Medicare, Medications & Mistakes: Avoiding Costly Underwriting Surprises

When the Best Treatments Plans Lead to the Worst Insurance Problem

The overwhelming majority of doctors mean well. Their job is to treat symptoms and find the most effective medications for their patients. But here's a common problem for those on Medicare: a prescription that works well for a minor issue might also be a primary treatment for severe conditions. When insurers see it on your medication list, they may assume you have the more serious diagnosis, even if that's not the case.

Once that flag is raised, getting a better rate, or qualifying at all, for a new Medicare Supplement plan becomes a real challenge.

As brokers who see several hundreds of people every year for plan reviews, we run into this daily. We often hear, "Oh, I'm very healthy and don't have any medical issues, I only take a couple of prescriptions." Then when we look at their list of medications, a different story is being told - at least on paper.

Doctors don't think about this because, well, they're not insurance agents. Their job is to treat you with the best tools available, and that's exactly what you typically want. But what they don't see is how insurance underwriting works or know the long-term consequences of a simple prescription request. And they certainly don't have time to keep up with which meds raise red flags for insurance companies. That's where we come in.

Underwriting Is a Tool, Not a Conversation

Underwriting decisions are purely data-driven—there’s no room for personal context. Some prescriptions, even when used for mild conditions or short-term treatment, can make insurers assume the worst. The underwriter reviewing the case (or more often, the computer system automatically rejecting an application) doesn't know you as a person. They don't see that you're active and healthy, and only take that medication "as needed." They simply see a name on a list - and sometimes, that's all it takes for a decline. Their job follows strict guidelines, and sometimes, it takes just one medication to get a "Declined" status.

Far too often, we see people who have an inhaler for seasonal allergies - something commonly seen in our area of South Louisiana during sugarcane season when the air is full of smoke and ash. That inhaler is marketed heavily for COPD, making it an automatic red flag for insurance carriers. Just the occasional fill of that inhaler at your local pharmacy is enough to get you automatically declined for a lower rate on a Medicare Supplement plan.

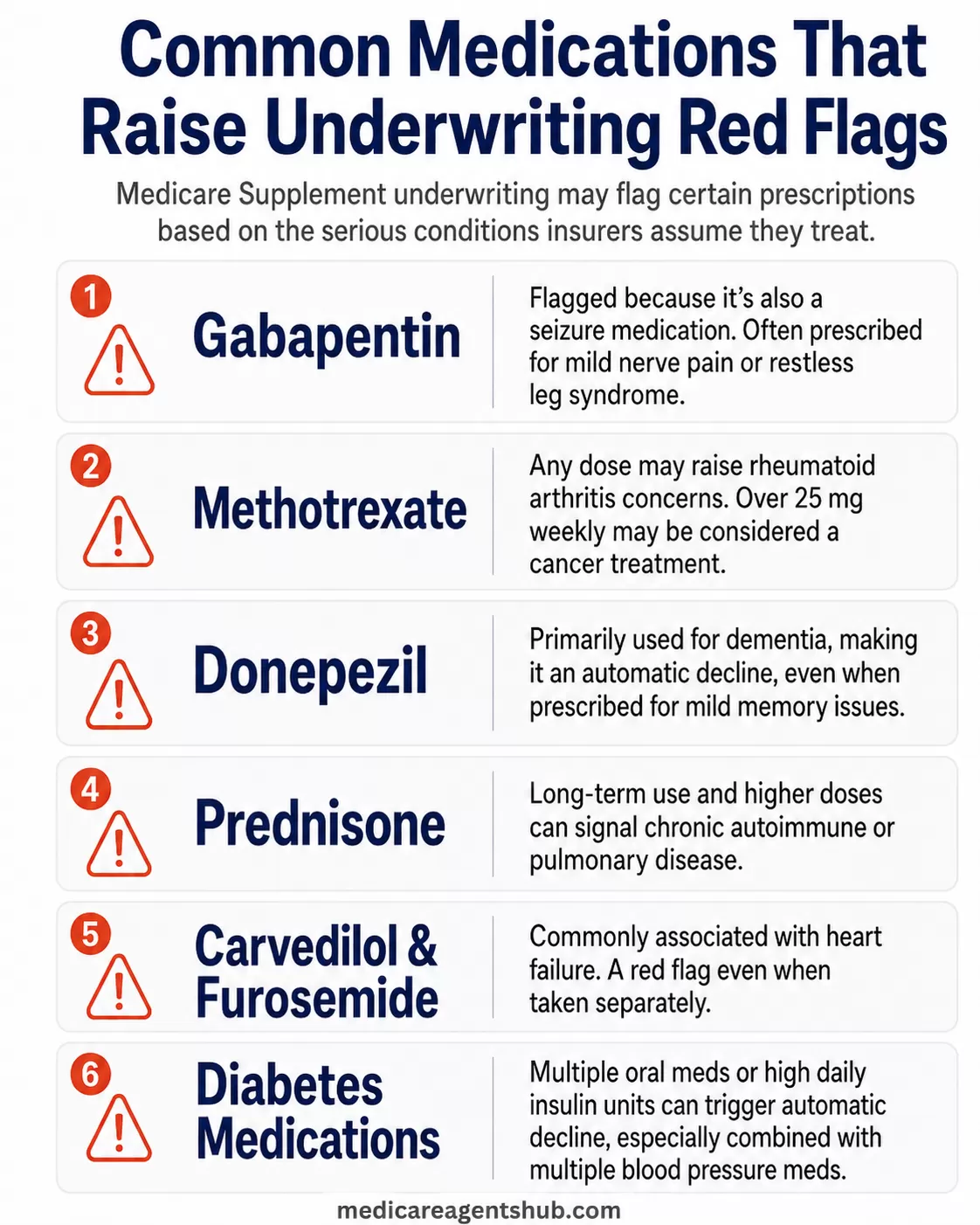

Common Medications That Raise Red Flags

Some of the most effective prescriptions can unintentionally lock you out of future savings. Here are a few examples:

- Gabapentin - Used for mild nerve pain or restless leg syndrome but flagged because it’s also a seizure medication.

- Methotrexate - If prescribed in any dose, it may be considered for rheumatoid arthritis raising concerns. Worse would be dosing over 25 mg weekly, which may be considered a cancer treatment.

- Donepezil - Sometimes prescribed for mild memory issues, but it is primarily used for dementia, making it an automatic decline.

- Prednisone - A common anti-inflammatory, but long-term use and higher doses over time can signal chronic autoimmune or pulmonary disease.

- Carvedilol & Furosemide - Often prescribed for high blood pressure and fluid retention but are commonly associated with heart failure, making them an underwriting red flag even when taken separately.

- Diabetes Medications - If someone takes multiple oral diabetes medications or over a certain number of units of insulin per day, they may be declined automatically. Also, when used in combination with multiple blood pressure medications, the rules may become even more strict.

There are many more common issues that we run into, and each individual case is different from those in the past and those yet to come. We take the approach to review every person as an individual and take time to educate them if they're interested to help get a better understanding of how their plans work.

The Disconnect Between Doctors and Medicare Costs

Doctors are focused on providing the best treatment, but they don’t keep track of Part D formularies. Just like a chef focuses on creating the best meal rather than checking grocery store coupons and discounts for the cheapest steaks nearing expiration. You want your medical team to perfect your care, not worrying about insurance rules that are constantly changing.

Unfortunately for those on Medicare, this can lead to unintended higher out-of-pocket costs when a drug moves to a higher tier on a Part D plan from year to year. It can also affect your ability to change plans any time of year by applying for a Medicare Supplement through underwriting which may lock you into a plan that has ever-increasing rates. If you're considering switching from Medicare Advantage back to Original Medicare, understanding how your medications could affect Medigap underwriting is essential.

I've been on a Part D plan for a while, and I'm wondering why my generic prescriptions suddenly cost more. Did something change?

If your same prescriptions from the same pharmacy on the same drug plan suddenly cost more this year, you’re not crazy. Part D plans reset every January, and even if you didn’t switch plans during Annual Enrollment Period (October 15 - December 7), your plan may have changed on you!The drug list, or formulary, may have shifted, bumping your med to a higher tier with a higher copay or dropping it from coverage altogether. They send those notices out in easy to overlook mailings and e-mail notifications that are generally ignored by many people who are happy with their coverage. That is, until those changes take effect.

And we can’t forget about the pharmacy game. If your go-to mom and pop shop isn’t considered a “preferred” pharmacy anymore, you’ll end up paying more just for sticking with what’s familiar. The big boys are playing hard ball and sometimes our local pharmacies end up paying the price or are forced to pass that on to you.

Bottom line: plans change, prices go up, and most people don’t find out until they’re standing at the pharmacy counter in January.

Don't wait to review these changes after you receive the shocking bill. Stay on top of changes or work with someone who will help review your options as part of your client relationship.

How to Protect Yourself

Ask your doctor about alternative medications if they are available and comparable. If you’re prescribed something new, feel free to ask if there’s another option that may prevent future insurance problems or a fallback plan if their first choice is unaffordable. Doctors appreciate informed patients. If a medication’s cost impacts your ability to take it as prescribed, discussing alternatives can lead to better options for both your health and future insurance choices. Take an extra minute to have this conversation on your next visit and you may be pleasantly surprised!

Review your plan options with an experienced Medicare advisor. Plan changes occur frequently when it comes to Medicare. Whether just an annual premium rate adjustment on a Medicare Supplement, a tier increase on a prescription that was covered on a drug plan, or a complete termination of a Medicare Advantage plan in an area, changes happen. Speaking with someone who regularly deals with these issues can help prevent future problems with your Medicare insurance options.

What is the biggest mistake seniors make when enrolling in Medicare?

The biggest mistake I see seniors make when enrolling in Medicare? Pretty simple. They listen to commercials with retired athletes or actors instead of getting real advice from someone they actually trust.They pick a plan because it says “$0 premium” or “extra benefits,” but don’t realize what they’re giving up until it’s too late like higher out-of-pocket costs, network restrictions, or a drug plan that doesn’t even cover their meds.

Medicare isn’t hard when you’ve got someone who sees you as a person, not a policy number or commission check. It feels like a pain because it’s designed that way so you’ll make a fast decision and never look back.

The key? Honest, no-pressure guidance from someone who knows the system and gives a damn. Not the people on TV reading a script about a “great” Medicare plan he probably doesn’t even use because, let’s be real, they’re either not on Medicare or have a low-cost group plan.

Start with a conversation, not a commercial.

Talk to an Expert Before Small Choices Become Big Problems

Medicare is tricky, and the choices made today - especially regarding prescriptions - can affect your coverage and costs for years to come. If you’re ever unsure, take the time to talk to a knowledgeable advisor. Finding the right professional to guide you through Medicare decisions can help you avoid costly mistakes and ensure you’re always in the best possible position - both medically and financially.

About the Author: Corey Romero is a Medicare Broker Licensed in LA and TX with 6+ years of experience. He is the founder of Acadiana Senior Advisors in Lafayette, LA.