The IEP Trap: Why Some Agents Say Picking Medicare Advantage at 65 Is the Biggest Mistake You Can Make

-

December 16, 2025

A $0 Premium That Could Cost You Everything

You just turned 65. The mailbox is stuffed with glossy Medicare Advantage brochures promising $0 premiums, dental coverage, gym memberships, and grocery allowances on some plans. The choice seems obvious. Why pay $150 to $250 a month for a Medigap plan when you can get all of that for free?

That logic makes sense on the surface. And for many people, Medicare Advantage works fine for years. But a growing number of licensed Medicare agents are warning their clients: the decision you make at 65 might be the one that traps you at 78.

The problem isn't Medicare Advantage itself. The problem is what happens when you try to leave.

The 6-Month Window Most People Don't Know Exists

When you first enroll in Medicare Part B, you get a one-time, 6-month Medigap Open Enrollment Period. During this window, insurance companies must sell you any Medigap plan they offer, regardless of your health. No medical questions. No denials. No higher premiums based on pre-existing conditions.

Once that window closes, the rules change completely. In most states, if you want a Medigap plan after your initial enrollment, you'll face medical underwriting. That means the insurance company can review your health history, charge you more, or deny you outright.

One agent put it bluntly: "You don't get homeowners insurance when the house is on fire." If you spend 10 years on a Medicare Advantage plan and then develop cancer, heart disease, or diabetes requiring insulin, your chances of qualifying for a Medigap plan in most states become very limited, unless you happen to live in a state with guaranteed-issue protections.

This is the trap. And according to multiple agents we spoke with, it's the single most misunderstood aspect of the Medicare system.

I missed my Medigap window by a few months and now no one will cover me without underwriting. Why isn't this rule more well known?

It’s mentioned in the Medicare & You handbook… but it’s not emphasized the way it should be. Most people are focused on:• Part A

• Part B

• Drug plans

• Medicare Advantage commercials

Medigap timing gets lost.

Insurance companies don’t advertise underwriting rules

Companies selling Medicare Supplement policies have no incentive to shout:

“After 6 months, we can deny you.”

They focus marketing on:

• “Freedom to choose doctors”

• “No networks”

• “Predictable costs”

The underwriting fine print isn’t the headline.

Agents don’t always explain long-term consequences

Some agents:

• Focus on getting someone enrolled

• Don’t explain future switching limitations

• Or assume clients won’t change later

Once someone chooses Medicare Advantage at 65 and later wants to move to Medigap, underwriting becomes a shock.

"Think About How Your Health Will Be at 80, Not at 65"

The agents who warn against choosing Medicare Advantage at initial enrollment aren't anti-MA. They're anti-short-term thinking.

One licensed agent framed it this way: "When choosing a plan, people should be thinking 'how will my health be 10 years from now,' not 'how's my health right now?'" Another said flatly that signing up for an Advantage plan at first eligibility is "the biggest mistake people can make."

Their reasoning comes down to a few specific concerns:

Medical underwriting locks the door behind you. If you choose MA at 65 and later want to switch to a Medigap plan, you may not be able to pass underwriting. Several agents described clients who spent years on Advantage plans, developed serious health conditions, and then discovered they couldn't switch back. As one agent explained: "The inability to switch back to a Medicare supplement with preexisting conditions is not a common option for very sick folks. Cancer, stroke, COPD, heart attack, insulin, dementia" all make it extremely difficult.

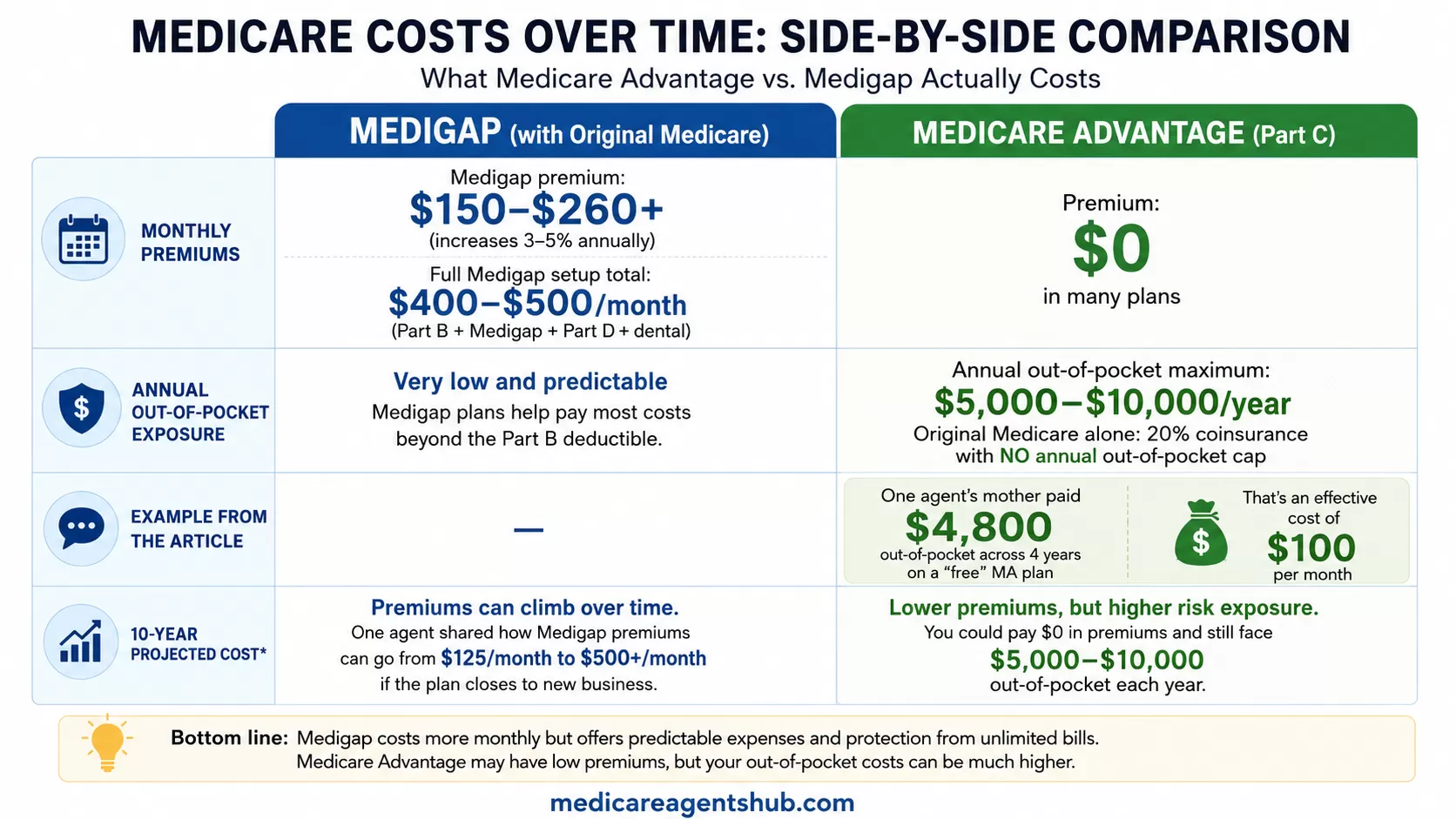

The costs compound when you actually need care. MA plans advertise $0 premiums, but the out-of-pocket maximums can reach $5,000 to $10,000 per year. One agent noted that clients who become seriously ill face those maximum costs "year after year." Another calculated that their own mother's "free" MA plan cost her an extra $100 per month when the $4,800 out-of-pocket maximum was spread across the four years between her two surgeries.

Prior authorizations and network restrictions get worse with age, not better. When you're healthy at 65 and seeing your primary care doctor once a year, network limitations barely register. When you're managing multiple specialists, need regular imaging, or require skilled nursing care at 78, those restrictions become the central obstacle in your healthcare. Several agents described clients who call Medicare Advantage plans "Disadvantage Plans" once they start needing significant care.

If you had to pick just one, what's the worst Medicare-related decision someone can make?

Signing up for an Advantage plan when they are first eligible is the biggest mistake people can make in my opinion. When choosing a plan, people should be thinking "how will my health be 10 years from now" not "how's my health right now?"The Other Side: Why Many Agents Still Recommend MA at 65

Not every agent agrees with the "never start on MA" position. And their counterarguments deserve serious consideration.

Medigap premiums aren't static. Multiple agents pointed out that Medigap premiums increase every year, sometimes significantly. One agent described clients who started paying $125 per month for a supplement but saw their premiums climb to $500 or more after their plan closed to new business. The agents who defend MA note that for people on fixed incomes, those rising premiums can become unaffordable by the time they're 75 or 80, potentially forcing them onto an Advantage plan anyway.

The budget reality is real. "If everyone could afford a Medicare Supplement Plan, they would probably have one," one agent wrote. Between the standard Part B premium ($202.90/month in 2026), a Medigap premium ($150-$260+), a standalone Part D drug plan, and separate dental coverage, a full Medigap setup can easily cost $400 to $500 per month. Many retirees simply cannot absorb that expense. An MA plan with a $0 premium, built-in drug coverage, and dental/vision/hearing benefits provides a more affordable entry point, even if the long-term math doesn't always favor it.

MA has a built-in financial ceiling. Original Medicare alone has no maximum out-of-pocket limit. If you have Part A and Part B with no supplemental coverage, you're responsible for 20% of all Medicare-approved costs with no cap. Medicare Advantage plans, by contrast, have annual out-of-pocket maximums. For someone who can't afford Medigap, MA provides financial protection that Original Medicare alone does not.

Most MA enrollees are satisfied. Over half of all Medicare beneficiaries are now on Advantage plans, and most report being happy with their coverage. Several agents noted they personally use MA plans and have no complaints. The regret stories are real, but they don't represent the typical experience for enrollees who stay relatively healthy.

Why do some people regret choosing a Medicare Advantage plan over Original Medicare?

When it comes to Medicare choices, most regrets come from a lack of knowledge or understanding of how a plan works. Whether it's an Advantage Care plan with a network of doctors or a Supplemental plan with ever-higher premiums, knowing how it works and what ot expect is key to high satisfaction. Neither Original Medicare (with a Supplemental plan) nor an Advantage Care plans are perfect. Both have upside AND downsides. The critical factors are understanding how the plan works and choosing one that fits your individual needs.The Escape Hatches: Guaranteed Issue and State-Specific Rules

For people who chose Medicare Advantage and now want out, the situation isn't always hopeless. But the exit routes are narrower than most people expect.

The 12-month trial right (new-to-Medicare version). If Medicare Advantage was your first Medicare choice at 65, federal law gives you a one-time, 12-month window to change your mind. Drop the MA plan within your first year of enrollment, and you get guaranteed-issue rights to buy any Medigap policy sold by any insurance company in your state, with no medical underwriting. This is the most direct escape hatch from the "IEP trap," but the clock is short and most people don't know it exists until it's already run out.

The 12-month trial right (switch-back version). If you had a Medigap plan first and then switched to Medicare Advantage, you have 12 months to switch back to your original Medigap plan (or a comparable one) without underwriting. Also a one-time right. After that window closes, you're subject to underwriting in most states.

Guaranteed-issue states. A handful of states, including New York, Connecticut, and Massachusetts, have guaranteed-issue protections that go beyond federal minimums. In these states, you may be able to get a Medigap plan without underwriting outside of your initial enrollment period. Some agents who recommend MA at initial enrollment specifically advise clients to be aware of their state's rules as a potential exit strategy.

Birthday rule states. States like California, Illinois, Louisiana, and Oregon have "birthday rules" that let you switch Medigap plans around your birthday without underwriting. This doesn't help you get into Medigap from MA, but it protects people who are already on Medigap from being stuck with a plan whose premiums have spiked.

The catch. None of these escape hatches are guaranteed to help everyone. If you're in a state without strong protections, have been on MA for years, and have developed significant health issues, your options may be extremely limited. That's the core of the "IEP trap" argument: by the time you realize you want out, the door may already be closed.

How to Think About Medicare 10 Years Out

The agents on both sides of this debate agree on one thing: most new Medicare beneficiaries make their choice based on today's budget and today's health, without thinking about what Medicare will look like for them at 75 or 80.

Here's a framework several agents recommended:

If you can afford Medigap at 65, seriously consider it. The guaranteed-issue window is the single most valuable enrollment right you'll ever have. Once it's gone, it's gone. Even if you're perfectly healthy at 65, you're buying future flexibility. One agent summarized: "Get the best when there's no underwriting to deny you, and the best plans are available."

If you can't afford Medigap, don't feel guilty about choosing MA. A $0-premium Advantage plan with a $4,000 to $8,000 annual out-of-pocket cap is vastly better than Original Medicare alone. Just go in with your eyes open about what the trade-offs are, and pair it with a hospital indemnity plan if possible to reduce your exposure.

Know your state's rules. If you're choosing MA, understand what guaranteed-issue protections your state offers. Some states give you more flexibility to switch later; others give you almost none. This is one of the most important questions to ask your agent before you enroll.

Factor in rising Medigap premiums. If you go with Medigap at 65, don't assume you'll be paying the same premium at 80. Ask about the carrier's rate history. Plan financially for 3-5% annual increases, and more in some years. If your budget is tight now, it'll be tighter in 15 years.

Talk to an independent agent who offers both. Multiple agents emphasized that agents who carry both Medigap and Medicare Advantage are less likely to steer you toward one product for commission reasons. One agent was candid about the industry reality: in many markets, MA plans pay roughly double the first-year commission of Medigap plans, which creates a structural incentive that doesn't always align with the client's best interest.

If Medicare Supplement (Medigap) plans are better for long-term coverage, why don't more people choose them?

Many people don’t choose Medicare Supplement (Medigap) plans because they often have higher monthly premiums, and the costs are more predictable but paid upfront. Others prefer Medicare Advantage plans because they bundle extra benefits like dental or vision and may have lower premiums, even though the long-term costs can vary—so the choice often comes down to budget, health needs, and personal preference.The Bottom Line: There Is No Perfect Medicare Plan

The agents who call MA at 65 a trap are protecting their clients from a specific, irreversible risk: losing Medigap access when they need it most. The agents who recommend MA are helping their clients afford quality coverage today, with built-in financial protections that Original Medicare alone doesn't provide.

Both sides are right, for different people.

The real mistake isn't choosing Medicare Advantage or choosing Medigap. It's making a 30-year healthcare decision in 30 minutes because you didn't understand what you were giving up. The 6-month Medigap Open Enrollment window is the most consequential deadline in Medicare, and most people don't even know it exists until it's too late.

Before you choose, find a local Medicare agent who represents both types of plans and will walk you through what each option looks like not just this year, but a decade from now.