Understanding Medicare Supplement Medical Underwriting: A Story of Making Informed Choices

Meet Diane: A Journey Through Medicare Decisions

Diane Chen turned 65 in April 2026, marking a significant milestone that came with important healthcare decisions. After working as an administrative assistant for 40 years, she was finally retiring and needed to navigate Medicare for the first time. Like many approaching this transition, Diane felt overwhelmed by the choices ahead. She had heard about Medicare Supplement insurance, also called Medigap, which could help cover the out-of-pocket costs that Original Medicare doesn't pay, like deductibles, coinsurance, and copayments.

What Diane didn't yet understand was the critical importance of timing and something called medical underwriting. Her story illustrates the journey many Medicare beneficiaries face when seeking supplemental coverage, and the lessons she learned could help others make more informed decisions about their healthcare future.

What Is Medical Underwriting for Medicare Supplement?

Medical underwriting is a risk assessment process that Medicare Supplement insurance companies use to evaluate applicants' health information and determine eligibility for coverage.

During this process, insurers review various health factors including age, chronic health conditions, medical history, prescription medications, tobacco use, weight or BMI, and family health history. The insurance company uses this information to decide whether to offer coverage and at what premium rate. In some cases, they may charge higher monthly premiums for pre-existing conditions, implement a pre-existing condition waiting period of up to six months, or even deny the application altogether.

Medical underwriting serves to prevent people from waiting until they have severe health conditions before purchasing a policy, which helps insurers manage costs and keep premiums stable for all policyholders. The underwriting process varies by insurer and may involve a health questionnaire, questions about hospital stays and upcoming procedures, or sometimes medical checkups and laboratory testing. Certain medications can also raise red flags during underwriting, so it pays to understand what insurers look for before you apply.

The Golden Window: Medigap Open Enrollment Period

Diane's insurance agent explained the most important concept she needed to understand: the Medigap Open Enrollment Period. This one-time, six-month window begins the first day of the month when you are both 65 years old and enrolled in Medicare Part B.

During Diane's open enrollment period from April 1 to September 30, 2026, insurance companies must accept her application regardless of any pre-existing health conditions she may have. They cannot use medical underwriting to deny coverage, charge higher premiums based on health status, or impose waiting periods for pre-existing conditions. This protection is a federal right that ensures the best opportunity to secure comprehensive Medigap coverage at preferred rates.

Diane learned that if she delayed enrolling in Part B due to employer coverage, her Medigap open enrollment wouldn't begin until Part B coverage started, not at age 65. The agent emphasized this crucial point: the Medigap Open Enrollment Period does not repeat annually like other Medicare enrollment periods. It's truly a one-time opportunity. Missing this window could mean facing medical underwriting, higher costs, or even denial of coverage later. This is one reason why some agents argue that choosing a Medicare Advantage plan at 65 can become a costly trap down the road.

Can you change Medicare Supplement plans at any time?

The answer is you can apply to change Medicare Supplement plans at any time. However, you have to keep in mind when you do this that the new Medicare Supplement company you are applying to outside of your open enrollment or special election periods will have the ability to ask you a number of medical questions. We'll call this medical underwriting, and they can deny you or change the price based upon your preexisting conditions or your current health situations.

That's not the same as Medicare Advantage plans, which have an open enrollment period every year. But that's the price of changing a Medicare Supplement plan. Good news is, if you're in great health, you can change Medicare Supplement plans at any time.

I hope that answers your question.

Health Conditions That May Affect Underwriting

When Diane's neighbor tried to enroll in a Medigap plan two years after his Medicare eligibility began, he faced medical underwriting and was denied coverage. Diane learned that certain health conditions commonly result in application denials when applying outside protected enrollment periods.

While every insurance company has different underwriting guidelines, some conditions consistently raise concerns:

- AIDS

- Alzheimer's disease

- Atrial fibrillation

- Any history of cancer

- Cirrhosis

- COPD

- Congestive heart failure

- Diabetes not controlled with medications

- End-stage renal disease

- Heart attack

- Kidney failure

- Multiple sclerosis

- Parkinson's disease

- Organ transplant

- Stroke

Other conditions may not result in outright denial but could lead to higher premiums, such as high cholesterol or high blood pressure when there aren't further health complications.

Diane realized how fortunate she was to learn about the open enrollment period before it was too late. Her neighbor's experience taught her that one company's denial doesn't mean all hope is lost. Different companies have different underwriting standards, and what one insurer declines, another might accept at a higher premium. When comparing carriers, it helps to understand what brokers actually recommend and why.

Guaranteed Issue Rights: Special Protection Periods

Diane's friend Robert had a different experience. He had been enrolled in his employer's retiree health plan that supplemented Medicare, but the company announced they were terminating the plan. Robert worried he had missed his chance for Medigap coverage since his open enrollment period had passed years ago.

However, he qualified for what's called guaranteed issue rights, special circumstances that allow enrollment in a Medigap policy outside the open enrollment period without medical underwriting.

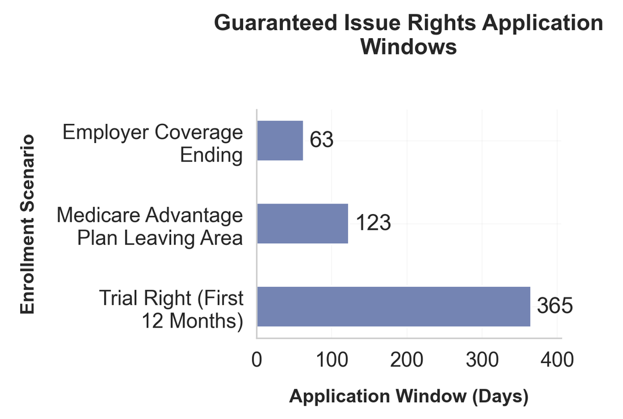

Under federal law, guaranteed issue rights apply in specific situations:

- When employer or union coverage that supplements Medicare ends

- When a Medicare Advantage plan stops operating in your area or you move out of the service area

- When returning to Original Medicare from Medicare Advantage within the first 12 months (trial right)

- When a Medigap insurer goes bankrupt

In these situations, insurance companies must sell you a Medigap policy at the best available rate regardless of health status and cannot deny coverage.

Application Window Timeframes

Timing is critical when using guaranteed issue rights. Each qualifying situation has a specific application window during which beneficiaries must act to secure coverage without medical underwriting. Robert had to apply within 63 days of losing his employer coverage.

The available plans under guaranteed issue rights typically include Plans A, B, C, D, F, G, K, or L, though some plans may have restrictions. Robert's story demonstrated that even if you miss the initial open enrollment period, life circumstances can create new opportunities for guaranteed Medigap access. For a deeper look at this process, see our guide on switching from Medicare Advantage back to Original Medicare.

The Pre-Existing Condition Waiting Period

Diane's sister Susan had a more complicated situation. She had missed her Medigap open enrollment period and didn't qualify for guaranteed issue rights, but she was able to get approved for a Medigap plan after going through medical underwriting. However, because she had been treated for diabetes within the past six months, the insurance company imposed a pre-existing condition waiting period.

This meant that for the first six months after her Medigap policy began, the plan could choose not to cover its portion of payments for conditions that were treated or diagnosed within six months of the policy start date. During this waiting period, Susan had to pay out-of-pocket for standard Medicare costs like Medicare Part B's 20% coinsurance for diabetes-related care, though Original Medicare still covered its portion.

The good news was that Susan's Medigap plan continued to cover medical costs for any new ailments or injuries during the waiting period, and after six months, the plan covered all conditions including her diabetes.

Susan learned she could have avoided or shortened this waiting period if she had maintained prior creditable coverage. Her pre-existing condition waiting period would have been reduced by one month for each month she was enrolled in creditable health coverage before purchasing the Medigap policy. This experience reinforced for Diane the value of enrolling during the open enrollment period when such waiting periods can be avoided entirely.

As a senior, what should I know about the differences between Original Medicare and Medicare Advantage before I choose?

Making the Right Choice at the Right Time

Diane decided to apply for her Medigap plan in early April, right when her Medicare Part B coverage began and her six-month open enrollment period started. She submitted her application before her 65th birthday, allowing time for processing so her Medigap coverage could start the same month Medicare became effective.

Because she enrolled during her open enrollment period, Diane was able to:

- Choose from any Medigap policy available in her state

- Receive the best premium prices without health-based surcharges

- Face no waiting periods for pre-existing conditions, even though she had well-controlled high blood pressure

Her decision was informed by understanding that applying outside this window could have resulted in medical underwriting where insurers could deny coverage, charge significantly higher premiums based on her health history, or impose waiting periods. It's worth understanding the pros and cons of Medicare Supplement insurance before making this decision.

Diane also learned that some states offer additional protections beyond federal law. States like California and Oregon have birthday rules allowing annual plan changes, while Connecticut, New York, Maine, and Massachusetts offer continuous or annual open enrollment.

As Diane reflected on her journey, she realized the most valuable lesson was this: the best time to enroll in Medigap is during your open enrollment period when you have the most choices, the best prices, and the strongest protections. "I'm so grateful I learned about this before it was too late," Diane told her friends. "Timing really is everything when it comes to Medicare Supplement insurance."

About the Author: Ed MacConnell is a Medicare supplement broker with 30 years experience in Feasterville PA. Feel free to contact him at Total Benefit Solutions Inc. or through Medicare Agents Hub.