How to Switch from Employer Health Insurance to Medicare

-

Last Updated August 3, 2026

Making the switch from employer health insurance to Medicare can be challenging, but with the right information, you can make the switch smoothly. Here’s a full guide on how to successfully move from employer-based coverage to Medicare, so you keep continuous and full health insurance coverage.

Can you have Medicare and employer insurance at the same time?

Yes. If you’re 65 or older and still working, you can keep your employer coverage and enroll in Medicare at the same time — the two plans coordinate, with one paying first and the other paying second. Whether you should enroll right away or delay Part B depends on the size of your employer and whether the employer plan is considered creditable coverage. The rest of this guide walks through the timing, the coordination rules, and what to do when you’re ready to switch fully to Medicare.

Can I drop my employer health insurance and switch to Medicare instead?

Maybe — but be careful.If you're still working and your employer coverage is considered "creditable" (which most employer plans are), you can delay Medicare without penalty. But if you drop employer coverage and enroll in Medicare, a few things to know:

Part A is usually free — grabbing it at 65 is generally fine.

Part B is the tricky one. Once you drop employer coverage, you typically have an 8-month Special Enrollment Period to sign up without penalty.

HSA conflict — if you're contributing to an HSA, enrolling in any part of Medicare stops that.

Cost comparison — employer plans are often cheaper (especially if your employer subsidizes premiums), so run the numbers before switching.

Bottom line: It's allowed, but whether it's smart depends on your employer's plan cost, your health needs, and whether you're still working. Worth doing a consultation where we can do a side-by-side comparison before you pull the trigger.

Understanding Medicare eligibility and enrollment periods

Medicare Eligibility: If you are a U.S. citizen or permanent resident aged 65 or older, you are eligible for Medicare. Eligibility is not affected by employment status, so you can enroll in Medicare even if you are still working and have health insurance through your employer.

- Initial Enrollment Period (IEP): This seven-month window begins three months before the month you turn 65, includes your birth month, and ends three months after your birth month. Enrolling during this period gets your coverage started without delay.

- General Enrollment Period (GEP): If you miss your IEP, you can enroll during the GEP from January 1 to March 31 each year. Coverage now begins the month after you sign up (a change from the old July 1 rule), but you may still incur late enrollment penalties.

- Special Enrollment Period (SEP): If you have employer health insurance, you can delay Medicare enrollment without penalty. You have an eight-month SEP to enroll in Medicare once your employment or health coverage ends.

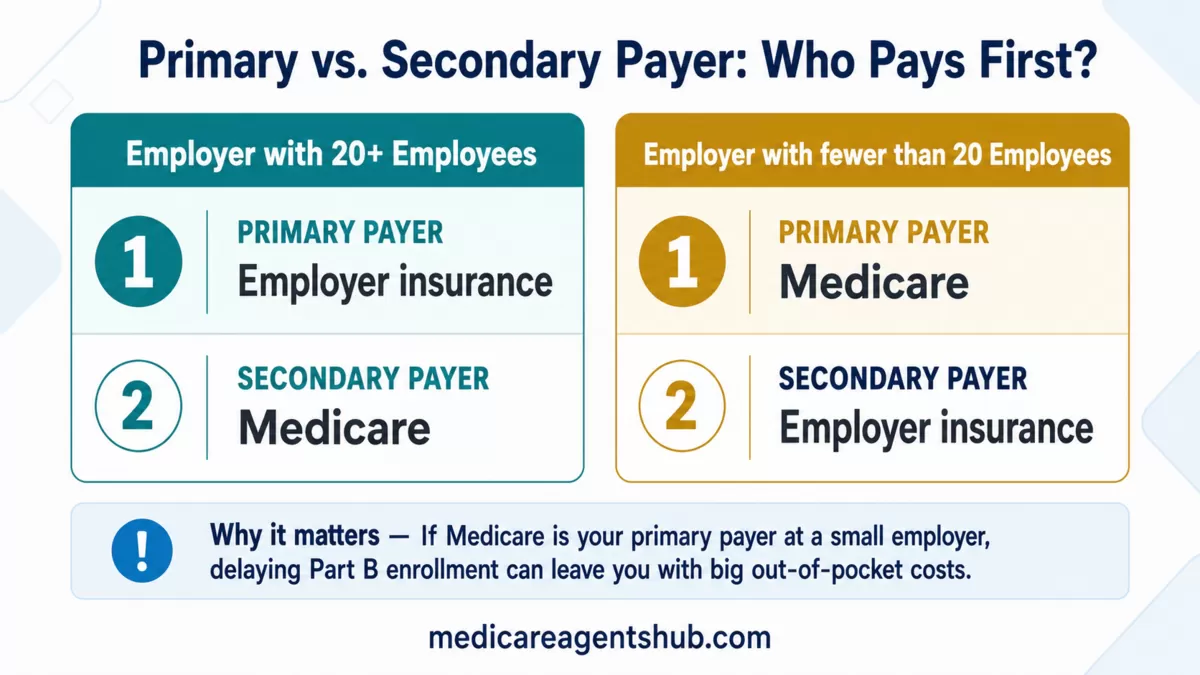

How Medicare works with employer insurance (primary vs. secondary payer)

When you have both Medicare and an employer health plan, one becomes the primary payer and the other pays second. This coordination is what makes it possible to hold both at once without duplicating coverage.

- For companies with 20 or more employees, your employer’s insurance is the primary payer, and Medicare is secondary.

- For companies with fewer than 20 employees, Medicare is the primary payer, and your employer’s insurance is secondary.

Understanding which payer is primary helps manage bills correctly and avoid coverage gaps. If Medicare is your primary payer at a small employer, delaying Part B enrollment can leave you with big out-of-pocket costs, since your employer plan will only pay after Medicare would have.

Should you drop employer insurance and go on Medicare?

Whether it makes sense to drop your employer coverage depends on the numbers. Compare your employer plan’s premiums, deductibles, and network against what you’d pay for Part B plus a Medigap policy or Medicare Advantage plan. Family coverage is a big factor — Medicare only covers you, not your spouse or dependents, so if others rely on your employer plan, dropping it has downstream consequences. When Medicare is the better deal, use your Special Enrollment Period to switch cleanly and avoid penalties.

Can I drop my employer health insurance and switch to Medicare instead?

Yes, you can drop your employer health insurance and switch to Medicare, but whether you should depends entirely on the size of your company and the cost of your current plan.Medicare gives you a Special Enrollment Period (SEP) to make this switch at any time without facing late enrollment penalties, provided your employer coverage is considered "creditable" by the government

Steps to transition from employer health insurance to Medicare

-

Evaluate Your Health Coverage Needs:

- Consider your current health, medication needs, and whether you require additional services like vision or dental coverage, which Original Medicare does not cover.

-

Medicare Parts and Additional Coverage:

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care.

- Part B (Medical Insurance): Covers outpatient care, doctor visits, preventive services, and medical equipment.

- Part D (Prescription Drug Coverage): Optional coverage for prescription drugs, available through private insurance companies.

- Medigap (Supplemental Insurance): Helps cover out-of-pocket costs not covered by Original Medicare.

-

Decide When to Enroll:

- If you qualify for premium-free Part A, enroll as soon as you are eligible.

- For Part B, consider your employer coverage. If it’s creditable (as good as or better than Medicare), you can delay Part B without penalty. Enroll during your SEP if you lose employer coverage. Be aware that a 2026 rule change affects Medigap enrollment timing for people who defer Part B — knowing about it before you retire can save you from a costly surprise.

-

Notify Your Employer:

- Inform your employer’s benefits administrator of your decision to transition to Medicare for proper coordination of benefits.

-

Enroll in Medicare:

- Enroll in Medicare through the Social Security Administration either online, by phone, or in person at your local Social Security office.

I've been on my employer's health plan but am retiring soon. What should I consider when moving to Medicare?

Retiring and moving from employer coverage to Medicare involves several moving parts, and the decisions you make in the first few months can affect your costs and coverage for years to come. The first thing to understand is that when your employer coverage ends due to retirement, you trigger a Special Enrollment Period that gives you eight months to sign up for Medicare Part B without facing a late enrollment penalty, but most people want to coordinate their start dates carefully so there is no gap in coverage. It is also important to know that COBRA does not count as qualifying coverage for purposes of delaying Medicare, so if you are considering COBRA as a bridge you need to be especially careful about how that interacts with your enrollment deadlines. Beyond the enrollment timing, you will want to think about whether Original Medicare with a Medigap policy and a Part D plan makes more sense for your situation, or whether a Medicare Advantage plan is a better fit, and that decision should factor in your doctors, your medications, your expected healthcare usage, and your budget. If your spouse is younger and still working, there may also be options worth exploring around their employer plan depending on how it coordinates with Medicare. People who have had good employer coverage for years are sometimes surprised by what Medicare does and does not cover, so sitting down with a knowledgeable agent before your retirement date rather than after is the smartest move you can make.Costs associated with Medicare

Part A Costs:

- Most people do not pay a premium for Part A if they or their spouse paid Medicare taxes for at least 10 years.

- There’s a Part A deductible per benefit period, with coinsurance amounts that increase the longer you stay in the hospital. Check the current-year Part A costs on Medicare.gov before you plan.

Part B Costs:

- Part B has a standard monthly premium and an annual deductible, after which you typically pay 20% of the Medicare-approved amount for services. Premium amounts change each year — look them up on Medicare.gov for the current year.

- Higher earners pay more under IRMAA (see below).

Part D and Medigap Costs:

- Premiums for Part D and Medigap plans vary based on the plan and provider. Late enrollment in Part D can incur lifelong penalties.

Important considerations

-

Health Savings Accounts (HSAs):

- You cannot contribute to an HSA if you have any part of Medicare. If you or your spouse has an HSA, plan accordingly before enrolling in Medicare.

-

COBRA and Retiree Insurance:

- COBRA is not considered active employer coverage by Medicare. Your 8-month Special Enrollment Period begins when your employment ends, not when your COBRA ends. Staying on COBRA past that window can trigger late enrollment penalties and gaps in coverage — so if you take COBRA, still enroll in Part B on time.

- Some employers offer retiree health insurance, which may work alongside Medicare. Make sure you understand how retiree insurance coordinates with Medicare.

-

IRMAA (Income-Related Monthly Adjustment Amount):

- Higher-income beneficiaries may pay more for Part B and Part D based on their income with this IRMAA fee. Plan for these additional costs.

Conclusion

Switching from employer health insurance to Medicare requires careful planning and understanding of enrollment periods, costs, and coverage options. By evaluating your needs, coordinating benefits, and making good decisions, you can keep your coverage continuous through the transition.

The rules for switching can get complicated. Find a licensed Medicare agent on MedicareAgentsHub.com for personalized, no-cost help with your transition.