When the Medicare Supplement You've Had for 20 Years Becomes Unaffordable

-

June 28, 2026

Your parent is 88. They bought Medicare Supplement Plan F twenty years ago, back when the premium felt reasonable. Now the monthly bill has crept past $400, maybe past $500, and the fixed income that once covered everything is stretched thin. They don't qualify for Medicaid. They're terrified of being uninsured. And they're asking you what to do.

This is one of the most common late-life Medicare crises, and it plays out in living rooms across the country every year. The good news: licensed Medicare agents have a well-worn playbook for stepping clients down from Plan F without leaving them exposed. The path isn't always simple, but it exists, and understanding it can turn a panicked situation into a manageable one.

Why Plan F Premiums Keep Climbing

Plan F is the most comprehensive Medicare Supplement plan ever offered. It covers 100% of the gaps in Original Medicare: no deductibles, no copays, no coinsurance for Medicare-approved services. Agents routinely call it the "Cadillac" of Medigap plans. That level of coverage comes with a price, and that price has been rising steadily.

There are a few reasons. First, Plan F was closed to new Medicare enrollees after January 1, 2020. That means the pool of people on Plan F is only getting older and sicker over time, with no younger, healthier enrollees entering to balance out the risk. Second, many Medigap plans use attained-age pricing, which means premiums increase as you age. A plan that cost $150 a month at 65 can easily cost $350 to $500 or more by age 85.

I'm enrolled in a Medigap Plan F, and I'm not sure how my emergency room visits are handled. Is there a copay I should expect?

With a Medigap Plan F you never have co-pays or out of pocket for any medical expenses. You should compare your Plan F side-by-side with a G plan. The only difference between the two is that you pay an annual Part B deductible with the G plan ($283 in 2026). Typically, F plans are $100-$200 more than G plans. You could be paying $1200 to $2400 to save $283. Depending on your state, there are typically ways to move you from F to G.Agents who work with older clients see this pattern constantly. The premium creep is gradual enough that many seniors don't notice until it becomes a crisis. By the time an adult child calls looking for help, the monthly bill may already be consuming a significant chunk of their parent's income.

The Real Danger: Original Medicare Has No Out-of-Pocket Maximum

Before exploring options for stepping down, it's critical to understand why simply dropping coverage is so dangerous. When agents discuss this topic, the phrase that comes up repeatedly is "incredible financial exposure."

Original Medicare (Parts A and B) covers about 80% of approved medical costs. The remaining 20% is the beneficiary's responsibility. Unlike most modern health insurance, Original Medicare has no annual out-of-pocket maximum. There is no cap. If a senior on Original Medicare alone has a major surgery, an extended hospital stay, or ongoing cancer treatment, that 20% coinsurance can add up to tens of thousands of dollars with no ceiling.

My parents, ages 90 and 91, can no longer afford their Medicare Supplement Plan F and do not qualify for Medicaid. What happens if they cannot pay the 20% not covered by Medicare after cancelling the supplement?

As far as what would happen if they had claims and had dropped their Medicare Supplements they would be at the mercy of the providers who had treated them, I have no way to answer that, but with Medicare having no limit, no max out of pocket on the 20% You could be speaking of incredible financial exposure. If they were my parents and they in fact had no choice but to drop their Medicare Supplements I would definitely recommend that they locate an Independent Agent whose focus is Medicare solutions and see what they would suggest in the way of the "best fit" Medicare Advantage Plan(s) for each of them, at least with the Advantage Plans there is a "MOOP" Maximum out of pocket safety net, usually capping anywhere from $4,000.00 for a year on up to 8 or $10,000.00, a much better option thanno cap whatsoever. Good Luck and God Bless You Folks! PS: Those MAPD plans have to by law be equal to or better than traditional Medicare A and B.More precisely, Medicare Advantage plans must cover all medically necessary services that Original Medicare covers, but they can structure access differently through networks, referrals, prior authorization, and plan-specific cost sharing.

This is the core problem families face. Dropping Plan F entirely to save on premiums might seem like a solution, but it replaces a manageable monthly cost with unpredictable, potentially catastrophic medical bills.

Agents hear from seniors who thought they could handle the 20% until they actually needed significant care. The bills from a single hospital stay without supplemental coverage can be devastating, particularly on a fixed income.

I chose Original Medicare to keep my doctors, but now I'm drowning in bills. Should I have gone with Advantage instead?

You didn’t make a wrong choice; Original Medicare lets you keep your doctors, but without a Supplement you’re responsible for about 20% of costs with no cap, which is why bills add up.A Medicare Advantage plan might lower upfront costs, or adding a Supplement could give you more predictable expenses—it’s just about finding the right fit for you now.

The goal of the step-down path is to reduce premiums while keeping some form of financial safety net in place. There's almost always a better option than going bare.

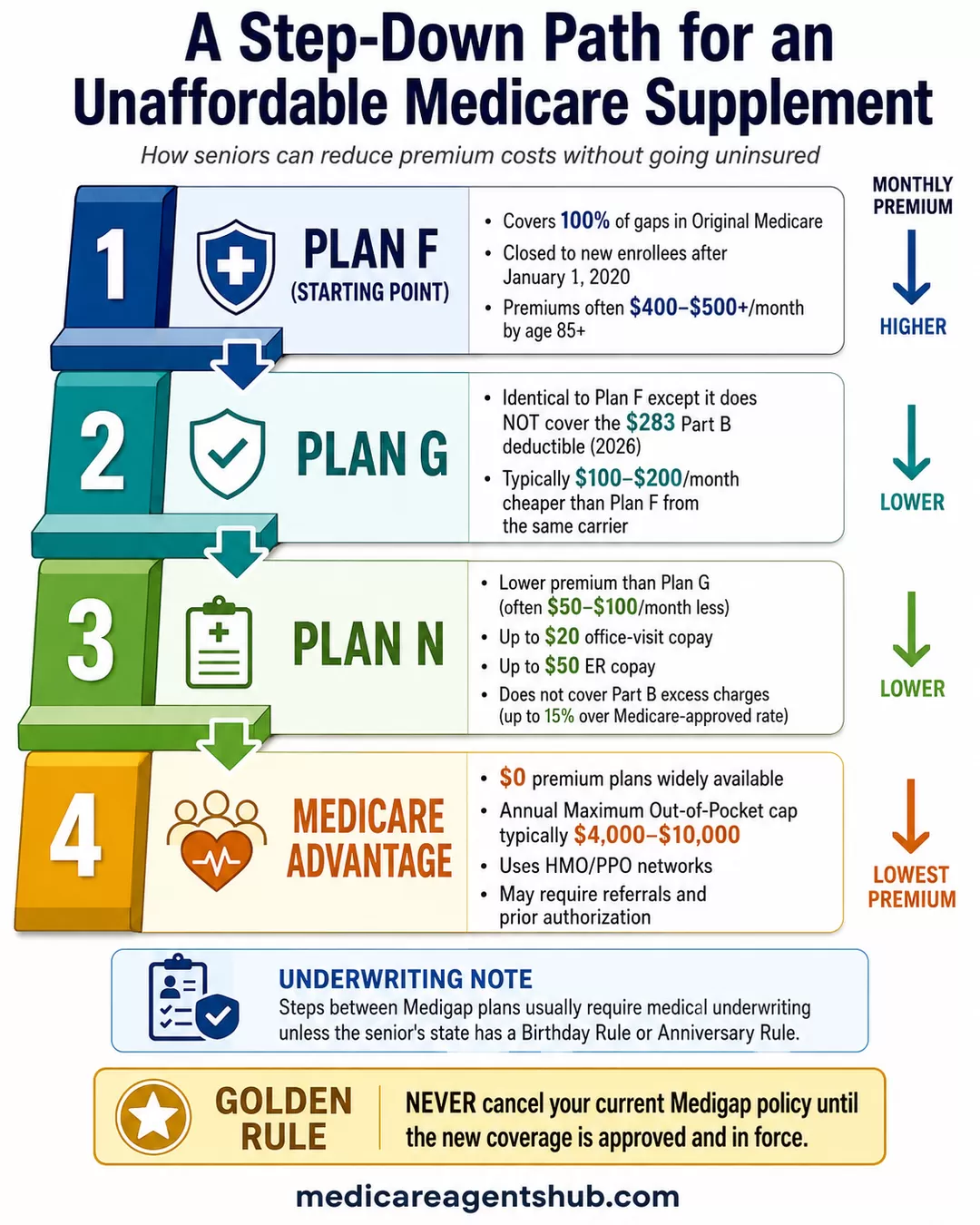

Step One: Plan F to Plan G

The first step agents almost universally recommend is moving from Plan F to Plan G. In most states, the difference between the two plans is small: Plan F covers the annual Part B deductible ($283 in 2026), and Plan G does not. That's it. Every other benefit is identical. (Massachusetts, Minnesota, and Wisconsin standardize Medigap differently.)

The premium difference, however, can be significant. Agents report that Plan F premiums are often $100 to $200 per month higher than Plan G from the same carrier. That means a senior paying $500 a month for Plan F might find Plan G at $300 to $400, saving $1,200 to $2,400 per year while only taking on a $283 annual deductible.

The math is straightforward, and it's the reason many agents view Plan F as a poor value even for seniors who can afford it. The savings from switching almost always exceed the cost of the deductible within the first few months of the year.

The catch: switching from Plan F to Plan G with a different carrier typically requires medical underwriting. The insurer will ask health questions and review prescription drug history. For a senior in their late 80s with multiple health conditions, passing underwriting can be difficult or impossible. Some carriers do allow internal downgrades (F to G within the same company) without full underwriting, but this varies by carrier and is worth asking about specifically.

In states with a Birthday Rule (more on this below), the move from F to G may be possible without any health questions at all.

Step Two: Plan G to Plan N

If Plan G is still too expensive, the next rung on the ladder is Plan N. This step involves a more meaningful trade-off in coverage.

Plan N has lower premiums than Plan G, but it introduces two cost-sharing elements. First, there may be a copay of up to $20 for some office visits and up to $50 for emergency room visits that don't result in an admission. Second, Plan N does not cover Part B excess charges. These are amounts that providers who don't accept Medicare assignment can charge above the Medicare-approved rate (up to 15% more).

For many seniors, the excess charges concern is manageable. The vast majority of doctors accept Medicare assignment, and in most parts of the country, finding providers who do is not difficult. The copays are modest. The premium savings compared to Plan G can be substantial, sometimes another $50 to $100 per month.

The same underwriting considerations apply when switching from G to N. The Birthday Rule, where available, can make this transition smoother.

The Underwriting Barrier: Why Switching Gets Harder with Age

The biggest obstacle for seniors trying to step down is medical underwriting. Outside of guaranteed issue periods and state-specific protections, any Medigap plan change requires the new insurer's approval. They'll review health history, current medications, and recent claims.

For a 70-year-old in good health, underwriting is usually straightforward. For an 88-year-old with diabetes, heart disease, or cancer history, it can be a dead end. The application gets declined, and the senior is stuck with their current premium.

Do I have to answer health questions when switching from one Supplemental/Medigap plan to another?

Medicare Supplements do have underwriting questions. Not all supplement companies have the same questions. Work with a local agent who can look at your specific health conditions to see if there is a company who's underwritting questions you may be able to pass.There are a few scenarios where you may be able to avoid underwriting questions altogether.

This is why agents are a huge resource when making Medicare decisions.

This is why the Birthday Rule (covered in the next section) is so important for older seniors. It's often the only realistic path to a different Medigap plan when health issues make standard underwriting impossible.

The Birthday Rule and Anniversary Rule: Underwriting Workarounds

For seniors who need to step down from Plan F but can't pass medical underwriting, the Birthday Rule may be the most important tool available. It's a state-level protection that gives existing Medigap policyholders a window around their birthday each year to switch to a new plan without medical underwriting. No health questions. No prescription drug checks. No denials for pre-existing conditions.

This means a senior on Plan F in a Birthday Rule state can move to Plan G or Plan N around their birthday, even if they have serious health conditions that would otherwise disqualify them from getting a new policy.

What states have the Medigap "birthday rule" and what is it?

You can switch from one Medigap plan to another without answering health questions or underwriting.California – 60 days around your birthday to switch to a plan with equal or fewer benefits with any carrier.

Idaho – 63-day window from your birthday to switch plans/companies.

Illinois – 45 days after your birthday (ages 65-75) to change plans with equal or lesser benefits (often with same insurer or affiliates).

Maryland – 30 days from your birthday to switch to a Medigap policy with equal or lesser benefits.

Nevada – 60 days from the first day of your birth month to change plans with equal or lesser benefits.

Oregon – ~30-day window around your birthday to switch plans with equal or lesser benefits.

Kentucky – 60-day period after birthday to switch Medigap plans.

Utah – 60-day window around your birthday (effective May 2025).

Virginia – 60 days from your birthday to change plans (effective July 2025).

Wyoming – 63-day period after your birthday (effective June 2025).

Oklahoma – Many sources indicate a ~60-day birthday rule window.

Louisiana – 63 days from your birthday to switch plans (often limited to same carrier or affiliates)

Delaware – Legislation effective in 2026 establishing a birthday rule (~30 days before and after)

State Medigap switching protections vary widely. Some states allow a same-or-lesser-benefit switch around your birthday. Others limit the switch to the same plan letter, the same benefits, or certain carriers. Some have a 30-day window, others 60 or 63 days. Always verify the current rule for your specific state through your state's Department of Insurance or a licensed agent before applying.

Missouri operates differently with an Anniversary Rule, which provides a similar 60-day window around your Medigap policy's anniversary date (rather than your birthday) to switch to the same plan letter with a different carrier.

A handful of states go even further. New York, Connecticut, Massachusetts, and Washington have more expansive protections that allow Medigap plan changes without underwriting outside of any birthday window. These are exceptions, and the specific rules vary, but they provide additional flexibility for seniors in those states.

Note: Birthday Rule and Anniversary Rule details change as states update their regulations. The state lists and enrollment windows described here reflect what agents reported as of mid-2026. Before acting on this information, verify the current rules for your specific state through your state's Department of Insurance or a licensed local agent.

When Medicare Advantage Becomes the Safer Landing Pad

For seniors who can't afford any Medigap premium, or who can't pass underwriting to switch plans, Medicare Advantage (Part C) may be the best remaining option. This is a significant shift in how their healthcare works, and agents approach it carefully.

The key advantage of Medicare Advantage in this situation is the Maximum Out-of-Pocket (MOOP) limit. Unlike Original Medicare, every Medicare Advantage plan is required by law to cap annual out-of-pocket costs. These caps typically range from around $4,000 to $8,000 or $10,000 per year, depending on the plan. Once that limit is reached, the member pays nothing for covered Medicare Part A and Part B services for the rest of the year, subject to the plan's network rules and in-network/out-of-network limits. Premiums and prescription drug costs are handled separately.

Many Medicare Advantage plans also have $0 monthly premiums. For a senior who was about to go bare on Original Medicare with no supplement at all, a $0-premium plan with a $5,000 MOOP provides dramatically better protection than the uncapped 20% exposure they'd otherwise face.

There are trade-offs, and agents are careful to explain them. Medicare Advantage plans use provider networks (HMO or PPO). A senior who has been on Original Medicare for decades, seeing any doctor who accepts Medicare with no referrals and no prior authorizations, will experience a very different system. Some agents, particularly in states like Texas and Maryland, caution that switching a 90-year-old onto a network plan after decades of Original Medicare freedom can be jarring and may surface prior authorization issues mid-treatment.

Others, especially agents in Kentucky and Illinois, point out that for seniors who are already priced out of Medigap, Medicare Advantage with a low MOOP is genuinely the better fit. The trade-offs of a network plan are real, but they're preferable to having no financial protection at all.

Medicare Advantage enrollment does not require medical underwriting. Seniors can enroll during the Annual Enrollment Period (October 15 through December 7) regardless of their health status.

Can You Go Back to Medigap After Switching to Medicare Advantage?

This is a question agents get frequently, and the answer is important to understand before making the jump. In most cases, switching from Medicare Advantage back to a Medigap plan requires full medical underwriting. For an older senior with health conditions, that likely means the door back to Medigap is closed. Medicare.gov warns that if you drop your Medigap policy, you may not be able to get it or any Medigap policy back later.

Can I switch from a Medicare Advantage plan to a Supplemental/Medigap plan during the Annual Enrollment Period without answering health questions?

No, you generally cannot switch from a Medicare Advantage plan to a Medigap (Supplemental) plan during the Annual Enrollment Period (AEP, Oct 15–Dec 7) without answering health questions, known as medical underwriting.Switching Process

During AEP, you can drop Medicare Advantage and return to Original Medicare (Parts A & B). However, applying for a new Medigap policy afterward typically requires insurers to review your health; they may deny coverage, charge higher rates, or exclude pre-existing conditions if you don’t qualify for an exception.

Exceptions for No Underwriting

Guaranteed-issue rights (no health questions) apply only in specific cases, like:

• Your initial Medigap Open Enrollment (6 months starting when you turn 65 and enroll in Part B).

• First 12 months (trial period) after joining Medicare Advantage.[ehealthinsurance +1]

• Plan termination, moving out of service area, or certain state rules (e.g., birthday rules in CA, OR).

The one exception is the Medicare Advantage Trial Right. If you switch to Medicare Advantage for the first time and decide it's not working, you have 12 months to return to Medigap with guaranteed issue rights (no underwriting). After that first year, the trial right expires. This is why agents stress that the move to Medicare Advantage should be treated as a significant, potentially permanent decision, not a test run you can easily reverse.

Your Policy Can't Be Taken Away: Why That Matters

One fear that drives panicked decisions is the worry that the insurance company will cancel the Medigap policy because of high claims or declining health. Agents are emphatic on this point: Medigap plans are guaranteed renewable. The insurer cannot drop you because you get sick, file too many claims, or become more expensive to cover.

Can a Medicare Supplement insurer cancel my Medigap policy?

Short answer: No—your Medigap (Medicare Supplement) policy is guaranteed renewable.As long as you keep paying your premium, the insurer cannot cancel you because of your health or claims.

This protection is required by the Centers for Medicare & Medicaid Services.

The only reasons a carrier can cancel a Medigap policy are non-payment of premiums, fraud on the original application, or the carrier withdrawing from the state market entirely. If a carrier does go insolvent or exit the market, the policyholder gets a special guaranteed issue period to enroll in a new Medigap plan without underwriting.

This matters because it means the current policy, however expensive, is a known quantity. It's a safety net that can't be pulled away. That's why the next rule is so critical.

The Golden Rule: Never Cancel Until the New Policy Is Approved

Across hundreds of agent responses on this topic, one piece of advice appears more consistently than any other: do not cancel your current Medicare Supplement until your new coverage is in place and confirmed.

Can you change Medicare Supplement plans at any time?

You can apply to change your Medicare Supplement plan at any time, but outside your initial enrollment window you'll have to go through underwriting and could be declined based on your health history. That's why I always advise my clients — don't cancel your current plan until the new one is approved.This matters because Medigap underwriting is not guaranteed. A senior who cancels Plan F and then gets denied for Plan G has no supplement at all, and getting back onto a Medigap plan with health issues can be extremely difficult or impossible outside of a guaranteed issue period.

Agents say this is the single most-violated piece of advice they give. Seniors (or well-meaning family members) cancel the expensive plan first, assuming the new one will go through. When it doesn't, they're left completely exposed. Keep the old plan in force until the new effective date is confirmed in writing.

State Assistance Programs Worth Checking First

Before making any plan changes, some agents recommend checking whether the senior qualifies for state or federal assistance programs that could reduce their existing costs. The Medicare Savings Programs (MSP), for example, can help pay Part B premiums and may cover some cost-sharing for people with limited income and resources, even if they don't qualify for full Medicaid.

The Extra Help (Low-Income Subsidy) program can reduce Part D prescription drug costs. And some states have additional programs that may not appear in a standard Medicaid screening. An agent or a State Health Insurance Assistance Program (SHIP) counselor can help identify whether any of these apply.

These programs won't always solve the problem, but they're worth exploring before making irreversible coverage decisions.

How to Start the Conversation

If you're an adult child watching a parent struggle with Medigap premiums, the first step is to connect them with an independent Medicare agent or broker who is licensed in their state. Independent agents (as opposed to captive agents who represent a single carrier) can compare options across multiple insurance companies and find the best fit for the specific situation.

The key questions to bring to that conversation:

- What is the current Plan F premium, and what would Plan G or Plan N cost from the same carrier or a competing carrier?

- Does the state have a Birthday Rule or Anniversary Rule that would allow a switch without underwriting?

- If underwriting is required, what health conditions might affect approval?

- What Medicare Advantage plans are available in the area, and what are their MOOP limits and provider networks?

- Does the senior qualify for any state assistance programs (MSP, Extra Help, SHIP)?

The agents who answered questions about this exact situation on Medicare Agents Hub overwhelmingly agree on the core principle: some coverage is always better than no coverage. Whether the answer is stepping down to a less expensive supplement or transitioning to Medicare Advantage, the goal is to keep a financial safety net in place while reducing the monthly burden.

This is not a decision to make alone. A licensed agent can walk through the numbers, check underwriting eligibility, verify what plans are available locally, and make sure nothing falls through the cracks during the transition. Find a licensed Medicare agent near you to start the conversation.