Snowbirds Beware: How Medicare Works When You Live in Two States

-

September 30, 2025

For many retirees, the snowbird lifestyle is the dream. Winters in Florida or Arizona, summers in New York, Michigan, or any other northern state, it’s the best of both worlds. While splitting time between two homes may sound simple, healthcare coverage can get complicated. Medicare doesn’t always follow you the way you might expect, and the plan you choose can make all the difference in avoiding unexpected bills.

Whether you’re a snowbird yourself or helping a parent manage their Medicare coverage, here’s what you need to know about how Medicare works when you live in two states.

Key Takeaways

- Original Medicare (Parts A and B) is accepted nationwide by any provider who takes Medicare.

- Most Medicare Advantage plans have regional networks, so out-of-state care is often limited to emergencies.

- Medigap plans travel with you across state lines, but eligibility is tied to your permanent residence.

- Part D drug plans and premiums can vary by state, so review coverage where you spend most of your time.

- Your permanent residence (the address used for taxes and Social Security) determines plan availability for Medigap, Part D, and Medicare Advantage.

I thought I was covered during my snowbird months in Florida, but apparently not. What kind of plan do I actually need for that?

This is a very common surprise for snowbirds. If you split time between states, you generally need a plan with nationwide provider access, such as Original Medicare with a Medigap plan, which allows you to see any Medicare-accepting doctor in the U.S. Many Medicare Advantage plans use local or regional networks, so routine care may not be covered when you’re out of state. Some PPO Advantage plans offer limited out-of-network coverage, but it’s often not ideal for long stays. For true flexibility across states, Original Medicare with a supplement is usually the best fit.Original Medicare: Nationwide Acceptance

Original Medicare (Parts A and B) is the most flexible option for people who live in more than one state. With Original Medicare, you can see any provider nationwide who accepts Medicare, and that’s the majority of doctors and hospitals. There are no restrictive provider networks and no need to switch plans when you change your location seasonally.

This nationwide acceptance makes Original Medicare ideal for snowbirds. If you’re in Florida during the winter and need to see a doctor, you’re covered. When you head back north in the summer, you can see a doctor there as well.

However, Original Medicare doesn’t cover everything. Beneficiaries typically add:

-

Part D prescription drug coverage, which can vary depending on where you live.

-

Medigap (supplemental) insurance, which helps pay for deductibles, coinsurance, and out-of-pocket costs.

With Original Medicare plus Medigap, snowbirds can enjoy the freedom to receive care almost anywhere in the country without worrying about network restrictions.

Medicare Advantage: Location Matters

Medicare Advantage (Part C) plans can be a great choice for some retirees, but they can pose challenges for snowbirds. Unlike Original Medicare, Medicare Advantage plans usually have geographic restrictions.

-

Networks are region-based. Most Advantage plans operate in a specific service area. For example, a Florida HMO may not have in-network providers in Michigan.

-

Emergency care is always covered, but routine or specialty care outside your plan’s network may not be.

-

Costs can vary. Out-of-network care often comes with higher copays or may not be covered at all.

For snowbirds, this means you could face limited provider choices for part of the year. While a PPO Advantage plan may offer some out-of-network flexibility, it still won’t provide the same nationwide access as Original Medicare.

One important point that catches snowbirds off guard: you can only be enrolled in one Medicare Advantage plan at a time. You can’t hold a Florida Advantage plan for winter and a Michigan Advantage plan for summer. Your plan is tied to your permanent residence, and switching plans generally has to happen during the Annual Enrollment Period (Oct 15–Dec 7) or the Medicare Advantage Open Enrollment Period (Jan 1–Mar 31), not simply when you cross state lines.

If you’re committed to Medicare Advantage, it’s important to talk with a broker about whether your plan’s network extends to both states or if switching plans seasonally is an option.

Medigap: Added Flexibility for Snowbirds

Medigap policies are supplemental plans that work alongside Original Medicare. They cover expenses like coinsurance, deductibles, and copayments, giving beneficiaries more predictable out-of-pocket costs.

For snowbirds, Medigap is often the most flexible choice because it pairs with Original Medicare’s nationwide acceptance. With Medigap, you won’t need to worry about whether a provider is in-network. If they take Medicare, they’ll accept your Medigap coverage as well.

One thing to note: Medigap premiums can vary by state, and your permanent residence (where you officially live and pay taxes) determines your eligibility. If you move permanently from one state to another, you may have the chance to change Medigap plans.

Key Questions Snowbirds Should Ask a Medicare Agent

Before committing to a plan, snowbirds should sit down with a Medicare agent or broker and ask questions like:

-

“Will my plan cover me in both of my home states?”

-

“If I need to see a specialist during the winter, will that be in-network?”

-

“Would I be better off with Original Medicare plus Medigap rather than Medicare Advantage?”

-

“How do Part D prescription drug plans differ depending on where I spend most of my time?”

Asking these questions up front helps avoid unpleasant surprises later, like discovering your doctor in one state isn’t covered by your plan.

Snowbird Scenarios: How It Plays Out in Real Life

-

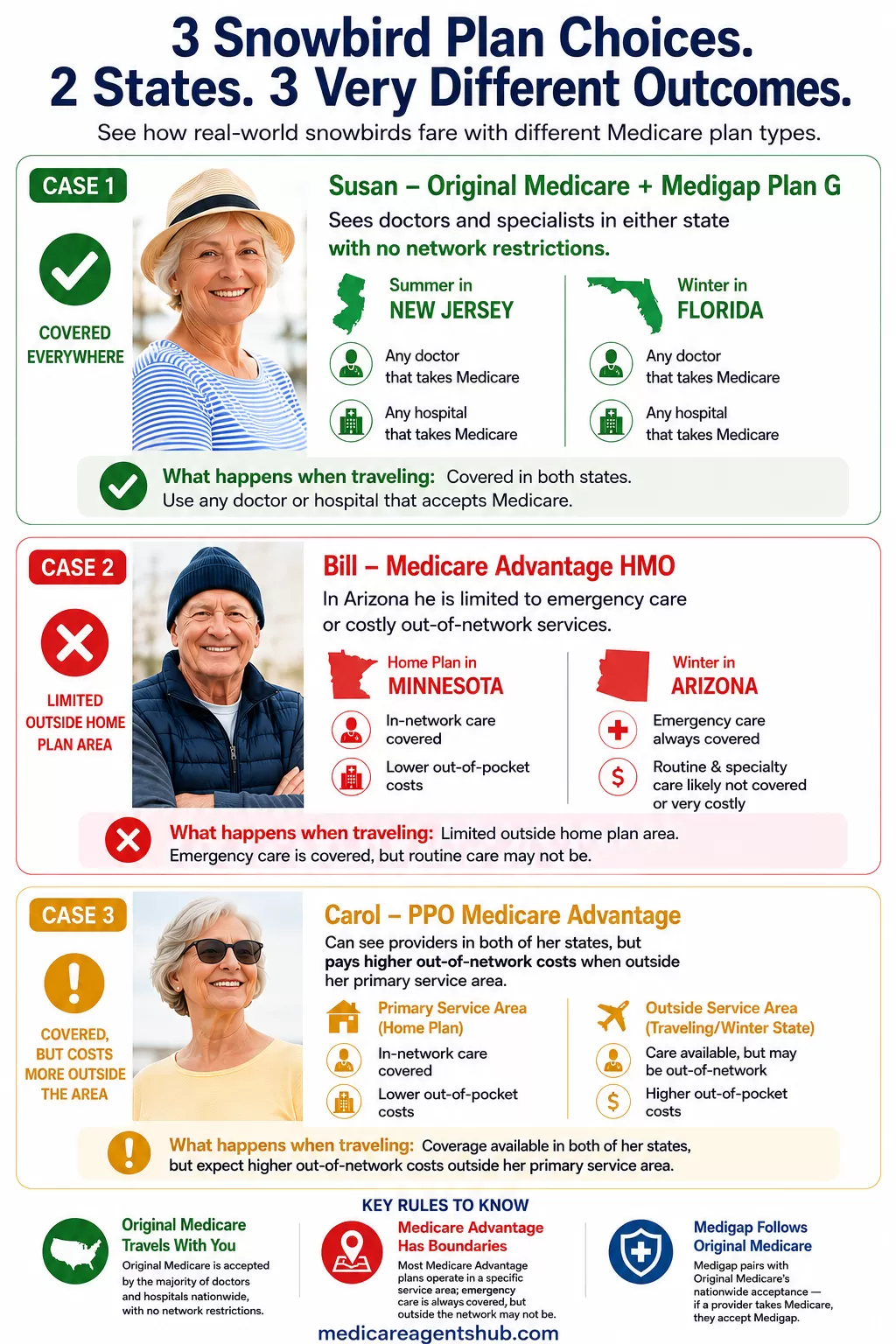

Case 1: Original Medicare + Medigap

Susan lives in New Jersey during the summer and Florida during the winter. She has Original Medicare and a Medigap Plan G policy. No matter which state she’s in, she can see doctors and specialists without worrying about network restrictions. -

Case 2: Medicare Advantage HMO

Bill splits his time between Minnesota and Arizona. His Advantage plan is based in Minnesota, which means when he’s in Arizona, his options are limited to emergency care or costly out-of-network services. -

Case 3: PPO Advantage with Out-of-Network Coverage

Carol has a PPO Advantage plan that allows out-of-network care but at higher costs. While she can see providers in both of her states, she pays more when outside her primary service area.

These scenarios show why plan choice is so important for retirees who maintain two homes.

Choosing the Best Medicare Plan for Snowbirds

The snowbird lifestyle comes with many perks, but Medicare coverage shouldn’t be left to chance. While Original Medicare plus Medigap generally offers the most flexibility for living in two states, every retiree’s situation is different. Medicare Advantage can work for some, but only if its network fits your travel lifestyle.

And splitting time between two states is just one scenario — retirees who spend part of the year abroad or are considering moving to a U.S. territory face even more unusual Medicare challenges that go beyond standard network questions.

Before you make a decision, talk to a Medicare agent who understands the snowbird lifestyle. The right plan can help ensure that wherever you spend your time (north, south, or somewhere in between) you’ll have the coverage you need without unexpected headaches.