Medicare Special Enrollment Period (SEP): How to Qualify for Part A, B, C, and D

: How to Qualify for Part A, B, C, and D")

-

Last Updated August 3, 2026

If you missed your initial Medicare enrollment window or the annual Open Enrollment Period, don’t worry, there’s still a way to get covered. Medicare offers Special Enrollment Periods (SEPs), also called Special Election Periods, that let you sign up or make changes to your coverage when certain life events occur. These SEPs help you avoid penalties and ensure you have the right coverage when your circumstances change.

What Is a Special Enrollment Period?

A Special Enrollment Period is a time outside the standard enrollment windows when you can enroll in or change your Medicare coverage due to specific life events. These events might include losing other health coverage, moving to a new area, or other qualifying situations. The timing and duration of your SEP depend on the specific event that qualifies you.

You’ll see the terms Special Enrollment Period and Special Election Period used interchangeably. Medicare uses both, and they refer to the same set of qualifying events, whether you’re looking at Part A, Part B, a Part C (Medicare Advantage) plan, or a Part D drug plan. For the official list of qualifying events, see Medicare.gov’s enrollment guidance.

SEP Timing at a Glance

Different qualifying events give you different windows to act. Here's a quick reference:

| Qualifying Event | SEP Length | Applies To |

|---|---|---|

| Losing employer/union coverage | 8 months | Part A & B |

| Losing employer/union coverage | 2 months | Medicare Advantage & Part D |

| Moving out of plan’s service area | 2 months after the move (or starts the month before if you give advance notice) | Medicare Advantage & Part D |

| Losing creditable drug coverage | 63 days | Part D |

| Medicaid or Extra Help status change | 3 months | Medicare Advantage & Part D |

| FEMA-declared disaster | Varies by declaration | Medicare Advantage & Part D |

| 5-star plan available in your area | Once per year (Dec 8 – Nov 30) | Medicare Advantage & Part D |

| Trial right (first 12 months on Medicare Advantage) | 12 months | Switch back to Original Medicare |

Common Reasons You Might Qualify for an SEP

✅ Part B SEP: Losing Employer or Union Coverage

If you're 65 or older and lose your employer or union health coverage, you have an 8-month SEP to enroll in Medicare Part B without facing a late enrollment penalty. This period starts the month after your employment or coverage ends, whichever comes first.

Am I eligible for a Special Enrollment Period if I lose employer coverage?

Yes, if you lose employer coverage, you qualify for a Medicare Special Enrollment Period (SEP).• For Original Medicare (Part A and/or Part B), you have 8 months from the date your group health plan ends or you stop working — whichever comes first—to enroll without penalty. This only applies if your coverage was through active employment (not COBRA or retiree coverage).

• For Medicare Advantage (Part C) and Part D (prescription drug coverage), the SEP is shorter: you have 2 months from the date your employer coverage ends to sign up.

Key points:

• The 2-month SEP for Part C and Part D starts when your employer coverage ends — not when employment ends.

• Missing this window may mean waiting until the next Annual Enrollment Period and possibly facing late enrollment penalties.

✅ Medicare Advantage & Part D SEP: Moving to a New Area

Relocating can impact your Medicare coverage, especially if you have a Medicare Advantage (Part C) or Part D prescription drug plan. If you move to a location outside your plan's service area, you qualify for an SEP to switch to a plan available in your new area.

An answer from an agent explains…

"When you move out of a service area, whether from one county to another, or a different state, you must change plans if you have a Medicare Advantage (MA) or Prescription drug plan (PDP). The ability to change plans after a move falls under a Special Enrollment Period (SEP)."

It's crucial to notify your plan provider about your move. If you inform them before moving, your SEP begins the month before your move and lasts for two months after. If you notify them after moving, your SEP starts the month you inform them and continues for two months.

✅ Part D SEP: Losing Other Creditable Drug Coverage

If you lose other creditable prescription drug coverage (like from an employer or union), you have a 63-day SEP to enroll in a Medicare Part D plan without penalty.

✅ Changes in Medicaid or Extra Help Eligibility

If you qualify for both Medicare and Medicaid and experience changes in your Medicaid eligibility, you may be eligible for an SEP to adjust your Medicare Advantage or Part D coverage. The same applies if your Extra Help (Low-Income Subsidy) status changes.

✅ 5-Star Plan Special Enrollment Period

If a 5-star Medicare Advantage or Part D plan is available in your area, you can use a one-time SEP to switch into it between December 8 and November 30 of the following year. Star ratings are published by Medicare each fall, so the plans that qualify can change from year to year.

✅ Other Life Events

Several other situations can trigger an SEP. They fall into a few groups:

Coverage loss through no fault of your own

- Your plan’s contract with Medicare ends, or CMS terminates your Medicare Advantage or Part D plan

- The plan misled you about coverage

- You lost coverage through no fault of your own

Emergencies and government-declared events

- You were affected by a FEMA-declared natural disaster or public health emergency

- You were released from incarceration

Eligibility and health status changes

- You have a chronic condition that qualifies you for a Chronic Care Special Needs Plan (C-SNP)

- You qualify for a Dual Eligible Special Needs Plan (D-SNP) because you have both Medicare and Medicaid

Medicare Advantage trial right

- You’re within the first 12 months of trying a Medicare Advantage plan and want to switch back to Original Medicare (the Medicare Advantage “trial right”)

I'm confused about when I can change my Medicare plan. Can you clarify the different enrollment periods for me?

Enrollment periods can be one of the most confusing aspects of Medicare. Below is information on the most common enrollment periods:Initial Election Period - occurs three months before the month of your 65th birthday and continues for three months past the month of your 65th birthday, seven months in total. During this time you can enroll in both Part A and/or B of Original Medicare. You can also enroll in a Medicare Advantage (Part C) plan or a Part D prescription plan.

Annual Election Period - occurs each year starting on October 15 and continues through December 7. During this time you may enroll in, change or cancel a Medicare Advantage or Part D prescription plan

Open Enrollment Period - occurs each year starting on January 1 and continues through March 31. During this time you may make one change to your Medicare Advantage (Part C) coverage only.

Special Election Periods - occur throughout the year and are usually tied to some change in circumstances such as moving, becoming eligible for financial assistance, being diagnosed with certain chronic conditions or losing creditable coverage such as employer-sponsored coverage.

Generally, Medicare enrollment periods do not apply to Medicare Supplements, also known as Medigap policies. If you are interested in purchasing a Medicare Supplement, you do have an open enrollment period during the first 6 months that you are eligible for both Part A & B of Medicare. During this time, you have the right to purchase any Medicare Supplement available to you based on where you live without having to answer health questions.

For more information on enrollment periods, it is always best to consult a local independent licensed insurance agent who can help guide you through the maze of enrollment periods.

How SEPs Can Trigger Medigap Guaranteed Issue Rights

An SEP lets you enroll in or change Medicare Parts B, C, or D. A related but separate protection, guaranteed issue rights, applies to Medigap (Medicare Supplement) policies. When a Special Enrollment Period is triggered by losing other coverage, it can also grant you guaranteed issue rights to buy a Medigap policy without medical underwriting.

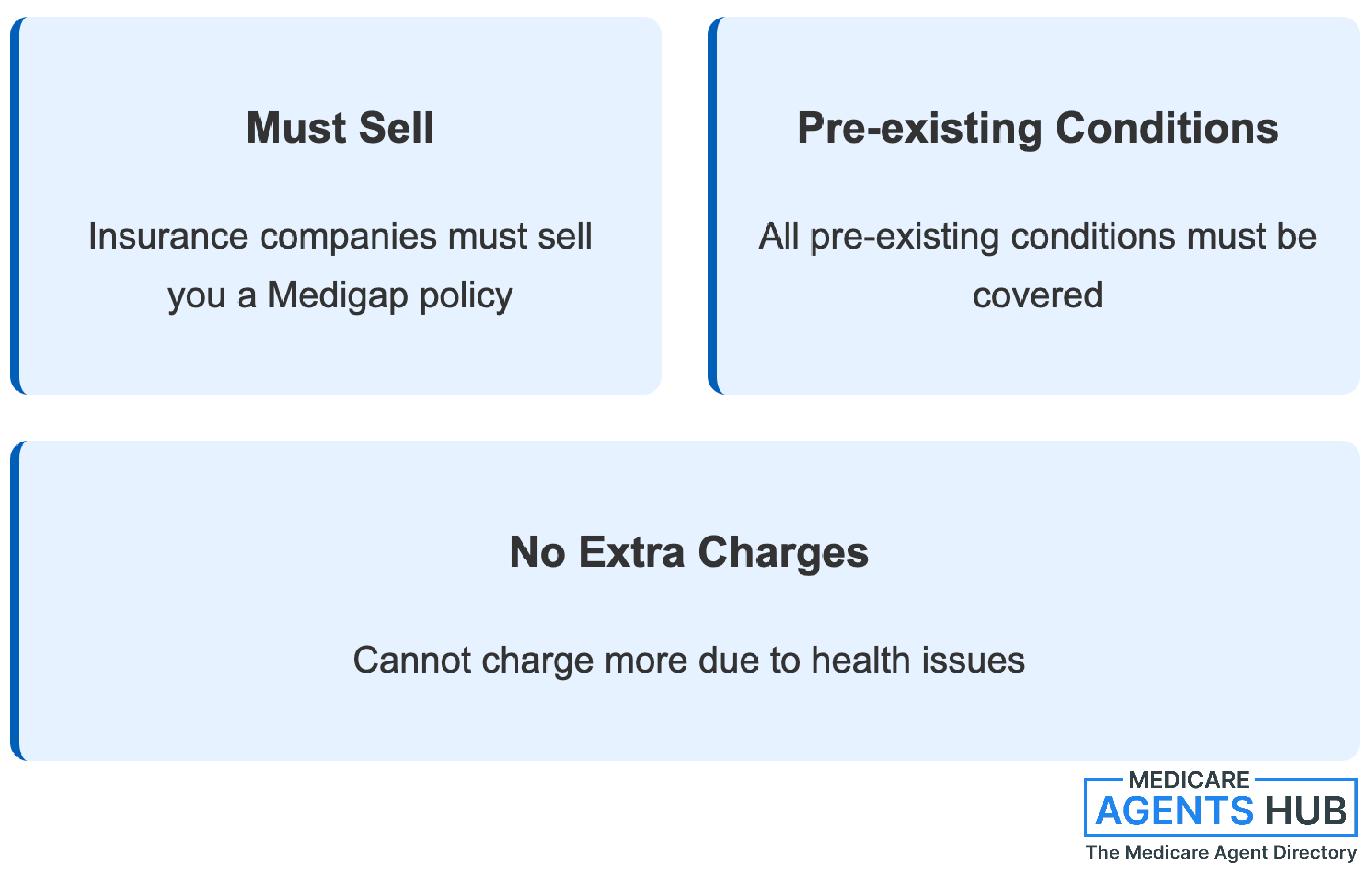

Guaranteed issue rights mean insurance companies must sell you a Medigap policy, cover all your pre-existing conditions, and can't charge you more due to health issues.

While the Medigap Open Enrollment Period is a one-time, six-month window starting when you're 65 and enrolled in Part B, there are situations where guaranteed issue rights apply outside this period. For example, if you lose other health coverage or your Medicare Advantage plan ends, you may have a guaranteed issue right to buy a Medigap policy.

In an answer to a question about Guaranteed Issue John Lopez adds:

"Guaranteed Issue is available for up to 6 months after your Part B becomes effective, and it doesn't have to coincide with the Medicare Open Enrollment Period. There are also other situations in which Guaranteed Issue applies, but consult with a local independent health broker to determine if your situation applies."

Steps to Take If You Qualify for an SEP

-

Identify your qualifying event: Determine the life event that makes you eligible for an SEP.

-

Mark your calendar: Note the start and end dates of your SEP to ensure you act within the allowed timeframe.

-

Review your options: Compare available Medicare plans in your area to find the best fit for your needs.

-

Enroll promptly: Sign up for or change your Medicare coverage within your SEP to avoid penalties or coverage gaps.

-

Seek assistance: If you're unsure about your options, consider consulting a licensed Medicare agent or visiting Medicare.gov for guidance.

What should I do if I miss the Medicare Open Enrollment period, and I want to change my plan?

Contact a local agent. There may be a special election period available that you aren't aware of. Your agent can help guide you.Final Thoughts

Life changes can impact your healthcare needs, and Medicare's Special Enrollment Periods are designed to provide flexibility during these times. By understanding the qualifying events and acting promptly, you can ensure continuous and appropriate coverage without unnecessary penalties.

Remember, staying informed and proactive is key to making the most of your Medicare benefits.