After a Spouse Dies, Medicare and Social Security Benefits May Change

-

January 8, 2026

When you lose your spouse, the last thing you want to think about is paperwork. But in the weeks and months that follow, decisions about your Social Security income, Medicare premiums, and health coverage won't wait, and missing a deadline can cost you money you can't get back.

This isn't a topic anyone wants to read about ahead of time. But if you're here, you probably need to know what's changing, what to do first, and where the landmines are. We'll walk through all of it.

Do You Get Your Spouse's Social Security After They Pass?

It's usually the first financial question that comes up, and the answer is yes, but it's not as straightforward as most people expect.

If your spouse worked long enough to qualify for Social Security (typically 10 years or 40 credits), you're likely eligible for survivor benefits. But here's where the confusion starts:

- You can receive the higher of the two benefits, but not both. If your spouse's monthly benefit was $2,400 and yours is $1,600, you'd receive the $2,400 amount. You don't get to stack them together.

- Age matters. You can claim survivor benefits as early as age 60 (or 50 if you're disabled), but claiming before your full retirement age means a reduced amount.

- A one-time lump sum death benefit of $255 is also available if you were living with your spouse or receiving benefits on their record.

- Divorced spouses may also qualify if the marriage lasted at least 10 years.

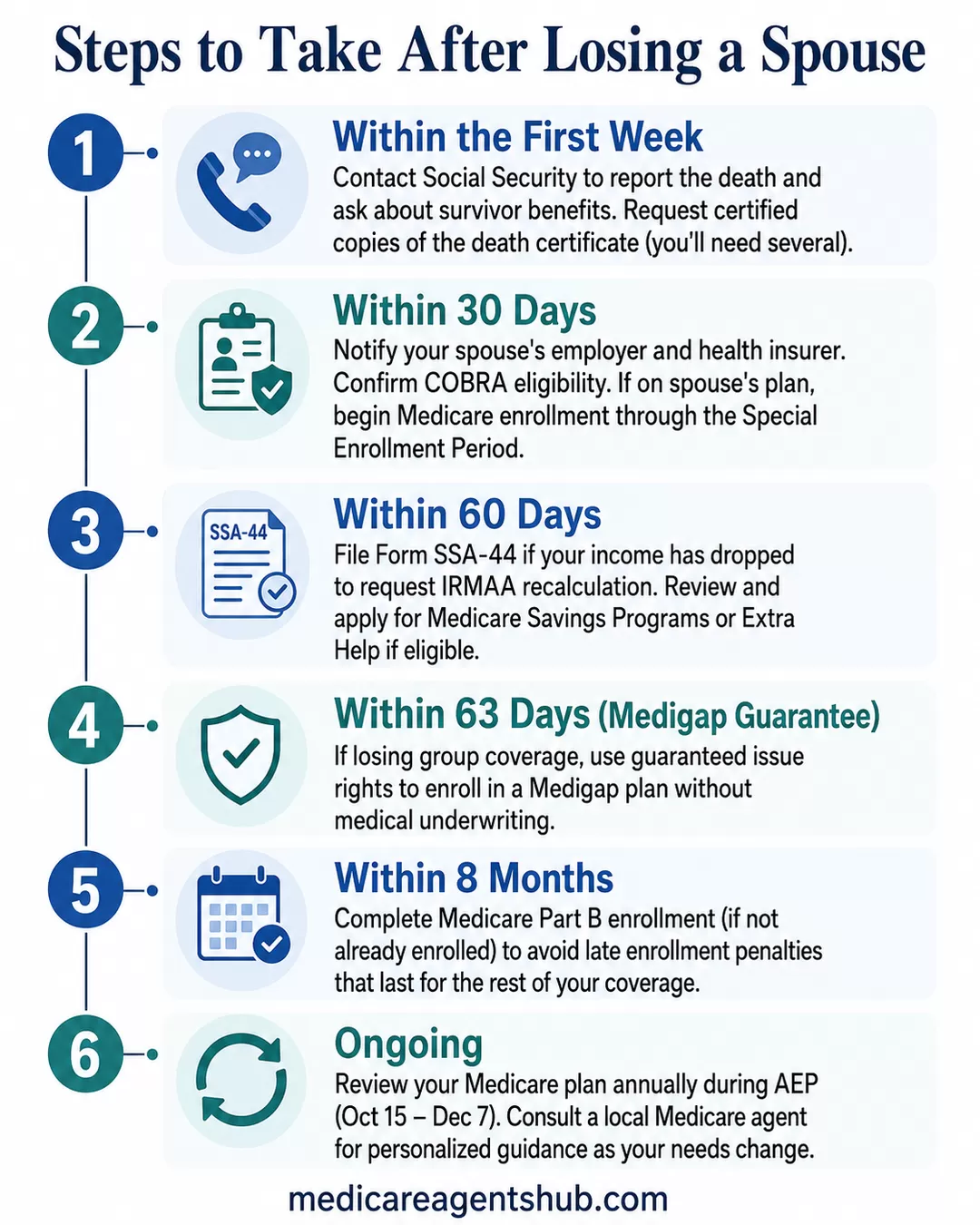

Don't wait on this. Call Social Security as soon as you can, ideally within the first week. Benefits are not applied retroactively in most cases, so every month you delay is income you won't recover. For more on how these two programs intersect, see our guide on how Medicare and Social Security work together.

When my husband dies, do I get his Social Security and mine?

That’s a very common and important question.When a spouse passes away, you don’t receive both benefits. Through the Social Security Administration, you would receive the higher of the two benefits, not both.

So if your husband’s Social Security benefit is higher than yours, you would step up to his amount. If yours is higher, you would continue with your own. The lower benefit stops.

There are also some timing and age factors that can affect the exact amount, so it’s always a good idea to review your situation in advance so you know what to expect and can plan accordingly.

How Losing a Spouse Can Change Your Medicare Premiums

This is the one that blindsides people. You'd think losing a spouse's income would at least mean lower bills, but Medicare premiums can actually go up, sometimes significantly, even when your household income drops.

The Tax Filing Status Shift

When a spouse passes, your tax filing status changes from "Married Filing Jointly" to "Single" (or "Qualifying Surviving Spouse" for up to two years). This matters because Medicare's Income-Related Monthly Adjustment Amount (IRMAA) uses your tax return from two years prior and applies different income thresholds based on your filing status.

The IRMAA income brackets for single filers are significantly lower than for joint filers:

So even if your household income decreases after losing a spouse, the switch to single filing thresholds can push you into a higher IRMAA bracket, meaning higher Part B and Part D premiums. For a deeper look at how IRMAA works, read our article on appealing IRMAA premium increases. You may also want to explore smart tax planning strategies for Medicare to reduce your IRMAA exposure going forward.

Filing Form SSA-44: The Life-Changing Event Appeal

Here's where you can fight back. The death of a spouse qualifies as a "life-changing event" under Social Security's rules, and that means you can ask them to throw out that old tax return and recalculate your IRMAA based on what you're actually earning now.

The process is simpler than most people expect:

- Download Form SSA-44 from the Social Security Administration website

- Select "Death of a spouse" as your life-changing event

- Provide your current (reduced) income estimate

- Include documentation: a death certificate and your most recent tax return or income records

- Submit to your local Social Security office. You can do this in person, by mail, or by phone.

Social Security typically processes these within a few weeks. If approved, your premiums drop to match your actual income, and the savings can be hundreds of dollars per month. It's one of the most impactful financial moves a surviving spouse can make, and too many people don't know it exists.

My husband passed away and now my Medicare premiums went up. Why does losing someone raise your costs?

I’ve had this come up with clients, and it catches people off guard.What usually causes it is the change in filing status. After a spouse passes, you go from married to single, and Medicare uses income from a couple years back to set your premiums. The income brackets for single filers are lower, so even if your income didn’t really change, your Part B and Part D premiums can go up.

Sometimes there’s also a small increase on the Medicare Supplement side if there was a household discount that no longer applies.

The one thing I always suggest is taking a look at your current income. If it’s gone down, you may be able to file an appeal with Social Security and get those premiums reduced.

It’s not always obvious, but definitely worth checking into.

What Happens If You Were on Your Spouse's Health Insurance

If your spouse's job was providing your health insurance, their passing doesn't just mean emotional upheaval. It means your coverage has an expiration date. How you handle the next few months matters a lot.

COBRA Coverage

Under federal law, you're entitled to up to 36 months of COBRA continuation coverage after a spouse's death (longer than the standard 18-month period for voluntary job loss). COBRA premiums can be expensive, though, often $600–$1,500+ per month since you're paying the full cost without an employer subsidy.

COBRA can buy you time, but it's expensive time. If you're Medicare-eligible, transitioning to Medicare is almost always the better long-term move. And you have a window to do it without penalties.

Medicare Special Enrollment Period (SEP)

Losing your spouse's employer coverage qualifies you for a Medicare Special Enrollment Period. This gives you:

- 8 months to enroll in Medicare Part B without a late enrollment penalty

- The ability to enroll in a Medicare Advantage plan or Part D prescription drug plan

- Federal guaranteed issue rights for Medigap (Medicare Supplement) policies when you lose employer group coverage. Insurers cannot deny you or charge higher premiums due to health conditions. Some states extend additional Medigap protections beyond the federal minimum.

Important: Do not rely on COBRA as a long-term solution if you're Medicare-eligible. COBRA is considered "continuation coverage," not "employer group coverage," so it does not protect you from Medicare late enrollment penalties if you delay past your SEP window. Learn more about qualifying in our guide to Medicare's Special Enrollment Period. If you're currently on an employer plan through your spouse, our article on switching from employer insurance to Medicare walks through the process in detail.

How does losing a spouse impact my Medicare plan if I was on their employer coverage?

If you were covered under your spouse’s employer insurance, that coverage usually ends when your spouse passes away. This qualifying event gives you an 8-month Special Enrollment Period to sign up for Medicare Part B (and Part D if needed) without a penalty. Once the employer coverage ends, Medicare becomes your primary insurance, so it’s important to enroll promptly to avoid gaps in coverage.Reassessing Your Medicare Coverage

Even if you've had your own Medicare coverage for years, everything looks different now. Your income has likely changed. Your daily health needs may have shifted. The plan that made sense as a couple might not be the right fit for your life going forward.

Questions to Ask Yourself

- Has your income changed? A lower income may qualify you for Extra Help or Medicare Savings Programs that reduce your premiums, deductibles, and copays.

- Are your healthcare needs different? If your spouse was your primary caregiver, you may need more home health services or a plan with stronger provider networks.

- Are you keeping the same doctors? If you're transitioning from employer coverage to Medicare, verify your providers accept Medicare or are in your chosen plan's network.

- Is your prescription drug coverage still adequate? Compare your medications against available Part D formularies. Drug coverage varies significantly between plans.

Medicare Advantage vs. Medigap After a Spouse's Death

If you're enrolling in Medicare for the first time after losing your spouse's employer coverage, you'll need to choose between Medicare Advantage and a Medigap supplement. There's no universally right answer; it depends on your health, your budget, and how much flexibility you need:

- You need to minimize monthly premiums

- You want bundled benefits (dental, vision, hearing)

- You're comfortable with a provider network

- You want predictable out-of-pocket costs

- You travel frequently or split time between states

- You have chronic conditions requiring specialist care

This is one of those decisions that's worth getting personal guidance on. A licensed Medicare agent can compare the plans available in your area and help you weigh the trade-offs based on your actual health and financial situation, at no cost to you. You can find a licensed Medicare agent near you to get started.

Programs That Can Help With Costs

Going from two incomes (or two Social Security checks) to one changes everything about your budget. The good news is that the lower income you're now living on may actually qualify you for help that wasn't available before:

- Medicare Savings Programs (MSP): State-run programs that pay your Part B premium and may cover deductibles and copays. Eligibility is income-based and varies by state.

- Extra Help (Low-Income Subsidy): A federal program that helps pay Part D premiums, deductibles, and copays. If your income and resources fall below certain limits, you may qualify for $0 or significantly reduced prescription drug costs.

- State Health Insurance Assistance Program (SHIP): Free, unbiased counseling available in every state. SHIP counselors can help you understand your options and apply for assistance programs.

- Social Security survivor benefits: As described above, make sure you're receiving the maximum benefit you're entitled to.

How can I avoid or reduce IRMAA charges on my Medicare premiums?

IRMAA is based on your income from two years ago, so keeping your adjusted gross income lower can help reduce future charges. If your income has dropped because of retirement, divorce, or another life change, you can file an SSA-44 form with Social Security to ask for a lower premium.A Step-by-Step Checklist After Losing a Spouse

Nobody wants to deal with a checklist while they're grieving. But some of these deadlines are unforgiving. Miss them, and you'll pay higher premiums or lose protections you can't get back. If nothing else, hand this list to a family member or trusted friend who can help keep things on track:

Key Takeaways

There's a lot to process here, and none of it is easy to think about while you're grieving. If you take away just four things:

- Claim survivor benefits promptly. Social Security won't apply them retroactively in most cases.

- File Form SSA-44 if your income has dropped. You may be paying higher IRMAA premiums than you need to.

- Don't miss your Special Enrollment Period if you were on your spouse's employer plan. You have 8 months, and late enrollment penalties are permanent.

- Check for assistance programs. Medicare Savings Programs and Extra Help can significantly reduce your costs.

You don't have to figure all of this out alone. A local Medicare insurance agent can sit down with you, look at your specific situation, and help you make sense of what to do next, at no cost to you. Sometimes just having someone walk through it with you makes all the difference.