Is IRMAA Permanent? How Medicare Recalculates Your Premiums Each Year

-

July 11, 2026

If Social Security sent you a letter saying your Medicare Part B and Part D premiums are going up because of IRMAA, the first question is usually the same one: is this thing permanent? The short answer is no. IRMAA is recalculated every single year, and for most people it eventually falls off on its own. But there are situations where you can get the surcharge removed earlier than the automatic reset would handle it.

This guide walks through how the recalculation actually works, when you have to wait it out, and when you can file a form to get it corrected sooner.

IRMAA is not permanent. Social Security generally recalculates it every year using tax information from two years earlier. In 2026, for example, SSA generally uses a beneficiary's 2024 tax return. If a later return falls below the applicable threshold, IRMAA normally decreases or ends automatically. Someone whose income dropped because of an approved life-changing event may be able to ask SSA to use newer income information sooner by filing Form SSA-44.

What IRMAA Actually Is

IRMAA stands for the Income-Related Monthly Adjustment Amount. It is not a penalty for late enrollment or a fine for doing something wrong. It is an income-based surcharge added on top of the standard Medicare Part B premium and the Part D premium for higher-income beneficiaries. Roughly the top 7 to 8 percent of Medicare enrollees pay it in any given year.

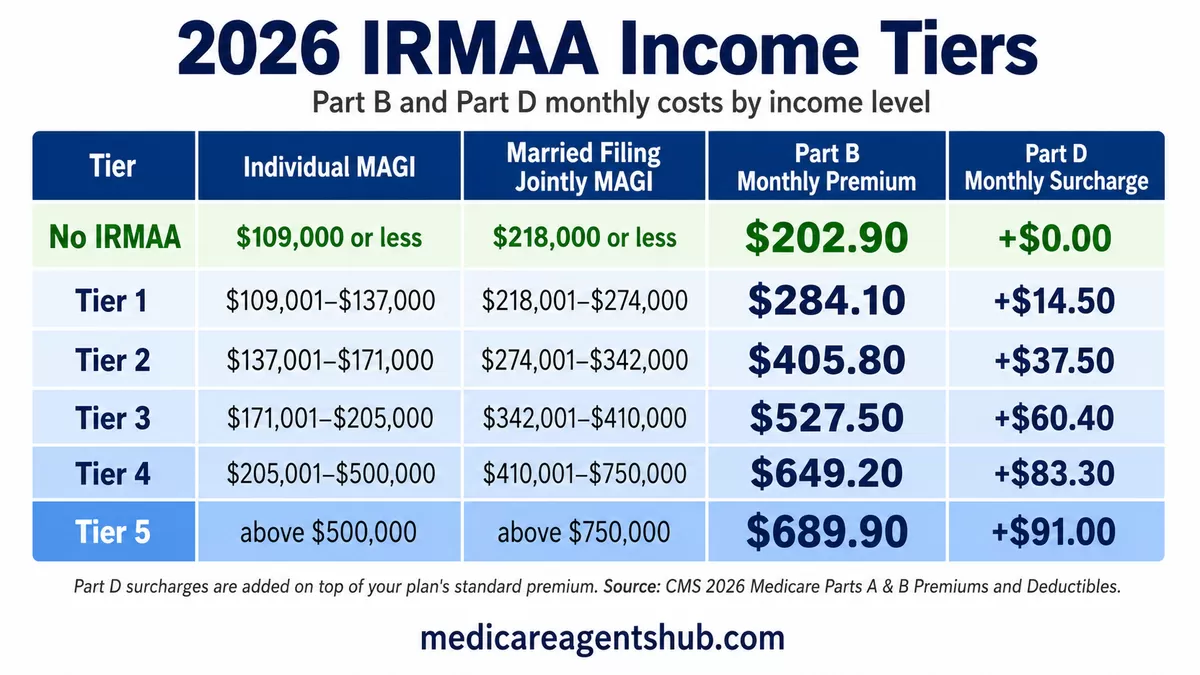

The surcharge is tiered. In 2026, most individual filers with a modified adjusted gross income (MAGI) of $109,000 or less pay no IRMAA. For married couples filing jointly, the no-IRMAA limit is $218,000. Income above those amounts enters the first IRMAA tier, and additional tiers apply as income rises through Tier 5.

2026 IRMAA Tiers at a Glance

| Tier | Individual Filer MAGI | Married Filing Jointly MAGI | Part B Monthly Premium | Part D Monthly Surcharge |

|---|---|---|---|---|

| No IRMAA | $109,000 or less | $218,000 or less | $202.90 | $0.00 |

| Tier 1 | $109,001 – $137,000 | $218,001 – $274,000 | $284.10 | $14.50 |

| Tier 2 | $137,001 – $171,000 | $274,001 – $342,000 | $405.80 | $37.50 |

| Tier 3 | $171,001 – $205,000 | $342,001 – $410,000 | $527.50 | $60.40 |

| Tier 4 | $205,001 – $500,000 | $410,001 – $750,000 | $649.20 | $83.30 |

| Tier 5 | Above $500,000 | Above $750,000 | $689.90 | $91.00 |

Part D surcharges are added on top of your plan's standard premium. Source: CMS 2026 Medicare Parts A & B Premiums and Deductibles.

The key mechanic that trips people up is the two-year look-back. Your 2026 IRMAA is based on your 2024 tax return, filed in 2025. That means the income Social Security is using to price your premium is almost always older than the life you are living now.

The Annual Recalculation, in Plain English

Every fall, the Social Security Administration receives updated tax data from the IRS. It uses that data to reset your IRMAA status for the following year. Nothing you do triggers this. It just happens.

Here is the practical version of the timeline:

- You file your 2024 tax return in early 2025.

- The IRS shares that data with Social Security later in 2025.

- Social Security decides your 2026 IRMAA based on that 2024 return and sends a determination letter in the fall of 2025.

- The new premium starts in January 2026 and stays in place for the full calendar year.

Then the cycle starts over. Your 2027 IRMAA will be based on your 2025 return. Your 2028 IRMAA will be based on your 2026 return. If your income dropped after retirement, that lower income eventually catches up with you, and IRMAA falls off without any paperwork on your part.

Why It Feels Permanent

The gap between when you actually earned the money and when it shows up in your Medicare bill is what makes IRMAA feel permanent. A big one-time event in 2024 (selling a business, cashing out an IRA, capital gains from selling a rental) does not affect your Medicare premium until 2026. And it stays there for all 12 months of 2026, even if your income in 2025 and 2026 is a fraction of what it was during that one taxable event.

Am I responsible for an IRMAA surcharge?

IRMAA is determined by Social Security based on your income from two years ago, so you are only responsible for it if your income was above Medicare’s set limits. For 2026, it generally applies if your 2024 income was over $109,000 filing individually or $218,000 filing jointly.When IRMAA Comes Off Automatically

If nothing else changes, IRMAA drops off the moment your two-year-old tax return no longer shows income above the threshold. This is the most common way people stop paying it.

A typical pattern looks like this. A married couple in their late 60s sold a rental property in 2023 and reported a big capital gain. In 2025 (based on the 2023 return), they landed in IRMAA Tier 2. In 2026, based on their much quieter 2024 return, Social Security recalculated and dropped them back to zero. They did not file any forms. They did not call anyone. Social Security just recalculated and sent a new determination letter in late 2025 confirming the lower premium for 2026.

Retirees who stop working at 65 or 66 are the classic case for the automatic reset. Their first year or two on Medicare often carries IRMAA because their pre-retirement salary is still on the two-year-old return. By years three or four, the recalculation catches up and the surcharge disappears.

When You Need to File Form SSA-44 to Fix It Sooner

You do not have to wait for the two-year look-back if you had a specific life-changing event. Social Security allows you to request an immediate IRMAA reduction using Form SSA-44 when one of these eight qualifying events has happened:

- Marriage

- Divorce or annulment

- Death of a spouse

- Work stoppage (you or your spouse retired or lost a job)

- Work reduction (major cut in hours or income from employment)

- Loss of income-producing property due to a disaster or other event beyond your control

- Loss or reduction of pension income

- Employer settlement payment from a bankrupt or closing employer

A large investment sale, a Roth conversion, or a lump-sum retirement plan distribution does not count as a life-changing event for SSA-44 purposes. Neither does a jump in required minimum distributions. If your high income was voluntary and predictable, you have to wait for the annual recalculation to catch up.

Does IRMAA go away automatically if my income drops, or do I need to report it to Social Security?

The IRMAA is reviewed annually. If the income you reported two years prior is below the IRMAA thresholds, the IRMAA charge will be reduced or removed automatically for the new year.How to Actually File Form SSA-44

The form itself is short, but the supporting documentation is what makes or breaks the request:

- Download Form SSA-44 from ssa.gov or pick it up at your local Social Security office.

- Identify your life-changing event(s) and the date or dates they occurred. Check every applicable event on the form and provide the corresponding dates.

- Estimate your MAGI for the current tax year and, if applicable, the following year. Use realistic numbers.

- Attach proof. A signed statement from an employer confirming retirement, a marriage certificate, a death certificate, or a divorce decree all work depending on the event.

- Submit the form. You can submit Form SSA-44 online through your Social Security account, or send the completed form and evidence by fax or mail. You can also schedule an appointment with a Social Security office if you need help completing the request.

Timing matters. If you had a work stoppage in June and your Medicare premium is already reflecting your pre-retirement income, file the form as soon as you have the paperwork. Social Security can retroactively adjust premiums back to the beginning of the tax year, and any overpayment gets refunded.

The One-Time-Event Trap and How to Time It

Roth conversions, real estate sales, and inherited IRA distributions are the three most common events that push people over an IRMAA threshold for a single year. None of them qualify for SSA-44 relief. But you can still keep the damage to that single year instead of two years, and there are timing strategies worth thinking through.

If a one-time event pushed your 2024 income into IRMAA territory, your 2026 premium is going up. There is no undoing that. What matters is not accidentally repeating the event in 2025, which would extend the surcharge into 2027 as well. Spreading a large Roth conversion across multiple smaller years, for example, can stack you into a lower tier for longer instead of the top tier for one year. Whether that math works depends on your specific tier position and future income projections. It is worth looking at Medicare and tax planning together rather than in isolation.

What If Your Income Drops Between Determinations?

This is the question that trips up almost every new Medicare enrollee. If your income dropped in 2025, but Social Security is still using your 2024 return for your 2026 premium, do you need to tell them?

The answer depends on why the income dropped:

- It dropped because of a qualifying life-changing event (retirement, spouse died, etc.): yes, file Form SSA-44 to get relief sooner.

- It dropped because a one-time income event ended (you sold a property in 2024 and 2025 is normal again): no, you just wait. The 2027 premium (based on your quiet 2025 return) will drop automatically.

- It dropped because of investment losses or a bad year for a business: no form applies here. You wait for the automatic reset.

The rule of thumb: if the drop matches one of the eight life-changing events listed above, you can file. If it does not, the two-year look-back has to run its course.

What Happens if You Miss the Threshold by a Few Dollars

IRMAA is a cliff, not a slope. Cross a threshold by even one dollar and you owe the full monthly surcharge for that tier. For a couple filing jointly, going from $218,000 to $218,001 in MAGI can add hundreds of dollars per month to your combined Part B and Part D premiums.

This is where year-end tax planning matters more for people near a threshold than for anyone else. Depending on eligibility and the advice of a tax professional, strategies such as qualified HSA contributions, qualified charitable distributions from an IRA, and careful timing of capital gains realization may affect the MAGI used for IRMAA. Ordinary itemized charitable deductions generally do not reduce AGI. A good Medicare agent will not do your tax planning, but they will flag when your IRMAA tier is unusually close to a break point so you can talk it through with your CPA before the year ends.

I start Medicare in 2026 and a one-time 401(k) withdrawal in 2024 placed me in the second IRMAA tier for part of that year. When should I file Form SSA-44 so my 2027 premium returns to the lowest tier?

You don't need to file Form SSA-44 because an event like a 401(k) withdrawal or a home sale do not qualify you for a premium reduction. The premium will automatically drop down in 2027 because it's based on the income shown on your 2025 tax return, as long as it's below the IRMAA thresholds.The bottom line is that you don't have to do anything for the 2027 premium reduction.

Appealing an IRMAA Determination

Life-changing events aside, you may also be able to get an IRMAA determination corrected if Social Security is using incorrect income data. This most often happens when:

- The IRS provided outdated or amended tax data

- You filed an amended return that lowered your MAGI

- You have documentation that shows the reported income is wrong

If Social Security used incorrect, outdated, or subsequently amended tax information, contact SSA and ask whether it can make a new initial determination using the corrected information. If you formally disagree with the resulting IRMAA determination, you can request reconsideration, including through Form SSA-561. For a broader walkthrough of contesting a surcharge, our guide on appealing IRMAA premium increases covers the process and what to expect from Social Security.

Common Situations Where IRMAA Feels Unfair

Some situations feel especially punitive because the person did not choose to have high income:

- You got married after 65 and your spouse's income lifted your combined MAGI into a joint IRMAA tier. Our article on how marriage after 65 spikes Medicare premiums walks through why filing jointly can trigger this and what you can do.

- You inherited an IRA and the required distributions bumped your MAGI. This is not a qualifying life event for SSA-44. See how an inherited IRA can raise Medicare premiums for the mechanics.

- Your spouse died and the surviving-spouse tax filing status changed how income is measured. This is a qualifying life event and SSA-44 applies.

Quick Answers to the Questions People Actually Ask

Is IRMAA permanent? No. It is recalculated every year using your tax return from two years earlier.

Will IRMAA go away automatically? Yes, if your income dropped and you had no qualifying life-changing event, it drops off automatically once the two-year look-back catches up.

Can I get IRMAA removed sooner? Yes, but only if you experienced one of eight specific life-changing events (retirement, marriage, divorce, spouse's death, work reduction, loss of income-producing property, loss of pension, or employer settlement payment). File Form SSA-44.

Does IRMAA get refunded if it drops off mid-year? Only when you file SSA-44 for a qualifying event and Social Security applies the reduction retroactively to the start of the year. Normal annual recalculations take effect January 1 without a refund for prior years.

How much can IRMAA cost me? For 2026, the highest tier adds $487.00 per month to Part B alone, plus $91.00 for Part D. Multiplied over 12 months, an unexpected IRMAA year can cost a couple well over $10,000.

Bottom Line

IRMAA is annoying and expensive, but it is not permanent. If the high income occurred in only one tax year, the surcharge generally lasts for the corresponding premium year and then drops once a later, lower-income tax return becomes the applicable lookback year. For people whose income dropped because of retirement, marriage, divorce, or the death of a spouse, Form SSA-44 shortens that wait dramatically. And for people who see themselves brushing against a threshold, the smart move is to talk to both a tax professional and a Medicare advisor who has helped clients understand IRMAA notices and prepare for conversations with Social Security and their tax professional so the timing of income events lines up with the tier breakpoints.

If you are trying to figure out whether your specific situation qualifies for SSA-44 relief or when your automatic reset will kick in, a licensed independent Medicare agent can walk you through the paperwork and coordinate with your tax preparer at no cost to you.