10 Medicare Insights from Experienced Agents

-

Last Updated July 25, 2026

Medicare decisions carry real financial consequences, and mistakes can be costly or even irreversible. These 10 insights from experienced Medicare agents cut through the noise and give you practical advice you can act on, whether you're approaching 65 or helping a loved one navigate their options.

- Shop around for options and pricing ahead of time.

- Research past rate increases.

- Consider dual residency and travel plans.

- Evaluate different drug plan options.

- Compare Medigap discounts, from 3% to 14%.

- Take advantage of free preventive screenings.

- Make the most of your Health Savings Account.

- Be prepared for changes and understand what is feasible.

- Timing matters in making Medicare decisions.

- Keep informed to make informed choices.

Options and Prices Can Be Misleading - Early Planning is Key

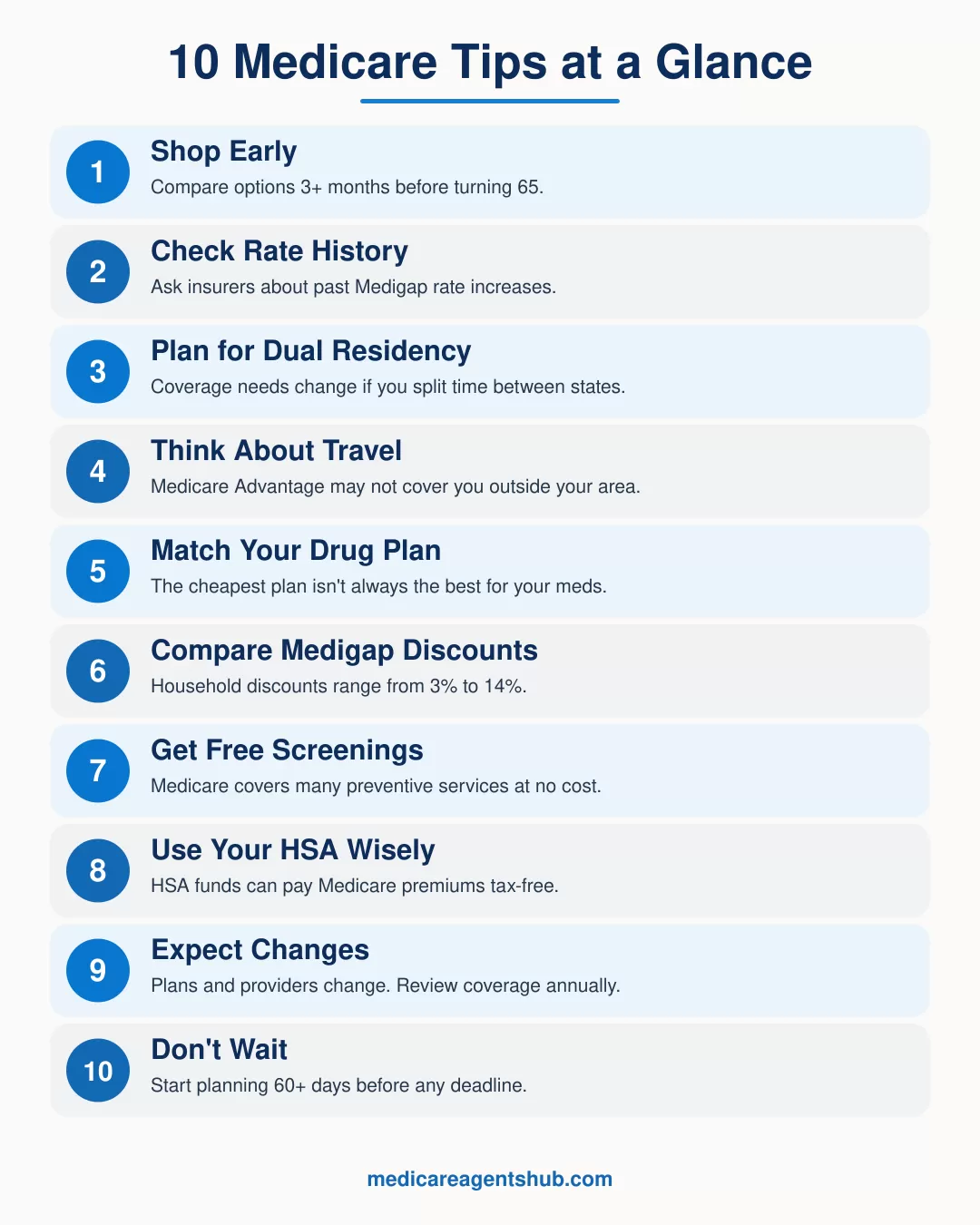

With numerous options available, it can be challenging to understand Medicare. Even if you think you can change plans later, it may not always be possible to get what you want. Understanding Medicare enrollment periods is key. Zero-cost Medicare Advantage plans may have a high deductible, and a long hospital stay may end up costing more than a plan with monthly premiums. Medicare Supplement insurance premiums also vary widely. To avoid confusion and make informed choices, it's important to start planning at least 3 months before turning 65 and to compare options on your own or with help from an expert.

Inquire About the Insurance Company's Rate Increase History

When evaluating Medicare Supplement insurance (Medigap), it's important to consider future rate changes as your rate today may not remain the same. To get a better understanding of this, ask the insurance company two questions: how long have they been offering Medicare Supplement insurance and what is their history of rate increases. A knowledgeable Medicare insurance agent can provide this information, as well as the insurance company's ratings, which indicate their financial strength.

Beyond costs and benefits, should I consider an insurance company’s reputation, values, or social responsibility when choosing a Medicare plan?

Absolutely, but do not solely rely on this. There is one company that has been around since Medicare began, and they are an A+ rated carrier by S&P, but because they do not advertise everywhere, many Medicare beneficiaries haven't heard of them. On the same note, many "Popular" carriers are inconsistent with their rates and have large increases every few years or so.Again, look at carrier ratings, time in the business, financials, and overall performance as determining factors

Consider Dual Residency and Future Moving Plans

Your Medicare decisions can have immediate effects on your healthcare options, especially if you're moving to another state, so it's important to think ahead. Many retirees move after retirement, sometimes to a more cost-effective location or to be closer to family. If you plan to divide your time between two locations, it's important to ensure that your Medicare coverage choices will meet both your current and future needs. Snowbirds and dual residents face unique challenges when it comes to network restrictions and coverage rules. Before making a decision, think about where you might be living 5 years from now and choose coverage that will be suitable for those future circumstances.

I am a resident in another country outside of America, will I still be covered living abroad?

Medicare is a US health insurance program, and in almost all cases, it does notcover you if you live outside of the US. Certain Medigap plans cover emergency foreign travel but typically with monetary financial limits. If your an expat you should purchase international or local health insurance in your country of residence.Consider Travel When Choosing Medicare Insurance

When selecting Medicare insurance, it's important to take future travel plans into consideration. Medicare Advantage plans may have restrictions on coverage outside of the local service area, which can leave you with unexpected bills if you need care while traveling. To fully understand the coverage and limits, ask about specific travel scenarios such as cruises outside US waters and emergency treatment both domestically and abroad. If you travel frequently, a Medicare Supplement plan may offer more flexibility since it works with any provider that accepts Medicare nationwide.

Consider Cost and Prescriptions When Choosing Medicare Drug Plan

The cost of prescription drugs is a significant concern for many seniors, making choosing the right Medicare prescription drug plan important. Many seniors take multiple medications, and cost can impact whether they fill a prescription. Work with a Medicare agent who can use systems to find the best drug plan options based on your current prescriptions, as the cheapest plan may not always be the best option. Be aware of when you can switch plans and start the process early.

I have multiple medications; how can I ensure my Medicare Part D plan covers them all without breaking the bank?

Prescription Drug Plans (PDP) have different formularies that have been approved by Medicare. Since, each plan covers different RX drugs, it's best to go to Medicare.gov to add your prescriptions, then after the system will indicate which PDP Plan best fits your individual needs. Another way is to go to the Plans website and check on their Formulary. The formularies are the list of Medications that are covered with the plan. It entails copays, coinsurance and any deductiblesHousehold Discounts on Medigap Insurance Plans

Medigap Household Discounts can save couples up to $700 per year and can range from 3% to 14%. Actual savings depend on the premium amount, and not all carriers or states offer these discounts. Rules for qualifying also vary. Some require both spouses to be on the same plan, while others simply require that you live at the same address. Check with the insurance company if household discounts are available and what the rules are.

Most Preventive Screenings Are Free with Medicare

Medicare covers a range of preventive screenings, including the "Welcome to Medicare" screening and breast and prostate cancer screenings. Most of these services are fully covered with no deductible or copay when your provider accepts Medicare. Taking advantage of these services can help catch health issues early, when treatment is more effective and less expensive. Check the Medicare website to see the list of covered screenings and take advantage of the "Welcome to Medicare" screening during the first year of eligibility.

Optimize Your Health Savings Account (HSA)

Upon reaching 65, changes in Medicare regulations will alter your HSA eligibility. If you're turning 65 and new to Medicare, here's what to know about the guidelines for withdrawals. The good news is that how you can use the funds actually broadens. You have the opportunity to use HSA funds tax-free and without penalty to pay for Medicare premiums.

Put your Health Savings Account balance to work sooner for the best benefits. As you age into your 70s and beyond, retirement income often drops while medical expenses tend to rise. HSA withdrawals for qualified medical expenses stay tax-free, which can be a meaningful advantage during those higher-spending years.

Can I use a health savings account (HSA) to pay Medicare premiums after I retire?

Yes, you can use HSA funds to pay certain Medicare premiums after you retire. You can use your HSA tax-free for Medicare Part B, Part D, and Medicare Advantage premiums. However, you cannot use HSA funds tax-free for Medigap (Medicare Supplement) premiums. You can also use HSA money for other qualified medical expenses, including deductibles and copays. Keep in mind, once you enroll in Medicare, you can no longer contribute to an HSA, but you can still use the funds.Anticipate Changes, Know Your Options

Reaching Medicare eligibility (age 65) means changes are coming. Health care providers merge, go out of business, and close down. Medicare rules change, and plans that were available last year may no longer be an option for those turning 65.

While it's impossible to plan for every outcome, it's important to work with someone knowledgeable about Medicare rules and options. That's why annual Medicare plan reviews are so valuable.

Medicare rules vary by state, so be sure to consult with someone experienced in your state's rules when changes occur.

Time is of the Essence

Procrastination is not an option with Medicare's hard and fast rules regarding timing. Remember, every day 11,000 Americans turn 65 and there are not enough Medicare insurance agents to assist those waiting until the last minute, especially during the Annual Enrollment Period (AEP).

Start planning at least 60 days in advance of the deadline, and aim to schedule an appointment even earlier.