You Paid Into Medicare for 40 Years. You Can Still Be Denied Medigap. Here’s Why

-

July 18, 2026

Reviewed by Rodney Powell

Medicare Broker Licensed in TX, AK, AL & 29 other states

You paid Medicare taxes for 40 years. Now a private insurance company says you can’t buy a Medigap plan because of your health. It feels wrong. It might even feel illegal. It isn’t.

Every Medicare agent hears this. It’s one of the most common misunderstandings in the whole program, and it’s also one of the most emotionally charged. The short version: the Medicare card in your wallet is federal. The Medigap policy is private. Two different products, two different rulebooks.

Can a Medigap plan deny you for a pre-existing condition?

Yes. Outside of specific protected enrollment periods, a Medigap carrier can review your health history and decline your application or charge a higher premium. This applies even if you’ve been on Medicare for years. The protection against health-based denials only exists during certain windows defined by federal and state law.

Medicare is federal. Medigap is private insurance.

This is the line almost every agent draws first. Your work history and Medicare taxes generally qualify you for premium-free Part A. Part B is federal Medicare coverage too, but most people pay a monthly Part B premium. Neither Part A nor Part B uses medical underwriting. That coverage cannot be denied for health reasons.

Medigap is a different product. It’s sold by private insurance companies to help pay the deductibles and coinsurance that Original Medicare leaves you responsible for. Because Medigap is private insurance, carriers in most states may use medical underwriting outside federal or state protected enrollment periods.

I applied for a Medigap plan and got denied because of my health history-how is that even legal when I've paid into Medicare for years?

I hear this concern a lot, and it can definitely feel frustrating and confusing.The key thing to understand is that Original Medicare (Part A and Part B) is guaranteed coverage based on your work history and taxes paid — and you cannot be denied that coverage due to health history. However, Medigap (also called Medicare Supplement insurance) is a separate private insurance policy, and that’s where underwriting rules can come into play.

In most states, Medigap plans are only guaranteed issue during specific enrollment windows, such as your initial Medigap Open Enrollment Period (which starts when you’re 65 or older and enrolled in Part B). Outside of that window, insurance companies in many states can review your health history and may approve, deny, or charge higher premiums based on medical underwriting.

There are exceptions. Some situations create guaranteed issue rights — such as losing employer coverage, moving out of a plan’s service area, or certain plan changes — which can give you another chance to get Medigap coverage without health questions.

So while it may feel unfair compared to Medicare itself, Medigap is regulated differently because it’s optional private insurance, not federal coverage.

If you’ve been denied, it’s worth reviewing whether you qualify for a guaranteed issue period or exploring alternative coverage options like Medicare Advantage. A licensed Medicare agent can walk you through those options and help you understand what you’re eligible for right now.

Your work history and Medicare taxes generally qualify you for premium-free Part A. They don’t purchase a separate Medigap policy from a private insurer.

Why federal law lets carriers say no

Medigap is governed by both federal and state law. Federal law creates baseline protections, including the six-month Medigap Open Enrollment Period and certain Guaranteed Issue rights. State insurance departments regulate the companies selling the policies and may provide additional protections.

Congress created a federally protected enrollment window when you first become eligible, but outside that window, carriers in most states can require medical underwriting: a health questionnaire, prescription history checks, sometimes an interview.

Depending on the carrier, active cancer treatment, a recent stroke, certain heart or lung conditions, or diabetes with particular complications may result in a denial. Each insurer applies its own underwriting guidelines. Some will offer coverage at a higher rate. Others will decline outright.

The 6-month window where underwriting is turned off

Your federal Medigap Open Enrollment Period lasts six months, beginning the first month you are 65 or older and enrolled in Part B. During that period, an insurer must sell you any Medigap policy it offers and cannot deny you or charge more because of your health. A pre-existing condition waiting period of up to six months may apply, but it can be reduced or eliminated by prior creditable coverage, and it cannot be imposed when someone purchases under a federal Guaranteed Issue right.

Miss those 6 months and the door closes in most states. Agents call this the enrollment cliff, and it’s why every serious Medicare conversation starts with your Part B effective date.

Is Guaranteed Issue available after the Medicare Open Enrollment period ends?

It depends, but in general the answer is no — Guaranteed Issue is only available in specific situations. Once the Medicare Supplement Open Enrollment Period ends, a person does not automatically have Guaranteed Issue rights. They only receive Guaranteed Issue protection if they experience a qualifying event, such as losing certain types of coverage, moving out of a plan’s service area, or using a trial right. Outside of Open Enrollment and outside of those specific Guaranteed Issue situations, a carrier can require medical underwriting.If you’re inside that window right now, apply. If you’re not, the next section is the one that matters.

The Guaranteed Issue events that override underwriting

Federal law recognizes a handful of situations where you get a second shot at Medigap without answering health questions. These are called Guaranteed Issue rights. Depending on the qualifying event, your application window may begin as early as 60 days before your existing coverage ends and generally closes 63 days after it ends. The Medigap plans you are guaranteed the right to purchase can also vary by event.

Common Guaranteed Issue triggers:

- Your Medicare Advantage plan leaves the market or ends its contract with Medicare

- You move out of your Medicare Advantage plan’s service area

- Certain employer or union coverage that supplements Medicare ends

- Your Medigap carrier goes bankrupt or ends the policy through no fault of yours

- You leave a Medicare Advantage plan because the company misled you or broke the rules

- You’re in your first year of a Medicare Advantage plan and want to switch back to Original Medicare (the Medicare Advantage trial right)

Federal law provides different Medicare Advantage trial rights. If you dropped a Medigap policy to join Medicare Advantage for the first time, you generally have one 12-month opportunity to return to your former Medigap policy if it is still available. A separate trial right may apply if Medicare Advantage was your first coverage choice when you became eligible at 65. The Medigap policies available depend on the situation, eligibility date and state law.

State exceptions: birthday rules, anniversary rules, and year-round enrollment

A growing number of states provide additional opportunities to buy or switch Medigap coverage without medical underwriting. These include birthday periods, anniversary periods, annual enrollment opportunities, and broader year-round protections. California, Connecticut, Oregon, Idaho, Maryland, and Maine are among the states with some form of additional protection, and New York skips underwriting entirely with year-round guaranteed access.

Because the list and individual rules continue to change, this is worth checking annually. Our full breakdown of state Medigap birthday and anniversary rules covers who qualifies where, or check with your state insurance department.

Denied by one carrier? Apply with another.

This is the part agents wish more people knew. Every Medigap carrier writes its own underwriting rules. A denial from one company is not a denial from all of them. The exact same health history that gets you turned down by Carrier A can get you approved at standard rates by Carrier B.

Carriers may evaluate diagnoses, recent treatments, upcoming procedures, hospitalizations, and prescription histories differently. A condition that produces a denial with one company may be acceptable to another.

I applied for a Medigap plan and got denied because of my health history-how is that even legal when I've paid into Medicare for years?

A Medicare Supplement, or Medigap, is a supplement to Original Medicare offered by private insurance companies. Your Medicare (Red, White & Blue card) is what you paid into. MedSupps are underwritten, very similar to life insurance. Being denied by one carrier does not mean that another company will not accept you. Each company has their own underwriting criteria.An independent agent who works with 8 or 10 carriers can look at your medications and conditions and tell you which company is most likely to say yes. This is a big part of what a good Medicare supplement underwriting review actually looks like.

When Medicare Advantage may be the remaining alternative

If no Medigap carrier approves you and you do not have a Guaranteed Issue right, Medicare Advantage may provide another path during a valid enrollment period. Eligibility is not based on Medigap-style health underwriting, but you must have Part A and Part B, live in the plan’s service area, and enroll during a valid enrollment period.

The Annual Enrollment Period runs October 15 through December 7 each year. Many plans offer a $0 additional plan premium, though beneficiaries generally continue paying their Part B premium. Advantage plans work differently from Medigap: you pay copays as you use services, they come with networks, prior authorizations, and yearly out-of-pocket maximums that cap your risk. Whether that trade is better or worse than Medigap depends on your health, your doctors, and your appetite for administrative friction, which is exactly what our real cost comparison of Medicare Advantage vs Medigap works through.

Are Medicare Advantage plans guaranteed issue?

Yes — Medicare Advantage plans are generally guaranteed issue as long as you are enrolled in Medicare Part A and Part B and live in the plan’s service area. Unlike Medigap plans, Medicare Advantage plans typically do not use medical underwriting, so you cannot be denied because of health conditions.However, you must enroll during a valid enrollment period, such as your Initial Enrollment Period, Annual Election Period, or a qualifying Special Enrollment Period.

The main exception is for people with End-Stage Renal Disease (ESRD), though most ESRD restrictions have been removed in recent years.

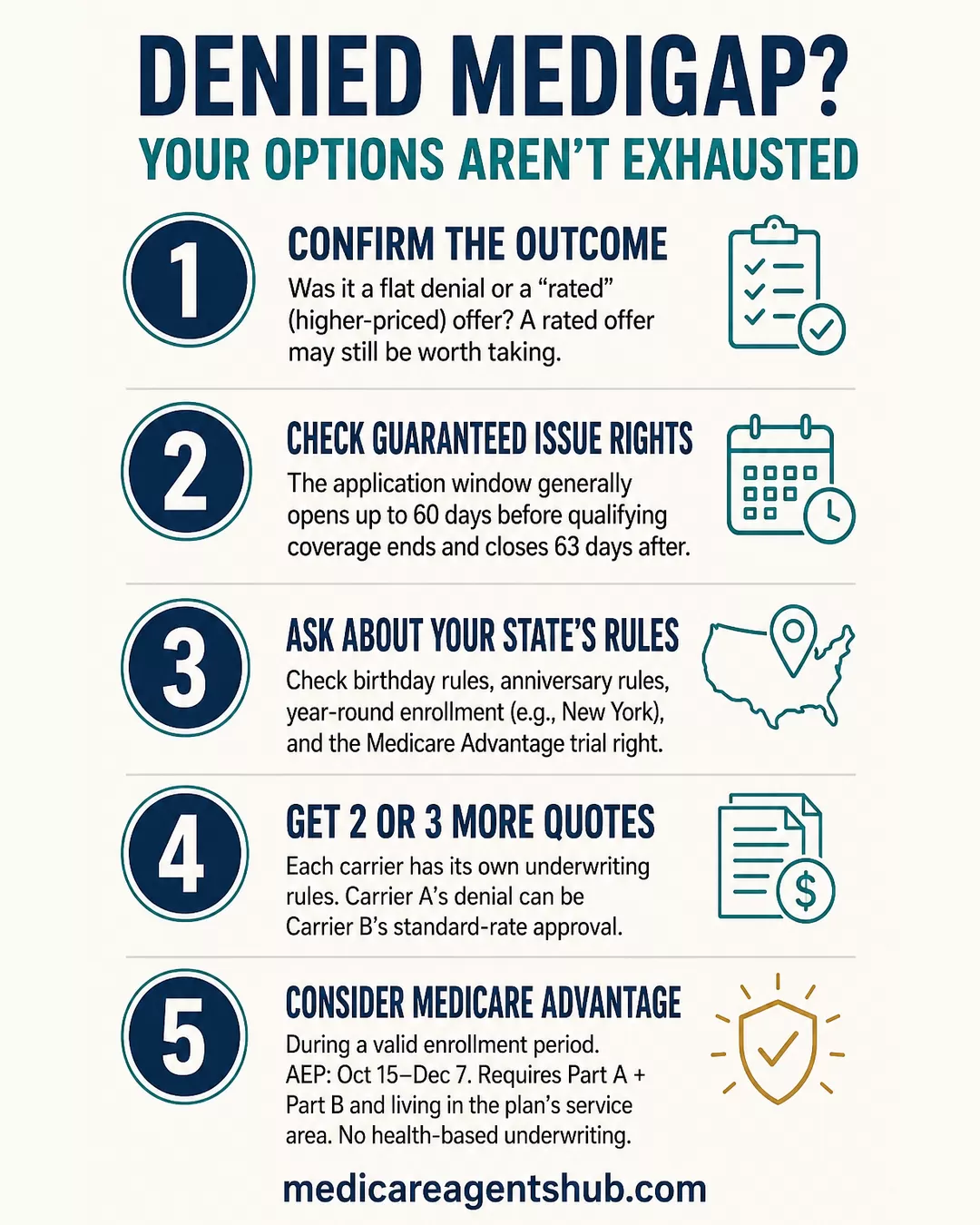

What to do right now if you’ve been denied

Take a breath, then work the checklist:

- Confirm you were actually denied and not just charged more. Some carriers offer coverage at a rated premium instead of a flat no. That may or may not be worth taking.

- Check whether you qualify for Guaranteed Issue. Certain qualifying coverage losses or plan changes within the applicable application window may create a Guaranteed Issue right.

- Ask about your state’s rules. Birthday, anniversary, year-round, and trial-right rules vary by state and are often missed.

- Get quoted by 2 or 3 other Medigap carriers. Different underwriting rules mean different outcomes.

- Look at Medicare Advantage during a valid enrollment period. You must have Part A and Part B and live in the plan’s service area, but health-based denials do not apply.

None of this makes the initial denial feel less unfair. But a Medigap denial usually still leaves options, and the fastest way to find yours is through a licensed independent agent who can pull quotes across multiple carriers, check your state’s exceptions, and price the Medicare Advantage alternative next to it.

Reviewed for accuracy against current Medicare.gov, CMS, and state insurance-department guidance. State Medigap rules can change; verify current rights with your state insurance department or SHIP.

Frequently asked questions

Can Medigap deny me because I have cancer or diabetes?

Outside of your protected enrollment periods, yes. Active cancer treatment and diabetes with certain complications are among the conditions commonly flagged during underwriting, but every carrier draws different lines and applies its own guidelines. A denial from one does not mean all will deny you.

Can I appeal a Medigap application denial?

Medigap denials based on medical underwriting generally cannot be appealed through Medicare. However, if you believe you were wrongly denied during a period when you had Guaranteed Issue rights or your Medigap Open Enrollment Period, you can file a complaint with your state insurance department.

Can another Medigap company approve me after a denial?

Yes. Each carrier sets its own underwriting criteria. The same health profile that results in a denial with one company can produce a standard-rate approval from another. An independent agent who represents multiple carriers can help identify which ones are most likely to accept you.

Can I join Medicare Advantage after being denied Medigap?

You can enroll in a Medicare Advantage plan during a valid enrollment period (such as the Annual Enrollment Period, October 15 through December 7) without health-based underwriting. You must have Part A and Part B and live in the plan’s service area.

Which states let you switch Medigap plans without underwriting?

A growing number of states offer additional enrollment windows beyond the federal minimum. These include birthday rules, anniversary rules, and in some cases year-round access. Check our state-by-state Medigap rules guide or contact your state insurance department for current details.

Start with our Medicare agent directory to connect with someone in your state who knows which carriers are most flexible with your specific health history.