What Florida Medicare Brokers Want You to Know Before Choosing a Plan

-

Last Updated July 23, 2026

Florida has more than 5 million Medicare beneficiaries, the second-highest total in the country, and the decisions they face are anything but simple. Between county-level plan variation, a massive provider landscape, and an advertising blitz that ramps up every fall, choosing the right coverage here requires more than a Google search.

We went to the people who navigate this every day. Medicare Agents Hub lists more than 6,000 Florida-licensed Medicare brokers, from communities like Margate and Oviedo to Lakeland, The Villages, and everywhere in between. We asked them a simple question: What do you wish every senior knew before making their Medicare decision?

Their answers covered everything from enrollment timing to the fine print on "free" plans. Some of them agreed. Some of them didn't. All of them were worth hearing.

That local variation matters because a retiree in Miami-Dade, The Villages, Tampa, Palm Coast, or the Panhandle may be looking at entirely different plan options. Miami-Dade County alone has over 40 Medicare Advantage plans to choose from. Some rural Panhandle counties have fewer than 10.

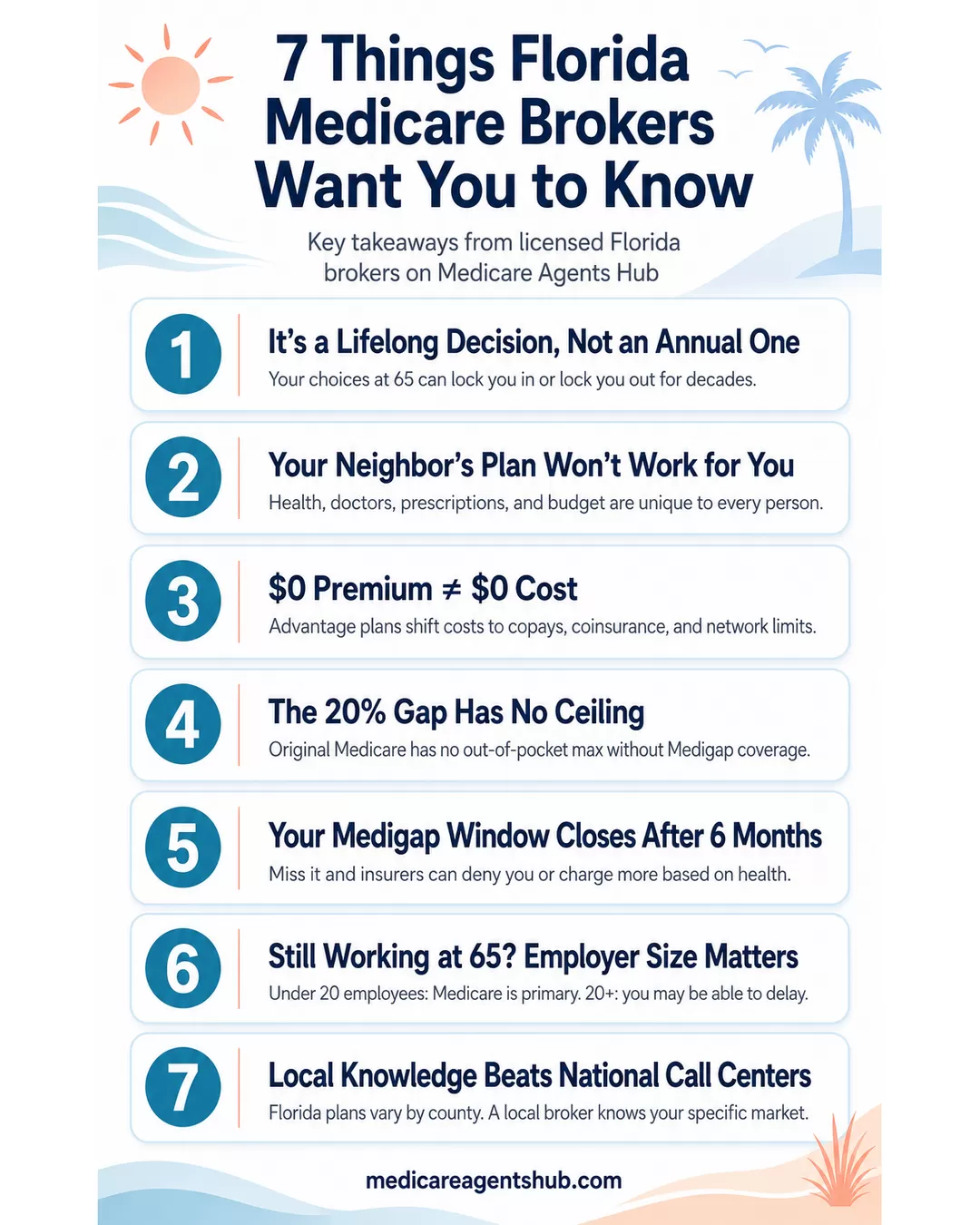

This Isn't an Annual Decision. It's a Lifelong One

When we asked Florida agents about the biggest mistake seniors make when enrolling, one theme came through louder than anything else: people treat Medicare like picking a phone plan. It's not. The choices you make at 65 can lock you in, or lock you out, for decades.

What is the biggest mistake seniors make when enrolling in Medicare?

The biggest mistake that I see seniors make when enrolling in Medicare is choosing a plan based only on the monthly premium and not on their doctors, medications, and total out-of-pocket costs.A low premium can end up being expensive if your prescriptions aren’t covered or your providers are out of network, or the plan has high copays and deductibles.

Also missing your Medigap open enrollment window can be permanent, which is why getting personalized guidance before enrolling is so important.

Medicare isn't something you set and forget. The plan structure you choose at enrollment, particularly whether you go with Medicare Advantage or Original Medicare with a supplement, shapes your costs and options for years to come. In Florida especially, where carriers like Humana, Aetna, and UnitedHealthcare are constantly reshuffling their county-level networks, a choice that works today can look very different two years from now.

Your Neighbor's Plan Won't Work for You

"My friend has this plan and loves it" is one of the most common, and most dangerous, starting points for a Medicare decision. When we asked brokers whether Original Medicare or Medicare Advantage is better, the answer was almost always the same: it depends entirely on you.

Is Original Medicare or Medicare Advantage better? Why do you recommend one over the other?

My joke is, the words insurance and best do not belong in the same sentence.They are different, pros and cons to each, as is everything in life..

Supplements give you the most freedom and flexibility, but freedom is not free. Rising cost over time with supplements could lead to you dropping the coverage when you need it the most. This is the most reliable coverage with the least amount of restrictions, but overall the highest cost when looking at the G or N which are most common. Hi Deductible G could be a good compromise and competitive to advantage options.

Advantage plans can have lower costs, but come with more restrictions, such as getting approval for treatments and surgeries. I don't think advantage is all doom and gloom as many seem to propose, however, you are making a deal with the devil.

My rule of thumb is that, if the client is not too concerned about changing doctors in the future or not being able to access some facilities like Mayo Clinic in FL, as of recent, while looking to save money, then MA plans are viable.

My next rule of thumb is that unless there is 100/mo of savings, then MA plans may not be worth the restrictions. In that case Hi Ded G would be a strong option to consider.

Ultimately, use a hammer for nails and a screwdriver for screws, to get the best results possible.

Your health history, your doctors, your prescriptions, and your budget are yours alone. A plan that covers someone with no chronic conditions and a low prescription load could be a financial disaster for someone managing diabetes or heart disease. That matters more in Florida than most states. According to KFF's 2024 enrollment data, roughly 60% of Florida's Medicare population is enrolled in Medicare Advantage, well above the national average. In Miami-Dade County, that figure is closer to 80%. More plans competing for your enrollment means more ways to pick the wrong one if you're going off someone else's recommendation. Before you take advice from anyone who isn't looking at your specific situation, understand the mistakes that catch people off guard.

The "$0 Premium" Question, Answered Two Ways

Few topics split the room like Medicare Advantage pricing. We asked Florida brokers point-blank: are Medicare Advantage plans really "free," or is that just clever marketing? We got two very different answers, and both are worth reading.

The Case for Advantage Plans

Some brokers see real value in the $0 premium model, especially for seniors on a tight budget.

Are Medicare Advantage plans really "free," or is that just clever marketing?

Most Advantage plans really do cost $0 each month (this is additional monthly - remember that pesky $185 part B premium will still come out of your social security check each month), which is a lifesaver if a hefty monthly premium just isn’t in the budget due to your part B premium. Yes, you’ll have co‑pays when you visit the doctor or fill a prescription, but here’s the big win: every plan puts a hard ceiling on what you’ll spend in a year.With Original or Traditional Medicare (part A and B only) you’re on the hook for 20 % of every bill—whether it’s a $100 X‑ray ($20 out of pocket) or a $100,000 surgery ($20,000 out of pocket!). An Advantage plan might cap your yearly costs at, say, $4,500 or $6,700. Once you hit that limit, the plan pays 100 % of covered services. For many folks, that cap is the difference between a manageable expense and a second mortgage.

Each plan sets its own max‑out‑of‑pocket and co‑pay schedule, so talking with a licensed, independent broker (that’s me!) is the best way to see the full landscape and pick the plan that saves you the most. If high monthly premiums aren’t an option—or you just like keeping more money in your pocket—let’s chat. Reach out today and we’ll find the Advantage plan that fits your health needs and your wallet.

The Case Against the Marketing

Others see it differently, and they're not shy about saying so.

Are Medicare Advantage plans really "free," or is that just clever marketing?

Clever Marketing!!! - the 9500 commercials you see during the Open Enrollment period, EVERYDAY, will never show you the limitations of your rights in your own health moving forward. It doesn’t speak as to the limited network they operate through, or the fact that the BEST doctors in the fields DO NOT ACCEPT MA plans!!! The entity you decided to ensure with can decide whether to allow a surgery or deny it, or require you to go through more tests while your health declines. This builds stress! And stress hurts organs and bodily operation, and unfortunately truly kills. Also, most MA plans DO JOT travel with you, or make you jump through hoops in order to prove you have coverage. Remember, you have to be in Network!So do want to give up your freedom and control of your health? Do you care if you travel - even out of county - that you may be in a Non-Network, no coverage zone? Do you want to give someone else the authority to decide if you will have a needed surgery or not? Is that grocery card worth it?

They have you focused on 1 thing that is less important, than where the real focus should be. It’s like a magician!!! So don’t be tricked!

The $0 premium is real, but it doesn't mean $0 cost. Advantage plans shift expenses to the point of care: copays, coinsurance, and network restrictions that vary wildly by county. In South Florida, carriers like Devoted Health and Humana dominate with aggressive $0 premium plans, but their provider networks look completely different in Broward versus Palm Beach. Every county in Florida has at least one $0 premium MA option available, but coverage details and provider access are not remotely the same from one ZIP code to the next. Understanding the difference between HMO, PPO, and POS Medicare plan structures also matters here, since network type directly affects which doctors you can see.

The 20% Coinsurance Gap Under Original Medicare

One of the most common misconceptions about Medicare is that once you have it, you're fully covered. You're not. For Part B services under Original Medicare, Medicare generally pays 80% of the approved amount after the deductible, leaving you responsible for the remaining 20% unless you have supplemental coverage. There is no built-in annual out-of-pocket maximum under Original Medicare alone. A single hospitalization or a cancer diagnosis can produce bills with no ceiling.

What is one of the the most common misconceptions people have about Medicare?

The most common misconception I hear about Medicare is that it will cost them less money once they have that red white and blue card. What people don't realize or understand are charges and surcharges that are placed on Medicare Part A (for some people) Medicare Part B monthly charges and IRMAA (Income Related Monthly Adjustment Amount) for higher income earners which dates back two years from the time you become eligible for Medicare. Don't forget about Late Enrollment Penalties that can be added monthly. Also there is no "cap" as to what your Medical expenses could be. Medicare has an 80/20 coinsurance split. Meaning Medicare pays 80% of the bill and you pay the remaining 20% of the bill. Most people think, that's not too bad when seeing a Doctor they go to once or twice a year but what about the Critical Illnesses that bring you to the hospital and if you had a helicopter ride to get there. That would bankrupt most people.This is the gap that Medigap policies are designed to fill. In Florida, Plan G premiums for a 65-year-old typically run between $225 and $280 per month depending on carrier and location, with companies like Cigna, Mutual of Omaha, and Florida Blue among the most common options. Whether that monthly cost is worth the protection depends on your risk tolerance and health outlook, but the important thing is to understand what you're exposed to without it. Too many seniors learn about the 20% when they're already staring at a bill.

Why Your First Six Months on Medicare Matter Most

When we asked agents about Medicare decisions people regret, a clear pattern emerged: the Medigap open enrollment window. Miss it, and you may not get the same access to supplemental coverage later.

Here's how it works. During your six-month Medigap open enrollment period, which starts the month you're both 65 and enrolled in Part B, insurers must sell you a policy regardless of your health. After that window closes, medical underwriting can come into play.

What's one Medicare decision that too many people regret later?

One Medicare decision too many people regret later is not considering a Medicare Supplement plan when they first become eligible. At that point, you're usually in what I call a "get out of jail free" window, meaning you can get a plan with no health questions asked. But if you wait and try to enroll later, you may have to go through medical underwriting—and could be denied based on your health. Some people start with a Medicare Advantage plan to save on monthly premiums, only to find out later that their out-of-pocket costs are higher than expected or that their preferred doctors aren’t in-network. By then, switching isn’t always simple. That’s why it’s so important to look at your long-term health needs and not just what seems cheapest upfront.This is one of the few areas of Medicare where the timing is truly unforgiving. If you develop a health condition after that window closes, you could face higher premiums or outright denial for supplemental coverage. Even if you're healthy today and leaning toward an Advantage plan, it's worth understanding what you're giving up by letting this window pass. If you're exploring supplement options, know that Plan G isn't always the best choice and that Plan N or high-deductible alternatives might fit your situation better.

Turning 65 While Still Working? The Rule Has a Catch

Plenty of seniors assume they can simply delay Medicare while they're still employed. The reality is more nuanced, and the details matter more than most people realize.

If a senior is turning 65 but still working, should they enroll in Medicare or delay it?

This depends on their situation:1. The rule from Medicare is that if 20 or more employees are enrolled in the group health plan of the employer, the senior can delay taking Medicare Part B without being later penalized. Notice I said 20 employees on the group health plan, not just 20 employees!

2. Compare Medicare premium to the group health premium and compare the co-pays and max out-of-pocket.

3. Does the senior have a younger wife on his group health plan, and if so, does she have an option on her employee plan, if she is still working.

The key variable is employer size. If you work for a company with 20 or more employees and have creditable coverage, you generally can delay Medicare without penalty. If your employer has fewer than 20 employees, Medicare typically becomes primary and you need to enroll at 65 to avoid gaps. Getting this wrong can mean late enrollment penalties that follow you permanently, or a stretch without adequate coverage.

Why County-Level Knowledge Matters in Florida

Florida doesn't have one Medicare market. It has dozens. There are over 600 Medicare Advantage plans available statewide, but what's actually offered in your county depends on where you live. Miami-Dade has more than 40 MA plan options. Monroe County (the Keys) has a fraction of that. A plan with strong hospital coverage in one county might not include the same providers two counties over.

When we asked agents about the benefits of working with a local agent versus going remote, the answers went beyond convenience.

What benefits are there to working with a Medicare Agent near me vs remote/virtual?

Working with a local agent allows you to build a relationship with that agent/broker who will have your best interests in mind. Sitting down with an agent allows you to see the plans in your area and make sure your doctors and hospitals are in your network. Agents in a "call center" do not meet you and do not know the plans in your area as well as your own agent in your area. I would love to be your local agent if you are in my area of SW Florida. Kim HumphriesA broker in your area knows which networks include your doctors, which plans have been reliable at local hospitals, and which carriers have a history of rate stability in your region. That kind of county-level knowledge is nearly impossible to get from a national call center or a TV commercial. If you split time between Florida and another state, the snowbird Medicare guide is also worth a read.

Frequently Asked Questions About Choosing a Medicare Plan in Florida

How do I choose the right Medicare plan in Florida?

Start by listing your current doctors, prescriptions, and any upcoming procedures. Florida Medicare plans vary by county, so a plan that works in Broward may not cover the same providers in Hillsborough. Compare both Medicare Advantage and Original Medicare with Medigap using your specific health needs and budget, not a neighbor's recommendation. Working with a local Florida Medicare broker is the most reliable way to match your needs to what's actually available in your area.

What is the difference between Medicare Advantage and Medigap in Florida?

Medicare Advantage replaces Original Medicare with a private plan that typically bundles medical, drug, and sometimes dental or vision coverage, often with a $0 monthly premium but with copays and network restrictions at the point of care. Medigap (Medicare Supplement) works alongside Original Medicare to cover costs like the 20% coinsurance, giving you broader provider access and more predictable expenses in exchange for a monthly premium. In Florida, where provider networks shift frequently between counties, this distinction matters more than in most states.

Can I change my Medicare plan if I pick the wrong one?

You can switch Medicare Advantage plans during the Annual Enrollment Period (October 15 through December 7) or the Medicare Advantage Open Enrollment Period (January 1 through March 31). However, switching from Medicare Advantage to Original Medicare with Medigap is harder. Once your initial Medigap open enrollment window closes, insurers in most states, including Florida, can require medical underwriting, which means you could be denied or charged more based on health conditions. That's why the initial enrollment decision carries so much weight.

Can I switch from a Medicare Advantage plan to a Supplemental/Medigap plan during the Annual Enrollment Period without answering health questions?

Usually not. During AEP (Oct 15–Dec 7), you can leave Medicare Advantage and return to Original Medicare — but Medigap plans may require health questions unless you qualify for a guaranteed issue right.You may skip health questions if you’re in your Medigap Open Enrollment or using a trial right (first 12 months on MA).

Are Medicare brokers in Florida free to use?

Yes. Licensed Medicare brokers are paid commissions by the insurance companies, not by you. Their services cost nothing out of pocket. A broker can compare plans across multiple carriers based on your county of residence and coverage needs. Unlike a captive agent who represents a single insurer, an independent broker can show you options from several companies.

When should I start planning for Medicare in Florida?

At least three to six months before you turn 65. Your Initial Enrollment Period begins three months before your 65th birthday month and ends three months after. During this time, you also have guaranteed access to Medigap plans without medical underwriting. Waiting too long can mean missed enrollment windows, late penalties, or losing access to supplemental coverage options. If you're still working at 65, the rules around employer coverage and Medicare add another layer of timing that's worth sorting out early.

What to Do Next

Every broker we heard from agreed on one thing: don't go it alone. Whether you're turning 65 and brand new to Medicare or re-evaluating a plan you've had for years, a conversation with a licensed broker costs nothing and can save you from the kind of mistakes that follow you for life. If you're approaching 65 in the Sunshine State, our guide on what Floridians specifically need to know about Medicare at 65 covers the state-specific details that matter most.

Medicare Agents Hub lists over 6,000 licensed Medicare brokers across Florida who can review your county-specific plan options, coverage needs, and long-term goals. The brokers quoted throughout this article are real professionals listed in our directory, and many of them are available to help you today.

Find a licensed Florida Medicare broker near you and start the conversation before your next enrollment window opens.