The Green Card Medicare Guide: The 5-Year Rule, Buy-In Premiums, and What Agents Tell Immigrants Turning 65

-

May 20, 2026

If you hold a green card and you're approaching 65, you've probably heard that Medicare is available to you. That's true, but the path to getting it looks different than it does for someone who spent their entire career in the U.S. There's a residency clock you need to satisfy, premiums that U.S.-born retirees never see, and a handful of lesser-known rules that can save you thousands of dollars a year if you know about them.

We pulled answers from dozens of licensed Medicare agents who field these exact questions from immigrants every week. What follows is what they actually tell green card holders sitting across the desk from them.

The 5-Year Continuous Residency Requirement

The single biggest eligibility gate for green card holders is the 5-year continuous residency rule. To qualify for Medicare, you must be a lawful permanent resident who has lived in the United States continuously for at least five years before enrolling.

Turning 65 alone is not enough. A green card holder who has been in the U.S. for four years and turns 65 next month is not yet eligible. They'll need to wait until they hit the 5-year mark. As one agent puts it: "Medicare states that an individual is eligible for Medicare if they are 65 and have resided in the U.S. continuously as a lawful permanent resident for at least five years."

The word "continuously" matters. Extended trips abroad can potentially reset or interrupt that clock, so if you're planning travel during those first five years, talk to an agent or Social Security about what counts as a break in residency.

Editor's note: Agent answers below were originally written using 2025 premium figures. The article text and table above reflect current 2026 Medicare premium amounts.

I'm a green card holder who's been in the US for 4 years and turning 65 soon. Am I eligible for Medicare?

Yes — green card holders can get Medicare, but they must have 5 continuous years of U.S. residency as a lawful permanent resident before they’re eligible. If you're turning 65 but have only been in the U.S. for 4 years, you aren’t eligible just yet. You’ll become eligible as soon as you reach the full 5-year residency mark, and at that point you can enroll in Part A, Part B, and the rest of Medicare just like anyone else.If you haven’t worked 40 quarters in the U.S., you’re still eligible once you hit the 5-year residency requirement, but you would pay a premium for Part A. For 2025, the Part A premium is $278/month with 30–39 work credits, or $506/month with fewer than 30 credits. Part B has the same standard premium for everyone regardless of work history.

Once you reach the 5-year mark (even if you're already past 65 by then), your Initial Enrollment Period begins. You get a 7-month enrollment window, and as long as you sign up during that period, you won't face any late penalties.

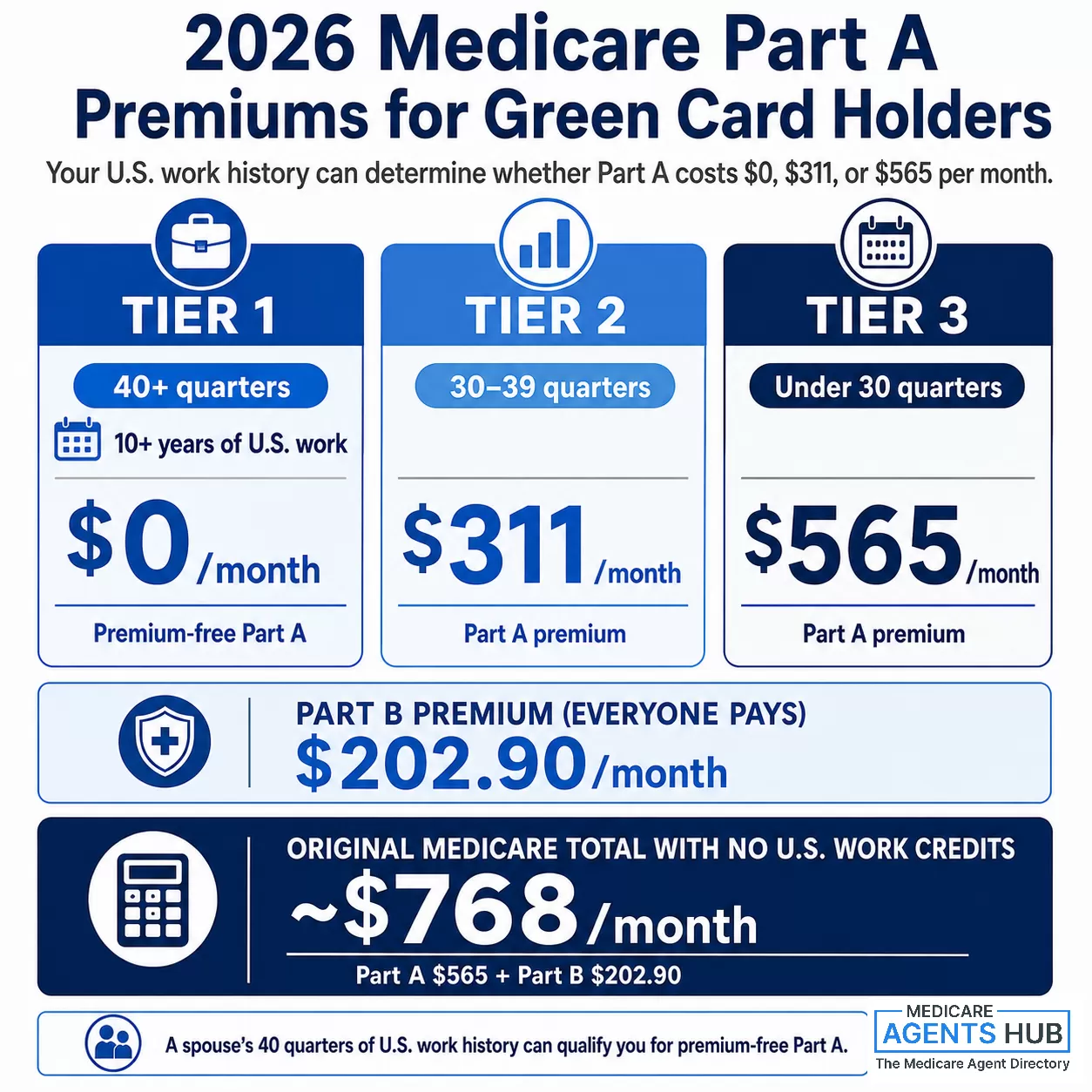

Buying Into Part A: The Three Premium Tiers

For most Americans who worked a full career in the U.S., Medicare Part A (hospital coverage) is premium-free. That's because they paid Medicare taxes for at least 40 quarters, or 10 years. Green card holders who spent their working years overseas typically don't have those credits, and that changes the math significantly.

Part A eligibility falls into three tiers based on how many quarters of U.S. work history you (or your spouse) have:

| Work Credits (Quarters) | 2026 Monthly Part A Premium |

|---|---|

| 40+ quarters (10+ years) | $0 (premium-free) |

| 30–39 quarters | $311/month |

| Under 30 quarters | $565/month |

Part B (medical coverage) works the same for everyone regardless of work history. The standard 2026 Part B premium is $202.90/month, and it applies whether you worked 40 years in the U.S. or zero.

Add those together and a green card holder with no U.S. work credits is looking at roughly $768/month just for Original Medicare (Parts A and B) before any supplemental coverage. That's a hidden cost that catches many first-time enrollees off guard.

Can I enroll in Medicare if I've never paid into Social Security due to working overseas?

If you are a US citizen or lawful permanent resident (with 5+ years of residency) you CAN enroll in medicare, but your cost will likely be different if you’ve never paid into the system.Part A is premium free if you’ve worked for 40 quarters (10 years) and paid into the system. If you don’t meet that requirement, you can BUY part A coverage.

Part B would be handled the same as everyone else - you’ll pay the premium appropriate for your income.

Your supplemental coverage (Medicare Advantage, Medigap and/or Part D) are based on your medicare eligibility and not based on your social security contributions.

NOTE - Foreign work credits from countries with TOTALIZATION agreements with the US (ie Canada, the UK, Germany) MAY count toward the Social Security eligibility and COULD reduce or eliminate the Part A premium. Also, if you’re married to someone with US Work Credits that can make a difference, so there are a lot of variables to this situation. Social Security can help you determine what comes next.

The Spouse Shortcut

Multiple agents flag this as the single most important thing to check before assuming you'll pay the full Part A premium: your spouse's work history. If you're married to someone (U.S. citizen or green card holder) who has earned 40 quarters of U.S. work credits, you can qualify for premium-free Part A based on their record.

The requirements are straightforward: you need to have been married for at least one year, and your spouse needs to be at least 62 years old with 40 quarters of work history. According to SSA guidance cited by AARP, when a green card holder qualifies for premium-free Part A through a spouse's work record, factors such as the five-year residency requirement may not apply. If neither spouse qualifies through work history, the standard 5-year continuous residency rule remains in effect.

Former spouses may qualify too. If you were married for at least 10 years to someone with 40 quarters, their work record can still help you, even after divorce.

Totalization Agreements: When Foreign Work Credits Count

This is the rule that almost no consumer-facing Medicare website mentions, but agents who work with immigrant clients bring it up regularly.

The U.S. has totalization agreements with roughly 30 countries, including Canada, the United Kingdom, Germany, Japan, South Korea, and Australia. Under these agreements, work credits earned in those countries can count toward your 40-quarter requirement for U.S. Social Security and Medicare eligibility.

What does that mean practically? If you worked 25 years in Germany and 5 years in the U.S. (20 quarters), those German work credits may push you over the 40-quarter threshold and qualify you for premium-free Part A. The difference between paying $565/month and $0/month is nearly $6,800 a year.

The Social Security Administration handles verification of foreign credits, and the process can take time. Agents recommend starting this conversation with SSA well before your enrollment window opens. If you're turning 65 and new to Medicare, getting your work credit situation sorted out early is one of the most valuable things you can do.

The Penalty Clock: Why It Doesn't Start Until You're Eligible

One of the most common fears green card holders have is that they'll be hit with permanent late-enrollment penalties for not signing up at 65. If you haven't met the 5-year residency requirement yet, this fear is unfounded.

Agents are nearly unanimous on this point: you cannot be penalized for not enrolling in something you aren't eligible for yet. The penalty clock for Medicare Parts A, B, and D does not begin ticking until you actually become eligible to enroll.

Is there a penalty for Medicare Part A or B for a 65-year-old green card holder who hasn’t met the five-year U.S. residency requirement and has no other insurance?

No—there is no late-enrollment penalty for Medicare Part A or Part B until the person actually becomes eligible to enroll.A 65-year-old green card holder who has not yet met the five-year U.S. residency requirement is not eligible for Medicare, so the clock for penalties hasn’t started.

Once they reach five years of continuous lawful residency, they can enroll during their Initial Enrollment Period, and as long as they sign up at that time, there is no penalty for not having had other insurance before then.

The critical moment comes when you do hit your 5-year anniversary. At that point, your Initial Enrollment Period opens, and you have a 7-month window (3 months before, the month of, and 3 months after your eligibility date). If you miss that window and don't have other creditable coverage, the Part B late-enrollment penalty kicks in: a 10% surcharge for every 12-month period you were eligible but didn't enroll, added to your premium for life.

So while you're safe before the 5-year mark, the moment you cross it becomes the most important enrollment deadline of your life. Mark it on your calendar and connect with an agent at least a few months ahead of time.

Covering the Gap: What to Do Before Year Five

If you're a green card holder who arrived at age 62 and won't be eligible for Medicare until 67, you still need health insurance for those years in between. Agents point to two main options.

ACA Marketplace Plans

Lawfully present immigrants can purchase coverage through the ACA Health Insurance Marketplace even if they haven't been in the U.S. for five years. Depending on your household income, you may qualify for premium subsidies, though eligibility rules and subsidy amounts can change from year to year. Check HealthCare.gov or work with a licensed broker to see what's available in your area and income bracket.

Several agents note that for green card holders who will eventually have to pay the full Part A premium anyway, an ACA plan can sometimes be the more cost-effective option even after they become Medicare-eligible, particularly if their income qualifies them for substantial subsidies. An independent broker can run the numbers both ways.

Short-Term or New Immigrant Insurance

Some private insurers offer temporary medical insurance products designed specifically for new permanent residents waiting for Medicare eligibility. These are typically less comprehensive than ACA plans but can serve as a bridge if you need basic coverage and don't qualify for marketplace subsidies.

Putting It All Together: A Timeline for Green Card Holders

Based on what agents tell their clients, here's the sequence that matters:

- As soon as you get your green card: Note your residency start date. The 5-year clock begins the day you become a lawful permanent resident.

- Years 1–4: Get coverage through the ACA Marketplace or employer. If you're working in the U.S., you're building quarters toward premium-free Part A.

- Around year 4: Contact the Social Security Administration to verify your work credit history. If you worked in a country with a totalization agreement, start the verification process now.

- 3 months before your 5-year anniversary (or 65th birthday, whichever is later): Your Initial Enrollment Period opens. Apply for Medicare Part A and Part B through Social Security.

- Once enrolled: Work with a licensed Medicare agent to add supplemental coverage (Medigap, Medicare Advantage, or Part D) based on your needs and budget.

Can I enroll in Medicare if I've never paid into Social Security due to working overseas?

Yes—you can still get Medicare even if your paychecks never fed the Social Security pot while you were globetrotting. Here’s the wrinkle: without 40 U.S. work credits (or a spouse who has them) you’ll have to buy Part A instead of getting it premium‑free; in 2025 that’s up to about $505 a month.Part B and Part D work the same for everyone—you pay the regular monthly premiums and must enroll during the proper windows to dodge late penalties. You’ll also need to be a U.S. citizen or a permanent resident who’s lived stateside at least five consecutive years. Bottom line: Medicare is still on the menu, it just may cost a bit more.

Let’s talk through the math and timing so your re‑entry to the U.S. health system is smooth and penalty‑free

What to Bring When You Visit Social Security

Agents recommend gathering these documents before your appointment with the Social Security Administration. Having everything ready can speed up the process significantly:

- Green card (with your permanent residency start date)

- U.S. work history documentation (W-2s, pay stubs, or tax returns showing quarters worked)

- Spouse's work record (if applying based on their credits), along with your marriage certificate

- Foreign pension or employment records (if you worked in a country with a totalization agreement)

- Current health insurance details (employer plan, ACA plan, or other creditable coverage)

- Proof of identity (passport, driver's license, or state ID)

Frequently Asked Questions

Can a green card holder get Medicare before five years?

Generally, no. The 5-year continuous residency requirement applies to all lawful permanent residents. The one notable exception: if you qualify for premium-free Part A through a spouse's U.S. work record (40 quarters), the residency requirement may not apply. Outside of that, you'll need to wait until your 5-year anniversary.

Does the Medicare penalty start at 65 or after the five-year residency mark?

After the five-year mark. The late-enrollment penalty only starts when you become eligible to enroll and choose not to. A green card holder who isn't yet eligible because they haven't met the residency requirement cannot be penalized. Once you hit the 5-year mark, your 7-month Initial Enrollment Period begins, and the penalty clock starts if you don't sign up.

Can my spouse's work record help me get premium-free Part A?

Yes. If your current spouse has at least 40 quarters (10 years) of U.S. work history, you've been married for at least one year, and your spouse is at least 62 years old, you can qualify for premium-free Part A on their record. Former spouses can also help if the marriage lasted at least 10 years. Check with the Social Security Administration to confirm your eligibility.

Can foreign work credits count toward Medicare?

They can if you worked in one of the roughly 30 countries that have a totalization agreement with the U.S. Work credits from those countries can be combined with any U.S. quarters you've earned to help you reach the 40-quarter threshold for premium-free Part A. Contact the Social Security Administration to start the verification process.

What health insurance can I use before I qualify for Medicare?

Lawfully present immigrants can buy coverage through the ACA Health Insurance Marketplace, and may qualify for income-based subsidies. Employer-sponsored insurance is another option if you're working. Some private insurers also offer short-term plans designed for new permanent residents. A licensed insurance broker can help you compare options for your specific situation.

Key Takeaways

- Green card holders need 5 years of continuous U.S. residency before they can enroll in Medicare, regardless of age.

- Without 40 quarters of U.S. work history, you'll pay a monthly Part A premium of up to $565 in 2026. A spouse's work record can eliminate this cost entirely.

- Totalization agreements with roughly 30 countries may let you combine foreign and U.S. work credits to qualify for premium-free Part A.

- There is no late-enrollment penalty for the period before you become eligible. The penalty clock starts at your 5-year mark, not at age 65.

- During the gap, ACA Marketplace plans are available to lawfully present immigrants and may include income-based subsidies.