Everything That Changed in Medicare for 2026

-

Last Updated July 25, 2026

Medicare costs and coverage shift every year, and 2026 brings some of the most significant changes in over a decade. Between the Inflation Reduction Act reshaping prescription drug costs, rising Part B premiums, and major shifts in Medicare Advantage plan offerings, staying informed directly affects what you'll pay and what you'll receive.

Here's what changed for 2026 and what it means for your coverage and your wallet.

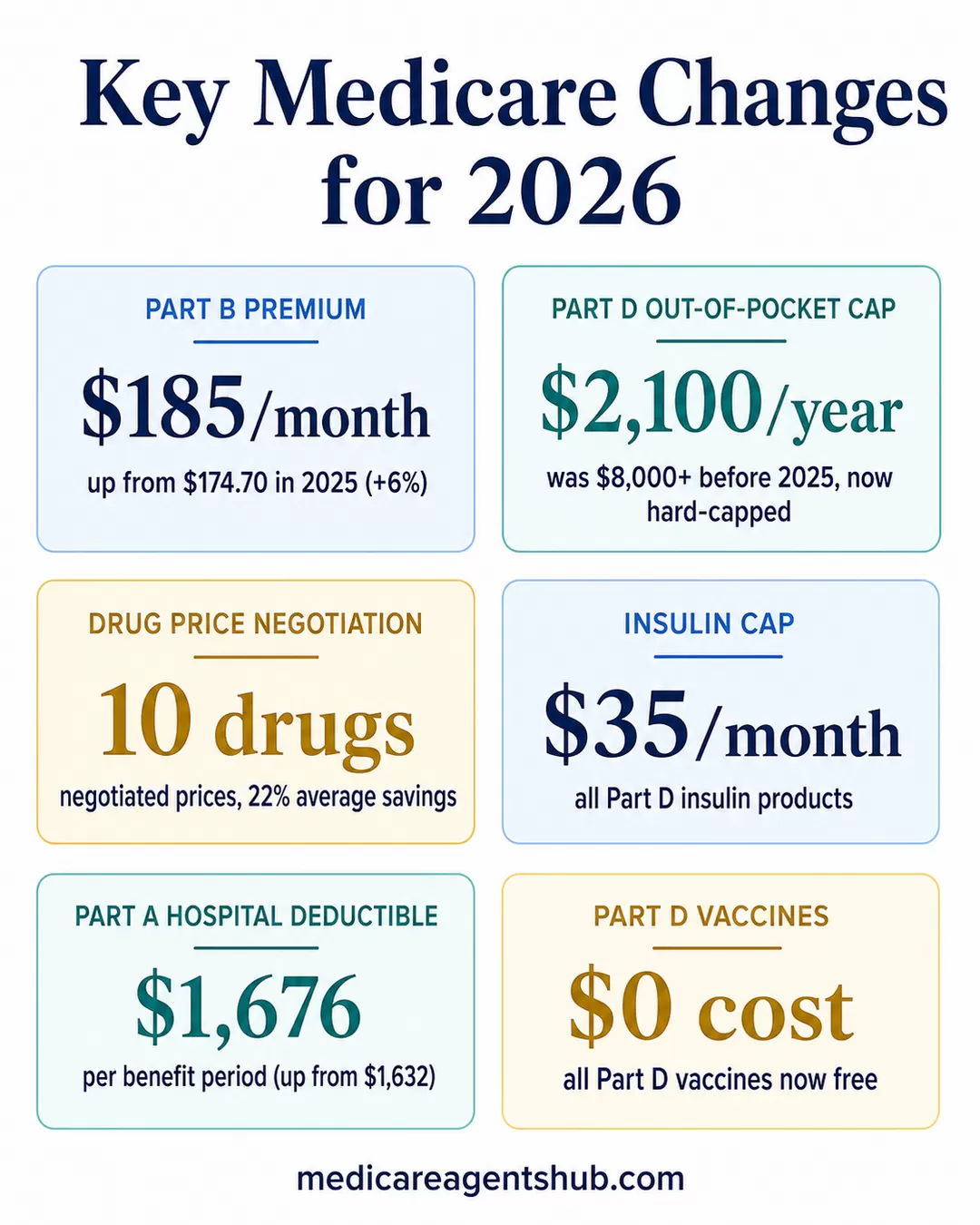

Part B Premium Increase: $185 Per Month in 2026

The standard Medicare Part B premium rose to $185 per month for 2026, up from $174.70 in 2025 (verify current amounts on the official Medicare costs page). That's roughly a 6% increase year over year. The Part B annual deductible also increased to $257, up from $240.

Part B covers outpatient care, doctor visits, preventive services, and medically necessary equipment. Every Medicare beneficiary pays this premium regardless of whether they have Original Medicare or a Medicare Advantage plan.

For higher-income beneficiaries, IRMAA (Income-Related Monthly Adjustment Amount) surcharges still apply on top of the standard premium. If your modified adjusted gross income from two years prior exceeded $106,000 (single) or $212,000 (married filing jointly), you'll pay more. The surcharge tiers range from an additional $74 to $419.30 per month depending on income bracket.

If your income has dropped since the tax year used for your IRMAA calculation (due to retirement, job loss, or other qualifying life events), you can file Form SSA-44 with Social Security to request a reduction. A local Medicare agent can help you determine whether an appeal makes sense for your situation.

Part A Costs: Hospital Deductible and Coinsurance Changes

The Part A inpatient hospital deductible increased to $1,676 per benefit period in 2026, up from $1,632 in 2025. This is the amount you pay before Medicare starts covering your inpatient hospital stay.

Coinsurance for extended hospital stays also changed:

- Days 61-90: $419 per day coinsurance (up from $408)

- Lifetime reserve days (91+): $838 per day (up from $816)

- Skilled nursing facility days 21-100: $209.50 per day (up from $204)

These costs highlight why many beneficiaries pair Original Medicare with a Medicare Supplement (Medigap) plan to cover the gaps in Part A coverage.

The $2,100 Prescription Drug Out-of-Pocket Cap

This is the change that affects the most people. Thanks to the Inflation Reduction Act (IRA), Medicare Part D now has a true annual out-of-pocket spending limit. For 2026, that cap is $2,100 (up slightly from $2,000 in 2025, the first year the cap existed).

Before 2025, there was no real ceiling on Part D drug costs. Beneficiaries taking expensive brand-name medications could spend $8,000 or more per year. The old "donut hole" coverage gap left many people paying high percentages of their drug costs in the middle of the year.

Now, once your out-of-pocket spending on covered Part D drugs hits $2,100 in 2026, you pay $0 for covered prescriptions for the rest of the year. This cap includes your deductible, copays, and coinsurance, but does not include your monthly premium.

The Part D standard deductible for 2026 is $590, the same as 2025. Keep in mind this is the standard set by Medicare — individual plans can offer a lower deductible, and many plans carry a $0 deductible on certain drug tiers (like generics). Check your specific plan's summary of benefits to see how the deductible applies to your medications. After the deductible, you enter the initial coverage phase where you pay copays or coinsurance until reaching the $2,100 cap.

Why is the new $2,000 out-of-pocket maximum for drug costs important?

This is a great question, and one that is commonly asked!Up until 1/1/2025, the out-of-pocket maximum for drug costs was $8,000. That is a *lot* of money to potentially be responsible for paying, should a Medicare beneficiary have to experience the full amount of it in a calendar year.

After the Inflation Reduction Act went in to effect 1/1/25, CMS adjusted that cap to $2000, and that represents a $6,000 potential cost-share savings yearly. Huge, huge relief to many, many Medicare beneficiaries!

With the reduction in cap, the additional amazing news - CMS removed the "coverage gap" or "donut hole" phase in Part D coverage. If you've ever experienced a brand name medication costing quite a bit more during the second half of the year, you know that coverage gap pain firsthand. No more of that, thanks to the Part D changes.

A payment plan is available through Part D insurance companies, where a Part D member can spread their annual costs out over the course of the calendar year, which can really help budget prescription drug plan costs rather than having to pay a significant deductible the first month of the year. You can contact your insurance company to arrange that payment plan.

The cascading effect along all of this has been seen throughout *all* Medicare coverage. Drug companies are reducing the number of listed drugs on their formularies, changing the ones they cover, prescription drug plan premiums are increasing, and multiple insurance companies have chosen not to continue Part D coverage in 2026.

It's *more important than ever* to review your Part D plan annually during Medicare Annual Enrollment Period (AEP) October 15 - December 7, to make sure you know the following:

1. Are your prescription drugs going to be covered on the plan you are in right now?

2. What will they cost?

3. What will your Part D premiums be?

4. Will you Part D plan still exist next year?

The Medicare Prescription Payment Plan

A related IRA provision: the Medicare Prescription Payment Plan lets you spread your out-of-pocket drug costs into predictable monthly installments rather than paying large amounts upfront when you fill expensive prescriptions. This is available through your Part D plan or Medicare Advantage plan with drug coverage.

You can opt into this payment plan at any time during the year. It doesn't reduce what you owe; it just smooths out the payments so you're not hit with a $500 copay in January for a specialty medication.

How will the new 2025 Medicare Part D out-of-pocket cap impact seniors and prescription drug costs?

The new Medicare Part D out-of-pocket cap has been updated for 2026. Once you spend $2,100 out of pocket on covered Part D prescription drugs, you'll pay $0 for covered medications for the rest of the calendar year. This change helps protect seniors with high prescription drug costs and makes expenses more predictable. You may also have the option to spread your prescription costs over the year through the Medicare Prescription Payment Plan.Inflation Reduction Act: Drug Price Negotiation Expands

The IRA gave Medicare the authority to negotiate prices on certain high-cost drugs for the first time (see CMS drug price affordability updates). The first round of negotiated prices took effect in 2026 for 10 drugs that account for some of the highest Medicare spending, including Eliquis, Jardiance, Xarelto, Januvia, Farxiga, Entresto, Enbrel, Imbruvica, Stelara, and insulin products.

CMS reported expected savings of 22% on average across these drugs compared to previous list prices. For individual medications, the negotiated discounts range from roughly 38% to 79% off what Medicare was previously paying.

An additional 15 drugs are slated for price negotiation in 2027, with more added each subsequent year through 2031. If you take any of the drugs on the current or upcoming negotiation lists, your costs at the pharmacy should be noticeably lower.

Insulin costs remain capped at $35 per month for all Medicare beneficiaries with Part D coverage, a cap that first went into effect in 2023 and continues under the IRA.

How will the Inflation Reduction Act's Medicare drug pricing changes really affect seniors?

This is one of the most common questions I’m getting right now, and honestly, the answer is a mix of “we’re already seeing real benefits” and “some parts are still developing.”The biggest win is there’s now a hard cap of $2,100 on your Part D prescription drug costs for the year.

That means once your out-of-pocket costs for covered medications hit that amount, you’re done paying for the rest of the year. For anyone taking higher-cost medications, this is a huge financial protection and peace of mind.

Another clear win is insulin costs are now capped at $35 per month for Medicare beneficiaries. No surprises, no spikes. This has already made a meaningful difference for a lot of people.

You’ve heard that Medicare is now negotiating drug prices. That part is real, but how much it will actually impact most seniors day-to-day still remains to be seen.

The negotiated prices are rolling out gradually and only apply to a very limited number of medications at first. So for now, some people may benefit directly, while others may not notice much change.

The bottom line is that the most important changes are already here. The $2,100 out-of-pocket cap and the $35 insulin cap are the real game changers right now.

The drug price negotiations may bring additional savings over time, but the biggest benefit today is knowing your costs are more predictable and protected than they’ve ever been.

Medicare Advantage: Benefit Reductions and Market Shifts

Medicare Advantage (Part C) enrollment continues to grow. Over half of all Medicare-eligible Americans are now enrolled in an Advantage plan rather than Original Medicare. But 2026 brought a wave of benefit reductions and plan exits across many markets.

Several large insurers scaled back or eliminated supplemental benefits that had become selling points for Advantage plans:

- Dental, vision, and hearing benefits were reduced or capped at lower dollar amounts in many plans

- Gym memberships and wellness perks were dropped from some plan lineups

- Over-the-counter (OTC) allowances were lowered in many markets

- Some plans exited certain counties entirely, forcing beneficiaries to find new coverage

- Grocery and food card benefits largely disappeared after CMS tightened SSBCI eligibility rules, limiting them mostly to Special Needs Plans

These reductions stem largely from CMS rate adjustments and changes to the Medicare Advantage star rating system. Plans that lost star ratings saw reduced bonus payments from CMS, which in turn meant fewer dollars available for supplemental benefits.

If you're on a Medicare Advantage plan, reviewing your Annual Notice of Changes (ANOC) each fall is more important than ever. Benefits, provider networks, and formularies can all shift year to year. Your annual plan review is the best defense against unwanted surprises.

How is Medicare Advantage expected to evolve in the future?

Based on current National trends in 2025-2026, Medicare Advantage plans (Medicare Part C) are reducing or ending many ancillary benefits such as Eyewear & Dental discounts, Gym memberships, cash offers, etc.Extra Help Program: Broader Eligibility Continues

The Extra Help (Low-Income Subsidy) program helps Medicare beneficiaries with limited income and resources pay for Part D prescription drug costs. This includes premiums, deductibles, and copays.

A change that first took effect in 2024 remains in place for 2026: everyone who qualifies for partial Extra Help now automatically receives full Extra Help benefits. Previously, partial Extra Help recipients paid higher copays and faced a coverage gap. Now, all qualifying individuals receive the full level of assistance.

For 2026, copays under the full Extra Help program are approximately $4.50 for generic drugs and $11.20 for brand-name drugs. These amounts are adjusted annually for inflation.

If you're on a fixed income and haven't checked your eligibility, it's worth applying. You can do so through the Social Security Administration or by contacting your state's Medicaid office. A licensed agent who specializes in prescription drug plans can also walk you through the process.

Vaccine Coverage: All Part D Vaccines Now Free

Another IRA-driven change that took effect in 2025 and continues in 2026: all vaccines covered under Part D are now free to Medicare beneficiaries, with $0 cost-sharing. This includes the shingles vaccine, which previously cost many beneficiaries $200 or more out of pocket.

Part B already covered certain vaccines at no cost (flu, pneumonia, COVID-19, Hepatitis B). The Part D change means vaccines like Shingrix (shingles), Tdap (tetanus/diphtheria/pertussis), and others are now available without copays regardless of which Part D plan you're on.

Mental Health Coverage Expansion

Medicare has continued expanding mental health coverage in 2026. Marriage and family therapists and mental health counselors, who became eligible Medicare providers in 2024, are now more widely available in provider networks.

Medicare also covers intensive outpatient programs for mental health and substance use disorders, a change that first took effect in 2024. This fills a gap between standard outpatient therapy and full inpatient hospitalization.

The 190-day lifetime limit on inpatient psychiatric hospital care under Part A remains unchanged. But for most outpatient mental health services, Medicare now covers 80% of the approved amount after you meet your Part B deductible.

How to Stay on Top of Medicare Changes

Medicare adjusts costs, benefits, and rules every year. What worked for your coverage last year might not be the best fit this year. Here's how to stay informed:

- Review your ANOC letter every fall. Your plan is required to send this before the Annual Enrollment Period begins on October 15.

- Check the Medicare Plan Finder at Medicare.gov to compare plans using your specific medications and doctors.

- Work with a licensed Medicare agent who tracks changes across all available plans in your area. Agents are paid by the insurance carriers, not by you, so their guidance comes at no cost. Understanding enrollment periods is especially important, since there are only specific windows when you can make changes.

- Follow updates from CMS at CMS.gov for official policy changes and announcements.

Confused by the 2026 Medicare changes? Get a free plan review.

A licensed Medicare agent can walk through your medications, doctors, and budget to make sure your current plan still fits — or help you find one that does. Their guidance is free; carriers pay their commissions, not you.