Medigap Birthday, Anniversary and Guaranteed-Issue Rules by State in 2026

-

July 12, 2026

Most Medicare content treats Medigap underwriting as a locked door once your six-month Open Enrollment Period ends. If you develop a health condition, the story goes, you are stuck on whatever plan (and whatever premium) you signed up for at 65. That is mostly true if you live in most states. It is not true if you live in one of the states that have built birthday rules, anniversary rules, or year-round guaranteed issue windows into their insurance codes.

These state-level protections rarely show up on medicare.gov's national pages, and they represent some of the most valuable geographic knowledge in the Medicare Supplement world. Below is what agents in those states actually tell their clients.

Why This Only Matters After Your Open Enrollment Period

During the six months that start the first month you are both 65 or older and enrolled in Medicare Part B, you can buy any Medicare Supplement plan from any carrier with no health questions. That is federal law, and everyone gets it. (Rights for beneficiaries who qualify for Medicare under 65 vary by state.)

What changes after that six-month window is that carriers can put you through medical underwriting, and they may decline applicants over conditions as ordinary as a controlled A1C or a procedure scheduled for next spring. Premiums can also increase over time, and the plan you selected at 65 may gradually become more expensive relative to newer blocks of business as healthier enrollees enter the market at lower rates.

The state rules below provide a way out. They give you a repeatable, once-a-year (or all-year) opportunity to shop the market and switch carriers without answering a single health question.

Can I change my Supplemental/Medigap plan at any time?

Yes, you can change your Medigap plan anytime, but depending on your state, you might have to go through medical underwriting.California has a birthday rule, which gives you 60 days after your birthday each year to switch to a plan with equal or lesser benefits—no health questions asked.

New York lets you switch anytime with no underwriting, so you’re always guaranteed coverage.

If you’re in another state, you might need to go through underwriting unless you qualify for a special exception. Always good to check before making a switch!

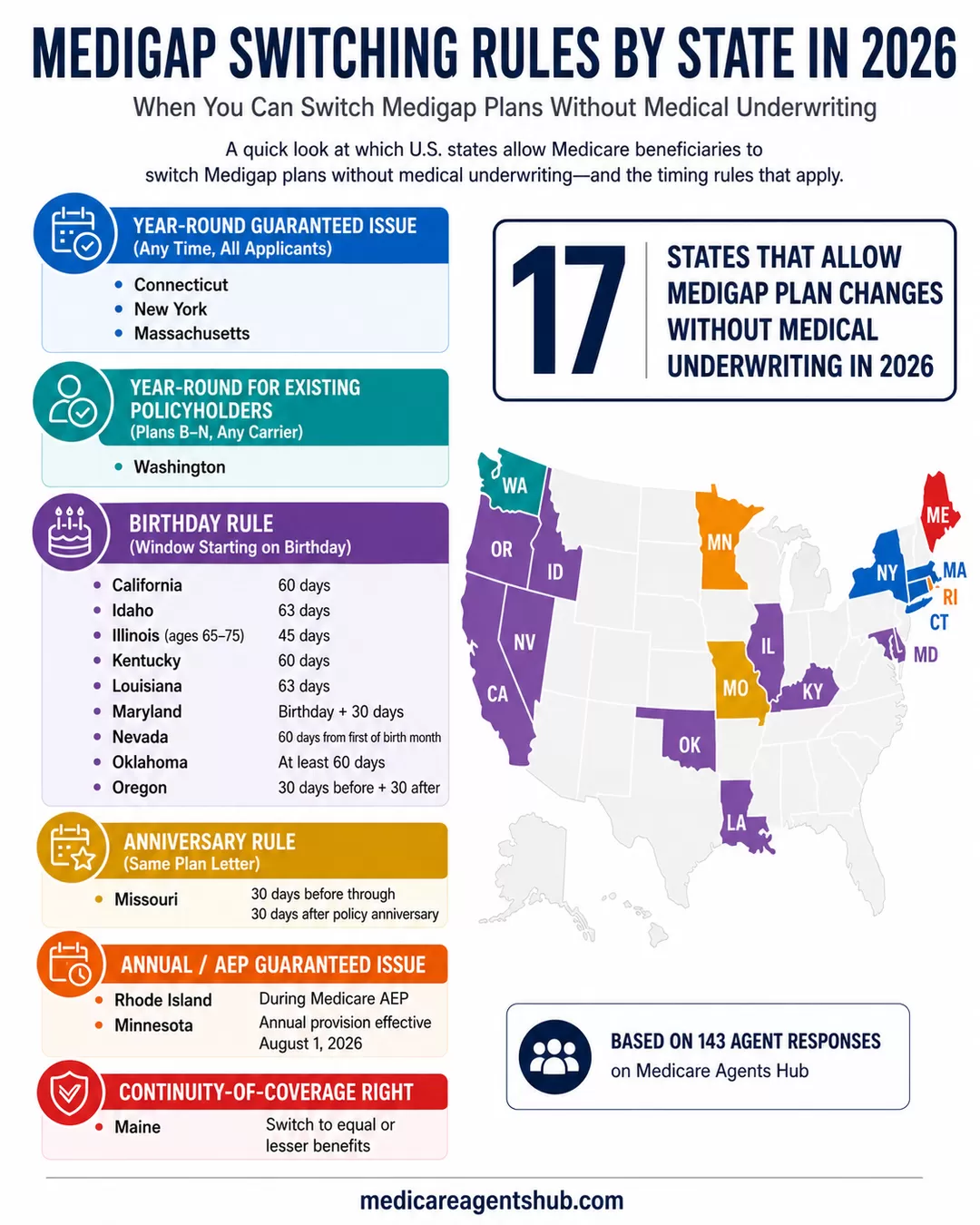

State Medigap Switching Rules at a Glance

The table below covers every state rule we have verified. Details, including window lengths and carrier restrictions, follow in the sections below.

| State | Rule Type | Enrollment Window | Who Qualifies | Carrier Restriction |

|---|---|---|---|---|

| California | Birthday | 60 days starting on birthday | All Medigap policyholders | Any carrier (equal or lesser benefits) |

| Connecticut | Year-round GI | Any time | All Medigap applicants | Any carrier |

| Idaho | Birthday | 63 days starting on birthday | All Medigap policyholders | Any carrier (equal or lesser benefits) |

| Illinois | Birthday | 45 days starting on birthday | Ages 65 to 75 | Same or affiliated issuer; equal or lesser benefits |

| Kentucky | Birthday | 60 days starting on birthday | All Medigap policyholders | Same plan letter, different carrier |

| Louisiana | Birthday | 63 days starting on birthday | All Medigap policyholders | Same or affiliated issuer; equal or lesser benefits |

| Maine | Continuity of coverage | Based on continuity-of-coverage right | Existing Medigap policyholders | Same or another insurer; equal or lesser benefits |

| Maryland | Birthday | Birthday plus the following 30 days | All Medigap policyholders | Any carrier (equal or lesser benefits) |

| Minnesota | Annual open enrollment | Annual provision effective August 1, 2026 | Existing Medigap policyholders | See state guidance when effective |

| Missouri | Anniversary | 30 days before through 30 days after policy anniversary | Existing Medigap policyholders | Same plan letter, any carrier |

| Nevada | Birthday | 60 days starting first day of birth month | All Medigap policyholders | Any carrier (equal or lesser benefits) |

| New York | Year-round GI | Any time | All Medigap applicants | Any carrier |

| Oklahoma | Birthday | At least 60 days starting on birthday | All Medigap policyholders | Same plan letter, different carrier |

| Oregon | Birthday | 30 days before through 30 days after birthday | All Medigap policyholders | Designated plans with equal or lesser benefits |

| Rhode Island | Annual GI (during AEP) | During Medicare's Annual Enrollment Period | Continuously covered Medigap policyholders | See state guidance |

| Washington | Year-round right to change (existing policyholders) | Any time | Existing Medigap policyholders (Plans B through N) | Any plan B through N, any carrier |

| Massachusetts | Year-round GI | Any time | All Medigap applicants | Any carrier (non-standardized plan structure) |

Maryland also enacted a law effective July 1, 2026 that created additional Medigap enrollment protections for certain individuals losing Medicaid coverage and certain pre-2020 Medicare beneficiaries who qualify for specified federal Special Enrollment Period protections. Contact the Maryland insurance department for details on whether you qualify.

Birthday Rule States: How They Work

Birthday rule states let you switch Medigap plans during a defined window tied to your birthday, every year, without underwriting. The window length, the carriers you can move to, and the plan letters you can move between vary by state. Here are the ones agents on the platform bring up most often:

- California gives you a 60-day window starting on your birthday. You can switch to any plan with equal or lesser benefits with any carrier.

- Oregon runs a window that begins 30 days before your birthday and ends 30 days after (roughly 61 days total). Eligible policyholders can move to designated plans with equal or lesser benefits without medical underwriting.

- Nevada uses a 60-day window that begins on the first day of your birth month.

- Idaho gives you a 63-day window that starts on your birthday.

- Illinois applies its birthday rule to beneficiaries aged 65 to 75 and gives a 45-day window. Two restrictions apply: the new policy must be from the same issuer or an affiliated issuer, and it must offer benefits equal to or less than the existing policy.

- Louisiana provides a 63-day window that begins on your birthday. The replacement policy must be offered by the same issuer or an affiliated issuer, and it must provide equal or lesser benefits.

- Maryland lets you switch during a window that includes your birthday and the following 30 days.

- Oklahoma gives you at least a 60-day window starting on your birthday and allows you to switch to the same plan letter with a different carrier.

- Kentucky runs a 60-day post-birthday window with same-letter switching.

Can I change my Supplemental/Medigap plan at any time?

Hi!Thanks for contacting me. Yes you may but you might have to go thru underwriting. Oklahoma has a Birthday Rule that was passed a couple of years ago. In short the rule states that you may change supplement carriers at the time of your birthday with guaranteed issue. This rule helps with lowering premiums.

If I can help with anything Medicare related, please be sure to reach out.

Dawn Young

HealthMarkets Insurance Agency

The common shape is: same plan letter or lesser benefits, with some states limiting you to the same or affiliated carrier, no health questions. That last part is the whole point. You are not upgrading your coverage; you are shopping the market for a better price on the coverage you already have. In practice that usually means moving from a legacy Plan F or Plan G that has had repeated rate increases to a newer Plan G with a fresh block of business at a lower monthly premium.

Can I change my Supplemental/Medigap plan at any time?

Yes, you can, but you would be subject to underwriting so if you have some health conditions then you might have a hard time finding another medicare supplement insurance company that is willing to insure you. If you do have chronic health conditions, then if you live in kentucky, we can invoke the kentucky birthday rule up to 60 days after your birthday and you'll have guaranteed issue into the exact same medicare supplement plan with another company, thus saving you premiumAnniversary Rule States: The Policy-Effective-Date Window

A small number of states use the anniversary of your Medigap policy's effective date instead of your birthday. If your Plan G went into force on May 1, your switching window opens on May 1, not on the date of your birthday.

- Missouri is the classic example. You get a 60-day window that straddles your policy's anniversary (30 days before through 30 days after). You can switch to the same plan letter with any carrier.

Can I change my Supplemental/Medigap plan at any time?

Yes, you can change your Medigap plan at any time, but you will be subject to underwriting and health questions. However, if you wait until the anniversary month of when your Medigap plan became effective, you may switch plans with no underwriting or health questions.The Missouri rule is especially useful for seniors who ended up with a bad initial-enrollment decision. If your policy anniversary is March, you do not have to wait until your November birthday to re-shop. You already have a March window built into your policy.

Year-Round Guaranteed-Issue States

A few states have effectively abolished Medigap underwriting for all applicants. If you live in one of these states, you can apply for a Medigap plan at any point in the year without health questions, whether you already hold a policy or not.

- New York and Connecticut require year-round guaranteed issue for any Medigap applicant. They are among the friendliest Medigap markets in the country, and the premiums reflect it (community-rated pricing, no age-based increases).

- Massachusetts also operates under community rating and offers year-round guaranteed issue, though the plan structures in Massachusetts are non-standardized and look different from the A-through-N letters used elsewhere. (Minnesota and Wisconsin also use non-standardized Medigap plans, but they have different enrollment rules.)

Existing-Policyholder Switching Rights

Some states offer broad switching protections that apply specifically to people who already own a Medigap policy, separate from the birthday or anniversary rules above.

- Washington allows any existing Medigap policyholder to switch to any other plan between letters B and N with no underwriting, at any time. Plan A holders can only switch to another Plan A. This right does not apply to new Medigap buyers coming from Original Medicare or Medicare Advantage; you have to already be in a Medigap plan to use it.

- Maine provides a broad continuity-of-coverage right that allows existing policyholders to move to a plan with the same or lesser benefits through the same or another insurer.

Can I change my Supplemental/Medigap plan at any time?

Yes, in Washington State, you can change your Medicare Supplemental (Medigap) plan at any time during the year, but there are specific rules depending on your current plan. Unlike most states, Washington has a unique "Right to Change" law that offers year-round guaranteed issue for existing Medigap policyholders, meaning you can switch plans without medical underwriting in certain cases. Here’s how it works:If you have Medigap Plan A: You can only switch to another Plan A offered by a different insurer without undergoing medical underwriting. You’re limited to staying within the same plan letter.

If you have Medigap Plans B through N: You can switch to any other plan between B and N (e.g., from Plan G to Plan N, or Plan B to Plan F) at any time, also without medical underwriting. This gives you more flexibility to adjust coverage or premiums.

Key Conditions: You must already be enrolled in a Medigap plan to use this rule. If you’re coming from Original Medicare alone or a Medicare Advantage plan, you can’t switch to a Medigap plan under this guaranteed issue provision—you’d need to apply normally, which might involve health questions outside your initial 6-month Medigap Open Enrollment Period or a Special Enrollment Period.

Practical Steps: To switch, contact the new insurance provider, apply for the desired plan, and, once approved, cancel your old plan. There’s no specific enrollment window like the Annual Enrollment Period (October 15–December 7) that applies to Medicare Advantage or Part D—Washington’s rule lets you do this anytime.

This flexibility is a big perk in Washington compared to most states, where switching outside specific periods often requires passing medical underwriting, risking denial or higher rates due to health conditions. Just make sure the new plan fits your needs—compare benefits and premiums carefully with your Medicare Insurance broker, as costs can vary by insurer even for the same lettered plan.

If you live in one of these states and you have not shopped your Medigap policy in the last few years, it is worth comparing rates. There is no penalty for looking, and no health question that can trip you up. The only reason most people do not do this is that they never learned they could.

Newly Enacted State Protections

Several states have recently passed or scheduled new Medigap protections that are worth tracking:

- Rhode Island enacted a 2026 law providing annual guaranteed-issue rights during Medicare's Annual Enrollment Period for individuals who have maintained continuous Medigap coverage.

- Minnesota has a delayed annual Medigap open-enrollment provision scheduled to take effect on August 1, 2026. Until that date, existing rules apply. Contact the Minnesota insurance department for details once the provision is in effect.

- Maryland added protections effective July 1, 2026 for certain individuals losing Medicaid coverage and certain pre-2020 Medicare beneficiaries qualifying for specified federal Special Enrollment Period protections.

These are recent changes. Agents and consumers should confirm current eligibility with the relevant state insurance department before applying.

The Rule Every Agent Repeats and Every Client Forgets

Here is the most common mistake that can undermine the state protections above: do not cancel your existing Medigap plan until the new carrier has issued the new policy in writing.

Even inside a guaranteed-issue window, the paperwork takes time. Applications get flagged, effective dates get pushed, signatures get missed. If you cancel your old policy the day you sign the application for the new one, you can end up with a gap in Medigap coverage. That gap can cost you thousands if you have a hospitalization during it. In many states, it can also jeopardize the guaranteed-issue right you were trying to use, because most of these rules require you to be actively enrolled in a Medigap plan at the time of the switch. (Some states, including Maine and Oklahoma, expressly permit a limited gap in coverage without forfeiting the right, but do not assume your state is one of them.)

Federal law also provides a 30-day free-look period for new Medigap policies. During that time you may be paying premiums on both the old and new policies while you decide whether to keep the replacement coverage. That overlap is normal and expected.

Can I change my Supplemental/Medigap plan at any time?

You can change from one Medicare Supplement (Medigap) Plan to another at any time, but you most likely will be subject to Medical Underwriting.Since Medicare Supplement (Medigap) plans are guaranteed renewal, as long as you pay your premiums, you can stay on the plan you have.

If you want to change, the carrier you want to change to can review your medical history to see if they want to accept you.

If you do make a change, DO NOT CANCEL your existing Medicare Supplement (Medigap) Plan until you have it in writing that you have been accepted into the new plan.

The right sequence is: apply for the new plan, get the written approval and the effective date, then submit the cancellation on the old plan timed to end the day the new one begins. Agents can coordinate the two dates for you. If you are shopping on your own, wait for the physical policy or an approval email before you touch the old carrier.

What Happens if the Carrier Cancels You (Spoiler: They Almost Never Can)

A common fear that keeps seniors from switching is the worry that a carrier will drop them for filing too many claims. Federal law makes that essentially impossible. Medigap plans are guaranteed renewable, which means the carrier has to keep your coverage in force as long as you pay the premium. Age does not matter. Health does not matter. Claims history does not matter.

Can my Medigap insurer terminate my policy?

In almost every situation, a Medigap insurer cannot cancel your policy as long as you keep paying your premiums and you didn’t commit fraud on your application. Federal law requires Medigap plans to be guaranteed renewable, which means the company has to keep your coverage in force.There are only a few situations where a Medigap company is allowed to end your policy:

• You stop paying your premiums.

If the payment goes past the grace period (usually about a month), they can cancel it.

• You gave false information when you applied.

If the insurer can prove you intentionally misrepresented something important on your application, they can terminate the policy.

• The insurance company goes bankrupt or stops selling Medigap plans altogether.

If they pull out of the Medigap market in your state, they can drop all policies—though you get special rights to switch to another plan without medical underwriting.

Outside of these situations, a Medigap insurer cannot drop you because of your age, your health, a new diagnosis, or because your medical care has gotten expensive.

Serving ALL of Texas, California & Florida

Contact us.

The narrow situations where a carrier can end a Medigap policy are limited to non-payment of premium, proven material misrepresentation on the application, and the carrier itself going insolvent or exiting your state's Medigap market. That last one is worth flagging: if your carrier pulls out of your state, you get federal guaranteed-issue rights to switch to another Medigap plan without underwriting, regardless of whether your state has a birthday rule. It is an extra safety net most beneficiaries never hear about until it happens to them.

How to Actually Use Your State's Rule

The mechanical process is the same across all of these state windows:

- Confirm your window. Call your state department of insurance or ask an independent agent to confirm the exact start date, length, and plan-letter limitations. State rules get amended more often than most people realize. Idaho, Illinois, Louisiana, Maryland, Rhode Island, and Minnesota have all had recent changes.

- Get quotes across the market. Independent brokers who represent multiple carriers can pull a rate sheet for every plan letter you are eligible to switch to. Agents who represent only one insurer may not be able to compare all Medigap carriers available in your state.

- Apply during the window, not before. The guaranteed-issue right exists inside the window. Applications submitted before the window opens may be subject to standard underwriting.

- Do not cancel the old policy until the new one is in force. This is the single most repeated piece of advice from every agent on the platform.

If you are worried about rate hikes on your current plan and you do not want to switch every year, this is also a decent time to review whether Medigap is still the right structure for your budget. Some seniors move to a lower plan letter within the same window rather than shopping for a new carrier.

The National Picture, in Plain English

If you live in a birthday-rule state, an anniversary-rule state, or one of the year-round guaranteed-issue states, you have a repeatable, no-underwriting exit ramp built into your state's law. Many seniors do not know it exists, do not use it, and stay on a legacy plan that may grow more expensive over time while other policyholders move to carriers with more competitive rates. If you live in a state without these protections, your best shot at a switch is still Open Enrollment when you first become eligible, or a Special Enrollment Period tied to a qualifying life event.

The single biggest thing to take away from all of this: check your state before you assume you are stuck. And if you weighed your options around underwriting and pre-existing conditions when you first enrolled and decided the current plan was the best you could do, redo that math the next time your birthday, anniversary, or open switching window comes around. The answer might be different now.

Frequently Asked Questions

What states have a Medigap birthday rule?

Birthday rules vary in structure, but the states with verified birthday-window protections include California, Oregon, Nevada, Idaho, Illinois, Louisiana, Maryland, Oklahoma, and Kentucky. Each state sets its own window length, plan-letter restrictions, and carrier limitations. Check the reference table above for specifics, and confirm current rules with your state insurance department.

Can I change Medigap plans without medical underwriting?

Yes, if your state has a birthday rule, anniversary rule, or year-round guaranteed-issue provision, and you apply during the correct window. Outside of these state windows, the main federal protection is the six-month Medigap Open Enrollment Period that begins when you are first eligible. After that window closes, carriers in most states can require medical underwriting.

Is the Medicare Annual Enrollment Period also a Medigap enrollment period?

No. The Medicare Annual Enrollment Period (October 15 through December 7) applies to Medicare Advantage and Part D prescription drug plans. It does not create a right to switch Medigap plans without underwriting. Medigap switching rights come from your state's rules or from qualifying federal protections, not from the AEP calendar. Rhode Island is a notable exception: its 2026 law ties annual Medigap guaranteed-issue rights to the AEP window for qualifying individuals.

Can I change from Plan G to Plan N during a birthday window?

In some states, yes. States like California, Oregon, and Idaho allow you to switch to a plan with equal or lesser benefits, which would include moving from Plan G to Plan N (since Plan N covers less). Other states, like Oklahoma and Kentucky, restrict you to the same plan letter with a different carrier. Check your state's specific rule in the table above. Plan N can sometimes be a smarter fit depending on how you use your coverage.

Should I cancel my old Medigap policy before the new one begins?

No. Wait until the new policy is approved and has a confirmed effective date before submitting a cancellation on the old one. You may briefly pay premiums on both policies during the federal 30-day free-look period, but that overlap is far safer than a gap in coverage that could leave you exposed to out-of-pocket costs or, in many states, jeopardize your guaranteed-issue right.