Can Veterans Skip Medicare Part B? The VA, TRICARE and Medicare Advantage Debate

-

July 10, 2026

Ask ten licensed Medicare agents how a veteran should handle Medicare at 65 and you will get answers that openly contradict each other. Some tell 100% service-connected vets to skip Part B entirely. Others say Part B is non-negotiable, no matter the disability rating. A third group recommends a zero-premium Medicare Advantage plan on top of VA care. The disagreement reflects different experiences and risk tolerances, but not every recommendation carries the same protections or rests on a complete reading of the federal rules. The right move depends on which VA benefit you carry, whether TRICARE for Life is in the picture, and how comfortable you are relying on a single system for all future care needs.

Reviewed for accuracy: July 2026. This article was reviewed against current guidance from Medicare.gov, the U.S. Department of Veterans Affairs, and TRICARE. Agent quotations represent individual professional perspectives and should not be treated as official government determinations.

| Veteran's Coverage | General Part B Rule |

|---|---|

| VA health care only | Part B is optional, but VA encourages eligible veterans to enroll for non-VA access and penalty protection |

| TRICARE for Life | Parts A and B are generally required to retain TRICARE coverage |

| Medicare Advantage | Parts A and B are required; plan costs, networks, and benefits vary |

Bottom line: Veterans using VA health care alone are not legally required to enroll in Part B, but delaying it can limit access to civilian outpatient care and create a lifetime penalty. Most Medicare-eligible TRICARE for Life and CHAMPVA beneficiaries generally need both Parts A and B. Medicare Advantage is optional and should be evaluated based on provider access, cost sharing, prior authorization, and benefits, not simply its $0 premium or extras.

The Core Confusion: VA Care Is Not Insurance

The reason agents disagree so often comes down to one technicality almost every veteran misses until it matters. VA health care is a system of care, not a portable insurance policy. VA health care generally covers care delivered by VA or specifically authorized through VA community care. Qualifying emergency treatment at a non-VA emergency department may also be covered, but only when VA's notification and eligibility requirements are met. Outside those scenarios, the VA does not pay, and that is when Medicare matters. That is also where the agent-to-agent disagreements start.

This is also why the existing overview of Medicare and VA benefits on this site recommends carrying both whenever possible. The framework here builds on that baseline by laying out exactly where licensed agents split, and why.

Debate #1: The 100% Service-Connected Vet Who Skips Part B

This is the most heated split in the agent community. A veteran with a 100% service-connected disability rating qualifies for VA Priority Group 1 and generally does not pay VA copays for care, tests, or medications. Some agents argue these veterans can safely skip Medicare Part B and its monthly premium because the VA may cover non-VA emergency care when notified within 72 hours of the start of treatment, though notification alone does not guarantee payment. The veteran and the emergency care must also meet VA eligibility and coverage requirements, including that a VA or federal facility was not feasibly available and that a reasonable person would have believed delaying treatment could be dangerous.

Other agents flatly refuse to recommend that path. Their reasoning is simple: the 72-hour notification is a paperwork trap that families forget in a real medical crisis, VA may deny payment when the situation does not satisfy the prudent-layperson emergency standard, when a VA or other federal facility was feasibly available, or when another eligibility or claims requirement was not met, and VA networks tighten and loosen on their own schedule. If the veteran gets sicker later and needs Part B to add a Medigap plan or shop a Medicare Advantage plan, the late-enrollment penalty applies for as long as the veteran has Part B.

Good afternoon. I am a Veteran as well, and depending on your level of disability or VA rating, this can work well for someone going onto Medicare. For example, someone who is 100% disabled does not always start their Part B of Medicare. This is because, as long as the VA is notified within the 72-hour window after admission to the hospital, the VA will cover the bill. However, all other services (medically) can be provided through the VA at no cost with this level of disability. If someone does not want to use the VA, they can enroll in Part B of Medicare and get an additional plan to cover the expenses left behind.

For those on employer plans, I usually sit down with folks to compare the summary of benefits and costs and see which is more beneficial to the consumer. However, to try to explain the differences on here, can be difficult since employee plans can vary so drastically.

Editor's note: Notifying VA within 72 hours is a requirement, but it does not guarantee payment. The veteran and the care must also meet additional VA eligibility criteria.

Notice the conditional language even from agents who say the skip-Part-B move can work. "As long as the VA is notified within the 72-hour window." "If someone does not want to use the VA." These are not casual edge cases. They are the exact moments when families assume Medicare is in place and learn the hard way that nobody enrolled.

Debate #2: TRICARE for Life Is the One VA-Adjacent Benefit That Requires Part B

Here the disagreement disappears, which is its own kind of warning sign. Agents who specialize in military families are unanimous: Most TRICARE-eligible retirees who qualify for premium-free Part A must have both Medicare Parts A and B to retain TRICARE coverage at 65. Limited exceptions apply, including certain beneficiaries with an active-duty sponsor. Medicare becomes the primary payer for civilian care, and TRICARE for Life slides in as the secondary, picking up most of what Medicare leaves on the table. Skip Part B and TRICARE for Life essentially stops paying for civilian care altogether.

That is a different universe from the 100% service-connected debate above. TRICARE for Life is a retiree benefit for TRICARE-eligible retirees and their family members. It is not the same as VA health care, and the rules do not transfer between them. The mistake agents see most often is a retired veteran assuming TRICARE for Life works like the regular VA system and putting off Part B to save the premium.

I am Retired Military and have Tri-Care. When I turn 65, I must enroll into Medicare Parts A & B. Medicare will be Primary and TriCare For Life will be secondary. I am also 100% Service-Connected Disabled through the VA. I will also need Medicare Parts A & B for providers and care outside of the VA and VA Network. The VA Network is no different than any other networks (Optum, Humana, Anthem, etc) in that it changes Network Providers from time to time and the patient has no control over the network care restrictions. If a Veteran gets all of their prescriptions from the VA or TriCare For Life, Medicare exempts them from enrolling into Medicare Part D. If a case ever arose requiring the Veteran to enroll in Medicare Part D, they will be required to fill out paperwork from Medicare which will exclude them from paying a Medicare Part D Late Enrollment Penalty.

When a retiree 65 or over leaves their company, the vast majority of the time they will have no employer health coverage exclusive of Medicare Parts A & B. Therefore, the retiree must enroll into Parts A, B, & C (Medicare Advantage with Drug Coverage) or A,B, & D with a Medicare Supplement.

This may sound convoluted and confusing, but is better accomplished when talking to an agent face to face who has a clear understanding of the VA and Tricare systems and their respective relationships to Medicare (based on current guidelines)

Editor's note: Original Medicare Parts A and B can be used without Medicare Advantage, Part D, or Medigap. Those additional coverage choices are optional and depend on the individual's other benefits, prescriptions, costs, and preferences.

There is a useful side benefit buried in that answer worth pulling out. A veteran with continuous VA or TRICARE prescription coverage can generally delay Part D without a late-enrollment penalty because that coverage is considered creditable. If the coverage ends, the veteran should enroll promptly and avoid going 63 consecutive days without Part D or other creditable prescription coverage. When the veteran later joins a Medicare drug plan, the plan may request documentation of the earlier creditable coverage.

What About CHAMPVA?

CHAMPVA is a separate benefit primarily for eligible spouses, surviving spouses, children, and certain caregivers. It is not the veteran's personal VA health care benefit. When a CHAMPVA beneficiary becomes eligible for Medicare, Medicare Parts A and B are generally required to obtain or retain CHAMPVA coverage. Veterans and family members sometimes confuse CHAMPVA with TRICARE for Life or VA health care, but the eligibility rules and Medicare coordination are different for each program.

Debate #3: Should a Veteran Stack a Zero-Premium Medicare Advantage Plan on Top of VA Care?

This is the point at which plan benefits and sales incentives require the closest scrutiny, and where consumers should read most carefully. A specific subset of Medicare Advantage plans are designed around veterans. Some of these plans exclude Part D drug coverage for veterans who use the VA pharmacy and may offer supplemental benefits such as dental, vision, hearing aid allowances, OTC allowances, or a Part B premium reduction that may lower some or all of the standard $202.90 monthly Part B premium in 2026, depending on the plan. Availability, benefit amounts, provider networks, and cost sharing vary by plan and location.

Typically, Veterans take the route of a ZERO PREMIUM Medicare Advantage Plan to co-exist with the services offered at the VA. These don't carry part D (prescription drugs) because they receive those from the VA, thus carry Great beefits such as a part B buyback, dental, vision, hearin, or just a 2nd opinion...

Employer plans need to be evaluated on a cost basis compared to a MEDicare Plan..

On paper, that is hard to argue with. A zero-premium Advantage plan with a Part B premium reduction, dental benefits, and the option to see a civilian doctor for a second opinion looks like an easy decision. But not every agent agrees the stack is worth it for every veteran.

If you have VA coverage you have many great options.

You can have Part A only and VA benefits. That is something to consider when the VA covers all your medical expenses.

You can have Part A Hospital and Part B Medical and VA coverage. If you chose this option, you are eligible for a Medicare Advantage plan that provides extra benefits that Medicare or the VA doesn't offer.

If you would like to further discuss your options I am here to help

The honest tension is that Medicare Advantage often exchanges Original Medicare's broader provider access for a plan network, plan-specific cost sharing, and prior-authorization requirements. A veteran who uses the VA for everything except dental and OTC items may never feel the network restrictions. A veteran who develops cancer and wants a top oncology center outside the VA might feel them immediately. The same caution applies that agents raise about zero-premium Advantage plans generally: the headline number is not the cost, the network is.

VA benefits will always be there for our military retires. I recommend a Medicare advantage plan to go with VA Benefits. I have helped many military retires and those just using the VA. To combine with a Medicare advantage plan.. By doing that you have other options for healthcare and do not have to wait for an opening to go tho the VA.

Editor's note: VA eligibility and available services depend on federal rules, the veteran's eligibility category, and the circumstances of the care.

Debate #4: The Part B Late-Enrollment Trap That Catches Older Vets

Agents see this pattern often enough that several mentioned it without being asked. A veteran in their 60s decides VA care is enough, skips Part B at 65, and uses the VA exclusively for ten or twelve years. Then something changes. The VA wait time for a specialty appointment stretches to six months. The veteran needs repeated outpatient treatment, rehabilitation, or specialist care outside the VA system. A son or daughter pushes for a second opinion at a private hospital that does not take VA referrals. The veteran calls an agent asking about a Medigap plan or an Advantage plan and learns two uncomfortable things in the same call.

First, the Part B late-enrollment penalty is permanent. It is 10% of the standard premium for every full 12 months the veteran could have had Part B but did not. Twelve years of delay means a 120% lifetime surcharge on top of whatever Part B costs that year. Second, enrolling in Part B outside the Initial Enrollment Period generally means waiting until the next General Enrollment Period (January through March), with coverage beginning the month after enrollment. The wait itself can leave the veteran without Medicare coverage for months. If the veteran is enrolling in Part B for the first time at age 65 or older, that enrollment generally triggers a new six-month federal Medigap Open Enrollment Period. During that window, the veteran can typically purchase any Medigap policy sold in their state without medical underwriting. The Part B penalty still applies, and the veteran may face a coverage gap while waiting to enroll, but federal Medigap Open Enrollment protections are not necessarily lost just because Part B was delayed.

The TRICARE for Life answer above quietly references this when it explains the Part D paperwork requirement. VA and TRICARE prescription drug benefits generally count as creditable drug coverage, which protects against the Part D penalty, but that protection does not extend to the Part B penalty. There is no equivalent protection from the Part B penalty for veterans who delayed Part B without qualifying group health coverage based on their own or their spouse's current employment.

Medicare can work alongside other insurance, but who pays first (primary) and who pays second (secondary) depends on which type of coverage you have and why you have it.

1. Employer or Union Group Health Plans

If you’re 65+ and still working (or covered by a working spouse’s plan):

Employer has 20+ employees: Employer plan pays first, Medicare pays second.

Employer has fewer than 20 employees: Medicare pays first, employer plan pays second.

Tip: Always confirm with HR whether your coverage is considered creditable for delaying Part B or Part D without penalty.

2. Retiree Coverage

Usually pays after Medicare.

You must enroll in Medicare Parts A & B for retiree coverage to work fully.

Retiree coverage may help pay Medicare’s deductibles and coinsurance, but benefits can change — especially if your former employer changes the plan.

3. Veterans Affairs (VA) Benefits

VA benefits cover care only in VA facilities.

Medicare covers care in non-VA facilities.

You can have both:

Use VA for prescriptions or specialty care.

Use Medicare for civilian doctors/hospitals.

Tip: Many vets keep Part B to avoid penalties and to have access to non-VA care.

4. TRICARE for Life (Military Retirees & Spouses)

You must have Medicare Parts A & B.

Medicare pays first for Medicare-covered services.

TRICARE pays second, often covering what Medicare doesn’t (including some drugs).

For VA or military facilities, TRICARE pays first.

5. Medicaid

Medicaid is always the payer of last resort — it pays after Medicare and any other insurance.

If you have both Medicare and Medicaid (“dual eligible”), you may qualify for a Special Needs Plan (D-SNP) that coordinates both.

6. Workers’ Compensation

Workers’ comp pays first for job-related injuries or illness.

Medicare may pay for unrelated services.

Editor's note: Billing at VA facilities follows different rules from billing at military hospitals. Medicare generally cannot pay a VA facility. Veterans using TRICARE for Life for non-service-connected care at a VA facility may face substantial out-of-pocket costs and should confirm coverage before receiving care.

What Agents Seem To Agree On

Underneath the visible disagreement, four points show up in nearly every answer:

- VA care does not coordinate with Medicare the way employer coverage does. Nobody is filing a claim with both. The veteran chooses which system to use at each point of care, and the two systems run on separate billing tracks.

- Part A is almost always free for veterans with 40 quarters of Medicare-taxed work history. Most veterans who qualify for premium-free Part A enroll when first eligible. One important exception involves veterans still contributing to a Health Savings Account, since Medicare enrollment can affect HSA eligibility and Part A may be retroactive. Veterans who must pay a Part A premium should also compare the cost and enrollment rules carefully. Premium-free Part A can provide valuable hospital coverage when a veteran receives Medicare-covered care outside the VA system. VA and Medicare generally do not pay the same claim as traditional primary and secondary insurers, so the veteran should confirm which benefit is being used for each episode of care.

- The decision is local and state-specific. A veteran in a rural state with one VA hospital two hours away makes a different math decision than a veteran in a metro area with multiple VA facilities. Agents who serve veterans in Texas, Florida, and California see this play out differently from agents in lower-density states.

- The wrong move at 65 is harder to undo than the wrong move at 70. Initial Enrollment Period decisions lock in penalties that follow the veteran for decades.

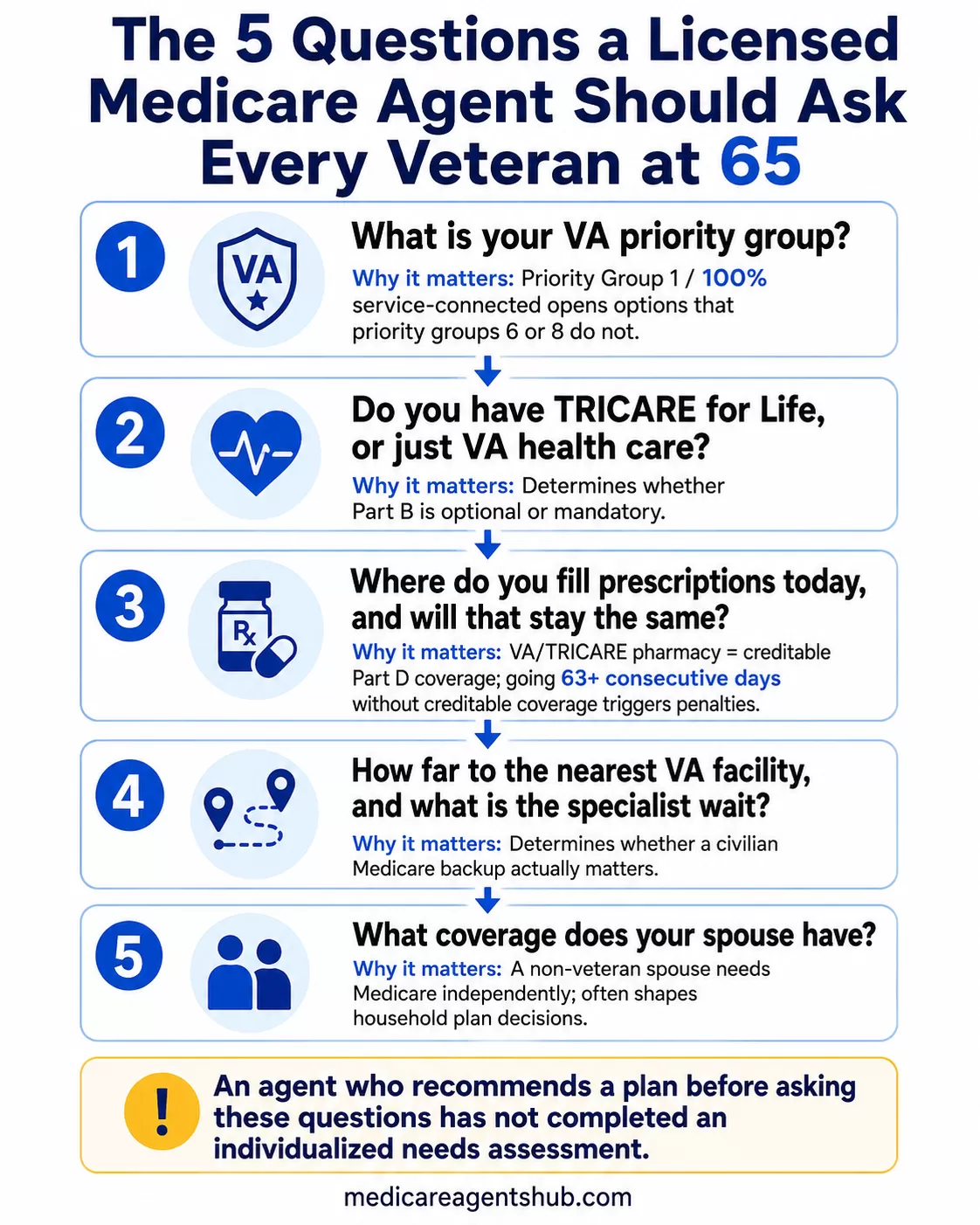

The Practical Decision Framework Agents Actually Use

When licensed agents sit down with a veteran, the conversation tends to follow a predictable sequence. The order matters because each answer changes which Medicare path makes sense.

- What is your VA priority group? Priority group 1 (100% service-connected) opens options that priority group 6 or 8 does not. Priority groups can also be reassigned over time, which means a comfortable strategy today can shift if income or disability status changes.

- Do you have TRICARE for Life, or just VA health care? The answer determines whether Part B is optional or mandatory.

- Where do you fill prescriptions today, and do you expect that to stay the same? A veteran fully reliant on the VA pharmacy can take advantage of the Part D late-enrollment exception. A veteran who might want commercial pharmacies later should think carefully before skipping Part D. VA and TRICARE prescription benefits generally count as creditable drug coverage for Part D purposes. The rules for delaying Part B without penalty are different and generally require qualifying group health coverage based on current employment.

- How far are you from the nearest VA facility, and what is the wait for a specialist? This determines whether a civilian backup through Medicare actually matters.

- What does your spouse have? A non-veteran spouse needs Medicare independently, which often shapes which Advantage or Medigap plan makes sense as a household decision.

This is also where a veteran-specific Advantage plan or a Medigap plan paired with original Medicare gets compared on real numbers rather than headline premiums. Agents who walk through the comparison openly will surface the trade-offs honestly. An agent who recommends a plan before asking these questions may not have completed a sufficiently individualized needs assessment.

Frequently Asked Questions

Do veterans need Medicare Part B if they use VA health care?

Part B is not legally required, but VA itself encourages eligible veterans to enroll. Without Part B, Medicare generally will not cover doctors, outpatient treatment, medical equipment, or other Part B services received outside the VA system. If the veteran has Part A, Medicare may still cover qualifying inpatient hospital care. Delaying Part B enrollment triggers a permanent late-enrollment penalty. Most agents recommend enrolling at 65 to keep options open.

Does a 100% VA disability rating make Part B unnecessary?

A 100% service-connected rating qualifies the veteran for comprehensive VA care at no cost, which leads some agents to say Part B can be skipped. However, VA emergency coverage at non-VA facilities requires meeting specific eligibility and notification rules, and the late-enrollment penalty applies if the veteran changes course later. The rating does not exempt the veteran from Part B penalties.

Do I need Part B to keep TRICARE for Life?

In most cases, yes. TRICARE-eligible retirees who qualify for premium-free Part A generally must enroll in both Parts A and B at 65 to retain TRICARE for Life coverage. Without Part B, TRICARE for Life will not pay for civilian care. Limited exceptions exist, such as certain beneficiaries with an active-duty sponsor.

Can a veteran have VA benefits and Medicare Advantage?

Yes. A veteran can enroll in a Medicare Advantage plan while continuing to use VA care. Some plans are specifically designed for veterans, offering supplemental benefits like dental and vision while excluding Part D drug coverage. The veteran must have both Parts A and B to enroll, and plan costs, networks, and benefits vary by location.

Does VA prescription coverage count as creditable Part D coverage?

Yes. VA and TRICARE prescription drug benefits generally count as creditable coverage for Medicare Part D purposes. A veteran can usually delay Part D without a penalty as long as that coverage continues and the veteran does not go 63 consecutive days without Part D or other creditable prescription coverage. When enrolling later, the drug plan may request documentation of the earlier creditable coverage.

What happens if a veteran delays Part B?

The Part B late-enrollment penalty is 10% of the standard premium for every full 12-month period the veteran was eligible but not enrolled. The penalty is generally added to the monthly premium for as long as the person has Part B. When a veteran does enroll late, the enrollment generally triggers a new Medigap Open Enrollment Period, preserving federal Medigap Open Enrollment protections, but the penalty itself cannot be reversed.

Does VA coverage count as creditable coverage for Medicare Part B?

No. VA health care does not generally give someone a Part B Special Enrollment Period or protect them from the Part B late-enrollment penalty. The Part B exception generally requires qualifying group health coverage based on current employment.

Can a 100% disabled veteran opt out of Medicare Part B?

Yes, Part B is optional for a veteran relying solely on VA health care, even with a 100% service-connected rating. However, the veteran may lose access to Medicare-covered outpatient care outside the VA and may face a permanent penalty if enrolling later.

How to Find an Agent Who Actually Understands the VA Side

Not every Medicare agent has worked with enough veteran families to handle the TRICARE for Life rules, the priority group nuances, or the Part D creditable-coverage exception without having to look it up mid-call. When interviewing a potential agent, ask directly how many veteran clients they have helped, whether they have personally worked with TRICARE for Life enrollees, and what their general recommendation is for a 100% service-connected vet at 65. The answer does not have to match what is written here. It does have to be specific, sourced in their own client experience, and free of the words "it depends" without any follow-up explanation.

A veteran can browse and contact licensed agents directly through the directory at Medicare Agents Hub. Many of the agents quoted above answer questions publicly, which makes it easier to read their actual approach before scheduling a call. The goal is not to find the agent with the most polished presentation. It is to find the one who can walk a veteran through the Part B math, the TRICARE rules, and the priority group implications in a single conversation, and back it up with what they have seen with other clients.