Plan G Isn't Always King: When Plan N, Plan K, or High-Deductible G Actually Beats It

-

Last Updated July 23, 2026

Plan G is the default recommendation for a reason, and Medicare Supplement agents will tell you exactly why. After the Part B deductible ($283 in 2026), it covers virtually everything Medicare approves. No copays. No coinsurance. No surprises. But "best coverage" and "best value" are not always the same thing. If you're healthy, live in a state that bans excess charges, or simply want to keep more money in your pocket each month, three alternatives deserve a hard look: Plan N, Plan K, and High-Deductible Plan G.

Here's how agents break it down when clients ask.

Plan N: The $20 Copay Trade-Off

Plan N is the closest thing to Plan G without paying full Plan G premiums. The coverage is nearly identical, with two differences that matter: a $20 copay for doctor visits, a $50 copay for ER visits (waived if you're admitted), and no coverage for Part B excess charges.

That last point scares people, and agents hear about it constantly. But the fear is often bigger than the reality. Excess charges only apply when a doctor does not accept Medicare assignment. A provider who doesn't accept assignment can bill up to 15% above the Medicare-approved amount, and you'd owe that difference. The thing is, the vast majority of providers accept assignment. And in some states, it's not even a question.

States That Ban Excess Charges

Connecticut, Massachusetts, Minnesota, New York, Ohio, Pennsylvania, Rhode Island, and Vermont all have laws that prohibit or restrict Medicare excess charges. If you live in one of these states, the gap between Plan G and Plan N narrows significantly because the excess charge protection in Plan G has no practical value for you.

In those states, the Plan N math is simple. Add up the premium savings over 12 months. Subtract the copays you'll actually pay based on how often you see a doctor. If the savings outpace the copays, Plan N wins.

What are the pros and cons of Medicare Supplement Plan G VS Medicare Supplement Plan N?

Both Medicare Supplement Plan G & Plan N are good choices for those looking to add a supplement to their Medicare plan. Plan G is the most comprehensive option, leaving the beneficiary only paying the Medicare Part B deductible annually for medical costs. Because this is the most comprehensive option for those aging into Medicare currently, these plans will be a higher monthly cost when comparing to Plan N. For those wanting to save a little on monthly premium and still have coverage that pays for most things, Plan N is a great option. Like Plan G, those who have Plan N are responsible for paying the Medicare Part B deductible annually. Once that deductible has been met, those who have Plan N will still have up to $20 copays when going to the doctor and $50 copays for an emergency room visit. These copays are the only other costs Plan N exposes someone too unless they see a doctor who does not accept Medicare assigned rates. If they see a doctor who does not accept assignment, Plan N would leave the beneficiary paying Medicare excess charges. When a doctor does not accept assignment, they can legally bill up to 15% more, which you would owe with Plan N.For someone who sees a doctor four to six times a year and lives in a state that restricts excess billing, Plan N can easily save $400 to $800 annually compared to Plan G, with very little change in day-to-day coverage. That's real money.

Plan K: Lower Premiums, Higher Stakes

Plan K operates on a fundamentally different model. Instead of covering nearly everything after the Part B deductible, Plan K covers 50% of most Medicare cost-sharing until you hit an annual out-of-pocket maximum. In 2026, that maximum is $8,000. Once you hit it, the plan pays 100% for the rest of the year.

The premium savings are substantial. In many areas, Plan K runs $60 to $100 per month less than Plan G. That adds up to $720 to $1,200 per year in premium savings alone.

But this is not a straightforward trade. Plan K also does not cover excess charges, does not cover foreign travel emergencies, and leaves you responsible for half of your Part A deductible, skilled nursing coinsurance, and Part B coinsurance until you reach that ceiling.

How does Medigap Plan K compare to Plan G for someone on a tight budget?

You would be responsible for a whole lot more out-of-pocket on a Plan G compared to a Plan K, which has $8,000 maximum out-of-pocket compared to $283 with Plan G. In my area Plan K is about $60 per month less than a Plan G. I'd recommend looking at a Plan N or maybe event Plan HDG if you are looking to same money, but want to stay on Original Medicare combined with a Supplement.Who Plan K Actually Works For

Plan K works for a specific type of person: someone who is in good health, rarely visits specialists, and has the savings to absorb a bad year. If your medical expenses typically run under $2,000 a year, the premium savings from Plan K can leave you well ahead of where Plan G would put you.

But if you have chronic conditions, see multiple specialists, or are the kind of person who loses sleep over unpredictable bills, Plan K introduces a level of financial uncertainty that Plan G eliminates. Several agents on Medicare Agents Hub have weighed in on Plan K vs. Plan G for budget-conscious seniors, and the consensus is clear: the lower premium is only a deal if you can stomach the downside.

High-Deductible Plan G: The Middle Path Most People Miss

High-Deductible Plan G (sometimes called HDG) is the least-discussed option, and several agents believe it's the most underrated. It works exactly like standard Plan G, with one catch: you pay a $2,950 deductible (2026) before the plan starts covering your costs. After that deductible is met, it behaves identically to regular Plan G. Full coverage. No copays. No excess charge exposure.

The premium difference is dramatic. In many markets, HDG premiums run $40 to $70 per month compared to $150 to $250 for standard Plan G. That's a savings of $1,000 to $2,000 per year in premiums.

Here's the math that makes agents take notice. Even in a worst-case year where you hit the full $2,950 deductible, your total cost (deductible plus premiums) often comes in lower than paying Plan G premiums all year while barely using the coverage. And in a healthy year where you spend little or nothing on medical care, you save substantially.

Is paying for a high-end Medicare Supplement plan really worth it, or is it overkill?

Paying for a high-end Medicare Supplement can be worth it if you value predictable costs, see doctors frequently, or want maximum freedom to see any Medicare provider with almost no bills beyond your premium and Part B deductible. It’s closer to “overkill” if you’re very healthy, rarely use care, and could comfortably handle higher deductibles or occasional bills in exchange for lower premiums (for example, Plan N or High-Deductible G)Compare that to Plan K's structure. Plan K's out-of-pocket maximum is $8,000. HDG's deductible is $2,950. Both have lower premiums than standard Plan G, but HDG gives you the same full coverage once the deductible is met, while Plan K only covers 50% until you hit a ceiling that's more than double. Multiple agents have pointed this out: if you're choosing between Plan K and HDG, the math favors HDG almost every time.

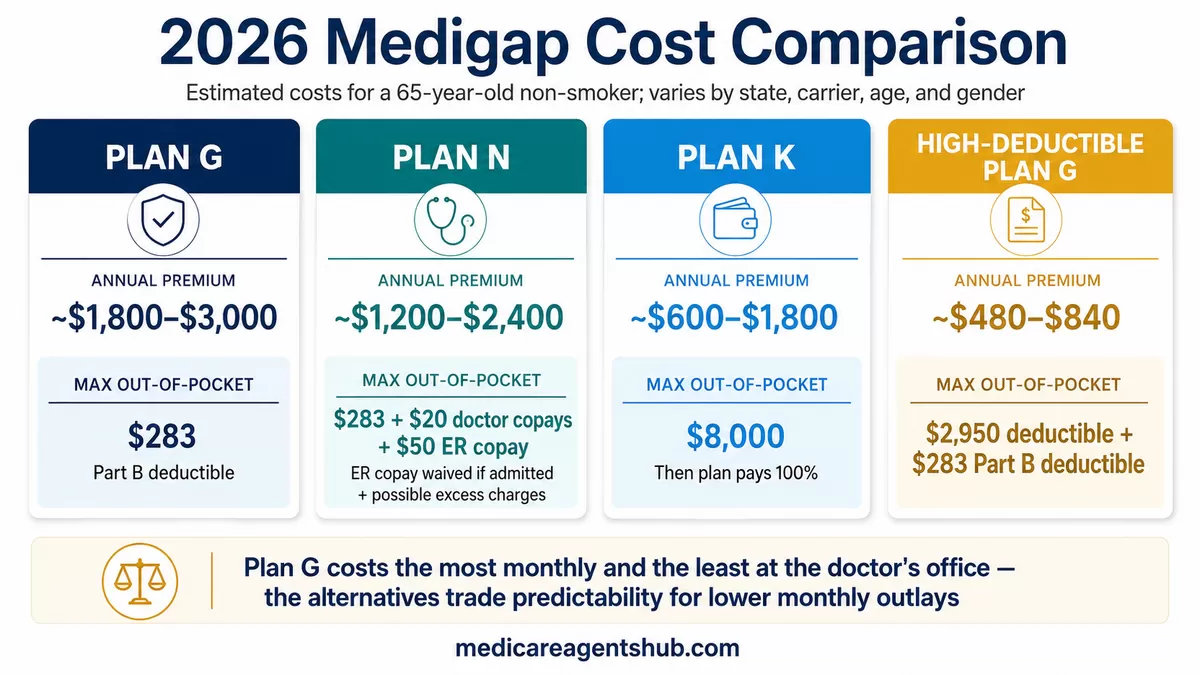

Running the Numbers: A Side-by-Side Comparison

| Plan | Estimated Annual Premium | Max Out-of-Pocket |

|---|---|---|

| Plan G | ~$1,800–$3,000 | $283 (Part B deductible) |

| Plan N | ~$1,200–$2,400 | $283 + copays + possible excess charges |

| Plan K | ~$600–$1,800 | $8,000 |

| High-Deductible G | ~$480–$840 | $2,950 + $283 (Part B deductible) |

These numbers vary by state, carrier, age, and gender. But the pattern holds: Plan G costs the most monthly and the least at the doctor's office. The alternatives trade some of that predictability for lower monthly outlays. The question is which trade-off matches your health, your budget, and your tolerance for risk.

How to Decide Which Plan Fits You

There is no universal right answer here. But there are questions that cut through the noise.

How often do you see a doctor? If you go once or twice a year for routine check-ups, you're paying Plan G premiums for coverage you're barely using. Plan N or HDG may serve you better.

Do you live in a state that bans excess charges? If yes, Plan N loses almost nothing compared to Plan G. The gap between them shrinks to a few copays per year.

Could you handle a $2,950 bill in a bad year? If so, High-Deductible G gives you the same coverage as Plan G at a fraction of the monthly cost. Think of it as self-insuring for the routine stuff while keeping full protection for the big stuff.

Are you genuinely healthy and willing to bet on it? Plan K is the highest-risk, highest-reward option. The premium savings are real, but so is the $8,000 ceiling. If a major health event hits, you'll pay significantly more than you would on any other plan on this list.

What's one tip for balancing affordability and personalization when finding the best Medicare options?

You might consider a Medicare Supplement plan N or High Deductible G instead of a regular plan G. The plan N has a small co-pay for doctor visits (no more than $20) and a $50 co-pay for the emergency room (waived if admitted within 24 hours). It doesn't cover excess billing on part B services but some states like Ohio do not allow this anyway.The Bigger Picture

Plan G became the gold standard after Plan F was closed to new enrollees in 2020. It earned that reputation for good reason. But the Medicare supplement market isn't one-size-fits-all, and agents who take the time to walk through the alternatives with their clients often find that another plan is the better fit. The plan letter is only half the decision — which carrier you choose matters just as much, since pricing, rate history, and claims handling vary significantly between companies.

If you're turning 65 or reviewing your current Medigap coverage, don't stop at Plan G. Run the math on Plan N, Plan K, and High-Deductible G. Look at your state's excess charge rules. Think about your actual health usage, not worst-case scenarios. And talk to a licensed Medicare agent who can pull real quotes. If you don't have an agent yet, find one near you here for your zip code and compare total annual costs side by side.

For free, unbiased help, you can also compare Medigap benefits on Medicare.gov or reach a local SHIP counselor, who can walk through your options at no cost.

The best plan isn't always the most expensive one. Sometimes the smartest coverage is the one that fits how you actually live.