Missed Your Medicare Special Enrollment Period? Recovery Options Agents Actually Recommend

-

Last Updated August 3, 2026

A woman who's had Medicare Parts A and B since 2006 through disability posted a question that hundreds of thousands of people have lived through: her husband retired, she lost his employer coverage, and she missed the 8-month Special Enrollment Period to pick up additional insurance. Social Security had also switched her from SSI to regular Social Security benefits. She was stuck with nothing but Original Medicare, exposed to 20% coinsurance on every doctor visit with no cap on what she'd owe.

Sixty licensed Medicare agents answered her question. The majority gave the expected advice: wait for the Annual Enrollment Period in the fall, or call an agent to check for SEP eligibility. But buried in those 60 answers were a handful of agents who surfaced specific recovery strategies that most Medicare websites don't cover, and that the other 50+ agents in the same thread either didn't know about or didn't think to mention.

Those strategies are worth understanding, because missing a Special Enrollment Period after losing employer coverage is one of the most common and costly Medicare mistakes a person can make.

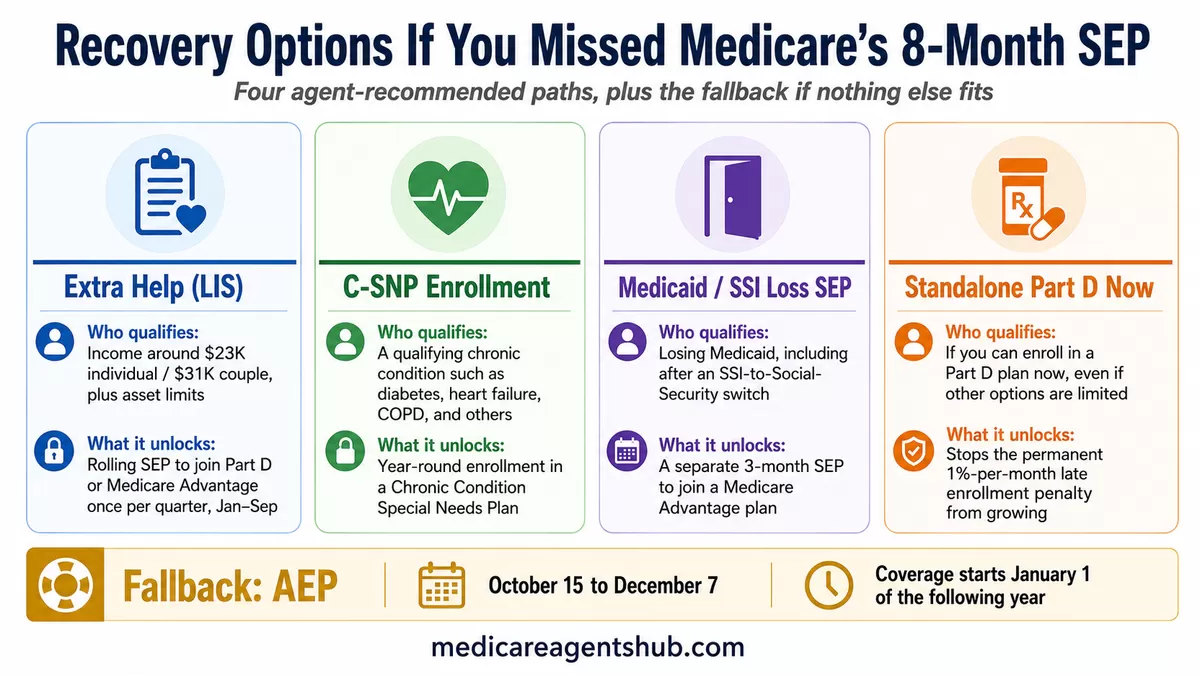

Key Recovery Options If You Missed Your SEP

- Apply for Extra Help (LIS). Qualifying based on income and assets triggers a Special Enrollment Period to join a Part D or Medicare Advantage plan on a rolling basis.

- Check for C-SNP eligibility. A qualifying chronic condition (diabetes, heart failure, COPD, and others) opens year-round enrollment in a Chronic Condition Special Needs Plan.

- Losing Medicaid or SSI? That loss creates its own 3-month SEP that most people don't realize they have.

- Enroll in a standalone Part D plan now. Even if nothing else is available until AEP, joining any drug plan stops the permanent late enrollment penalty from growing.

What Happens When the 8-Month Window Closes

When you lose employer-sponsored health coverage (whether your own or a spouse's), Medicare gives you an 8-month Special Enrollment Period to add coverage. During that window, you can enroll in a Medicare Advantage plan, a standalone Part D drug plan, or (with guaranteed-issue rights) a Medigap policy without medical underwriting.

Once those 8 months expire, the doors close in sequence:

- Medicare Advantage and Part D: You typically have to wait until AEP (October 15 through December 7) for a plan effective January 1 of the following year.

- Medigap: You lose your guaranteed-issue rights, meaning insurers can now medically underwrite you. If you have health conditions, you may be denied outright or charged higher premiums, depending on your state's rules.

- Part D late enrollment penalty: For every full month you went without creditable drug coverage, Medicare adds 1% of the national base beneficiary premium to your Part D cost. That penalty is permanent. It follows you for life.

As one agent in the thread put it bluntly: "That penalty is forever. It never goes away." The longer you sit without Part D coverage, the larger it grows.

The Extra Help Backdoor: How LIS Reopens Enrollment

This was the single most valuable piece of advice in the entire 60-agent thread, and only a small handful of agents mentioned it.

The Low Income Subsidy (LIS), also called "Extra Help," is a federal program that helps people with limited income and assets pay for Medicare Part D prescription drug costs. That much is widely known. What's far less known is the enrollment consequence: qualifying for Extra Help triggers a Special Enrollment Period that lets you enroll in a Medicare Advantage plan or Part D drug plan outside of AEP. And unlike the one-time SEP you get from losing employer coverage, the LIS-triggered SEP is available on a rolling basis. Under current rules, LIS enrollees can use this SEP to switch plans once per calendar quarter during the first three quarters of the year (January through September). In the fourth quarter, you'd use AEP instead.

I have Medicare Part A and B since 06/01/2006 because of disability. My husband retired on 4/1/2024, and I now have no other coverage except for Medicare Parts A and B because I missed open enrollment for insurance coverage. Note: SS dropped SSI and changed it to straight SS. Please help.

You currently have Medicare only, and when your husband retired you had an 8 months Special Enrollment Period (SEP) to pick up additional coverage. Unfortunately, that period has passed.Here’s the good news: You can sign up for a Medicare drug plan now, so you are protected going forward. You may have a penalty, but enrolling now stops the penalty amount from growing.

Next, I recommend applying for LIS/ Extra Help (Low Income Subsidy). If you qualify, it may remove penalties and allow you to enroll in a Medicare Advantage plan sooner. You can call 1-800-MEDICARE to apply.

If you don’t qualify for Extra Help, your next Medicare Advantage enrollment window is October 15 – December 7, for coverage effective January 1.

That answer from Marie Smith in Athens, Alabama, hits the three critical points: enroll in a drug plan immediately to stop the penalty from growing, apply for Extra Help because qualifying can reopen your enrollment options, and if Extra Help doesn't work out, AEP is the fallback.

Who Qualifies for Extra Help

Extra Help eligibility is based on income and assets. The general thresholds are roughly $23,000 per year for an individual and $31,000 for a married couple, with asset limits in the mid-teens for individuals and mid-thirty-thousands for couples. These numbers are adjusted annually, so check the current limits on ssa.gov/extrahelp before ruling yourself out.

Several agents across the Extra Help question thread confirmed the mechanics. Joe Graves, an agent in Oklahoma City, provided one of the clearest breakdowns:

I'm on a fixed income and struggling to afford my medications. What's this Extra Help program I've heard about for Medicare Part D?

Extra Help is a program from Social Security that does several things if you qualify: 1) it may help pay your Part D premium, 2) it may lower/eliminate your Part D penalty if you have one, and 3) it may set your prescription copays at low amounts.In general, a single person must have around $1500 or less in income with very limited asses such as savings or retirement funds. If you think you qualify, the Social Security department can help you apply for Extra Help.

That third point is the one people miss: Extra Help can eliminate or reduce your Part D late enrollment penalty. For someone who's been without drug coverage for a year or more, that alone can save hundreds of dollars over time. One caveat worth knowing: the penalty is waived only for as long as you continue to qualify for Extra Help. If you later lose LIS (for example, because your income or assets rise above the threshold), the full penalty can be reinstated.

How to Apply

You can apply for Extra Help in three ways:

- Online at ssa.gov/extrahelp

- By calling Social Security at 1-800-772-1213

- Through your local State Health Insurance Assistance Program (SHIP), which provides free Medicare counseling

If you already receive full Medicaid, Supplemental Security Income (SSI), or participate in a Medicare Savings Program, you typically qualify automatically and don't need to apply separately. For everyone else, the application is straightforward, and the savings can be significant even beyond the enrollment benefit.

C-SNP Enrollment: A Year-Round Path for Chronic Conditions

The second recovery strategy that surfaced in the agent thread applies to people who have qualifying chronic health conditions. Chronic Condition Special Needs Plans (C-SNPs) are a type of Medicare Advantage plan that can enroll members year-round, bypassing the AEP calendar entirely.

Mitchell Jerome, a licensed agent in Kingwood, Texas, was one of the agents who flagged this directly: "If you have Medicare A and B then you can enroll in Medicare Advantage plans... At this time of year you can still enroll in plans that would be Chronic Special Needs Plans (C-SNP). Find an agent that can help you in your area as these plans are not widespread."

Jim Carroll, an agent in Titusville, Florida, provided the most detailed response in the thread, including the full list of CMS-recognized chronic conditions that qualify:

I have Medicare Part A and B since 06/01/2006 because of disability. My husband retired on 4/1/2024, and I now have no other coverage except for Medicare Parts A and B because I missed open enrollment for insurance coverage. Note: SS dropped SSI and changed it to straight SS. Please help.

How old are you?For clarity, when exactly did you lose SSI? You have 3 months to join a Medicare Advantage Plan from either the date you lost Medicaid or the date you were notified that you're no longer eligible, whichever is later.

Also, regardless if you lost SSI, if your disability is due to one or more of the chronic conditions recognized by Centers for Medicare & Medicaid Services (CMS), you would qualify to join a Chronic Condition Special Needs Plans (C-SNPs). Those chronic conditions are:

Chronic alcohol and other dependence

Certain autoimmune disorders

Cancer (excluding pre-cancer conditions)

Certain cardiovascular disorders

Chronic heart failure

Dementia

Diabetes mellitus

End-stage liver disease

End-Stage Renal Disease (ESRD) requiring dialysis (any mode of dialysis)

Certain severe hematologic disorders

HIV/AIDS

Certain chronic lung disorders

Certain chronic and disabling mental health conditions

Certain neurologic disorders

Stroke

That answer also surfaces a second critical detail: losing SSI (and by extension Medicaid eligibility) creates its own 3-month enrollment window. For the woman who originally asked the question, that SSI-to-Social Security switch may have generated a separate SEP that she didn't realize she had.

What C-SNP Enrollment Looks Like

C-SNPs work like other Medicare Advantage plans: they cover everything Original Medicare covers, typically include Part D drug coverage, and often add benefits like dental, vision, and transportation. The difference is that the plan's benefits and provider network are built around managing a specific condition.

There's one catch agents flagged across the Special Needs Plan question thread: your doctor has to verify your qualifying condition by completing a Chronic Condition Verification (CCV) form, usually within 60 days of enrollment. If that form doesn't get submitted, you can be disenrolled from the plan. Several agents recommended getting this handled before or immediately after enrolling.

C-SNP availability varies by county. Not every area has a C-SNP option, and the qualifying conditions covered can differ by plan. This is one of the strongest reasons to work with a local Medicare agent who knows what's available in your specific area.

Stop the Part D Penalty Clock Right Now

Even if Extra Help doesn't pan out and you don't have a qualifying chronic condition, there's one thing every agent in this situation agrees on: get Part D drug coverage as soon as possible.

The Part D late enrollment penalty works like a taxi meter. Every month you go without creditable drug coverage, it ticks up by 1% of the national base beneficiary premium (roughly $37 per month in recent years). Miss 12 months of coverage, and you're looking at about $4 to $5 per month added to every Part D premium you pay for the rest of your life. Miss 24 months, and it doubles.

The math is straightforward: a 24-month gap means roughly $9 per month in permanent penalties, or over $100 per year, compounding as the base premium rises. Over a 20-year retirement, that's thousands of dollars in avoidable costs.

The action item is simple. If you can enroll in any Part D plan right now, do it. Even if you can't add Medicare Advantage or Medigap coverage until AEP, a standalone drug plan stops the penalty from growing. And if you later qualify for Extra Help, the penalty may be reduced or eliminated entirely while you remain on LIS.

When AEP Is the Only Path Forward

For people who don't qualify for Extra Help, don't have a C-SNP qualifying condition, and have exhausted any other SEP windows, the Annual Enrollment Period (October 15 through December 7) is the next opportunity. Plans chosen during AEP take effect January 1.

That gap between now and January can feel enormous when you're sitting on Original Medicare with no supplemental coverage. A few agents in the thread suggested steps to bridge it:

- Apply for Medicaid in your state. If you qualify, Medicaid can cover costs that Original Medicare doesn't, and Medicaid eligibility itself triggers new enrollment options including Dual Special Needs Plans (D-SNPs).

- Look into your state's Medicare Savings Programs. Even if you don't qualify for full Medicaid, programs like QMB (Qualified Medicare Beneficiary) can pay your Part B premiums and cost-sharing.

- Consider a hospital indemnity plan. These aren't Medicare plans, but they pay a flat daily benefit if you're hospitalized, which can help cover the Part A hospital deductible (well over $1,600 per benefit period) and offset some of the financial exposure while you wait.

One agent, Cody Hebden in Mount Holly, North Carolina, also raised an important point about Medigap: "You may have guaranteed rights to purchase additional private medicare supplemental insurance, as long as you can prove that you had creditable coverage from his employer all this time." The key phrase is "guaranteed rights." If you can document continuous creditable coverage, some Medigap guaranteed-issue protections may still apply, though the specifics depend heavily on your state.

I have Medicare A and B, which was secondary to my large group health plan. My spouse passed away in late June 2025, and his company is providing COBRA coverage for six months, through January. If I wait until then, will I still have guaranteed issue for a Medicare supplement, or do I have only 63 days from June 30 (until Sept 1) to enroll? I'm in CO

You have a 63-day guaranteed issue window for a Medicare supplement following the loss of active employer coverage, and COBRA is not considered active employment coverage for that purpose. If you already have Medicare A and B, you likely need to enroll in a Medigap plan within 63 days of when the active group coverage ended (late June), or you may lose your guaranteed issue rights, even if you continue COBRA.The SSI-to-Social Security Switch: A SEP Most People Don't Know About

The original question mentioned that Social Security had switched the person from SSI to regular Social Security benefits. Multiple agents overlooked this detail, but it may be the most immediately actionable piece of the whole situation.

Losing SSI often means losing Medicaid eligibility (since SSI recipients automatically qualify for Medicaid in most states). And losing Medicaid creates a Special Enrollment Period of its own: you have 3 months to join a Medicare Advantage plan, starting from either the date you lost Medicaid or the date you were notified of the loss, whichever is later. That notification-date rule matters, because official letters often arrive weeks after the coverage actually ends. Save every notice you get.

Sterling Warmack, an agent in Duncan, South Carolina, was one of the few who caught it: "The change from SSI to SS also should qualify you for a special enrollment period."

If you've recently transitioned from SSI to Social Security and lost Medicaid as a result, check whether you're still inside that 3-month window. It's a separate SEP from the 8-month employer coverage SEP, and the two don't cancel each other out.

Why This Matters Beyond One Question

The woman who posted that question isn't an outlier. People on disability-based Medicare are especially vulnerable to coverage gaps because their Medicare journey started years before age 65, often under complicated circumstances. A spouse's retirement, a change in SSI status, or a move to a new state can each trigger enrollment deadlines that aren't obvious and aren't well publicized.

Out of 60 licensed agents who answered, fewer than 10 specifically mentioned the Extra Help backdoor, the C-SNP year-round enrollment path, or the Medicaid-loss SEP. The other 50+ gave answers ranging from "wait for AEP" to "call an agent" to "you're in open enrollment right now" (which many answered during the fall AEP window, not realizing the question was about a longer-term gap).

That's not a criticism of those agents. It's an illustration of how buried these recovery paths are in the Medicare system. The rules exist, but knowing which ones apply to your exact situation requires someone who's looking for them.

If you or a family member has missed a Medicare enrollment window, don't assume you're stuck waiting until fall. Connect with a licensed Medicare agent in your area who can review your specific situation, check for SEP eligibility you may not know about, and determine whether Extra Help or a C-SNP enrollment could get you covered sooner than you think.