Scheduled Surgery and Buying Medigap: What Actually Happens and the Underwriting Lie That Can Cost You the Policy

-

June 18, 2026

You have a knee replacement on the calendar for next month. You also just enrolled in a Medicare Supplement Plan G. Will the plan actually pay for the surgery, or did you just sign up for a policy that won't cover the one thing you need it for?

The answer depends almost entirely on when you enrolled and how you got the policy. Agents who deal with this scenario regularly say it's one of the most misunderstood areas of Medicare, and the consequences of getting it wrong range from a delayed claim to a rescinded policy and an uninsurable senior.

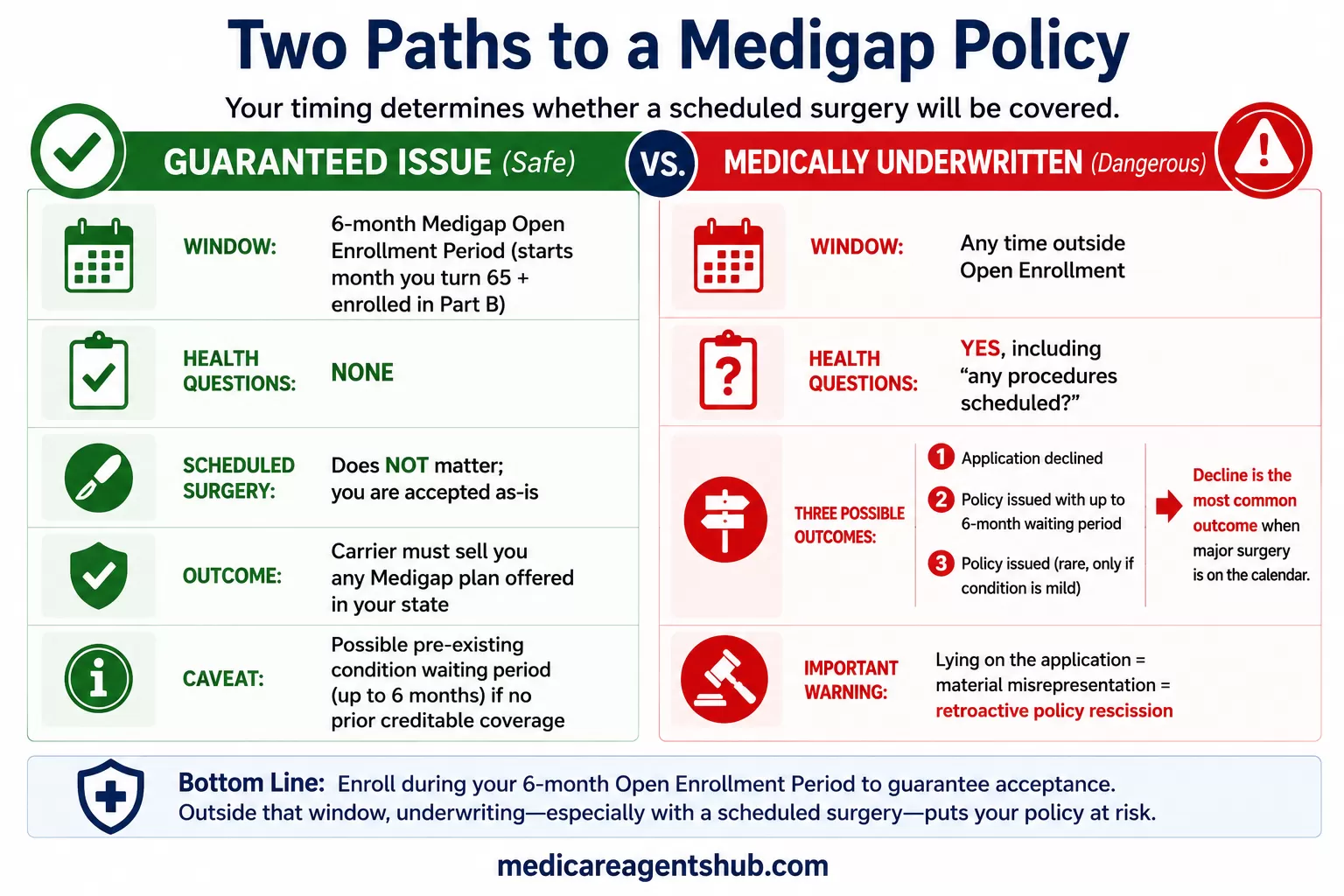

The Two Paths to a Medigap Policy (and Why Only One Protects You)

Every Medigap enrollment falls into one of two buckets: guaranteed issue or medically underwritten. The distinction is everything when there's a surgery on the books.

Guaranteed Issue: The Safe Window

During your Medigap Open Enrollment Period (the six months starting the month you turn 65 and are enrolled in Part B), insurance companies must sell you any Medigap plan they offer in your state. They cannot deny you or charge you more based on your health. A scheduled knee replacement, a cancer diagnosis, a history of heart disease: none of it matters. You are accepted as-is.

This is federal law. It applies in every state. If you buy Plan G during your Medigap Open Enrollment Period with a surgery already scheduled, the company cannot deny you or charge you more because of that health condition. The plan should pay its share for Medicare-covered care after the policy effective date, but there is one important caveat: if you did not have enough prior creditable coverage, the insurer may be able to apply a temporary pre-existing-condition waiting period for that condition.

I was already scheduled for total knee replacement when I took out my policy, will my supplemental plan G still pay?

Whether your Medicare Supplement Plan G will pay for a scheduled knee replacement depends primarily on when you enrolled and your prior insurance history. Under most circumstances, if the surgery takes place after your policy's effective date, it will be covered.Here is how the timing and rules work:

1. The "Open Enrollment" Rule If you bought your Plan G during your Medigap Open Enrollment Period (the 6-month window starting the month you turn 65 and enroll in Part B), the insurance company cannot deny you coverage or refuse to pay for a pre-existing condition, even if a surgery was already on the books. Verdict: Your surgery should be covered if you enrolled during this one-time window.

2. The "Creditable Coverage" Factor Even if you are in your Open Enrollment period, an insurer could technically impose a pre-existing condition waiting period of up to 6 months if you did not have "creditable coverage" leading up to your new policy. If you had insurance: If you had at least 6 months of continuous health coverage (like an employer plan or a different Medigap policy) with no gap longer than 63 days, the waiting period is usually waived. If you had no insurance: You might have to wait up to 6 months before the supplemental plan pays its portion for that specific condition.

3. Original Medicare Still Pays It is important to remember that Original Medicare (Parts A and B) has no waiting periods for pre-existing conditions. Even if your Plan G has a waiting period, Medicare will still pay its 80% of the approved costs. The Plan G would only be "missing" for its portion (the 20% coinsurance and the Part A hospital deductible) during that waiting period.

Medically Underwritten: Where It Gets Dangerous

Outside your Open Enrollment Period, Medigap carriers can (and do) ask health questions before issuing a policy. These applications typically include questions about current medications, recent hospitalizations, and critically, whether you have any procedures scheduled that have not yet been performed.

If you answer those questions honestly and disclose the upcoming surgery, one of three things happens: the carrier declines your application outright, the carrier issues the policy with a pre-existing condition waiting period of up to six months (meaning the surgery won't be covered until the waiting period expires), or, in rare cases, the carrier issues the policy anyway because the condition is mild enough to pass their underwriting guidelines.

The first outcome is the most common when there's a major procedure on the calendar.

Can I be denied for a Medicare Supplement plan?

Yes, you can absolutely be denied a Medicare Supplement (Medigap) plan, but it depends entirely on when you apply.Unlike standard health insurance or Medicare Advantage, Medigap plans are not protected by the Affordable Care Act’s pre-existing condition rules. Private insurance companies can look at your medical history and deny you coverage unless you qualify for a legally protected window.

The Underwriting Lie: Material Misrepresentation and Policy Rescission

This is where the real danger lives. Some seniors, whether on their own or coached by an agent, answer "no" to the question about scheduled procedures on a Medigap application when the truth is yes. The surgery happens, the claim is filed, and the carrier investigates.

Carriers have access to your medical records. They can request them during the policy's contestability period, often two years depending on the policy and state. If they find evidence that a surgery was scheduled before you applied, and you failed to disclose it, they can rescind the policy retroactively. That means the policy is treated as though it never existed. You lose coverage, you may be required to repay claims the carrier already paid, and you are now an uninsured senior with a pre-existing condition trying to find new coverage outside of any protected enrollment window.

The legal term for this is material misrepresentation. It's not a gray area. Carriers don't have to prove you intended to commit fraud; they only need to show that the information you provided was materially false and that it would have changed their underwriting decision.

I was already scheduled for total knee replacement when I took out my policy, will my supplemental plan G still pay?

That all depends on your situation. If you were new to Medicare, meaning you got part B for the 1st time then yes pre-existing conditions won't matter. If you were underwritten and had to answer health questions and knowingly answered NO to the questions about knee or joint replacement, then yes, the insurance company could deny the claim because of misrepresentation and can even resend your policy. If an agent told you to do this the agent could lose his/her license. So, I always tell my clients you need to just be honest and answer the questions truthfully and if an agent is telling you not to be truthful you need to run away from them fast.Likely the insurance company will probably know about your knee replacement anyway if you have seen a doctor about it when you apply if you are not in open enrollment or guarantee issue. I had a client tell me once that the underwriter knew more about her health conditions than she did.

For agents who help clients through underwritten applications, this is a firm line. An agent who encourages a client to omit a scheduled surgery faces disciplinary action from their state's department of insurance, potential loss of licensure, and liability for the client's resulting losses. Reputable agents will always tell you to answer the application honestly, even when the honest answer means you won't be approved.

The Pre-Existing Condition Waiting Period (It's Not a Denial)

Some carriers will still issue a Medigap policy to someone with health issues but impose a pre-existing condition waiting period of up to six months. During this period, the plan will not pay for treatment related to conditions you had before enrolling. After the waiting period ends, the condition is covered going forward like anything else.

There's an important nuance here: if you had creditable coverage (employer insurance, COBRA, another Medigap plan, or Medicare Advantage) for at least six months before your Medigap effective date without a gap longer than 63 days, the carrier must credit that time toward the waiting period. Six months of prior coverage means no waiting period at all.

This rule catches many people off guard. A senior coming off an employer plan who enrolls in Medigap within 63 days of losing that coverage can often bypass the waiting period entirely, even outside of the standard Open Enrollment window.

Guaranteed Issue Back Doors: Getting Medigap Without Underwriting Outside OEP

The six-month Open Enrollment window at 65 is the most well-known path to guaranteed issue, but it's not the only one. Federal law creates several other situations where carriers must accept you regardless of health:

- Medicare Advantage Trial Right: If you joined a Medicare Advantage plan or PACE when you were first eligible for Medicare Part A at 65, and you decide within the first year that you want to switch back to Original Medicare, you generally have a trial right to buy any Medigap policy sold by an insurance company in your state. Other guaranteed-issue situations may limit you to certain Medigap plan letters, so confirm the specific right that applies before choosing a plan.

- Involuntary Loss of Coverage: If your MA plan leaves your area, your Medigap carrier goes bankrupt, or your employer group coverage ends, you get guaranteed issue rights to switch back to a Medigap plan without underwriting.

- Medicare SELECT Plan Loss: If you have a Medigap SELECT plan and move out of its service area, guaranteed issue kicks in.

- State-Specific Rules: Several states go beyond federal minimums. New York and Connecticut require continuous open enrollment for Medigap, meaning you can enroll at any time of year without underwriting regardless of health. Other states offer birthday rule protections that allow annual plan switches without medical questions. Rules, windows, and eligible plan changes vary by state, so confirm with your State Health Insurance Assistance Program (SHIP) or your state insurance department before relying on a state-level protection.

What is Guaranteed Issue for Medicare Supplement plans, and when does it apply?

Guaranteed Issue (GI) rights for Medicare Supplement (Medigap) plans are special situations where an insurance company must sell you a Medigap policy, cannot deny you because of health problems, cannot charge you more because of your health, and cannot impose waiting periods for pre-existing conditions (if you had prior creditable coverage).The Most Important Guaranteed Issue Situations

1. You Lose Medicare Advantage Coverage Through No Fault of Your Own

2. Medicare Advantage Trial Right

3. Your Medigap Company Goes Bankrupt or Coverage Ends

4. You Were Misled by an Insurance Company

Timing Strategy: How Agents Advise Clients with Upcoming Procedures

When a client comes to an agent with both a surgery on the calendar and a need for Medigap coverage, the conversation almost always starts with timing.

If the client is still in their Open Enrollment Period, the advice is straightforward: enroll now, because the surgery is irrelevant to guaranteed issue enrollment. The plan will cover its share as long as the procedure date falls after the policy effective date.

If the client is outside OEP and would need to go through underwriting, agents generally recommend one of several approaches:

- Check for guaranteed issue rights first. Did they recently leave an employer plan? Are they within a trial right window? Is their state one of the continuous-enrollment states? Any of these can bypass underwriting entirely.

- Consider the birthday rule. In states that have one, the annual birthday window lets you switch Medigap plans (same letter or lower) without health questions. This doesn't help if you don't already have a Medigap policy, but for existing policyholders looking to switch carriers for a better rate before a procedure, it's a valuable option.

- Delay elective surgery until after enrollment. For truly elective procedures where timing is flexible, some agents advise clients to get the Medigap policy in place first, wait for any applicable waiting period to pass, and then schedule the surgery. This only works when the procedure is genuinely elective and the client's health allows for the delay.

- Explore Medicare Advantage as a bridge. Unlike Medigap, Medicare Advantage plans are guaranteed issue during the Annual Enrollment Period. A senior who cannot pass Medigap underwriting can enroll in an MA plan to get coverage for the surgery, though the trade-offs (networks, prior authorization, out-of-pocket maximums) need to be weighed carefully.

What Plan G Actually Covers for Surgery (Once You're In)

Assuming you have an active Plan G policy with no waiting period exclusions, the coverage for surgery is comprehensive. Medicare Part A covers the hospital stay for inpatient procedures, and Plan G covers the Part A deductible and coinsurance. For outpatient procedures, Medicare Part B covers 80% of the approved amount after you meet the annual Part B deductible ($283 in 2026), and Plan G picks up the remaining 20%.

In practical terms, a senior with Plan G who has already met their Part B deductible pays $0 out of pocket for a Medicare-approved knee replacement, hip replacement, or other covered surgery. That's the reason Medigap is so attractive to people who know they have procedures ahead, and it's also why the underwriting rules exist to prevent people from buying coverage only when they know they'll need it.

I'm on Medigap Plan G, and I'm curious how my upcoming knee replacement surgery will be billed. Does the plan cover it all after my deductible?

The answer to that is yes. If you are getting this surgery done at a Medicare-approved facility and it is medically necessary, the only thing you have to pay for with a Medicare Plan G is a $283 deductible for this year. After that, you won't pay anything.

What to Do Right Now If You Have Surgery Scheduled and Need Medigap

If you're reading this with a procedure on the calendar and no Medigap policy in place, here's the practical sequence:

- Check your enrollment timeline. Are you within your six-month Medigap Open Enrollment Period? If yes, enroll immediately. Your health doesn't matter during this window.

- Check for guaranteed issue rights. Review whether you qualify through loss of coverage, a trial right, or state-specific protections.

- Talk to an independent agent. Not a carrier's 800 number. An independent agent who works with multiple carriers can tell you which companies have the most favorable underwriting for your situation. Some carriers are more lenient than others on specific conditions.

- Be honest on every application. No exceptions. The short-term gain of an approved policy is not worth the risk of rescission, and any agent who tells you otherwise is putting their license and your coverage at risk.

- Understand your coverage start date. Even with guaranteed issue, your policy needs to be effective before the surgery date for the plan to pay its share. If timing is tight, confirm the effective date with your carrier before scheduling the procedure.

The gap between "I have Medicare" and "I have Medicare plus a supplement that actually covers my surgery" is smaller than most people think if you act at the right time. It becomes a wall if you wait too long or try to game the system. The agents on Medicare Agents Hub can walk you through your specific situation and help you find the path that works without putting your coverage at risk.