Navigating Medigap: Rate Hikes & Coverage Denials

We are coming off of what may be the most disruptive two years in Medicare's sixty-year history. As we start a new year, it feels like the right time to give you a high-level look at the Medicare landscape and some of the challenges I see for seniors in 2026. Think of this as one of those "State of the Industry" updates for Medicare.

I want to focus on three key areas:

- The recent surge in Medigap premiums.

- The differences between Medigap and Medicare Advantage.

- How to handle Medigap underwriting and pre-existing conditions.

Here we go...

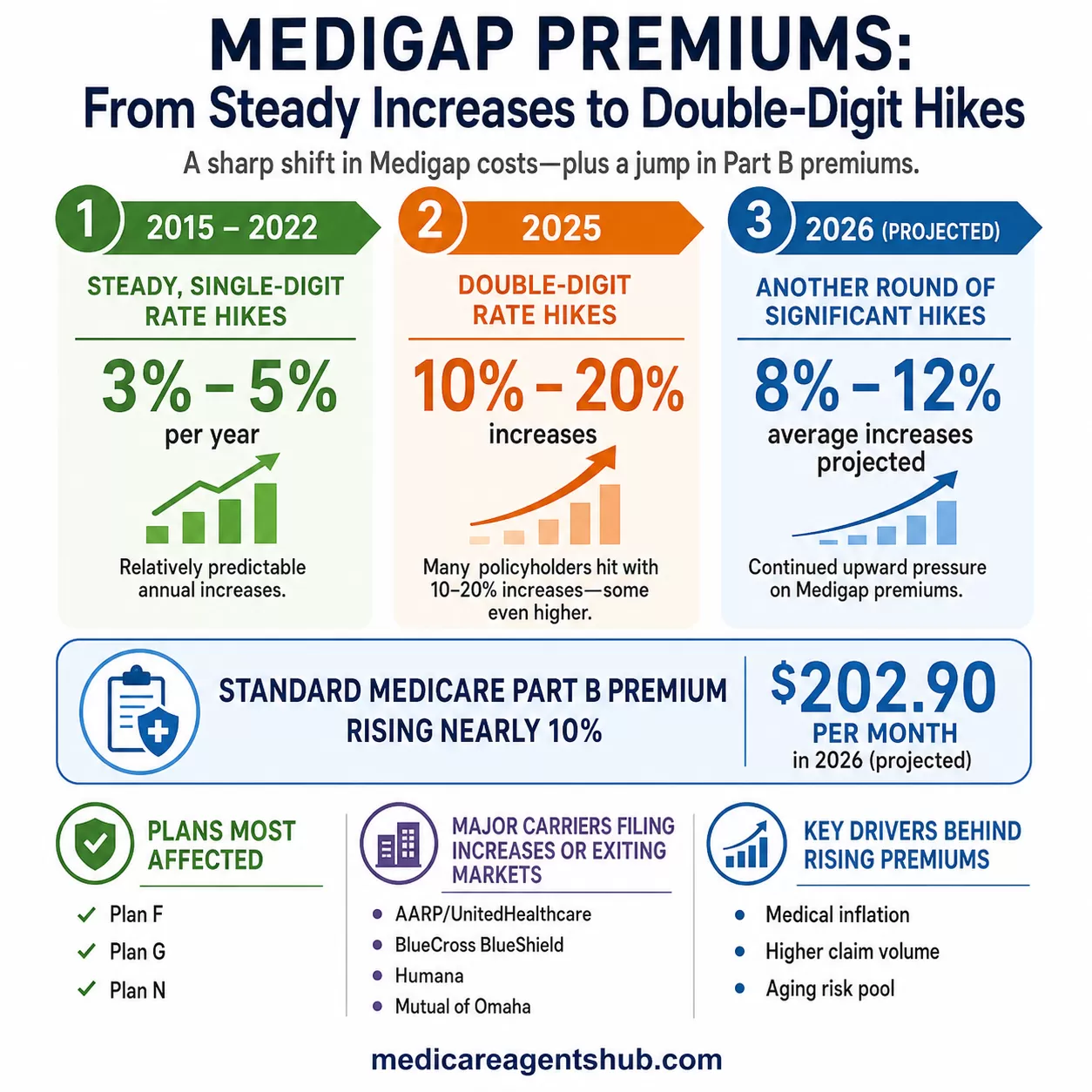

Why Are Medigap Premiums Surging?

Medicare Supplement premiums are on the rise again, and the increases are sharper than what we've seen in the past. We used to see steady, predictable hikes of 3-5% from 2015 to 2022. That pattern has changed.

Many policyholders were hit with 10-20% increases in 2025, and some faced even higher spikes. Following these trends, we can expect average hikes of 8-12% in 2026. This is happening at the same time the standard Medicare Part B premium is increasing by nearly 10% to $202.90 per month.

So, what’s causing this? A few factors are at play, including medical inflation, a higher number of claims, and an aging risk pool. These forces are driving up costs for popular Medicare Supplement policies like Plan F, Plan G, and Plan N. As a result, major carriers like AARP/UnitedHealthcare, BlueCross Blue Shield, Humana, and Mutual of Omaha have either left certain markets or filed for significant rate increases that affect millions.

It's a tough spot to be in. You pay your premiums faithfully, only to get hit with a massive increase. Or, you try to switch to a more affordable plan and get denied because of a health condition.

While these rate hikes are not ideal, you can manage them by staying proactive. A double-digit increase can strain any budget, so it's essential to review your plan every year. If your premium jumps, let's compare what other carriers can offer. We have the resources to help you find potential savings.

Is paying for a high-end Medicare Supplement plan really worth it, or is it overkill?

Are Medicare Supplements worth it? In many cases, yes — absolutely. And it’s not always a math problem. A big part of this decision is about control over your healthcare and how much uncertainty you’re willing to live with.The phrase that stands out in your question is “high-end,” as if a Medicare Supplement (Medigap) is a luxury item. If your premiums truly feel high, that’s worth reviewing — sometimes there is room to fix or optimize that. But “high-end” often just means more comprehensive and predictable, not extravagant.

It’s also important to remember that Medicare Advantage plans aren’t really “free.” They come with copays, coinsurance, and out-of-pocket limits that can add up quickly when you actually need care. Over time, the choice often comes down to this: pay more upfront with a Medigap plan for consistency and peace of mind, or pay as you go with an Advantage plan and accept more financial surprises.

And here’s a telling litmus test: ask doctors and independent Medicare brokers what coverage they would choose for themselves. The honest answer from most? A Medicare Supplement, without hesitation.

Medigap vs. Medicare Advantage: Which is Right for You?

The choice between Medigap and Medicare Advantage often comes down to freedom versus frills. Understanding the core differences can help you decide which path offers the right long-term security for you.

The Case for Medigap: Freedom and Predictability

Medigap plans offer unparalleled freedom. You can see any doctor or visit any hospital that accepts Medicare in the United States. There are no networks to worry about and you don't need a referral to see a specialist. This is ideal for frequent travelers or seniors managing chronic health conditions. With Medigap, you get nationwide flexibility and predictable costs, which means fewer surprises when a medical bill arrives.

However, Medigap does have some downsides. The premiums are generally higher, a fact made more apparent by the recent rate hikes. You will also need to purchase separate plans for Part D prescription drug coverage and other benefits like dental or vision care.

The Case for Medicare Advantage: Bundled Benefits

Medicare Advantage plans are often appealing because of their low or zero-dollar monthly premiums. They also bundle extra benefits, like routine dental, vision, and hearing coverage, into one convenient plan.

The trade-off comes with restrictions. Most Advantage plans have provider networks, which limit your choice of doctors and hospitals. You may also need prior authorization for certain procedures, which can delay care. While these plans look attractive with their bundled benefits, I've seen too many people regret the switch when they can't see their preferred specialist or face unexpected out-of-pocket costs.

If you are healthy and plan to stay local, a Medicare Advantage plan might be a good fit. But for long-term peace of mind and flexibility, Medigap is often the better choice. And remember, switching back to Medigap after being on an Advantage plan may require medical underwriting.

Overcoming Medigap Denials and Pre-Existing Conditions

Switching from a Medigap policy to a Medicare Advantage plan might lower your monthly premium, but returning to Medigap later is not always simple. In most cases, it requires medical underwriting, which can lead to a denial if your health has changed.

Too many people are tempted by the low premiums of Advantage plans without understanding this risk. My goal is to help you look at your specific situation and find a solution that protects both your healthcare access and your finances for the long run.

Why Do Denials Happen?

The most common reason for a Medigap denial is applying outside of an enrollment period that offers guaranteed acceptance. Your six-month Medigap Open Enrollment Period is your golden window. This period starts the month you're 65 or older and enrolled in Medicare Part B. During this time, insurance companies cannot deny you a policy or charge you more due to your health.

Outside of this window, and with only a few exceptions, you will face medical underwriting. The insurance company will scrutinize your health history for pre-existing conditions like cancer, COPD, diabetes complications, or heart issues.

Don't panic if you've been denied. You may still have options. Certain situations grant you "guaranteed issue rights," which allow you to buy a policy without underwriting. Exploring alternative carriers may also be a solution. A denial is not always the end of the road, but it's a situation that requires careful navigation.

Strategies for Success in 2026

The Medicare landscape is constantly changing, and it can feel overwhelming. But you have options, whether you're trying to avoid rate hikes or deciding between Medigap and Medicare Advantage.

Here are a few strategies to help you succeed:

- Budget for Increases: Whether you have Medigap or Medicare Advantage, plan for rising costs. A good rule of thumb is to set aside an extra 5-10% in your budget for premiums and out-of-pocket expenses.

- Act During Open Enrollment: If you are in your six-month Medigap Open Enrollment Period, now is the time to act. Lock in a plan with guaranteed acceptance to secure your coverage.

- Review Your Coverage Annually: Don't "set it and forget it." Your health needs and the plans available can change each year. Work with a trusted, independent broker who can provide multi-carrier comparisons.

- Get Help If You Need It: If you receive a denial notice or a significant rate increase, let's look at your options together.

Knowledge is your best tool for navigating Medicare. Understanding your choices can save you hundreds — or even thousands — of dollars a year and give you lasting peace of mind.

About the Author:

Rodney Powell is the #1 Top Rated Local Medicare Agent for Texas in 2025 with Medicare Agents Hub. "Do It Yourself" isn't a Medicare plan. A FRIEND to come alongside you is priceless. Rodney Powell, the "Medicare Video Guy" - is that person for you. Licensed in 30+ states - he never charges a consultation fee.

Powell has gained a following for his guidance on Medicare Supplement (Medigap), Advantage plans, and prescription drug coverage.

His online resource, MedicareVideoGuide.com, has earned over 50 five-star Google reviews — 100% testament to the trust and satisfaction of the people he serves. For those seeking clarity and confidence in their Medicare choices, he is a trusted advocate who makes Medicare work for people.