Medicare When You Live Abroad: Coverage, Premiums, and Penalties to Watch

-

June 15, 2026

If you're retiring overseas, splitting time between countries, or already living abroad, Medicare gets confusing fast. Coverage outside the U.S. is almost nonexistent, but you can still owe premiums, still face late penalties if you drop coverage, and still need a plan for the day you move back. This guide walks through the actual rules so you can decide what to keep, what to cancel, and what it will cost you later.

The Short Answer: Medicare Stops at the Border

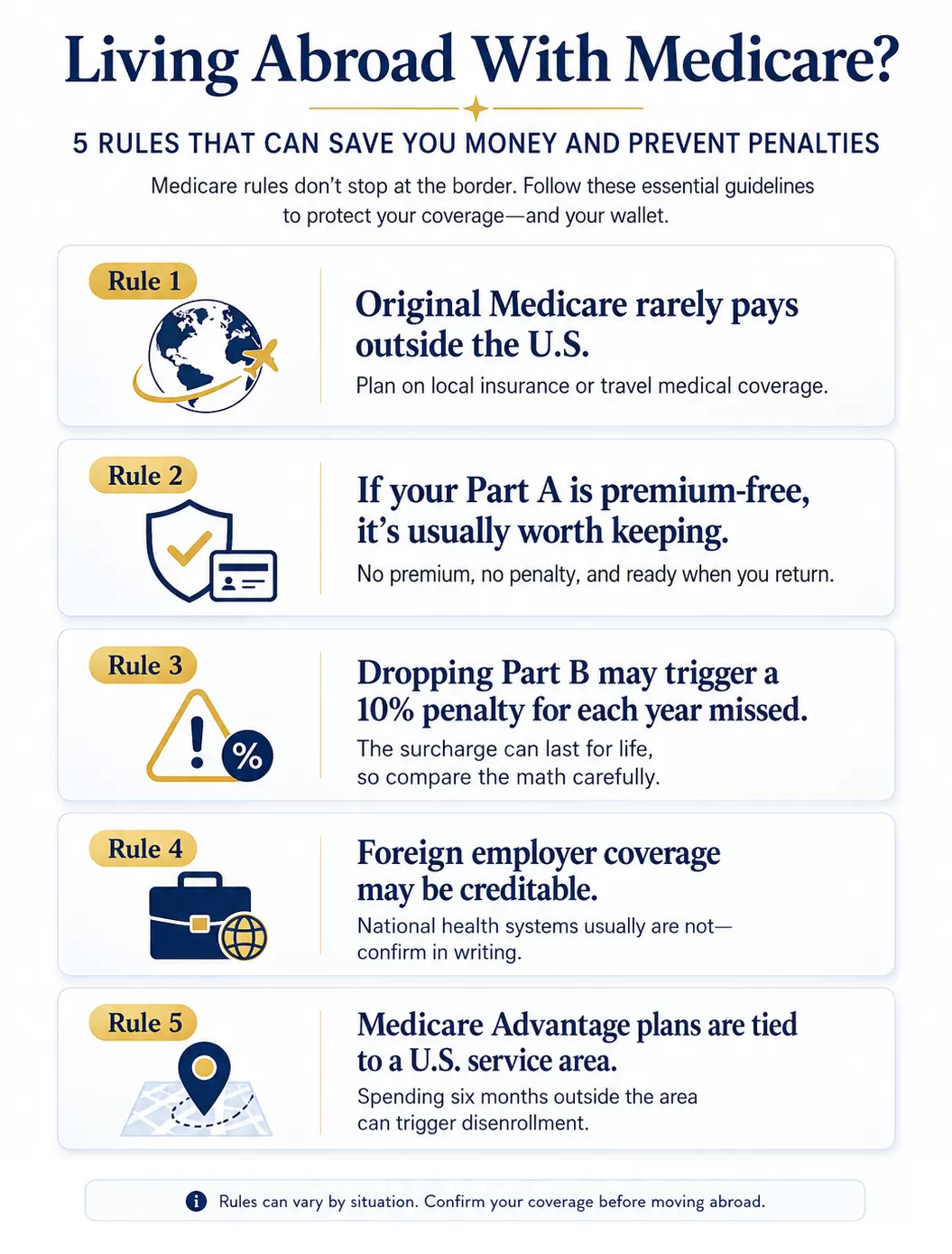

Original Medicare (Part A and Part B) almost never pays for care delivered outside the United States. The exceptions are narrow and mostly involve emergencies near the U.S. border, on a ship within six hours of a U.S. port, or when a foreign hospital is genuinely closer than the nearest U.S. hospital that can treat you.

For day-to-day care in another country, Medicare pays nothing. That's the same reality covered in our overview of Medicare's limits on international claims, and it applies whether you're abroad for two weeks or two decades.

What changes when you live abroad rather than travel is the premium math, the enrollment penalties, and what happens when you come back.

I am a resident in another country outside of America, will I still be covered living abroad?

If you are talking about Medicare - keep in mind that Medicare does not cover outside the USA.If you have a Medicare Supplement - then they will cover up 80% up to a lifetime maximum of $50,000 after you meet a $250 deductible. Also keep in mind - it is really for "emergency" needed care that would be considered a life-threatening emergency. All claims must be in English or at least converted to English before submitting it to your insurance carrier.

Should You Keep Paying for Part B While Living Abroad?

This is the question most expats wrestle with, and the right answer depends on three things: how long you plan to stay, whether you'll have local insurance you trust, and how likely it is you'll return to the U.S.

Part A is usually free if you or your spouse paid Medicare taxes for at least 10 years. Most people keep Part A while abroad because there's no premium to drop. It also stays available the moment you set foot back on U.S. soil.

Part B has a monthly premium (the standard amount changes each year, and higher earners pay more through IRMAA). You're paying for coverage that won't help you in Madrid, Mexico City, or Manila. That makes dropping Part B tempting, but the math has a sharp edge.

The Part B Late Enrollment Penalty

If you drop Part B and later re-enroll, you'll likely pay a 10% premium surcharge for every full 12-month period you went without it, and that surcharge sticks to your premium for life. Someone who drops Part B for five years pays a 50% higher premium for the rest of their time on Medicare.

The same dynamic applies to Part D drug coverage, where the late penalty is 1% of the national base premium per uncovered month. We've documented how this plays out for real beneficiaries in our piece on lifelong Part B and Part D penalties, and the stories are painful.

The Exception That Can Save You

If you're living abroad and remain covered under a group health plan based on your or your spouse's current employment, you may qualify for a Part B Special Enrollment Period when that employment or coverage ends. That's the specific standard Medicare uses for the SEP: current employment-based group health plan coverage. It avoids the penalty entirely.

Do not assume a foreign national health system, retiree coverage, or private local insurance will protect you from Part B penalties. Those generally do not qualify. Coverage through a U.S. employer group plan while working abroad is the clearest path. Get written confirmation from your employer and insurer before dropping Part B, ideally with help from a licensed agent who has handled returning expats. Our guide to qualifying for a Special Enrollment Period walks through the full rules.

Can I cancel or drop Medicare Part B if I move abroad?

Yes, you can drop Medicare Part B if you move abroad, since Medicare generally doesn’t cover care outside the U.S. To do this, you must contact the Social Security Administration and submit a request to disenroll.Keep in mind, if you later return to the U.S. and want Part B again, you may face a late enrollment penalty and have to wait for an appropriate Enrollment Period.

Before dropping Part B, make sure you’ll have adequate health coverage in the country you’re moving to.

What If You Split Time Between Countries?

Snowbirds who winter in Costa Rica or summer in Portugal usually keep both Part A and Part B. You're paying premiums for the months you're in the U.S. anyway, and dropping coverage would expose you to penalties for the privilege of saving a few months of premiums. The smarter move for part-time expats is to keep Medicare intact and buy travel medical insurance for time spent abroad.

Original Medicare paired with a Medigap plan that includes foreign travel emergency coverage (Plans C, D, F, G, M, and N) gives you up to a $50,000 lifetime cap for emergencies in the first 60 days of each trip, after a $250 deductible and 20% coinsurance. This is emergency travel coverage, not full expat health insurance. It handles the worst-case scenarios like a hospital admission or emergency surgery abroad, but it won't cover routine doctor visits, prescriptions, or ongoing treatment in another country. If you spend significant time overseas, you'll still want a separate international health or travel medical policy for day-to-day care.

Medicare Advantage and Living Abroad

Medicare Advantage plans are tied to a U.S. service area. If you move out of your plan's service area for more than six months, you can be disenrolled and dropped back to Original Medicare. This is a genuine problem for retirees who maintain a U.S. address on paper but spend most of the year overseas: keeping a Medicare Advantage plan you can't actually use is wasted money and a compliance risk.

For long stretches abroad, Original Medicare plus a Medigap policy is generally the cleaner setup. The trade-offs are the same ones we cover in our breakdown of Medicare Advantage versus Medigap, just with foreign travel emergency benefits weighing more heavily in the decision.

If I live part of the year abroad, do I still have to pay for Medicare if I don’t use it?

Yes—if you want to keep your Medicare Part B active, you still have to pay the monthly premium even when you’re living abroad and not using the coverage. Medicare generally doesn’t pay for care received outside the U.S., but dropping Part B to save money can backfire because you’ll face a permanent late-enrollment penalty and limited enrollment windows if you ever move back and want it again.Most people who spend part of the year overseas keep their Medicare in place as “insurance for the future,” since re-establishing it later can be costly and difficult.

Coming Back to the U.S.: Re-Enrollment Rules

If you canceled Part B while abroad and now want it back, here's how the timeline works:

- General Enrollment Period: January 1 through March 31 each year. Coverage starts the month after you sign up. This is the default re-enrollment window for anyone without a Special Enrollment Period.

- Special Enrollment Period: If you were covered under a group health plan based on current employment (yours or your spouse's) while abroad, you get an 8-month window to enroll without penalty after that employment or coverage ends.

- Part D: Has its own enrollment windows and its own penalty. You generally need to enroll within 63 days of losing creditable drug coverage to avoid the late fee.

If your return aligns with a change of residence inside the U.S., you'll also want to read our notes on Medicare and moving to a new state, because plan choices and Medigap rules can shift dramatically depending on which state you land in.

Premium Payments From Overseas

If you keep Part B while living abroad, premiums still need to be paid. The two reliable methods:

- Automatic deduction from Social Security: Easiest if you collect Social Security and have the deposits routed to a U.S. bank account. Premiums come out automatically each month.

- Medicare Easy Pay: Authorizes Medicare to pull premiums from a U.S. checking or savings account. You'll need a U.S. account in your name; foreign banks generally can't be used.

Beneficiaries who lose access to a U.S. account sometimes fall behind on premiums without realizing it, and that's a direct path to losing coverage. If you're planning a long stay overseas, keep at least one U.S. account open for this purpose.

How long can I stay abroad without losing my Medicare benefits?

There is no time limit as to how long you can be outside the U.S The bigger issue is Medicare generally does not pay for care outside the U.S, except in very limited situations:A medical emergency in the U.S. but the nearest hospital is across the border (e.g., Canada or Mexico)

You’re traveling between Alaska and another state and need emergency care in Canada

You live in the U.S. and a foreign hospital is closer than the nearest U.S. hospital.

Also If you have Part B, you must keep paying premiums to stay enrolled

If you stop paying, your coverage can be dropped—and restarting later may come with penalties.

Special Situations Worth Flagging

Naturalized Citizens and Green Card Holders

Lawful permanent residents generally need five continuous years of U.S. residence before they can buy into Medicare, even if they've worked and paid into the system. Time spent abroad before hitting the five-year mark can reset the clock. If you're planning extended trips during that window, talk to an agent before you leave.

Federal Retirees and Military Beneficiaries

If you have FEHB, VA, or TRICARE coverage, the calculus changes. TRICARE For Life requires Part B enrollment to function, so dropping Part B abroad can blow up your TRICARE coverage in a way most people don't expect. Federal retirees with FEHB have more flexibility but still need to coordinate carefully.

Spouses Who Stay Behind

If one spouse moves abroad and the other stays in the U.S., decisions about Part B, Medigap, and Medicare Advantage have to be made separately for each person. There's no "household" Medicare; each beneficiary's situation is evaluated on its own.

The Practical Checklist Before You Go

- Decide on Part B. Run the math: monthly premium savings versus the lifetime penalty risk if you return.

- Confirm whether your foreign coverage is creditable. Get it in writing from the insurer or employer.

- Keep a U.S. bank account open for premium payments and Social Security deposits.

- Update your address with Social Security and Medicare so notices reach you.

- Buy travel medical or international expat insurance. This is what actually pays your medical bills overseas.

- If you have Medicare Advantage, understand the six-month service area rule before you leave.

- Talk to a licensed Medicare agent who's worked with returning expats. The penalties are too expensive to guess wrong.

Frequently Asked Questions

Does Medicare cover me if I live abroad?

Almost never. Original Medicare (Part A and Part B) does not pay for routine care outside the United States. The only exceptions involve emergencies near the U.S. border, on certain cruise ships, or when a foreign hospital is the closest facility that can treat you. For day-to-day healthcare abroad, you'll need local insurance or an international health plan.

Should I keep Medicare Part B if I move overseas?

It depends on how long you plan to stay and whether you're likely to return. If you drop Part B and later re-enroll, you'll pay a 10% premium surcharge for every full 12-month period without coverage, and that lasts for life. Unless you have qualifying group health plan coverage through current employment, keeping Part B is usually the safer financial decision.

Can I avoid Part B penalties if I return to the U.S.?

You can avoid the penalty if you were covered under a group health plan based on your or your spouse's current employment while abroad. That qualifies you for a Special Enrollment Period with no penalty when the employment or coverage ends. Foreign national health systems, retiree plans, and private international insurance generally do not count.

Does Medigap cover foreign travel?

Some Medigap plans (C, D, F, G, M, and N) include a foreign travel emergency benefit with up to a 0,000 lifetime cap. This covers emergencies only, not routine care abroad. It applies during the first 60 days of each trip, with a 50 deductible and 20% coinsurance.

Can I keep Medicare Advantage while living abroad?

Medicare Advantage plans are tied to a U.S. service area. If you leave your plan's service area for more than six months, you risk being disenrolled and returned to Original Medicare. For extended stays overseas, Original Medicare with a Medigap supplement is usually the more reliable setup.

The Bottom Line for Expats and Long-Term Travelers

Medicare is built around U.S.-based care, and that fact doesn't change when you cross a border. Keep Part A, think carefully before dropping Part B, document any creditable coverage you have, and plan for re-entry before you ever leave. The mistakes that turn into lifelong penalties almost always come from beneficiaries making decisions without understanding how the re-enrollment math works.

If you're weighing a move or already overseas and trying to figure out what to do, a licensed independent Medicare agent can map your situation against the rules and flag the traps before they cost you. That's free guidance that can save thousands over the next decade.