Can an Inherited IRA Increase Your Medicare Premiums?

-

March 28, 2026

You inherited an IRA from a parent or spouse. You took a distribution, paid the taxes, and moved on. Then, a year or two later, Social Security sends a letter saying your Medicare Part B premium just doubled. What happened?

The short answer: that IRA distribution counted as taxable income, and Medicare uses your income from two years ago to set your premiums. If the distribution pushed your income past certain thresholds, you got hit with IRMAA, the Income-Related Monthly Adjustment Amount. It's a surcharge on top of your standard Part B and Part D premiums, and it catches a lot of people completely off guard.

Why Medicare Looks at Your Tax Return, Not Your Bank Account

Medicare doesn't care how much money you have in savings, investments, or even how much your home is worth. What it cares about is your Modified Adjusted Gross Income (MAGI), which comes straight from your federal tax return.

MAGI includes wages, Social Security benefits, pension income, capital gains, rental income, and yes, distributions from traditional IRAs and inherited IRAs. It also adds back in any tax-exempt interest income (like from municipal bonds). If your MAGI crosses specific income thresholds, Medicare tacks on IRMAA surcharges to both your Part B and Part D premiums.

Here's the part that trips people up: Medicare doesn't use this year's income. It uses your tax return from two years prior. So your 2024 income determines your 2026 premiums. Your 2025 income determines your 2027 premiums. This two-year lookback is baked into the system, and there's no way around it.

For a full breakdown of how your income affects what you pay, take a look at what determines your Medicare costs and how to reduce them.

When an Inherited IRA Distribution Triggers IRMAA

Inheriting money, by itself, is not a taxable event. If someone leaves you a house, a bank account, or a life insurance payout, none of that shows up as income on your tax return. But an inherited traditional IRA is different. The money in that account has never been taxed. When you take a distribution, the IRS treats it as ordinary income, just like a paycheck.

That distribution gets added to everything else you earned that year. Social Security benefits, pension payments, any part-time work, investment income. All of it rolls into your MAGI. And if the total crosses one of the IRMAA thresholds, your Medicare premiums go up.

The 2026 IRMAA brackets for individuals start at $109,000 in MAGI (based on the 2024 tax return). For married couples filing jointly, the first threshold is $218,000. Go above those numbers and you'll pay anywhere from about $70 to over $400 extra per month for Part B alone, depending on how far over you land. Part D gets its own surcharge on top of that.

A few things worth knowing about inherited IRAs specifically:

- Non-spouse beneficiaries generally must empty the account within 10 years of the original owner's death (under the SECURE Act rules). Some are also required to take annual distributions during that window, depending on whether the original owner had already started taking Required Minimum Distributions.

- Spousal beneficiaries have more flexibility. They can roll the inherited IRA into their own IRA and treat it as their own, which lets them delay distributions until their own RMDs kick in.

- Inherited Roth IRAs are a different story. Qualified distributions from a Roth IRA don't count as taxable income, so they won't affect your MAGI or trigger IRMAA. The 10-year rule still applies for non-spouse beneficiaries, but the tax impact is zero.

Do IRA or 401(k) withdrawals increase Medicare costs?

Yes. Withdrawals from traditional IRA or 401(k) accounts count as taxable income, which can increase your Medicare premiums through IRMAA.Medicare looks at your income from 2 years prior, so even a large one-time withdrawal can raise your Part B and Part D costs for a year.

Note: Roth IRA withdrawals (if qualified) typically don’t count toward Medicare income.

The Two-Year Delay That Catches People Off Guard

This is where the real frustration lives. You take an inherited IRA distribution in 2024, pay the income taxes on it that spring, and assume you're done. But Medicare is working on a different timeline.

In late 2025, Social Security reviews your 2024 tax return. If your MAGI crossed an IRMAA threshold, they send you a letter, usually around November or December, telling you that your 2026 Medicare premiums are going up. By the time you get that letter, the distribution happened almost two years ago. The money is long spent. And now you're paying higher premiums for the next 12 months.

Here's a concrete example:

Margaret, age 72, single filer

Normal annual income: $85,000 (Social Security + pension + small RMDs)

In 2024, she takes a $45,000 distribution from an IRA inherited from her late mother.

Her 2024 MAGI jumps to ~$130,000, pushing her into the first IRMAA surcharge tier.

Result: In 2026, her Part B premium increases by roughly $70/month and her Part D premium goes up by about $13/month. That's almost $1,000 in extra Medicare costs for the year.

By 2027, assuming her income returns to normal, her premiums drop back down automatically.

The good news is that IRMAA resets every year. If the inherited IRA distribution was a one-time event and your income drops back below the threshold the following year, your premiums should return to normal. But that one high-income year still costs you a full 12 months of higher premiums, and there's no refund.

If you've been blindsided by a sudden premium increase and aren't sure why, this breakdown of how IRMAA works and strategies to fight back covers the mechanics in more detail.

Can SSA-44 Help After an Inherited IRA Distribution?

You may have heard about appealing IRMAA using Form SSA-44. It's a real option, but it doesn't apply to every situation, and this is where inherited IRAs get tricky.

Form SSA-44 lets you ask Social Security to use a more recent (lower) income year instead of the two-year-old tax return they'd normally rely on. But there's a catch: you can only file it if you've experienced a qualifying life-changing event. The list is specific:

- Marriage or divorce

- Death of a spouse

- Work stoppage or reduction

- Loss of income-producing property

- Loss of pension income

- Employer settlement payment

Notice what's not on that list: receiving an inheritance. Taking a one-time distribution from an inherited IRA is not, by itself, considered a qualifying life-changing event. So if your income spiked solely because of an inherited IRA distribution and nothing else changed, SSA-44 probably won't help you.

There is an important exception, though. If you inherited the IRA because your spouse passed away, the death of a spouse is a qualifying event. In that case, you could file SSA-44 and ask Social Security to use your current-year income instead. This is especially relevant because losing a spouse also changes your tax filing status from married filing jointly to single, which has lower IRMAA thresholds. You could get hit twice: once from the distribution income and once from the filing status change.

I start Medicare in 2026 and a one-time 401(k) withdrawal in 2024 placed me in the second IRMAA tier for part of that year. When should I file Form SSA-44 so my 2027 premium returns to the lowest tier?

Form SSA-44 is used to request a reduction in your IRMAA if you experience a "life-changing event" that significantly reduces your income (such as retirement, marriage, divorce, or loss of income-producing property). A one-time 401(k) withdrawal is not typically considered a qualifying life-changing event by itself, unless it is directly tied to retirement or work stoppage.If your income in 2025 returns to the lowest tier and there is no qualifying life-changing event after 2024, you generally do not need to file Form SSA-44. Your IRMAA should automatically adjust in 2027 when the Social Security Administration reviews your 2025 tax return.

However, if you retire or have another qualifying life-changing event in 2025 that further reduces your income, and you want your 2027 IRMAA to reflect that change sooner, you can file Form SSA-44 after the event occurs and you have documentation (such as a final pay stub or retirement letter). This allows Social Security to adjust your premiums based on your current lower income, rather than waiting for the next tax return review.

The bottom line on SSA-44: don't assume you can appeal just because the income spike was temporary. The form is designed for life changes, not income fluctuations. If you're not sure whether your situation qualifies, talk to a Medicare agent or contact your local Social Security office before the premium increase takes effect.

How to Plan Distributions Around IRMAA Brackets

If you know an inherited IRA distribution is coming, or if you have the flexibility to control the timing and size of your distributions, some advance planning can save you real money on Medicare premiums.

This section covers general planning concepts, not personalized tax or Medicare advice. Everyone's situation is different. Work with a qualified tax professional and a licensed Medicare agent before making financial decisions based on anything you read here.

Spread distributions across multiple years. This is the single most effective strategy. Instead of taking one large lump sum, break it into smaller annual distributions that keep your MAGI below the nearest IRMAA threshold. Even staying one dollar under the line makes a difference. For non-spouse beneficiaries under the 10-year rule, you have a full decade to empty the account. Use that runway.

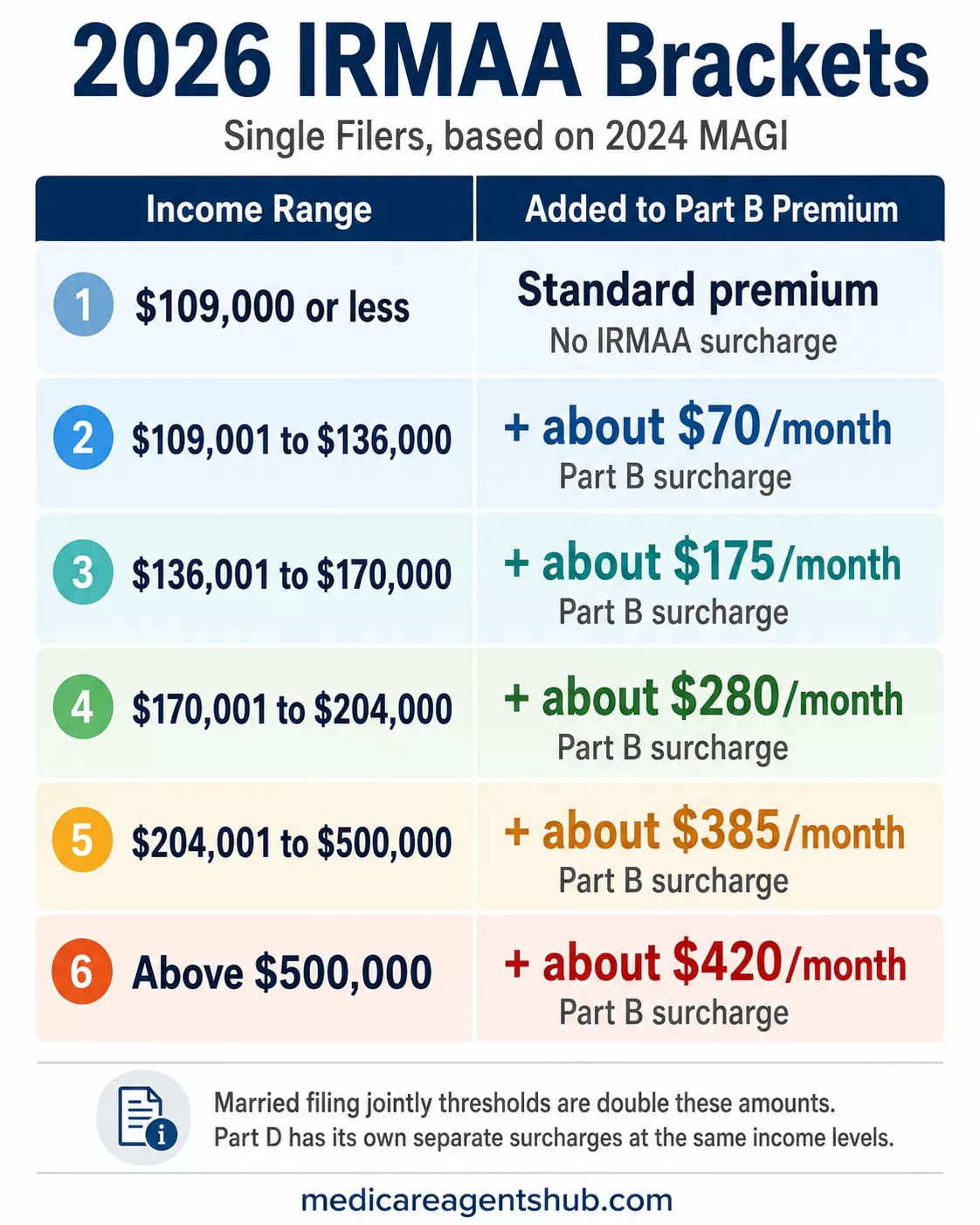

Know exactly where the IRMAA brackets are. For 2026 (based on 2024 income), the thresholds for single filers are roughly:

- $109,000 or less — Standard premium (no IRMAA)

- $109,001 – $136,000 — ~$70/month surcharge on Part B

- $136,001 – $170,000 — ~$175/month surcharge on Part B

- $170,001 – $204,000 — ~$280/month surcharge on Part B

- $204,001 – $500,000 — ~$385/month surcharge on Part B

- Above $500,000 — ~$420/month surcharge on Part B

Married filing jointly thresholds are double these amounts. Part D has its own separate surcharges at the same income levels. These brackets are adjusted periodically, so verify the current numbers with the Social Security Administration's IRMAA page before making decisions.

Time distributions strategically. If you're turning 65 and starting Medicare, think carefully about when you take inherited IRA distributions relative to your enrollment year. A large distribution taken two years before you start Medicare will affect your premiums right out of the gate.

Be careful with Roth conversion advice. A surviving spouse may have options to roll an inherited IRA into their own IRA and then consider Roth conversion planning before Medicare age. But non-spouse beneficiaries generally cannot convert an inherited IRA directly to a Roth IRA. They may still be able to manage taxable income by spreading inherited IRA distributions across the 10-year window, coordinating withdrawals with other income, and working with a tax professional to find the most efficient schedule.

Offset distribution income when possible. Charitable contributions, qualified charitable distributions (QCDs) from your own IRA if you're over 70½, and other deductions can help bring your MAGI back down in years when you need to take a larger inherited IRA distribution.

For more on how tax planning and Medicare costs interact, see how smart tax planning can lower your Medicare costs.

How can I avoid or reduce IRMAA charges on my Medicare premiums?

Yeah, IRMAA can be a surprise hit to your Medicare premiums if your income’s above a certain level. But there are a few ways to either avoid it or bring it down.First, it all comes down to your income from two years ago, so if you can keep your taxable income under those limits, you’re golden. You can use Roth IRAs or Roth 401(k)s because money from those dont count toward your income, so it helps keep you under the radar. And if you’re taking money from traditional retirement accounts, you could think about converting some to Roth early on (before Medicare kicks in) to lower your future tax hits.

Also, if you’ve had a big life change like retirement, loss of a spouse, or a drop in income—you can actually appeal your IRMAA charge. You just fill out a form (SSA-44) and explain your situation.

Keep in mind the sale of a home with capital gains income can affect your IRMAA as well which could throw you into a higher income level.

Bottom line: it’s all about planning ahead. If you’re getting close to retirement or Medicare age, it’s worth sitting down with a tax or financial advisor and figuring out what moves you can make now to avoid that extra premium later.

What to Ask Your Medicare Agent and Tax Professional

Inherited IRAs sit at the intersection of tax law, estate rules, and Medicare pricing. No single professional covers all of it, so you'll likely need both a tax advisor and a Medicare-savvy insurance agent working in coordination. Here's what to bring up with each.

Questions for your tax professional

- What's the most tax-efficient way to distribute this inherited IRA over the 10-year window?

- How much can I take this year without crossing an IRMAA threshold?

- Are Roth conversions an option in my specific situation, or do beneficiary rules prevent it?

- Are there deductions or offsets I can use to counterbalance a large distribution year?

- How does my filing status (single vs. married filing jointly) affect the IRMAA thresholds I need to watch?

Questions for your Medicare agent

- Based on my projected income, should I expect IRMAA surcharges on my Part B and Part D premiums next year?

- If I'm already paying IRMAA, does my plan choice (Medicare Advantage vs. Original Medicare) affect the total surcharge amount?

- Does filing SSA-44 make sense in my situation, or should I just wait for IRMAA to reset?

- Are there savings programs I should look into while I'm paying higher premiums?

Having these conversations before you take the distribution is always better than trying to fix it after. But even if you've already been hit with IRMAA, understanding your options can help you manage costs going forward and avoid repeating the mistake in future distribution years.

Frequently Asked Questions

Does inheriting an IRA automatically increase Medicare premiums?

No. The inheritance itself does not affect your Medicare premiums. What matters is whether you take taxable distributions from a traditional inherited IRA. Those distributions count as income, and if your total income crosses IRMAA thresholds, your premiums go up two years later.

Can I appeal IRMAA if the IRA distribution was a one-time event?

Usually not. Form SSA-44 requires a qualifying life-changing event like the death of a spouse, marriage, divorce, or work stoppage. A temporary income spike from an IRA distribution alone does not qualify. The exception is if you inherited the IRA because your spouse died, which is itself a qualifying event.

Do inherited Roth IRA distributions affect IRMAA?

Qualified distributions from an inherited Roth IRA generally do not count toward your MAGI, so they won't trigger IRMAA surcharges. This is one of the key tax advantages of inheriting a Roth IRA versus a traditional IRA.

The Bottom Line

An inherited IRA distribution is taxable income, and taxable income is what Medicare uses to calculate your premiums. Take a large enough distribution and your Part B and Part D costs can jump significantly, starting two years after the fact. The increase is temporary if the distribution was a one-time event, but SSA-44 won't bail you out unless you also experienced a qualifying life change like losing a spouse.

The best defense is planning ahead. Spread distributions over multiple years, know where the IRMAA brackets fall, and coordinate with both a tax professional and a Medicare agent before making big moves. The money you save on premiums could easily run into thousands of dollars.