Your Medicare Bill Explained: What Determines Costs and How to Reduce Them

-

November 16, 2025

Understanding your Medicare bill can feel overwhelming, whether you are preparing to enroll soon or you already have coverage. Medicare is designed to make healthcare more affordable for older adults and certain individuals with disabilities, but it still comes with monthly premiums, deductibles, copays, and out of pocket costs that can vary widely depending on the coverage you choose.

This guide breaks down what determines the cost of your Medicare bill and what steps you can take to reduce those costs. The goal is to give both new and current beneficiaries a simple, accurate overview that helps you feel more confident about your healthcare expenses.

What Determines the Cost of Your Medicare Bill

Your Medicare costs are shaped by several factors. Some are standard for everyone, while others depend on personal income, the type of coverage you select, and how often you use healthcare services.

1. Your Medicare Part A and Part B Premiums

Most people do not pay a monthly premium for Medicare Part A because they earned it through payroll taxes during their working years. If you or your spouse did not pay into Medicare long enough, you may have a Part A premium which can vary based on your work history.

Medicare Part B always has a monthly premium. The amount is set by the federal government and can change each year. Most beneficiaries pay the standard premium, although higher income beneficiaries may pay more through the Income Related Monthly Adjustment Amount known as IRMAA. IRMAA is applied when your income exceeds specific thresholds based on your tax return from two years earlier.

2. Whether You Choose Original Medicare or Medicare Advantage

Your Medicare costs are also affected by the type of plan you have.

Original Medicare (Parts A and B)

You pay premiums for Part B, plus deductibles and coinsurance when you use services. Many people add a Part D prescription drug plan and sometimes a Medigap plan to reduce out of pocket costs.

Medicare Advantage (Part C)

Medicare Advantage plans combine your Part A, Part B, and often Part D coverage into a single plan offered by a private insurer. Some plans have low or even zero dollar premiums, but you will still owe your standard Part B premium. Your bill may include additional costs depending on the plan, such as copays for visits, prescriptions, and diagnostic services.

Choosing between Original Medicare and Medicare Advantage can significantly affect how predictable your costs feel throughout the year.

As a senior, what should I know about the differences between Original Medicare and Medicare Advantage before I choose?

As an Agent, I try to remain neutral as to my own preferences between Original Medicare and Medicare Advantage. That said, there are some critical details which really need to be shared.Network:

Original Medicare has Medicare's largest network... comprising around 98% of doctors and hospitals in the nation. Some of the Top Tier providers, like Mayo, John C Hopkins, Scripts... and a growing number of others do NOT accept Medicare Advantage plans.

Approval:

For some time now, Medicare Advantage plans have been developing a reputation (a bit behind the scenes) for NOT approving procedures and surgeries. Your doctor submits an approval request... and a large number of those requests are being denied ("In 2023, insurers fully or partially denied 3.2 million prior authorization requests...").

A friend's (and fellow agent's) mom started into Medicare with an Advantage plan. Her doctor's requests for an MRI were declined twice! Her Agent/son was still able to move her over to an Original Medicare plan... and $100's of thousands of dollars later, (PRAISE God!!) she is now cancer FREE! Her portion? Less than $250.

As an Agent, your Choice is your Own... AND... you need to know the Playing Field.

Some Agents are extremely biased in how they steer their clients. I know of Agents that have 95% of their clients in Original Medicare... while other Agents have 95% Medicare Advantage plans. Make sure your Agent's bias is your Preference... NOT theirs.

Blessings-

Mike

3. Prescription Drug Coverage and Medication Costs

If you choose Original Medicare, you will need a separate Part D plan for prescription coverage. Each plan has its own monthly premium, deductible, and copay structure.

Your personal medication list also affects what you pay. Drugs are placed into tiers. Lower tiers typically cost less. Higher tiers, especially brand name or specialty medications, may cost significantly more.

Medicare Advantage plans that include drug coverage follow similar tiered pricing structures.

I'm confused about the different tiers in Medicare Part D plans. How do they affect what I pay for my medications?

There are normally 5 tiers of medication on a Medicare Part D plan. Tiers 1 and 2 are generally generic medications, Tier 3 and 4 are generally brand name medications and Tier 5 is generally for specialty medications. One medications may be listed as Tier 1 on one Part D plan and may be listed as Tier 2 or Tier 3 on another Part D plan; there is not consistency on tiers from one plan to the next so it is always important to discus your plan options with an agent before enrolling in a plan. Usually, the higher the tier for a medication, the higher the risk of copay / coinsurance will be when filling the medication at the pharmacy.4. Out of Pocket Costs for Medical Services

Even with Medicare in place, you may still have out of pocket costs such as:

-

Deductibles

-

Coinsurance

-

Copayments

-

Costs for services not fully covered

These vary based on how often you visit doctors, which specialists you see, the tests you need, and whether your providers accept Medicare or are in network for Medicare Advantage.

5. Income Based Adjustments

Your income affects more than just your Part B premium. It can also increase your Part D costs through an additional IRMAA charge. Higher income beneficiaries may see a noticeable increase on their monthly bill if they exceed the income thresholds.

How can I avoid or reduce IRMAA charges on my Medicare premiums?

Great question—IRMAA catches a lot of people off guard, especially around retirement.First, quick refresher (in plain English)

IRMAA = Income-Related Monthly Adjustment Amount

It’s an extra charge added to your Medicare Part B and Part D premiums if your income is above certain limits.

Important (and annoying) detail:

Medicare looks at your income from TWO YEARS AGO.

So in 2026, they’re usually using 2024 tax data.

How to avoid or reduce IRMAA (the practical stuff)

1. Watch your “MAGI” like a hawk

IRMAA is based on Modified Adjusted Gross Income (MAGI), not just your paycheck.

Common things that push people over the line:

Large IRA or 401(k) withdrawals

Roth conversions

Capital gains from selling property or investments

One-time bonuses or severance

Required Minimum Distributions (RMDs)

💡 Strategy: Spread income over multiple years when possible instead of taking a big hit in one year.

2. Use Roth accounts strategically

Roth IRA withdrawals do not count toward MAGI

Partial Roth conversions done before age 65 can reduce future IRMAA exposure

This is one of the most powerful long-term planning tools.

3. Time big financial moves carefully

If you can control when income hits:

Delay selling investments until a lower-income year

Spread withdrawals across December/January to straddle tax years

Avoid stacking multiple income events in the same year

Sometimes staying $1 over the limit can cost thousands in extra premiums.

4. File an IRMAA appeal if your income dropped

This is HUGE—and underused.

If your income went down due to a life-changing event, you can ask Social Security to reduce or remove IRMAA.

Qualifying events include:

Retirement or work reduction

Loss of income-producing property

Divorce or death of a spouse

Employer settlement ending

You do this using SSA Form 44.

👉 This can lower your premiums immediately, not years later.

5. Coordinate Medicare decisions with tax planning

This is where people get burned:

Medicare choices

How to Reduce Your Medicare Costs

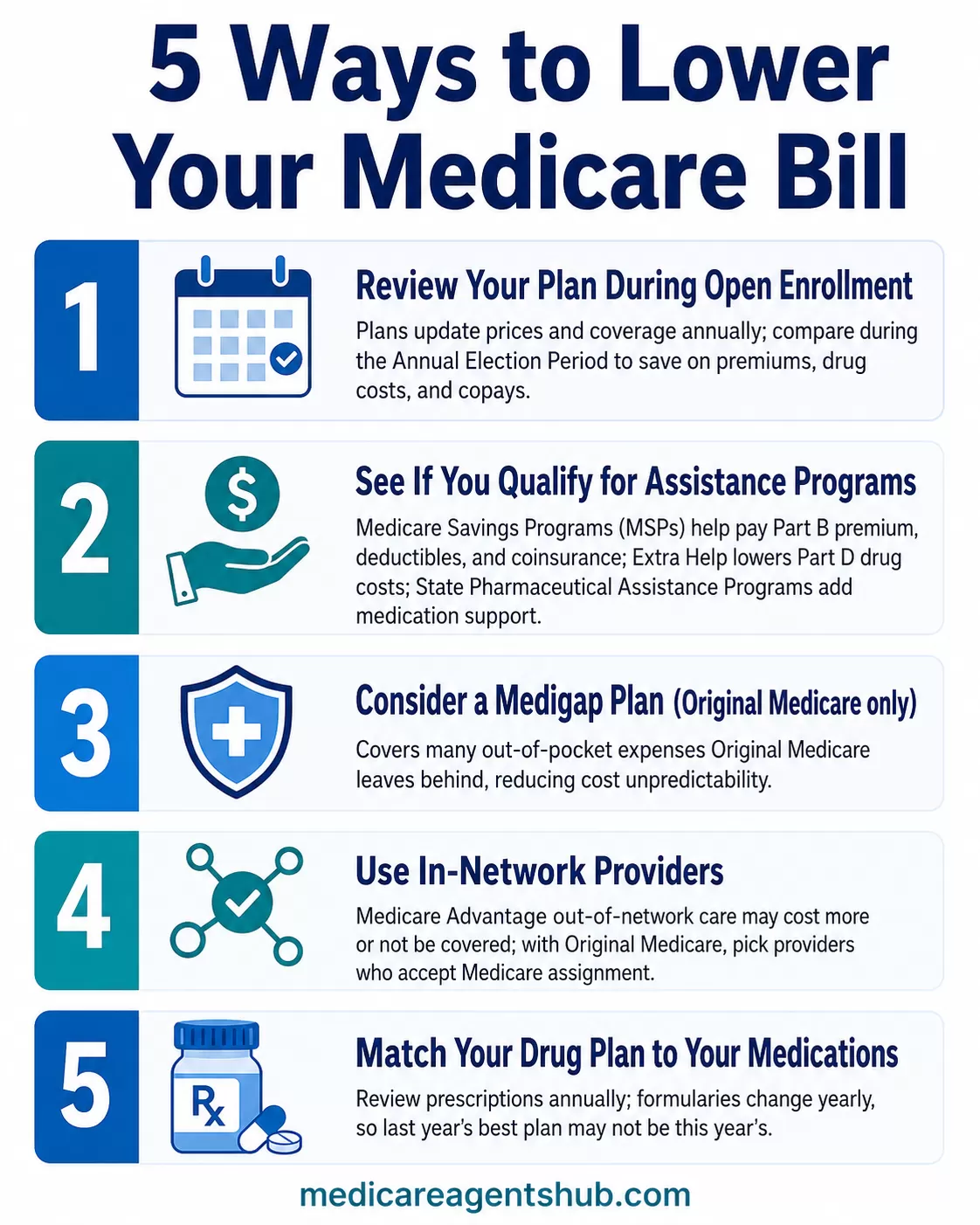

There are several legitimate ways to reduce your Medicare bill, and most beneficiaries benefit from reviewing their options at least once a year.

1. Review Your Plan During Open Enrollment

Your healthcare needs, prescriptions, and provider networks can change. Medicare plans also update their prices and coverage annually. Comparing plans during the Annual Election Period can save you money in premiums, drug costs, and copays.

Many people discover that a different Medicare Advantage or Part D plan better fits their needs and budget. A Medicare agent or advisor can help you compare plans during the Annual Election Period, ensuring you choose coverage that matches your medications, doctor preferences, and budget. Broader healthcare spending trends also play a role in what you pay each year; for context on the forces driving those trends, see our analysis of CMS expenditure data and the federal budget battles shaping Medicare costs.

2. See If You Qualify for Assistance Programs

Several programs can reduce your Medicare costs if you qualify.

-

Medicare Savings Programs (MSPs) can help pay your Part B premium and sometimes deductibles and coinsurance.

-

Extra Help lowers prescription drug costs for people with limited income.

-

State Pharmaceutical Assistance Programs may offer additional support for medication costs depending on your state.

These programs are often underused because many people do not realize they qualify.

3. Consider a Medigap Plan If You Have Original Medicare

A Medigap policy can significantly reduce the unpredictability of healthcare costs by covering many out of pocket expenses that Original Medicare leaves behind. Although Medigap plans come with their own monthly premium, many beneficiaries feel the stability and cost protection are worth it.

What's the financial risk of sticking with Original Medicare without a Medigap plan?

A specific example: I've got a client at CMC who had some heart issues. The bill was $65,000. Thankfully, they have a Medigap policy, which will pay all of their 20% for them. Had they not had the Medicare Medigap supplement policy, they'd be paying $13,000 out of pocket, and I don't know who has that just laying around.

So please, before you make any decisions or non-decisions on Medicare, Original Medicare, Supplement, or Medicare Advantage, speak to someone like myself who deals with it every single day with clients and has real-life experience and real stories to tell about horror stories from making the wrong decisions.

I would be glad to help you. We'll go over the pros and cons of Original Medicare, sticking with that, or doing a Medicare supplement to add to A and B that will pay all of your out-of-pocket costs, or even going to a Medicare Advantage plan, which I believe would be better than sticking with just Original Medicare. Anyway, we're here to help. My office is right on Kelly Street in Manchester, Tony Capraro State Farm. Have a great weekend!

4. Use In Network Providers When Possible

If you are in a Medicare Advantage plan, using in network doctors and facilities reduces your costs. Out of network care may be more expensive or may not be covered at all depending on the plan type.

Even with Original Medicare, choosing providers who accept Medicare assignment ensures you pay only the Medicare approved amount.

5. Choose a Drug Plan That Matches Your Medications

Reviewing your prescriptions annually and matching them with a Part D or Medicare Advantage plan that covers them at the lowest cost can reduce your monthly bill. Formulary changes are common, so a plan that worked last year may not be the best this year.

A local Medicare broker can help you match your medications with the most cost-effective Part D or Medicare Advantage drug plan, potentially lowering your monthly bill and out-of-pocket costs.

Save Your Costs

Whether you are preparing to enroll in Medicare or have been on it for years, understanding what affects your costs gives you more control and confidence. Your Medicare bill is influenced by your plan selections, prescription needs, provider network choices, and even your income level.

The good news is that many cost saving strategies are available. Reviewing your coverage annually with a Medicare advisor, considering assistance programs, and choosing plans that align with your needs can help you manage your Medicare expenses more effectively.