What Floridians Need to Know About Medicare at 65

Turning 65 is one of the most important milestones in your financial and healthcare life, especially if you live in Florida. With one of the largest senior populations in the country, Florida offers a wide range of Medicare options, but that also means more decisions, more confusion, and more opportunities to make costly mistakes.

Whether you're planning to retire, still working, or helping a loved one navigate the process, this guide will walk you through everything you need to know about Medicare when turning 65 in Florida, step by step.

Why Turning 65 Matters

Age 65 is when most Americans become eligible for Medicare, the federal health insurance program designed primarily for people 65 and older. Medicare covers millions of Americans and provides a foundation for healthcare coverage in retirement.

In Florida, where healthcare costs and retiree populations are both high, making the right Medicare decisions early can save you thousands of dollars over time.

Understanding Medicare Basics

Before diving into enrollment, it's important to understand the different parts of Medicare. Each plays a specific role:

Original Medicare

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facilities, hospice, and some home health care.

- Part B (Medical Insurance): Covers doctor visits, outpatient care, preventive services, and medical equipment.

Is Medicare Part A enough for hospital coverage?

Medicare Part A is generally not enough for comprehensive hospital coverage, as it only covers inpatient stays and includes significant deductibles and coinsurance. While it covers essential inpatient services, it does not cover outpatient care, private rooms, or long-term care, and features a ($1,736) deductible per benefit period in 2026. Additional coverage (Part B or Medicare Advantage) is necessary.Additional Coverage Options

- Part C (Medicare Advantage): Private plans that replace Original Medicare and often include extra benefits like dental, vision, and hearing.

- Part D (Prescription Drug Plans): Helps cover the cost of medications.

- Medigap (Supplement Plans): Helps pay out-of-pocket costs like deductibles and coinsurance.

Florida residents can choose any combination of these options depending on their needs. Medicare Supplement Plans: Which is Right for You?

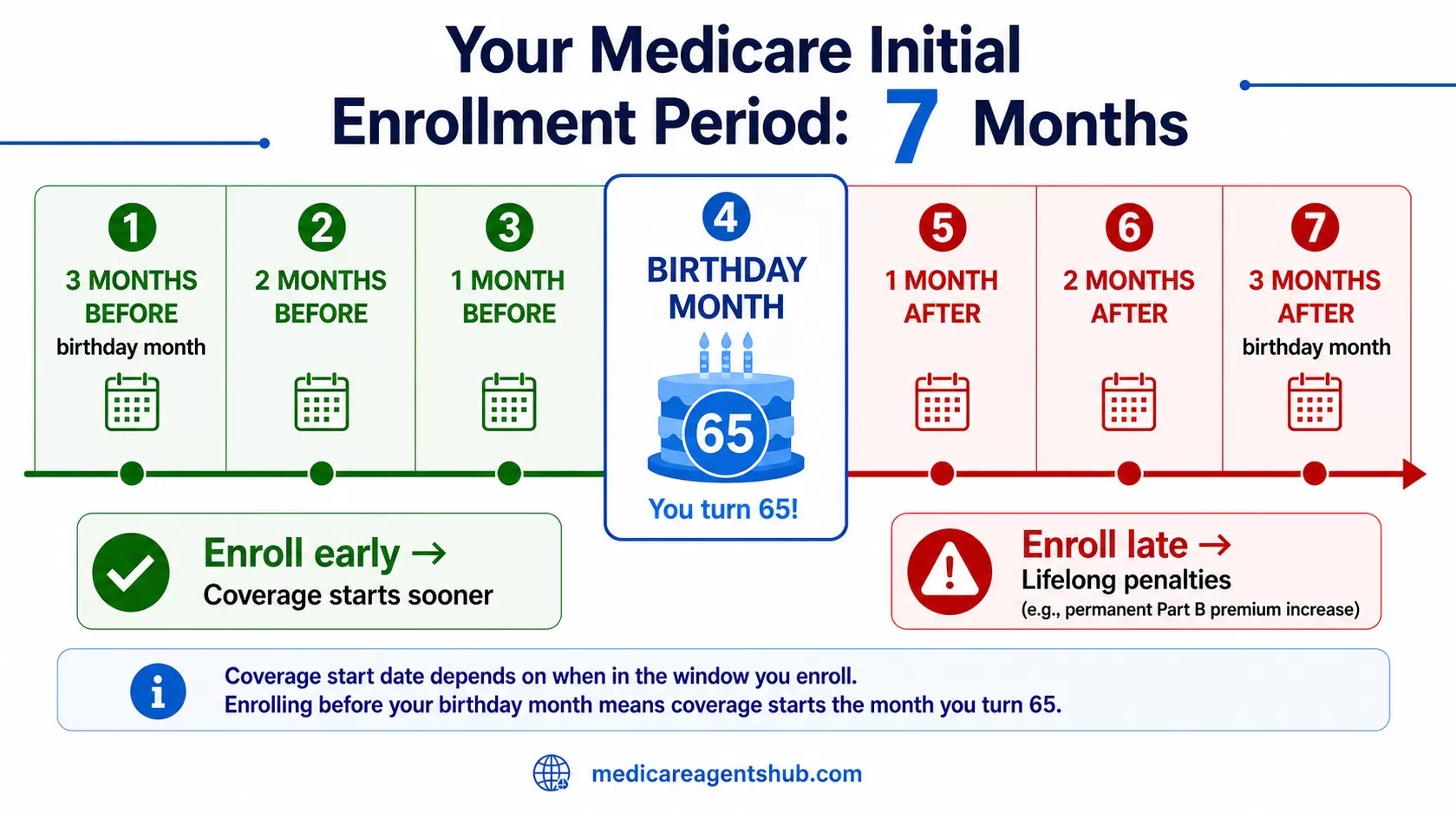

Your Initial Enrollment Period

When you turn 65, you get a 7-month enrollment window known as your Initial Enrollment Period:

- 3 months before your birthday month

- Your birthday month

- 3 months after

This is your best opportunity to enroll in Medicare without penalties.

Why Timing Matters

- Enroll early → Coverage starts sooner

- Enroll late → You may face lifelong penalties

For example, missing Part B enrollment could result in a permanent premium increase. For more details on enrollment windows and deadlines, see how to avoid Medicare penalties when turning 65.

Are You Automatically Enrolled?

It depends on your situation:

- Yes, automatic enrollment: If you're already receiving Social Security benefits

- No, you must enroll yourself: If you're not collecting Social Security yet

If you're not automatically enrolled, you'll need to sign up through Social Security.

What If You're Still Working at 65?

This is one of the most common, and most misunderstood, situations.

If you (or your spouse) still have employer-sponsored health insurance:

- You may be able to delay Part B without penalty

- You'll qualify for a Special Enrollment Period (SEP) later

However, not all employer plans are equal. The size of your employer and the type of coverage you have can affect how Medicare works with your insurance.

Key tip: Always compare your employer coverage to Medicare before deciding to delay. If you're considering the switch, read more about how to switch from employer health insurance to Medicare.

What do I need to do if I didn't take Medicare at 65 and am now retiring?

Upon retiring after age 65, you must enroll in Medicare during your 8-month Special Enrollment Period (SEP) to avoid penalties, starting when your employer coverage ends. You need to submit Forms CMS-40B (Application) and CMS-L564 (Employment Information) to Social Security to prove "creditable" coverage and avoid late fees.Medicare Options in Florida

When you enroll, you'll face a major decision:

Option 1: Original Medicare + Supplement + Part D

This includes:

- Part A + Part B

- A Medigap plan

- A standalone Part D drug plan

Pros:

- Maximum flexibility (see any doctor who accepts Medicare)

- Predictable out-of-pocket costs

Cons:

- Higher monthly premiums

For a closer look at supplement plans, see the pros and cons of Medicare Supplement insurance.

Option 2: Medicare Advantage (Part C)

These plans are offered by private insurance companies and bundle:

- Hospital + medical coverage

- Often prescription drugs

- Extra benefits (dental, vision, gym memberships)

Pros:

- Lower premiums

- Additional benefits

Cons:

- Network restrictions

- Potential for higher out-of-pocket costs when you need care

Can I keep seeing my current doctors if I switch to a Medicare Advantage plan, or do I have to find new ones?

That depends on the Medicare Advantage plan that you switch into. I would recommend that you make sure the doctors that you're using accept the plan you're thinking of joining.Otherwise, you will have to switch to new doctors if the doctors that you use aren't in the new plan's network.

Medicare Costs in Florida

Even though Medicare provides essential coverage, it's not free.

Common Costs Include:

- Part B premium (standard monthly premium, varies by income)

- Deductibles and coinsurance

- Prescription drug costs

- Supplement or Advantage plan premiums

Recent updates have also introduced changes like caps on prescription drug spending, which can significantly help beneficiaries manage costs.

Medigap Open Enrollment

If you choose Original Medicare, your Medigap enrollment window is critical.

You get a 6-month Medigap Open Enrollment Period starting when:

- You are 65 or older

- AND enrolled in Part B

During this time:

- You cannot be denied coverage

- You cannot be charged more for pre-existing conditions

After this window, underwriting may apply, making coverage more expensive or unavailable. Learn more about your options in our guide to Medicare Supplements.

Prescription Drug Coverage (Part D)

Even if you don't take medications now, enrolling in a Part D plan is usually a smart move.

Why?

- Delaying enrollment can trigger lifetime penalties

- Drug costs can rise unexpectedly with age

New Medicare rules are improving affordability, including caps on out-of-pocket drug costs. For help choosing the right plan, check out our guide to choosing the right prescription drug plan.

Common Medicare Mistakes to Avoid

Turning 65 comes with a lot of moving parts. Here are the most common mistakes Florida residents make:

1. Missing Your Enrollment Window

This can lead to permanent penalties and coverage delays.

2. Assuming Medicare Is Free

Many people are surprised by premiums, deductibles, and out-of-pocket costs.

3. Choosing the Wrong Plan Structure

Picking between Medicare Advantage and Original Medicare without understanding the trade-offs can be costly.

4. Not Reviewing Drug Coverage

Even one expensive prescription can significantly impact your budget.

5. Ignoring Provider Networks

Especially important with Medicare Advantage plans.

Florida-Specific Medicare Considerations

Florida has unique factors that affect your Medicare decisions:

Large Senior Population

More plan options, but also more complexity.

Competitive Insurance Market

You'll find a wide variety of Medicare Advantage and Medigap plans. For a deeper look at what local experts recommend, read what Florida Medicare brokers want you to know before choosing a plan.

Weather and Lifestyle

Seasonal residents ("snowbirds") should consider coverage that works across multiple states.

When Does Your Coverage Start?

Your Medicare start date depends on when you enroll:

- Enroll before your birthday month → Coverage starts the month you turn 65

- Enroll after → Coverage may be delayed

Planning ahead ensures no gaps in coverage.

How to Enroll in Medicare

You can enroll in Medicare through:

- Social Security website

- Phone

- Local Social Security office

Enrollment can also coincide with applying for Social Security benefits.

Special Situations to Consider

If You Have an HSA: You'll need to stop contributing before enrolling in Medicare to avoid tax penalties.

If You're Retiring Soon: Coordinate your Medicare start date with the end of your employer coverage.

If You're Helping a Parent or Spouse: Make sure decisions align with their doctors, prescriptions, and budget.

Planning Ahead Makes All the Difference

Turning 65 in Florida is more than just a birthday, it's a major financial decision point.

The choices you make now will affect:

- Your healthcare access

- Your monthly expenses

- Your long-term financial security

The key is to start early, understand your options, and avoid rushing into decisions.

Medicare can be overwhelming, but you don't have to figure it out alone. Working with a licensed local agent can help you:

- Compare plans side-by-side

- Avoid costly mistakes

- Find coverage tailored to your doctors, prescriptions, and budget

If you're in Florida, especially in areas like Jacksonville, having a local expert who understands the market can make all the difference. Find a Medicare agent in Florida to get started.

Turning 65 is your opportunity to take control of your healthcare future. With the right guidance and a clear understanding of Medicare, you can confidently choose coverage that protects both your health and your finances for years to come.