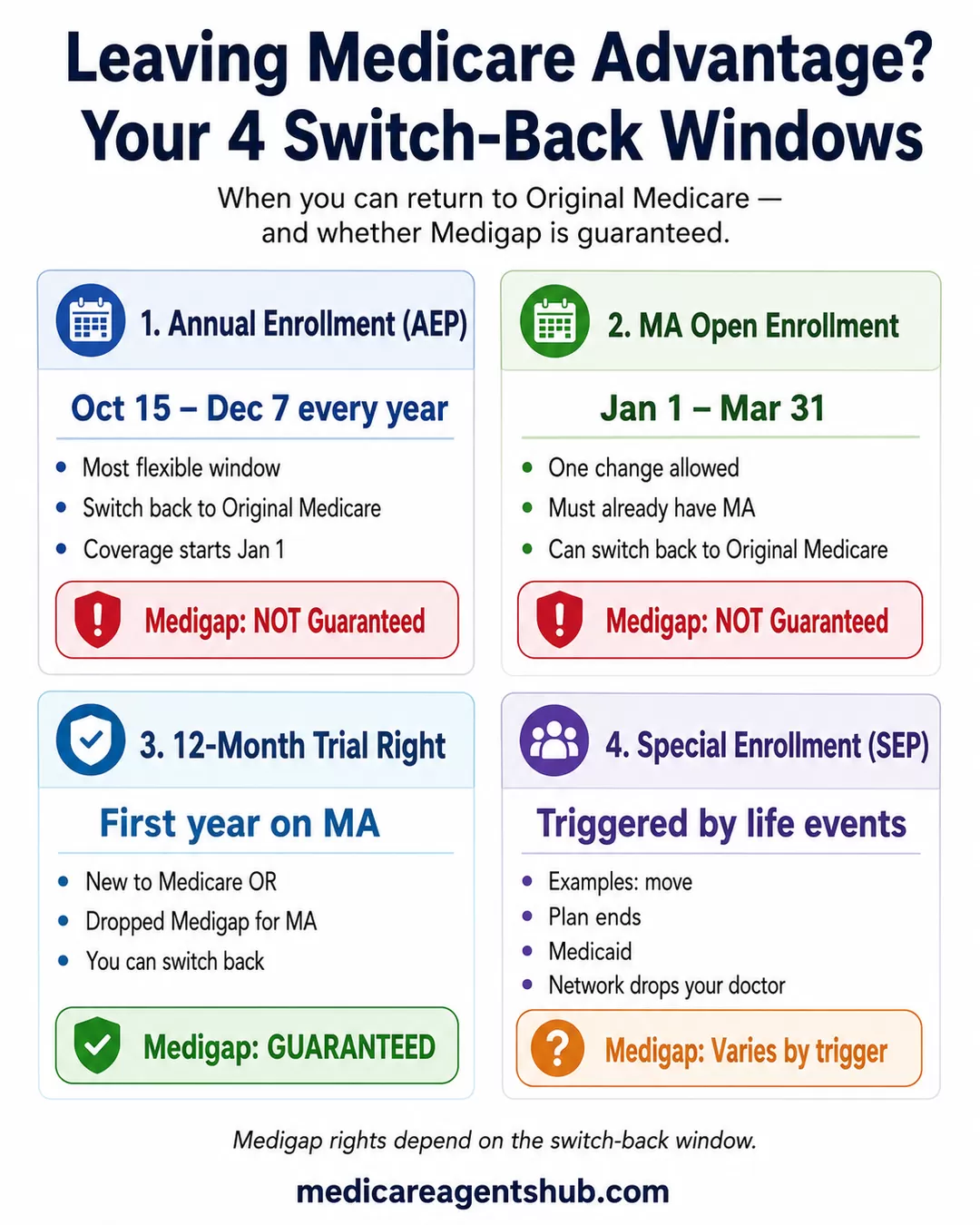

The Four Windows You Can Use to Switch

There are four main opportunities each year (or in your lifetime) to drop an Advantage plan and go back to Original Medicare. Pick the right one and the transition is clean. Pick the wrong one and you may end up on Original Medicare without a Medigap plan to cover the gaps.

1. Annual Enrollment Period (AEP): October 15 – December 7

This is the window most people know about. During AEP, anyone on Medicare Advantage can switch back to Original Medicare, with the new coverage starting January 1. You can also pick a standalone Part D plan during this window to keep drug coverage uninterrupted.

AEP is the most flexible window, but it's also the most crowded. Plans change, commercials run nonstop, and agents are booked solid. If you want help, start the conversation in September.

2. Medicare Advantage Open Enrollment Period (MA-OEP): January 1 – March 31

If you're already enrolled in a Medicare Advantage plan as of January 1, you get a second chance. During MA-OEP you can:

- Switch to a different Medicare Advantage plan, or

- Drop your Advantage plan and return to Original Medicare (and add a standalone Part D plan).

You only get one change during this window, and the new coverage starts the first of the month after the plan receives your request. This is the window to use if you enrolled during AEP and quickly realized the plan wasn't what you thought.

3. The Medicare Advantage Trial Right (First 12 Months)

This is the rule most agents wish more beneficiaries knew about. If you are in one of two specific situations, you have a guaranteed right to drop your Advantage plan, return to Original Medicare, and buy a Medigap policy without answering any health questions:

- You joined Medicare Advantage when you first became eligible for Medicare at 65, and it's been less than 12 months.

- You dropped a Medigap policy to try Medicare Advantage for the first time, and it's been less than 12 months.

Within that 12-month trial period, you have a guaranteed-issue right to a Medigap plan. Outside of it, you may be stuck. If you're within your first year on Medicare and regretting the Advantage choice, do not wait. This window closes on the anniversary of your enrollment and does not reopen.

4. Special Enrollment Periods (SEPs)

Life events can trigger a Special Enrollment Period that lets you leave an Advantage plan outside the normal windows. Common triggers include:

- You moved out of your plan's service area.

- Your plan is leaving Medicare or ending its contract.

- You qualified for Medicaid, Extra Help, or a Special Needs Plan changed.

- Your plan's provider network dropped your doctor or hospital (in some cases).

- You moved into, out of, or are living in a skilled nursing facility.

SEPs usually give you two months to make a change. Rules vary by trigger, so document the event and act fast.

Can I switch from a Medicare Advantage plan to Original Medicare with a Medigap plan mid-year if I’m diagnosed with a serious illness?

The answer to this is no for two reasons.1. You cannot leave your advantage plan in the middle of the year. You can only change from advantage to Original Medicare during the Annual Election Period (October 15th-December 7th), Medicare Advantage Open Enrollment Period (January 1st - March 31st) or under special circumstances such as moving to a new service area.

2. In most states, you have to be able to health qualify for a Medigap plan. This means that having a serious illness would likely disqualify you.

If you are contemplating moving to Original Medicare with a Supplement, I would recommend speaking with an agent now instead of waiting. Trying to change your plan once you are sick will be too late.

The Medigap Trap: The Real Risk in Switching Back

This is the piece that catches more Medicare beneficiaries off guard than anything else. Original Medicare pays roughly 80% of covered Part B services, and there is no annual out-of-pocket maximum. One serious illness can cost tens of thousands of dollars. That's why most people pair Original Medicare with a Medicare Supplement (Medigap) policy, which picks up the coinsurance, copays, and the hospital deductible.

The trap: outside of a guaranteed-issue window, insurance companies can underwrite you for Medigap and say no.

When you first turned 65 and enrolled in Part B, you had a one-time 6-month Medigap Open Enrollment Period where any carrier had to sell you any plan regardless of health. Once that window closed, the rules change in most states:

- Carriers can ask detailed health questions.

- They can deny your application.

- They can charge higher rates based on pre-existing conditions.

- They can impose a look-back period for recent conditions.

This means a senior who dropped Medigap five years ago to try Medicare Advantage, and is now dealing with diabetes, heart disease, or cancer treatment, may switch back to Original Medicare only to discover that no Medigap carrier will take them. They're now exposed to unlimited out-of-pocket costs with no safety net. If you're concerned about Medigap underwriting and coverage denials, it's worth understanding how the process works before you start.

A few exceptions exist:

- The 12-month trial right (described above) guarantees a Medigap policy.

- Some states have their own rules. New York, Connecticut, Maine, Massachusetts, and Washington have continuous or annual guaranteed-issue protections. Several other states have Medigap "birthday rules" that let you switch plans once a year without underwriting.

- Certain SEPs (like a plan ending its Medicare contract) can trigger guaranteed issue.

The bottom line: before you drop your Advantage plan, find out whether you can actually qualify for the Medigap plan you want. Apply for the Medigap policy first, get the approval in hand, then disenroll from Advantage. Doing it in the other order can leave you stuck.

Can I switch from a Medicare Advantage plan to a Supplemental/Medigap plan during the Annual Enrollment Period without answering health questions?

This is one of the most misunderstood parts of Medicare. The Annual Enrollment Period (AEP) only lets you switch between Medicare Advantage plans or change your drug plan. It does not guarantee that you can move from a Medicare Advantage plan to a Medicare Supplement (Medigap) without health questions.To enroll in a Medigap plan without medical underwriting, you need a Guaranteed Issue (GI) right — and those are limited. Most people only get GI rights when they’re first turning 65, leaving employer coverage, or if their Advantage plan is terminating. Outside of those situations, if you try to switch from Medicare Advantage to a Medigap plan, the insurance company can require health questions and can deny the application based on medical history.

So yes, you can apply for a Medigap plan during AEP — but unless you have a GI right, you’ll typically need to go through underwriting.

Don't Forget Part D

Most Medicare Advantage plans bundle in prescription drug coverage (that's the "MA-PD" part you see on plan names). When you go back to Original Medicare, that drug coverage ends with the Advantage plan. You need to pick up a standalone Part D prescription drug plan to keep coverage.

If you go more than 63 days without creditable drug coverage, you'll face the Part D late enrollment penalty: a permanent surcharge added to your Part D premium for as long as you have Medicare drug coverage. The math works out to about 1% of the national base premium per month you went without coverage, compounded for life.

When you use a valid switch window (AEP, MA-OEP, trial right, or SEP), you can enroll in a Part D plan at the same time without penalty. The trick is making sure the paperwork actually gets filed. Don't assume dropping Advantage auto-enrolls you in a Part D plan. It doesn't.

The Switch-Back Checklist

Before You Drop Your Medicare Advantage Plan

- Confirm your switch window. Are you in AEP, MA-OEP, your 12-month trial right, or a valid SEP? If not, wait.

- Check Medigap eligibility. Apply for the Medigap policy you want. If you're within a guaranteed-issue window, great. If not, get underwriting approval before you disenroll from Advantage.

- Pick a Part D plan. Compare standalone Part D plans on Medicare.gov using your current medication list. Enroll as part of the switch.

- Confirm your doctors take Original Medicare. Most do (99% of non-pediatric physicians accept it), but verify before assuming.

- Time the effective dates. Medigap and Part D should start the same day your Advantage plan ends. Gaps of even a few days can trigger penalties or leave you exposed.

- Disenroll from Advantage last. Enrolling in Original Medicare-compatible coverage (a new Part D plan, for example) automatically disenrolls you from most Advantage plans. You usually don't need to call the Advantage carrier separately.

Why do some people regret choosing a Medicare Advantage plan over Original Medicare?

In my years of experience three main regrets are common: **Usually, the person was not told these below restrictions will be part of their respective MA/MAPD plan1) inability to switch back to a Medicare supplement with preexisting conditions (unless a guaranteed issue special enrollment criteria is met)--not a common option for very sick folks. Meaning most sick folks can change from one MAPD to another in the fall AEP, but not back to Original Medicare with a Medicare Supplement in most circumstances (cancer, stroke, COPD, heart attack, nitroglycerin, insulin, dementia, etc).

2) large yearly maximum out of pocket (MOOP) charges: such as 20% co-pays for chemotherapy, DME, etc. Some PPO plans have a smaller in network MOOP (i.e. $4900) and out of network MOOP ($10,000).

3) network restrictions of some HMO plans and large co-pays for out of network PPO plans.

When Switching Back Might Not Be Worth It

To be fair, Medicare Advantage isn't universally bad, and going back to Original Medicare isn't always the right call. Advantage plans can make sense for beneficiaries who:

- Are healthy and want low monthly premiums with predictable copays.

- Rely heavily on the extra benefits Advantage plans bundle in, like dental, vision, hearing, fitness, and OTC cards.

- Can't qualify for a Medigap policy due to health history and would face unlimited out-of-pocket exposure on Original Medicare.

- Live in an area with strong local Advantage networks and are happy with the providers.

If you're simply frustrated with your current plan, switching to a different Advantage plan during AEP or MA-OEP may fix the problem without forcing the bigger Medigap conversation. Not every problem needs a return to Original Medicare, but when it does, timing is everything. Medigap.

When to Call a Medicare Agent

This is a decision where the help of a licensed, independent Medicare agent is worth more than almost any other. A good agent will:

- Tell you which Medigap carriers will actually approve you, based on your health history.

- Run the underwriting before you disenroll from Advantage.

- Time the effective dates so you have no coverage gap.

- Compare standalone Part D plans against your medication list.

- Know your state's specific rules (birthday rule, annual guaranteed-issue windows, etc.).

You can find a licensed independent Medicare agent in your area using the Medicare Agents Hub directory. Most agents don't charge you directly (they're paid by the insurance company), so a second opinion costs nothing.

Bottom Line

You can switch from Medicare Advantage back to Original Medicare. The enrollment itself is free and straightforward. The real work is making sure you land softly on the other side, with a Medigap policy that accepts you, a Part D plan that covers your medications, and effective dates that line up. Do those three things and you're good. Skip any of them and you can end up worse off than you were on the plan you're leaving.

If you're in your 12-month trial right window, the clock is ticking. If you're not, start with the Medigap application, not the Advantage disenrollment form.