How to Enroll in Medicare If You're Not Taking Social Security Yet

-

July 2, 2026

If you're turning 65 and you've decided to hold off on Social Security until 66, 67, or even 70, you might assume Medicare waits with you. It doesn't. Medicare eligibility is tied to your age, not to when you start drawing Social Security benefits. That means the enrollment window opens the same way it would if you were already collecting a check, and missing it can leave you with lifelong penalties.

This guide walks through what changes when you enroll in Medicare without a Social Security check to help pay for it, how to actually sign up, and what to expect on the billing side.

Medicare Eligibility Is Not Tied to Social Security

A lot of people confuse the two programs because Social Security processes Medicare enrollment. But the rules for each are separate. You become eligible for Medicare the month you turn 65 as long as you're a U.S. citizen or a lawful permanent resident who has lived in the country for at least five continuous years. Filing for Social Security has nothing to do with it.

The catch is automatic enrollment. If you're already receiving Social Security or Railroad Retirement Board benefits four months before you turn 65, the government signs you up for Medicare Part A and Part B automatically and mails you a card. If you're not collecting yet, that automatic sign-up doesn't happen. You have to enroll yourself, and if you wait too long, you're on the hook for late enrollment penalties that follow you for the rest of your life.

This is one of the most common tripwires our readers hit. It's also one of the biggest items on the list of mistakes seniors make when enrolling in Medicare, and it's entirely avoidable once you know the rule.

Can you get Medicare without Social Security?

Yes, you can apply for Medicare benefits without starting your Social Security benefits. In that case, you would be responsible for paying your Part B premium directly until you begin collecting Social Security, at which time the premium is typically deducted from your monthly benefit. You would also need to pay a premium for Medicare Part A if you have not earned the required 40 quarters of paying into Social Security through work history.Why People Delay Social Security in the First Place

Delaying Social Security is a smart move for a lot of retirees. Every month you wait past your full retirement age until 70, your future benefit grows by roughly 8 percent per year. Someone who would have collected $2,400 a month at 67 could get around $2,976 by waiting until 70. Over a long retirement, that extra income can add up to six figures.

But that decision creates a mismatch. Your Medicare eligibility hits at 65 while your Social Security check is still years away. The health coverage side of retirement can't wait, so you need to handle enrollment on your own.

Your Initial Enrollment Period Is Still the 7-Month Window Around 65

Your Initial Enrollment Period, or IEP, is a seven-month window: it starts three months before the month you turn 65, includes your birthday month, and runs three months after. This applies to everyone, whether you're collecting Social Security or not.

If you enroll in the three months before your birthday month, your coverage starts the first day of your birthday month. There's one exception: if your birthday falls on the first of the month, your coverage can start the month before you turn 65. Enroll during or after your birthday month, and coverage is delayed. Missing the window entirely usually means waiting for the General Enrollment Period from January through March, with coverage not starting until the month after you sign up, plus a Part B late penalty that raises your premium by 10 percent for every 12 months you were eligible and didn't enroll.

The fix is easy: put the IEP dates on your calendar the moment you decide to delay Social Security. Don't rely on a card showing up in the mail, because it won't. For a deeper look at the timing, our guide to enrolling in Medicare as you're turning 65 covers the sequence step by step.

How to Sign Up for Medicare Without Social Security

You have three ways to enroll. All of them route through the Social Security Administration, since SSA is the enrollment agent for Medicare regardless of whether you're collecting benefits from them.

- Online at ssa.gov. This is the fastest option for most people. Create a My Social Security account, then use the Medicare-only application. You'll be asked to confirm you do not want to start Social Security retirement benefits at the same time. Read that question carefully, because checking the wrong box could trigger a retirement claim you weren't ready to make.

- By phone. Call SSA at 1-800-772-1213. Ask specifically for a Medicare-only application. Expect a hold time and have your Social Security number, date of birth, and employer coverage details ready.

- In person at a local Social Security office. Appointments are required at most locations. This is a good route if your situation is complicated (working past 65, HSA contributions, cross-border residency).

After you apply, you'll get a decision letter and your red, white, and blue Medicare card in the mail. Coverage begins on the date shown on the card.

What About Signing Up for Just Part A?

Some people enrolling without Social Security choose to take only Part A and delay Part B, usually because they still have group health coverage through their own job or a spouse's job based on current employment. Delaying Part B is generally safe when the employer has 20 or more employees. If the employer has fewer than 20, Medicare is typically primary and delaying could leave gaps. COBRA, retiree coverage, Marketplace coverage, and VA-only coverage do not count the same way, so confirm your situation before delaying Part B. Part A is premium-free for most people, so there's rarely a reason to skip it, though there is one exception: if you contribute to an HSA, enrolling in any part of Medicare (including Part A) ends your ability to contribute.

The full breakdown of that decision is covered in our guide to whether you need Medicare if you keep working past 65.

I'm planning to delay Social Security until age 70, but I'm turning 65 soon. How does this affect my Medicare enrollment?

Delaying Social Security until age 70 does not delay your Medicare enrollment — and this is an important distinction that often surprises people.Even if you don’t start Social Security at 65, you are still expected to sign up for Medicare around your 65th birthday. Your Medicare eligibility is based on age, not when you begin collecting Social Security benefits.

Most people should enroll in Medicare Parts A and B during their Initial Enrollment Period, which begins three months before the month you turn 65, includes your birthday month, and continues for three months after. If you delay enrollment without having other qualifying coverage (such as active employer insurance), you could face late enrollment penalties and gaps in coverage.

Part A is usually premium-free if you’ve worked enough years, and many people enroll in it at 65 even if they delay other benefits. Part B has a monthly premium, and delaying it is only recommended if you have other creditable coverage through current employment.

Delaying Social Security simply means your monthly retirement income increases later — it does not change Medicare enrollment rules.

If you’re unsure about timing, it’s a good idea to review your situation carefully, especially if you’re still working or have spousal coverage. A licensed Medicare agent can help you map out the best enrollment strategy so you avoid penalties and stay fully covered.

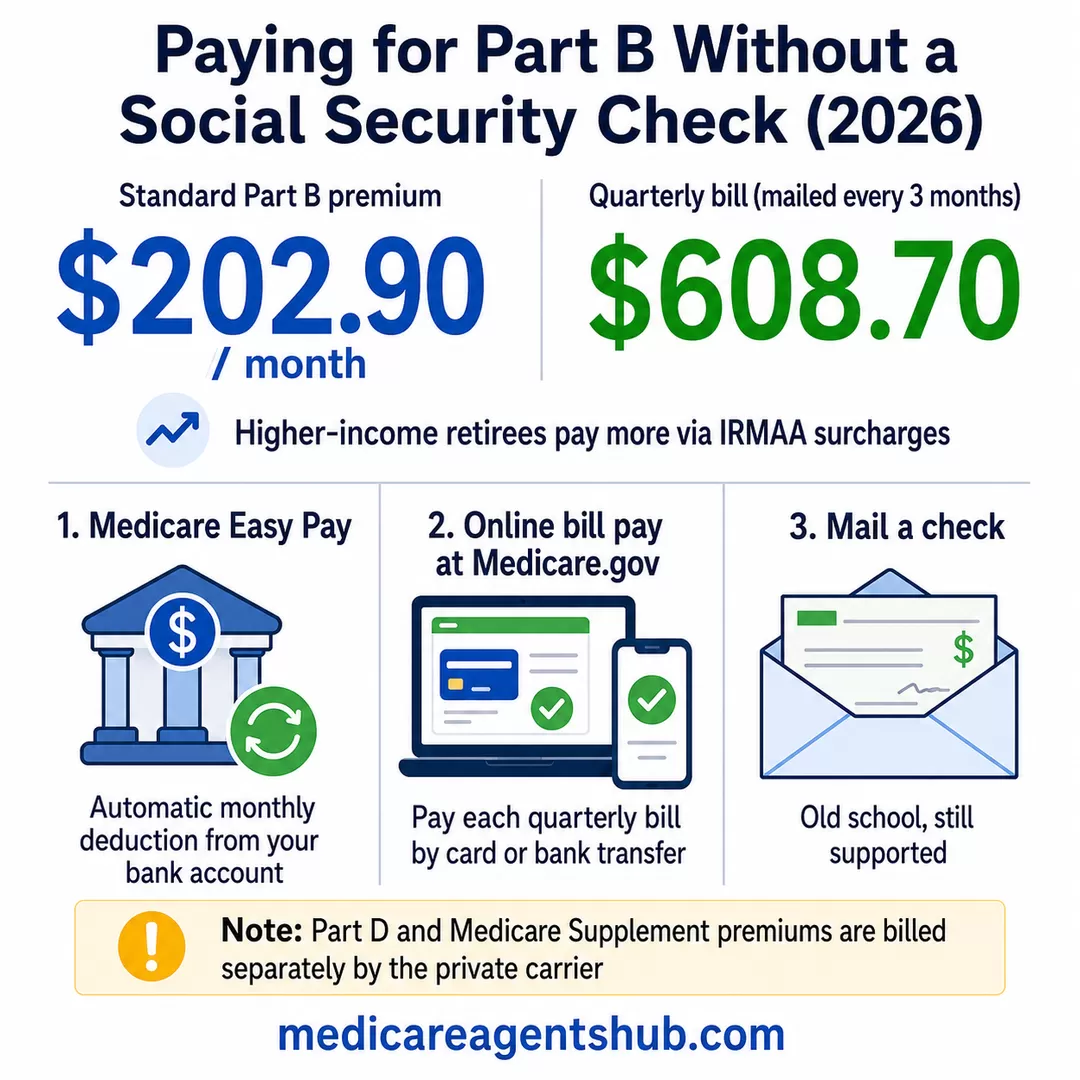

Paying for Part B When There's No Social Security Check

Here's where things look different from someone who's already retired. Normally, Medicare Part B premiums come straight out of your Social Security benefit. If you're not drawing Social Security yet, that isn't an option. Instead, Medicare will bill you directly.

The standard Part B premium for 2026 is $202.90 per month, though higher-income retirees pay more through IRMAA (Income-Related Monthly Adjustment Amount) surcharges. Because SSA can't deduct it from a check, you'll receive a bill through the mail every three months. The quarterly total at the standard rate comes to $608.70. You have a few options for paying it:

- Medicare Easy Pay. Automatic monthly deduction from your bank account. This is the cleanest setup and the one most agents recommend.

- Online bill pay through Medicare.gov. Log in to your account and pay each quarterly bill by card or bank transfer.

- Mail a check. Old school but still supported.

If you also enrolled in a Part D drug plan or a Medicare Supplement, those premiums are billed separately by the private carrier. They don't come through Medicare, and they can't be pulled from a Social Security check either way.

Is my Medicare Part B premium automatically deducted from my Social Security check?

In most cases, yes. If you're receiving Social Security retirement benefits, your Medicare Part B premium is typically deducted automatically from your monthly Social Security check. If you're not yet collecting Social Security, Medicare will usually bill you directly for your Part B premium.You can verify how your premium is being paid by checking your Social Security statement online or reviewing your Medicare premium bill. If you're unsure, a quick review of your Social Security deposit amount will often show whether the premium is already being deducted.

What Happens When You Finally Start Social Security

Once you file for Social Security, the billing setup shifts automatically. SSA will start deducting your Part B premium from your monthly benefit and stop the quarterly Medicare bills. You don't need to cancel Easy Pay yourself. SSA and CMS coordinate the switch on the back end, though it can take one or two billing cycles to fully transition.

If you're also paying Part D premiums, you can request that those be deducted from Social Security too. It's optional. Some people prefer to keep drug plan and Supplement premiums separate from their SSA deposit so they can track them cleanly. Either approach is fine.

One thing to watch: the first year you receive Social Security, your Part B premium may adjust based on the hold-harmless rule and any IRMAA changes tied to your most recent tax return. If your income dropped after retirement, you can appeal an IRMAA surcharge using Form SSA-44, which is covered in detail in our piece on how to beat IRMAA.

What If You Never Paid Enough Into Social Security?

Everything above assumes you'll qualify for premium-free Part A when you enroll. That's based on work history, not on whether you're collecting Social Security. You (or your spouse) need 40 quarters of Medicare-taxed work (roughly ten years) to get Part A at no cost.

If you don't have 40 quarters, you can still buy into Medicare, but Part A comes with a premium. In 2026, that premium runs up to $565 per month for people with fewer than 30 quarters, or $311 for those with 30 to 39 quarters. Part B is priced the same regardless of work history.

This situation comes up more often than you'd think. It affects people who worked mostly overseas, spouses of high earners who never had W-2 employment of their own, and small business owners who under-reported income for decades. In every case, enrolling in Medicare is still worth it. The alternative is going without hospital coverage or trying to find a private plan at Medicare-eligible age, which is expensive and limited.

A Quick Checklist Before You Enroll

Before you file your Medicare-only application, have this ready:

- Your Social Security number and date of birth

- A recent tax return (needed if IRMAA might apply to you)

- Details of any current employer or spouse's employer coverage, including the employer's size

- Bank account info if you want to set up Easy Pay for the Part B premium

- A decision about Part A only vs. Part A and B, based on your current coverage

- Your target Part D and Supplement or Advantage plan choices, if you're pairing enrollment with a plan pickup

When It's Worth Talking to an Agent

Enrolling in Medicare while delaying Social Security is one of those situations where an independent local agent earns their keep. There are moving parts: HSA rules, employer coverage size thresholds, IRMAA planning, Part B vs. Part A timing, and the actual pick of a Part D or Supplement plan. Any one of these can cost you thousands over the next decade if it's handled wrong.

An agent doesn't charge you a fee. They're paid by the carrier when you pick a plan, so getting a second set of eyes on your enrollment strategy is free. If you don't already work with one, you can find a local Medicare agent through our directory, or read our Medicare agent selection guide to know what to look for.

The short version: delaying Social Security is often a smart financial move, but Medicare doesn't wait. Set the calendar, apply during your IEP, plan for the direct Part B bill, and you'll skip the penalties that trip up most people in your situation.