Is Medigap the Same as 'Secondary Insurance'? 65 Agents Can't Agree

-

May 28, 2026

We put a simple question to 65 licensed Medicare agents: Are Medicare Supplement plans the same thing as "Medicare secondary insurance"?

The answers split almost down the middle. Some said yes without hesitation. Others said absolutely not. A third group tried to thread the needle. The disagreement wasn't just academic. The vocabulary trap can cost people real money when employer coverage, TRICARE, Medicaid, COBRA, or VA benefits enter the picture. And the confusion starts at the front desk of every doctor's office in America.

65 Agents, Three Camps, One Clearer Answer

When we tallied the responses, here's how the split looked:

About one in four agents said yes, flat out. To them, Medigap, Medicare Supplement, and secondary insurance are interchangeable terms. Paul Barrett, a licensed agent in Melville, New York, summed up this camp: "Medicare Supplement, secondary insurance, Medigap — all three are essentially the same thing in the Medicare world."

Another roughly one in three gave a more precise answer: Medigap is a type of secondary insurance, but secondary insurance is a much bigger category. Terry Nacion, an agent in Henderson, Nevada, put it clearly: "Medicare Supplement plans, also called Medigap, are a type of secondary insurance, but not all secondary insurance is a Medicare Supplement plan."

The remaining agents either said no outright or gave answers that sidestepped the question entirely. And a few got the mechanics flat wrong, which we'll get to.

Why the "Yes" Camp Isn't Wrong (Just Incomplete)

The agents who said "yes" are thinking about billing order, and in that narrow sense, they're correct. When you have Original Medicare plus a Medigap plan, here's exactly what happens when you visit a doctor:

- Medicare processes the claim first (primary payer)

- Your Medigap plan picks up part or all of the remainder (secondary payer)

- You pay whatever's left, which on a Plan G is often nothing beyond the annual Part B deductible

Tyler Haskell, an agent in Payson, Utah, described the relationship in a way that sticks: "They piggyback off of original Medicare. Original Medicare runs the show, what they say goes. If they pay for it, the secondary has to pay its part. If Original Medicare doesn't pay, the supplement will not pay either."

Patricia Lewis in Sarasota, Florida, added the numbers: Medigap helps cover "the $1,736 deductible for being hospitalized, as well as the 20% on Part B that has no max out-of-pocket." That last part — no max out-of-pocket on Original Medicare — is exactly why people buy Medigap in the first place, and why agents who understand that nuance tend to recommend a supplement plan. If the premium math on Medigap seems steep, consider what 20% of a $300,000 surgery looks like without it.

Are Medicare Supplement plans the same thing as "Medicare Secondary Insurance"?

Yes. The reason a Medicare Supplement would be referred to as "Medicare Secondary Insurance" is because Medicare would be your primary insurance coverage and the Medicare Supplement would be your secondary insurance. Medicare pays first and then the supplement pays second. Important to note... the supplement will pay the balance after Medicare pays according to the "Plan Letter" of supplement you chose (i.e. Plan G, Plan N, etc.).The Agents Who Got It More Right: All Squares Are Rectangles

The more precise agents recognized something the "yes" camp glossed over. Medigap is one type of secondary insurance. But secondary insurance is a broad category that includes several types of coverage that work nothing like a Medigap plan.

Are Medicare Supplement plans the same thing as "Medicare Secondary Insurance"?

All Medigap plans are secondary to Medicare -but not all secondary insurance is Medigap.

“secondary insurance” describes how a plan pays, not what kind of plan it is.

Here are some examples of secondary insurance:

Employer or retiree health coverage

Union plans

VA benefits

Tricare

Medicaid

Dustin Haffner, an agent in Grove, Oklahoma, nailed the distinction that matters: "secondary insurance" describes how a plan pays, not what kind of plan it is. Any coverage that pays after another insurer has already paid its share qualifies as "secondary." Medigap is one flavor. There are at least five others.

Five Types of Secondary Coverage That Aren't Medigap

This is where the "yes, same thing" answer starts causing problems. Each of the following is commonly confused with "secondary insurance" in a Medicare situation, though some coordinate with Medicare directly and others, like VA benefits, operate separately. Each one follows completely different rules than a Medigap plan:

1. Employer or Retiree Group Coverage

If you're still working at 65 and your employer has 20 or more employees, your employer plan is actually primary and Medicare is secondary. That's the opposite of how Medigap works. If you retire and keep retiree coverage, the roles typically flip — Medicare becomes primary and the retiree plan pays second. The coordination rules depend entirely on employer size and your employment status.

2. TRICARE For Life

Military retirees who enroll in Medicare Parts A and B get TRICARE For Life as automatic secondary coverage. In the common Medicare + TFL setup, it works similarly to Medigap in that Medicare pays first, but the enrollment rules, cost-sharing, and pharmacy benefits are completely different. If someone also carries other health insurance alongside Medicare and TFL, TRICARE may pay last after both Medicare and the other insurer. You don't shop for it, you don't pick a plan letter, and it covers things Medigap never will.

3. Medicaid

For people who qualify for both Medicare and Medicaid ("dual eligibles"), Medicaid acts as the payer of last resort. It picks up costs after Medicare and any other insurance have paid their share. The coordination between Medicare and Medicaid follows its own set of federal and state rules that look nothing like Medigap billing.

4. VA Benefits

Here's where it gets tricky. VA benefits and Medicare don't coordinate at all in the traditional sense. The VA is a separate healthcare system. If you see a VA doctor, Medicare doesn't pay and the VA doesn't bill Medicare. If you see a civilian doctor, Medicare is primary and the VA typically isn't involved. Calling VA benefits "secondary insurance" is technically inaccurate, though many people use both systems side by side.

5. Union Plans and COBRA

Union retiree benefits and COBRA continuation coverage can both function as secondary to Medicare, but their coordination rules depend on the specific plan terms. COBRA in particular is a trap. It usually does not protect you the same way active employer coverage does for delaying Medicare Part B, and relying on it after 65 can leave you exposed to gaps, limited COBRA payment, or late enrollment penalties. COBRA drug coverage may be creditable for Part D, but that is a separate issue.

Are Medicare Supplement plans the same thing as "Medicare Secondary Insurance"?

All Medicare Supplements are secondary insurance, however not all secondary insurance is a Medicare Supplement. Medicare supplements assist in cost that Original Medicare (Parts A & B) does not fully cover.Medicare Secondary Insurance is a broad term which means that it will pay after Medicare does. Beside Medicare Supplements there are other coverages that individuals may have, such as: Employer or retiree group coverage, TRICARE For Life, Medicaid, Union Benefits, or COBRA.

It is best to talk with a licensed agent in your area to help you understand and explore the best options for your unique situation.

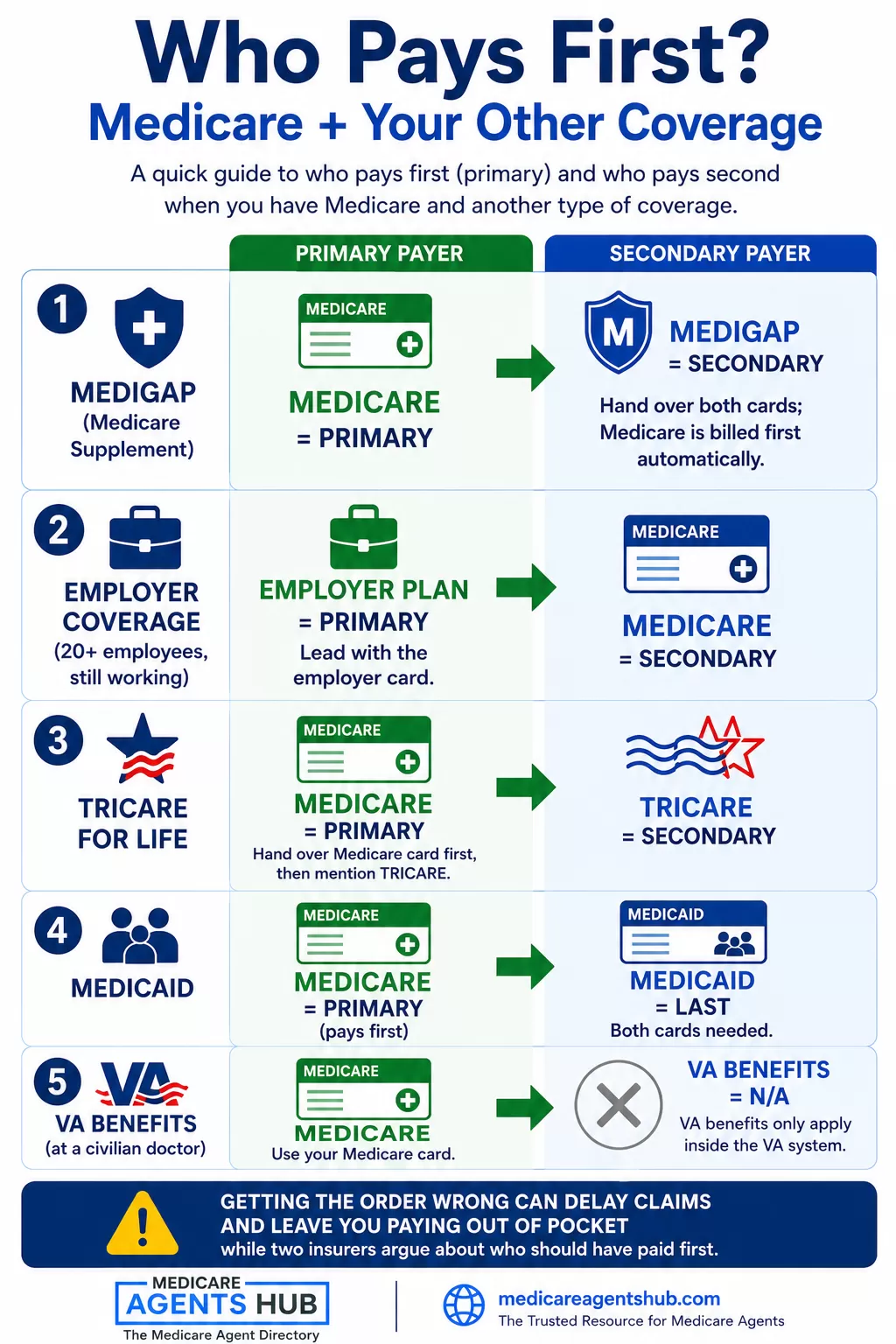

What to Say When the Front Desk Asks

If you walk into a doctor's office and someone asks "do you have secondary insurance?", here's what they're actually trying to figure out: who pays after Medicare?

Your answer depends on your actual coverage:

- If you have a Medigap plan: "Yes, I have a Medicare Supplement plan" — and hand them both your Medicare card and your Medigap card. Medicare gets billed first, automatically.

- If you're still working with employer coverage (20+ employees): Your employer plan is actually primary, not secondary. Medicare is your secondary. Lead with the employer card.

- If you have TRICARE For Life: Medicare is primary, TRICARE is secondary. Hand them the Medicare card first, then mention TRICARE.

- If you have Medicaid: Medicare pays first, Medicaid pays last. Both cards needed.

- If you have VA benefits: At a civilian doctor, Medicare is your insurance. VA benefits only apply within the VA system.

Getting the order wrong doesn't just cause paperwork headaches. It can delay claims, trigger incorrect billing, and leave you paying out of pocket while two insurers argue about who should have paid first.

The 20-Employee Rule That Reverses Who Pays First

One of the most consequential details buried in the agent answers is the 20-employee threshold that determines billing order when someone is still working past 65.

If your employer has 20 or more employees: Your employer plan is primary. Medicare is secondary. You can typically delay Part B enrollment without penalty.

If your employer has fewer than 20 employees: Medicare is primary. Your employer plan is secondary. You need to enroll in Parts A and B at 65 or risk a permanent late enrollment penalty.

These are the general rules, but coordination of benefits can vary when disability, ESRD, retiree coverage, or multi-employer plans are involved. Confirm with your employer's benefits administrator to be sure.

I'm turning 65 in three months but still working with employer coverage. Do I need to sign up for Medicare right now or can I wait?

As long as you are working for an employer of 20 + employees you do not have to sign up for medicare.You group plan would be primary

If under 20 employees then you need to sign up for A&B

Aa medicare would be primary

If you havw an HSA plan do not sign up for medicare until you retire.

I recommend that when you decide to retire to sign up for medicare 3 months prior to retirement

Notice what's happening here. In the "under 20" scenario, your employer plan is functioning as secondary insurance to Medicare — but it's an employer plan, not a Medigap plan. This is exactly the situation where treating "secondary insurance" and "Medigap" as the same thing leads people astray. Someone with an employer plan that pays after Medicare has secondary coverage, but they do not have a Medigap plan, and the billing, networks, and cost-sharing rules are different.

Amine Amraoui, an agent in Clearwater, Florida, flagged why this matters at the front desk: "Sometimes calling it that can cause confusion, because if let's say you have employer coverage, sometimes your employer coverage is primary, and Medicare would be secondary." The terminology reversal confuses patients, office staff, and billing departments alike.

Where Wrong Answers Get Expensive

Most of the 65 agents gave answers that were at least partially correct. But a few responses contained errors that could cost someone money if acted on.

One agent stated that "if you choose a Medicare Supplement it becomes your primary insurance and Medicare is your secondary." That's backwards. Medicare is always the primary payer when you have a Medigap plan. The supplement never pays first. If you handed your Medigap card to a doctor's office and told them it was your primary insurance, the claim would be processed incorrectly and you'd likely get a bill for the full amount while it gets sorted out.

Another agent said "a supplement plan is not health insurance" — meaning it only supplements Medicare and doesn't function as standalone coverage. That's technically true in spirit (you can't use Medigap without Medicare), but calling it "not health insurance" could lead someone to think it doesn't count toward their coverage needs when making enrollment decisions.

A third agent said Medicare secondary insurance "has nothing to do with private carrier Medigap/Supplement" plans — defining secondary insurance exclusively as the employer plan scenario and excluding Medigap from the category entirely. That's the mirror image of the mistake the "yes" camp makes. Medigap is absolutely a form of secondary insurance. It's just not the only form.

How TRICARE For Life Actually Works as Secondary Coverage

The TRICARE scenario deserves its own section because it's one of the most common and least understood forms of Medicare secondary coverage. Military retirees often assume TRICARE and Medicare are either/or. They're not.

Can you explain how Medicare works with other types of insurance like Veterans Affairs benefits or employer plans?

I am Retired Military and have Tri-Care. When I turn 65, I must enroll into Medicare Parts A & B. Medicare will be Primary and TriCare For Life will be secondary. I am also 100% Service-Connected Disabled through the VA. I will also need Medicare Parts A & B for providers and care outside of the VA and VA Network. The VA Network is no different than any other networks (Optum, Humana, Anthem, etc) in that it changes Network Providers from time to time and the patient has no control over the network care restrictions. If a Veteran gets all of their prescriptions from the VA or TriCare For Life, Medicare exempts them from enrolling into Medicare Part D. If a case ever arose requiring the Veteran to enroll in Medicare Part D, they will be required to fill out paperwork from Medicare which will exclude them from paying a Medicare Part D Late Enrollment Penalty.When a retiree 65 or over leaves their company, the vast majority of the time they will have no employer health coverage exclusive of Medicare Parts A & B. Therefore, the retiree must enroll into Parts A, B, & C (Medicare Advantage with Drug Coverage) or A,B, & D with a Medicare Supplement.

This may sound convoluted and confusing, but is better accomplished when talking to an agent face to face who has a clear understanding of the VA and Tricare systems and their respective relationships to Medicare (based on current guidelines)

Christopher Boyd, a retired military agent licensed in Indiana, described his own situation: Medicare will be primary, TRICARE For Life will be secondary, and his VA benefits operate as a completely separate system. That's three layers of coverage that each follow different rules — and none of them is a Medigap plan. Calling all of that "secondary insurance" without distinguishing between the types is where the vocabulary breaks down.

Frequently Asked Questions

Is Medigap secondary insurance?

Yes. In standard Original Medicare + Medigap billing, Medicare pays first as the primary payer and your Medigap plan pays second, covering part or all of the remaining costs.

Is all secondary insurance Medigap?

No. Employer coverage, retiree plans, Medicaid, TRICARE For Life, COBRA, and other arrangements may also pay after another payer, depending on the situation. Each follows its own coordination rules.

Can I use Medigap with Medicare Advantage?

No. Medigap is designed to work with Original Medicare only, not Medicare Advantage. You need Original Medicare Parts A and B to buy and use a Medigap plan.

Who should I show first at the doctor's office?

Show every insurance card you have and explain the type of coverage. The billing office needs to know which payer is primary and which is secondary to process your claim correctly.

The One Sentence That Clears It Up

Roughly a third of the 65 agents landed on the same formulation, phrased different ways: All Medigap plans are secondary insurance, but not all secondary insurance is a Medigap plan.

Brandon Brown, an agent in Lexington, Kentucky, added a practical distinction: "If you're buying it yourself specifically to fill Medicare's gaps, it's a Medicare Supplement. But not all 'secondary insurance' is a Medigap plan — some people might have secondary coverage through a retiree plan, Medicaid, or an employer too."

The vocabulary confusion isn't harmless. It's one of many questions most seniors don't think to ask but should. When someone transitions from employer coverage to Medicare, they need to understand exactly which type of secondary coverage they had, which type they're moving to, and how the coordination of benefits changes. A local, independent Medicare agent can walk through your specific situation and make sure you're not handing the wrong card to the wrong person at the wrong time.