Can You Lower Your Medicare Costs With Smart Tax Planning?

-

January 5, 2026

Short answer: yes, sometimes.

Longer answer: it depends on your income, how that income is reported on your tax return, and whether you plan ahead or let Medicare costs happen to you by surprise.

Many people assume Medicare costs are fixed. You pay Part B, maybe a Part D plan, and that is that. But for millions of beneficiaries, taxable income directly affects Medicare premiums, sometimes by thousands of dollars a year. Understanding that connection puts you back in control.

Let’s break it down in plain English.

Why Taxes Matter More Than You Think With Medicare

Medicare bases some of its costs on your Modified Adjusted Gross Income, or MAGI. This number comes straight from your federal tax return.

If your MAGI crosses certain thresholds, you may pay an Income-Related Monthly Adjustment Amount, better known as IRMAA. This is a surcharge added to:

-

Medicare Part B premiums

-

Medicare Part D premiums

IRMAA does not affect Part A.

Am I responsible for an IRMAA surcharge?

Possibly — IRMAA is an extra surcharge on Medicare Part B and Part D if your income is above certain limits. Medicare looks at your tax return from two years ago to determine this.You’ll get a letter from Social Security if IRMAA applies to you, and it will show the amount. If your income has gone down due to something like retirement, you can usually appeal it.

Here’s the part that catches people off guard: Medicare looks at your income from two years ago, not last year or this year. Your 2026 premiums are based on your 2024 tax return.

That means a financial decision you already made can quietly raise your Medicare costs today.

What Triggers Higher Medicare Premiums?

You do not need to be ultra-wealthy to get hit with IRMAA. For 2026, IRMAA begins when MAGI exceeds:

-

$109,000 for individuals

Go just one dollar over, and the surcharge applies.

Common triggers include:

-

Required Minimum Distributions from retirement accounts

-

Capital gains from selling investments

-

Selling a home or business

-

Roth IRA conversions

-

One-time income events like bonuses or large withdrawals

These are normal financial moves — and some you don't even choose, like inheriting an IRA and being required to take taxable distributions. The problem is when they happen without considering Medicare.

Smart Tax Planning Can Reduce or Avoid IRMAA

This is where strategy comes in. Smart tax planning is not about dodging taxes. It is about managing when and how income shows up. For a deeper look at the income game retirees face with IRMAA, see our guide on how to beat IRMAA with smarter income strategies.

Here are some proven ways people reduce Medicare-related costs.

1. Control the Timing of Income

Because Medicare looks back two years, timing matters. Spreading income over multiple years can keep you under IRMAA thresholds.

Examples include:

-

Taking smaller retirement withdrawals over time

-

Spacing out Roth conversions instead of doing one large conversion

-

Planning asset sales across tax years

This approach helps smooth income instead of creating spikes that trigger higher premiums.

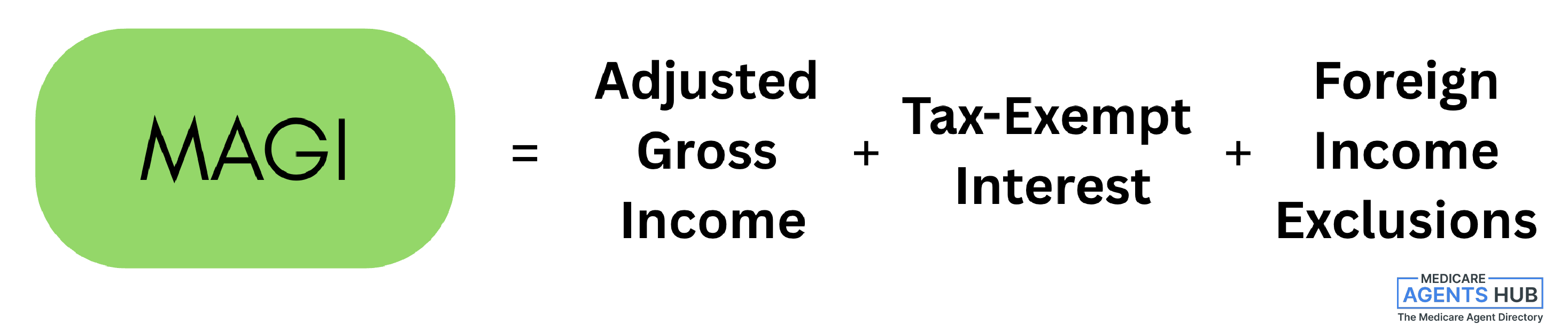

2. Understand How MAGI Is Calculated

MAGI is not just your paycheck. It includes:

-

Adjusted Gross Income

-

Tax-exempt interest

-

Certain foreign income exclusions

Some income sources feel “invisible” but still count for Medicare. Knowing what feeds into MAGI helps you make better decisions before tax season arrives.

3. Use Roth Accounts Strategically

Withdrawals from Roth IRAs do not count toward MAGI when taken correctly. That can make Roth funds valuable for covering expenses without increasing Medicare premiums.

This does not mean Roth accounts are always the answer, but when used intentionally, they can help manage taxable income in retirement.

4. Appeal IRMAA After Life Changes

Not all income increases are permanent. Medicare allows appeals when you experience a life-changing event, such as:

-

Retirement or reduced work hours

-

Divorce

-

Loss of income-producing property

You can file Form SSA-44 and request that Medicare re-evaluate your premiums based on current income instead of past earnings.

Many people qualify for relief and never realize it.

Medicare Planning Is Not Just a Tax Issue

Tax planning affects Medicare, but Medicare choices also affect your overall costs.

Plan selection, drug coverage, and enrollment timing all matter. This is where working with a knowledgeable local Medicare agent in your state can help. A local agent understands regional plan options and can coordinate with your tax or retirement strategy so one decision does not accidentally raise costs elsewhere.

The goal is alignment, not guesswork.

What Smart Planning Really Looks Like

Smart Medicare tax planning is not about chasing loopholes. It is about:

-

Knowing your income thresholds

-

Avoiding unnecessary income spikes

-

Planning withdrawals intentionally

Even small adjustments can prevent large premium increases.

And because rules and thresholds change over time, reviewing your situation annually matters. A local Medicare agent who works with beneficiaries year after year can help spot issues early, before they turn into expensive surprises.

The Bottom Line

Yes, you can lower your Medicare costs with smart tax planning, but only if you understand how taxes and Medicare interact.

Medicare premiums are not just about age or enrollment. They are tied directly to income decisions you make, often years earlier. With a little foresight and the right guidance, many beneficiaries avoid overpaying and keep more of their retirement income where it belongs.

If you are approaching Medicare or already enrolled, now is the time to look beyond premiums and start looking at the tax picture behind them.