Enrolling in Medicare As You Are Turning 65

-

Last Updated July 22, 2026

Should You Enroll in Medicare at 65, or Wait?

One of the most important (and often confusing) first steps when turning 65 is figuring out whether you even need to enroll in Medicare right away. The short answer? It depends. The long answer came through loud and clear in the advice your network of agents shared.

Many professionals emphasized that your employment status and current insurance coverage are the key deciding factors.

If you're still working and covered by an employer-sponsored health plan (or your spouse's), you may be able to delay signing up for Part B, which carries a monthly premium. But it's not automatic. You have to make sure that the plan is considered "creditable coverage" by Medicare standards. If it is, you're allowed to postpone Part B enrollment without penalties. If it's not, you could face lifelong late fees and coverage gaps if you delay.

Some agents advised starting with a simple question: Are you going to continue working after 65? If so, and if your employer plan is strong, you might be better off sticking with it for now. Others suggested comparing the costs and coverage of your employer plan versus what you’d pay and receive with Medicare. If Medicare looks more cost-effective, or your employer coverage is thin, that may be your cue to switch.

A few pointed out that if you’re covered through the Marketplace (healthcare.gov or a state exchange), you’re required to leave it and move to Medicare as soon as you're eligible for premium-free Part A. Otherwise, you could lose your coverage and miss out on your benefits.

In contrast, if you're retiring at 65, self-employed, or have no group health coverage, nearly every agent was in agreement: apply for Part A and Part B right away. There’s no upside to waiting if you need coverage, and the sooner you apply, the smoother the process will go.

Ultimately, this first fork in the road, enroll now or wait, depends on your personal situation, your coverage, and whether your current plan stacks up well against Medicare.

I'm turning 65 in three months but still working with employer coverage. Do I need to sign up for Medicare right now or can I wait?

The short answer is no, but you can. If your employer is a large group (at least 20 employees), they can not force you to exit your group plan and go on Medicare. Having said that, it may not be a bad idea depending on your income, how much the group insurance is costing you, and what your benefits and deductibles look like. You generally have the option of deferring Part B until you are ready to leave the group plan. We sit down with our clients and review their current summary of benefits and costs to see if it would make better financial sense to stay put or make the move.Special Cases: VA, COBRA, and Marketplace Coverage

A few situations trip people up more than any others. If any of these describe you, read carefully before deciding to delay Part B:

-

VA benefits: VA coverage alone doesn’t protect you from a Part B late-enrollment penalty. Most veterans still take premium-free Part A, and many take Part B as backup in case they ever need non-VA care. Skip Part B and you’ll wait for the next General Enrollment Period, plus pay a lifetime penalty, if you ever want to enroll later.

-

COBRA and retiree plans: COBRA is not considered creditable coverage for delaying Part B. If you go from active employment to COBRA at 65, you generally still need to enroll in Part B on time or you’ll owe a penalty.

-

Marketplace / ACA plans: Marketplace plans do not count as creditable coverage either. Once you’re eligible for premium-free Part A, you’re expected to move to Medicare. Staying on your ACA plan past that point means losing premium subsidies and risking late-enrollment penalties.

-

Small-employer plans (under 20 employees): When your employer has fewer than 20 workers, Medicare is usually your primary payer, not the employer plan. Enroll in Part B at 65 or you may end up with big gaps in coverage.

When in doubt, confirm with your HR department in writing that your plan is creditable, or call 1-800-MEDICARE.

How to Sign Up for Medicare at 65: Enrolling in Parts A and B

Once you’ve figured out whether you need to enroll, the next step is knowing how to enroll in Medicare Parts A and B, and exactly what happens next.

For those who aren’t automatically enrolled, the enrollment process starts with a visit to SSA.gov, the Social Security Administration’s website. You’ll need to create or log into your account, locate the Medicare section, and submit your application for Part A and Part B. Several agents noted that the online application is straightforward, and many recommend it as the fastest and most convenient option, especially if you’re short on time before your 65th birthday.

Other options include calling Social Security directly at 1-800-772-1213 or visiting your local Social Security office, though this often requires an appointment and can take longer. A few advisors emphasized that if you're only a month out from your birthday, it’s better to go the online route or call. Walk-ins may not guarantee timely processing.

Do You Automatically Get Medicare When You Turn 65?

What if you’re already receiving Social Security retirement or disability benefits? In that case, your enrollment is typically automatic. Medicare will mail you a red, white, and blue Medicare card a few months before your 65th birthday. That card confirms your Part A and Part B effective dates, and you’ll need it to choose additional coverage like a Part D plan or Medicare Advantage. But if you haven’t received your card two months before your birthday month, it’s time to follow up with Social Security to ensure your enrollment is moving forward.

A few agents also pointed out a common mistake: assuming you're all set without checking. Whether you're planning to continue working, apply manually, or expect automatic enrollment, it’s worth verifying that Parts A and B are active and that you know your effective dates.

Once you apply and are approved, you’ll receive a confirmation letter and eventually your Medicare card. Keep this card safe; you'll need it to move on to selecting a plan. And don’t worry if you're still waiting for your card when shopping for plans. Having your Medicare Beneficiary Identifier (MBI) and effective dates is often enough for your agent to help you choose coverage.

How Long Before Turning 65 Should You Apply for Medicare?

The timeline is important too. It can take several weeks for your application to process and your card to arrive. That’s why so many advisors recommend applying at least three months before your 65th birthday, to avoid delays or missing your enrollment window altogether.

I'm turning 65 in three months but still working with employer coverage. Do I need to sign up for Medicare right now or can I wait?

No, you do not have to wait until your birthday month to sign up for Medicare. It is best to start gathering all the information at least 3 months prior, so you have all the coverage you need. Do you have all the doctors' information? Your prescriptions and health records? If you will need any procedures that you have been holding off until retirement, that also needs to be considered.In short, whether you’re going online, calling, or visiting in person, your first real task is activating Parts A and B. Once that’s done and you’ve got your card (or at least your MBI), you’re ready for the next big step: picking a plan.

Choosing Your Coverage: Medicare Advantage vs. Supplement + Part D

Once you’ve enrolled in Medicare Parts A and B, the next step is to decide how you want to receive your coverage. This is where things can get overwhelming, but the agents who responded offered a wide range of helpful advice, each with a unique take on how to evaluate your options.

Most advisors agree that this decision comes down to choosing between two core paths:

-

Original Medicare (Parts A & B) + a Medicare Supplement Plan + a separate Part D plan, or

-

Medicare Advantage (Part C), a bundled plan offered by private insurance companies.

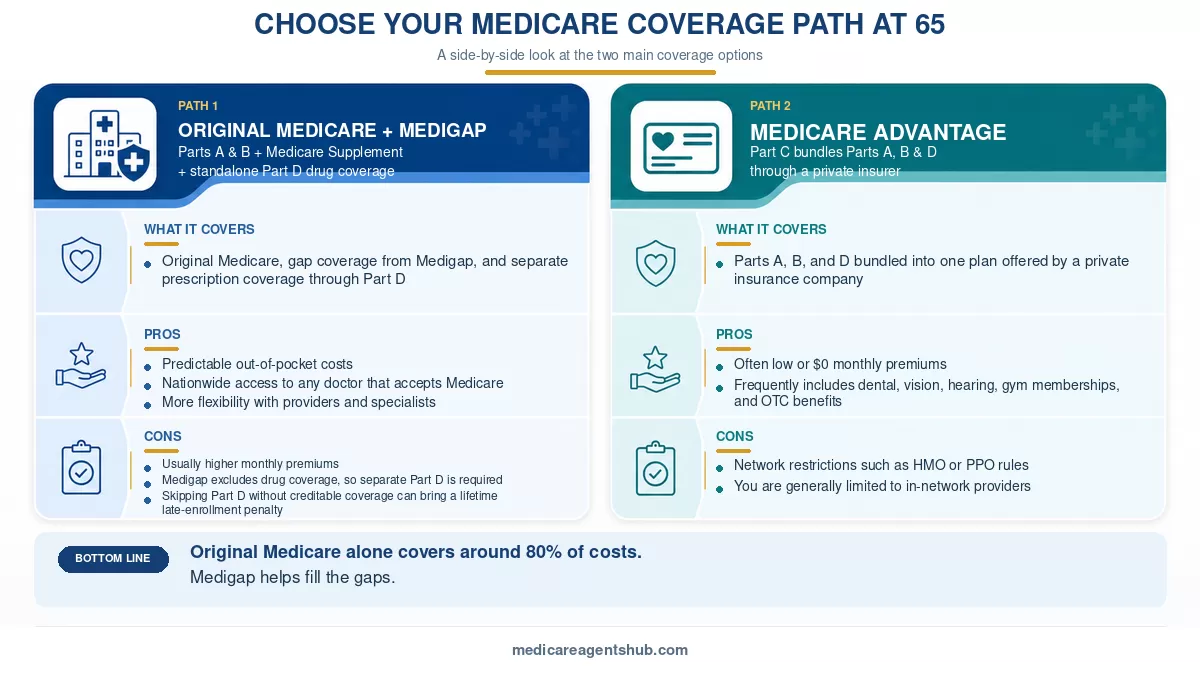

Path 1: Original Medicare + Supplement + Part D

With Original Medicare, you get hospital and medical coverage (Parts A & B), but it only covers around 80% of your costs. That’s where a Medicare Supplement (also called Medigap) plan comes in. These plans help fill the gaps, covering things like deductibles, copays, and coinsurance.

A number of agents noted that this combo is ideal for people who want:

-

Predictable out-of-pocket costs

-

Nationwide provider access (see any doctor that accepts Medicare)

-

More flexibility with providers and specialists

However, it’s important to know that Medigap plans do not include prescription drug coverage. That means you’ll also need to enroll in a standalone Part D plan to get coverage for medications. Skip Part D when you’re first eligible (and you don’t have other creditable drug coverage), and you’ll owe a lifetime late-enrollment penalty added to your monthly premium every year you have Medicare drug coverage after that.

Some advisors added that while Medigap plans offer stability and broad access, they usually have higher monthly premiums than Medicare Advantage. But for many, the peace of mind and provider freedom is worth the price.

Path 2: Medicare Advantage (Part C)

The alternative route is a Medicare Advantage plan, which bundles your Parts A and B with Part D, and often includes extras like:

-

Dental

-

Vision

-

Hearing

-

Gym memberships

-

OTC benefits

These plans are run by private insurance companies and are approved by Medicare. A few agents noted that for many people, Medicare Advantage plans are attractive because they often have low or even $0 monthly premiums. That said, they typically involve network restrictions, like HMOs or PPOs, meaning you may need referrals or stick to local providers.

Several agents suggested that Medicare Advantage might work best for those who:

-

Don’t travel much

-

Prefer all-in-one convenience

-

Are comfortable using a defined network of providers

-

Want extra non-medical benefits like dental or fitness perks

But others emphasized that these plans aren’t for everyone. Some shared that clients are often surprised by co-pays and coverage limits, especially for specialists, hospital stays, or out-of-network care. One common theme was that Medicare Advantage involves trade-offs between cost and flexibility, and it’s critical to weigh those carefully.

| Feature | Original Medicare + Medigap + Part D | Medicare Advantage (Part C) |

|---|---|---|

| Monthly premium | Higher (Medigap + Part D premiums) | Often low or $0 |

| Provider access | Any doctor that accepts Medicare, nationwide | Usually local HMO/PPO networks |

| Out-of-pocket costs | Predictable, minimal after Medigap pays | Copays and coinsurance can vary by service |

| Prescription drugs | Separate Part D plan required | Usually bundled in |

| Extra benefits | None built in | Often dental, vision, hearing, gym, OTC |

| Referrals | Not needed | May be required, depending on plan type |

| Best fit for | Frequent travelers who want provider freedom and steady costs | Homebodies who want all-in-one convenience and lower premiums |

So, Which One Is Right for You?

There’s no one-size-fits-all answer here, and nearly every agent made that clear. Instead of guessing or going with what a friend or relative chose, the most consistent advice was this: sit down with someone who can run a side-by-side comparison based on your:

-

Zip code

-

Health history

-

Prescription drug list

-

Preferred doctors and hospitals

-

Budget and comfort with risk

Some even mentioned conducting a formal Needs Assessment, which helps tailor the plan to your individual circumstances. A few advisors also suggested watching Medicare 101 educational videos, or using plan comparison tools, but emphasized that a conversation with a broker tends to make the process much easier.

Your choice isn’t just about which plan looks better on paper. It’s about which one fits your life, your habits, and your health.

Whether you want the structure and added benefits of an all-in-one Medicare Advantage plan, or the freedom and predictability of Original Medicare + Medigap, the key is making that choice with guidance, not guesswork.

Can I switch from a Medicare Advantage plan to a Supplemental/Medigap plan during the Annual Enrollment Period without answering health questions?

No. The Annual Enrollment Period doesn't let you switch to a Medigap plan without answering health questions. The only ways to avoid medical underwriting are:• During your Medicare Supplement Open Enrollment Period (the first 6 months after you start Part B at age 65)

• If you live in a "birthday rule" state (like California, Oregon, Idaho, Illinois, or Nevada) where you can switch Medigap plans each year around your birthday without health questions

• If you qualify for a Guaranteed Issue situation, such as losing coverage or moving out of your plan's service area

After You Apply: Your Medicare Card, What to Expect, and What to Do Next

Once you’ve submitted your application for Medicare, whether online through SSA.gov, over the phone, or in person, the waiting begins. But this isn’t a passive process. According to the professionals who weighed in, there are several smart steps to take while you wait for your Medicare card to arrive.

Step 1: Watch for Your Medicare Card

After you’re approved for Medicare Parts A and B, you’ll receive your red, white, and blue Medicare card in the mail. For most people, this happens within a few weeks, but timelines can vary.

Your card will include:

-

Your Medicare Beneficiary Identifier (MBI), a unique ID number

-

Your Part A and B effective dates

If you're already receiving Social Security benefits, you might receive your card automatically, generally about two months before your 65th birthday. But if you applied manually, it's important to keep an eye on your mailbox, and follow up with Social Security if the card hasn’t arrived by about a month before your coverage needs to start.

Some agents also noted that you’ll receive a confirmation letter or tracking number after applying, which you can use to monitor your application progress through the SSA portal. Hang onto this letter. It can serve as temporary proof of Medicare eligibility in some cases.

Step 2: Gather Key Information

Once your enrollment is approved, or even before the card arrives, it’s time to start preparing to shop for coverage. Agents frequently recommended having this info ready:

-

Your MBI number (from the card or SSA confirmation)

-

The effective dates for Parts A and B

-

A list of your doctors and specialists

-

Your current prescriptions

-

Your preferred pharmacies

-

Any details about existing coverage (employer plan, union plan, Marketplace, etc.)

Having these details upfront allows an agent or broker to help you evaluate plans efficiently and avoid delays once enrollment windows open.

Step 3: Talk to Someone Who Can Help

The message was clear across multiple responses: Don’t try to do this alone unless you want to. Medicare can be complicated, and working with a licensed broker comes at no cost to you. Premiums are the same whether you work with someone or not.

Many agents offer free consultations, either in person or virtually, and can walk you through:

-

Comparing Medicare Advantage vs. Medigap + Part D

-

Reviewing local plans in your ZIP code

-

Helping you fill out additional applications

-

Ensuring your plan is active before your start date

Some even provide Medicare 101 education, tailored assessments, and annual plan reviews to ensure your coverage stays aligned with your needs over time.

Step 4: Don’t Delay. Act Within Your Enrollment Window

Remember, your Initial Enrollment Period (IEP) spans seven months: starting three months before the month you turn 65, continuing through your birthday month, and ending three months after.

Multiple advisors stressed that the earlier you apply, the better. If you wait until your birthday month or later, your coverage could be delayed, and your choice of plans may be limited. And if you miss the IEP altogether and don’t qualify for a special enrollment period, you could face lifetime penalties for late enrollment.

So even after you apply, you’re still on a deadline. Take action, stay organized, and don’t assume you have more time than you do.

Bottom Line

Your Medicare card isn’t the finish line. It’s the start of your real planning. Getting that card in hand opens the door to choosing the right plan, ensuring continuous coverage, and getting the health benefits you need without interruption.

From that point on, it’s all about aligning your options with your real-world needs, and that’s where personal guidance can make all the difference.

Why You Don’t Have to Navigate Medicare Alone

One of the most consistent messages across the dozens of agent responses was this: You don’t have to do this by yourself. Medicare enrollment can feel overwhelming. There’s a reason so many people describe it as a “maze.” But you don’t have to wander through it without a guide.

In fact, a number of agents described themselves not just as brokers, but as navigators, coaches, or even translators. Medicare comes with terms, acronyms, timelines, and decision points that most people have never encountered before. And while the system is technically “learnable,” that learning curve can be steep, especially if you’re trying to make the right decisions quickly.

Medicare is a Process, Not a Checkbox

It’s easy to think that enrolling in Medicare is just a form you fill out and move on, but many agents pushed back on that idea. They framed it as a series of decisions, each dependent on your:

-

Health history

-

Financial picture

-

Prescriptions

-

Family situation

-

Travel habits

-

Employer benefits

-

Retirement timeline

One agent referred to it as the difference between a “direct process” and a “wandering in the desert” process. And it’s true: if you try to absorb everything at once, from scratch, it can get overwhelming fast.

But with help? It becomes a step-by-step journey, where you only need to make one decision at a time.

Agents Are Educators, Not Just Salespeople

Another theme that stood out was how much emphasis your advisors put on education. Several mentioned conducting Medicare 101 sessions, offering basic explainer videos, or providing a structured walkthrough of the different Medicare paths.

And importantly: they don’t just explain the rules. They relate them to you. They help you understand how Part A works for you. How Medigap vs. Advantage shakes out for your lifestyle. What each timeline, form, and card means in your specific case.

This is the kind of guidance people don’t get from online articles or comparison tools alone.

There’s No Cost to Use a Broker, But the Value Is Huge

Multiple agents made this point clearly: you don’t pay anything extra to work with a licensed Medicare broker. Plan prices are set. They won’t be higher because someone helped you enroll.

But the value? It can be massive. Agents can:

-

Run personalized plan comparisons

-

Review your doctors, prescriptions, and pharmacy preferences

-

Help you fill out plan applications

-

Handle follow-ups and documentation

-

Provide support if your circumstances change

-

Make sure you avoid penalties or late fees

-

Offer yearly check-ins during the Annual Enrollment Period

Some even shared that they apply on your behalf, make sure your cards arrive, and walk you through the first day of using your benefits.

It's Not Just About Plans. It’s About Peace of Mind

Beyond the paperwork and timelines, many responses acknowledged the emotional side of turning 65. For a lot of people, it’s a moment of transition: from work to retirement, from employer insurance to Medicare, from independence to seeking help.

And that’s where having a trusted guide can make all the difference. It’s not just about “what’s covered.” It’s about clarity, confidence, and knowing you made the right choices.

Agents described the process as a relationship, not a transaction. One that continues beyond the initial signup, with ongoing support, questions answered, and annual reviews to make sure your coverage keeps up with your needs.

A Final Word From the Field

Even among such a wide range of perspectives, this was a near-universal belief: getting help makes this process better. You’re not just filling out forms. You’re building your healthcare future. And having someone in your corner can mean the difference between confusion and clarity.

So whether you're just now applying or already have your Medicare card in hand, don’t hesitate to reach out. A good broker will listen, explain, guide, and stand by you through the entire process, and often beyond.

I’ll be turning 65 in April. I have full VA coverage and good hospital and doctor coverage through Eisenhower here in the desert. The VA doesn’t provide dental care. Do I still need to enroll in Medicare, and if so, which part makes sense for my situation?

With full VA coverage, you don’t have to enroll in Medicare at 65. Most veterans still take Part A (free hospital coverage) as backup. Part B is optional, you can skip it if VA care is enough, but delaying may lead to a penalty if you enroll later. Dental would need a separate plan either way.Your Medicare Roadmap: A Real-World Guide to Getting It Right

Turning 65 and stepping into Medicare doesn’t have to be overwhelming, especially when you break the process down into practical, human steps. Based on the diverse, grounded insights from professionals across the country, here’s a step-by-step roadmap built not from theory, but from real-world experience.

Step 1: Decide Whether You Need to Enroll Right Now

-

Are you still working and covered by an employer or union health plan?

-

Is your coverage considered "creditable" under Medicare rules?

-

Are you planning to retire before or after 65?

-

Are you currently on Marketplace coverage (which you’ll need to leave)?

Answering these questions determines whether you should enroll now or delay Part B to avoid unnecessary premiums or penalties.

Step 2: Apply for Medicare Parts A and B

If you need coverage, apply through one of three methods:

-

Online at SSA.gov (fastest and most recommended)

-

By phone at 1-800-772-1213

-

In person at your local Social Security office

If you’re already receiving Social Security, your enrollment may be automatic, but don’t assume. Check your status and timeline to avoid delays.

Step 3: Watch for Your Medicare Card

After you apply (or once you’re automatically enrolled), you’ll receive your red, white, and blue Medicare card. It will show your Medicare ID and the effective dates for Parts A and B.

You’ll need this card, or at least your Medicare number and start dates, to shop for additional coverage like a Medicare Supplement, Part D drug plan, or Medicare Advantage.

Step 4: Evaluate Your Coverage Options

You’ve got two main paths:

Path A: Original Medicare + Medigap + Part D

-

More predictable costs

-

Broad provider access

-

Requires separate drug plan

Path B: Medicare Advantage (Part C)

-

Bundled coverage (often includes drugs, dental, vision, etc.)

-

May have $0 premiums

-

Typically uses local provider networks

Each path has pros and cons. What matters is what fits your prescriptions, your doctors, your routine, your budget, your risk tolerance. There is no “best plan,” only the one that’s best for you.

Step 5: Gather Your Info

To choose the right plan, you’ll need:

-

Your Medicare Beneficiary Identifier (MBI) number

-

Your Part A & B effective dates

-

A list of current medications

-

Your preferred doctors or clinics

-

Any coverage you’re keeping or replacing

Step 6: Talk to Someone Who Can Guide You

Licensed Medicare brokers can:

-

Compare your options side-by-side

-

Help you apply

-

Answer questions year-round

-

Make sure you’re covered on Day 1

-

Help you avoid penalties, gaps, or the wrong fit

There’s no charge to you, and for many people, it makes all the difference.

I've been on my employer's health plan but am retiring soon. What should I consider when moving to Medicare?

You will need to enroll in part A and B of Medicare through the Social Security Administration with a requested start date corresponding to the end of your employer health plan. You can do this online at SSA.gov or by calling your local Social Security office and scheduling a phone appointment. If you are over the age of 65, you and your employer will need to complete the form CMS-L564 Request for Employment Information to show you had employer coverage during the time you delayed enrolling in Medicare. This keeps you from having to pay the part B late enrollment penalty.Step 7: Enroll in Your Chosen Plan on Time

Use your Initial Enrollment Period wisely. It spans:

-

3 months before your 65th birthday

-

Your birthday month

-

3 months after

Enroll early if you can. It ensures smooth transitions and maximizes your plan options.

Step 8: Don’t Panic. You’ve Got Support.

This process has a lot of moving parts, but it doesn’t have to be stressful. With help from experienced professionals who walk people through this every day, you can go from overwhelmed to in control, one step at a time.

Final Thought

You’ve reached an important milestone. While Medicare may seem complicated at first, it doesn’t have to stay that way. When you focus on your personal situation, take each step with purpose, and work with someone who understands the system, Medicare becomes less of a maze and more of a map.

This isn’t about knowing everything. It’s about knowing what to do next.

And now, you do.