Medicare Special Enrollment Period After Losing Employer Coverage

-

Last Updated August 3, 2026

Losing your health insurance from work is stressful, but there's good news: it qualifies you for a Medicare Special Enrollment Period (SEP). This window lets you enroll in Medicare without facing late penalties. To help you navigate the transition, we gathered insights from licensed Medicare agents on the rules, deadlines, and common pitfalls, all in response to a single focused question: “Am I eligible for a Special Enrollment Period if I lose employer coverage?” You can also read every agent's answer on the original question page.

If a senior is turning 65 but still working, should they enroll in Medicare or delay it?

Whether a senior turning 65 should enroll in Medicare or delay it while still working depends on their job situation—specifically, their employer’s size and health plan. Here’s how it breaks down:If the employer has 20+ employees: The company’s group health plan is usually "primary" (pays first), and Medicare is "secondary." In this case, they don’t have to enroll in Medicare right away. They can stick with the work plan and delay Medicare Parts A and B without penalties, as long as the job coverage is “creditable” (meets Medicare standards). Part A (hospital coverage) is free, though, so some sign up for it as a backup since it can coordinate with the work plan. Part B (doctor visits, outpatient care) has a monthly premium, so delaying it often makes sense to avoid double costs.

If the employer has fewer than 20 employees: Medicare typically becomes primary, and the work plan secondary. Here, they should enroll in Medicare Parts A and B at 65, because the work insurance might not cover much unless Medicare kicks in first. Skipping it could mean gaps in coverage or higher out-of-pocket costs.

Other Factors: If their work plan is pricey or skimpy (high deductibles, limited drug coverage), switching to Medicare might save money or improve care, even with a big employer. They’d need to compare premiums, copays, and drug formularies. Also, if they have an HSA, signing up for Medicare stops HSA contributions—something to weigh if they’re still saving there.

How to Delay: If they skip Medicare Part B (the part that costs a monthly premium) at 65 because of a solid work plan, they will get a Special Enrollment Period (SEP) later to turn on Part B and enroll in a plan in short order at that time.

Confirming SEP Eligibility After Employer Coverage Ends

If you lose your health coverage through an employer, it typically triggers a Special Enrollment Period, allowing you the opportunity to enroll in Medicare. Across all the responses provided, this was a consistent theme: losing employer coverage is recognized as a qualifying event that opens up an SEP.

In nearly every case, losing job-based coverage grants access to a Medicare SEP, provided the coverage was deemed creditable. This includes situations like losing coverage after a spouse passes away. Some professionals described this as a life-changing event that initiates eligibility to sign up for Medicare plans. This can include enrolling in various parts of Medicare such as A, B, C, or D. Even if you are over 65 and delayed enrolling in Medicare while covered by an employer plan, the end of that coverage creates an opportunity to enroll without standard penalties.

Several responses emphasized the importance of verifying that the lost coverage was creditable. When your group coverage is creditable, it essentially means it met or exceeded the benefits Medicare offers. This status is often confirmed through your group insurance provider or human resources department. Losing such coverage typically makes you eligible to enroll in a Medicare plan without late penalties.

Some professionals also noted that SEP eligibility can apply in a range of other situations beyond job loss, such as moving to a new state or being affected by a natural disaster, though the context here specifically relates to losing employer coverage. Regardless of circumstance, a SEP becomes available when that loss occurs.

I have Medicare Part A and B since 06/01/2006 because of disability. My husband retired on 4/1/2024, and I now have no other coverage except for Medicare Parts A and B because I missed open enrollment for insurance coverage. Note: SS dropped SSI and changed it to straight SS. Please help.

Since you already have Medicare Parts A and B and recently lost other coverage through your husband’s retirement, that loss of coverage can trigger a Special Enrollment Period. This may allow you to enroll in additional coverage now instead of waiting for the fall. With only Parts A and B, you’re exposed to unlimited out-of-pocket costs, so most people in your position add either a Medicare Advantage plan or a Medigap (supplement) plan along with a Part D drug plan.Part B Special Enrollment Period Timeframes: How Long You Have

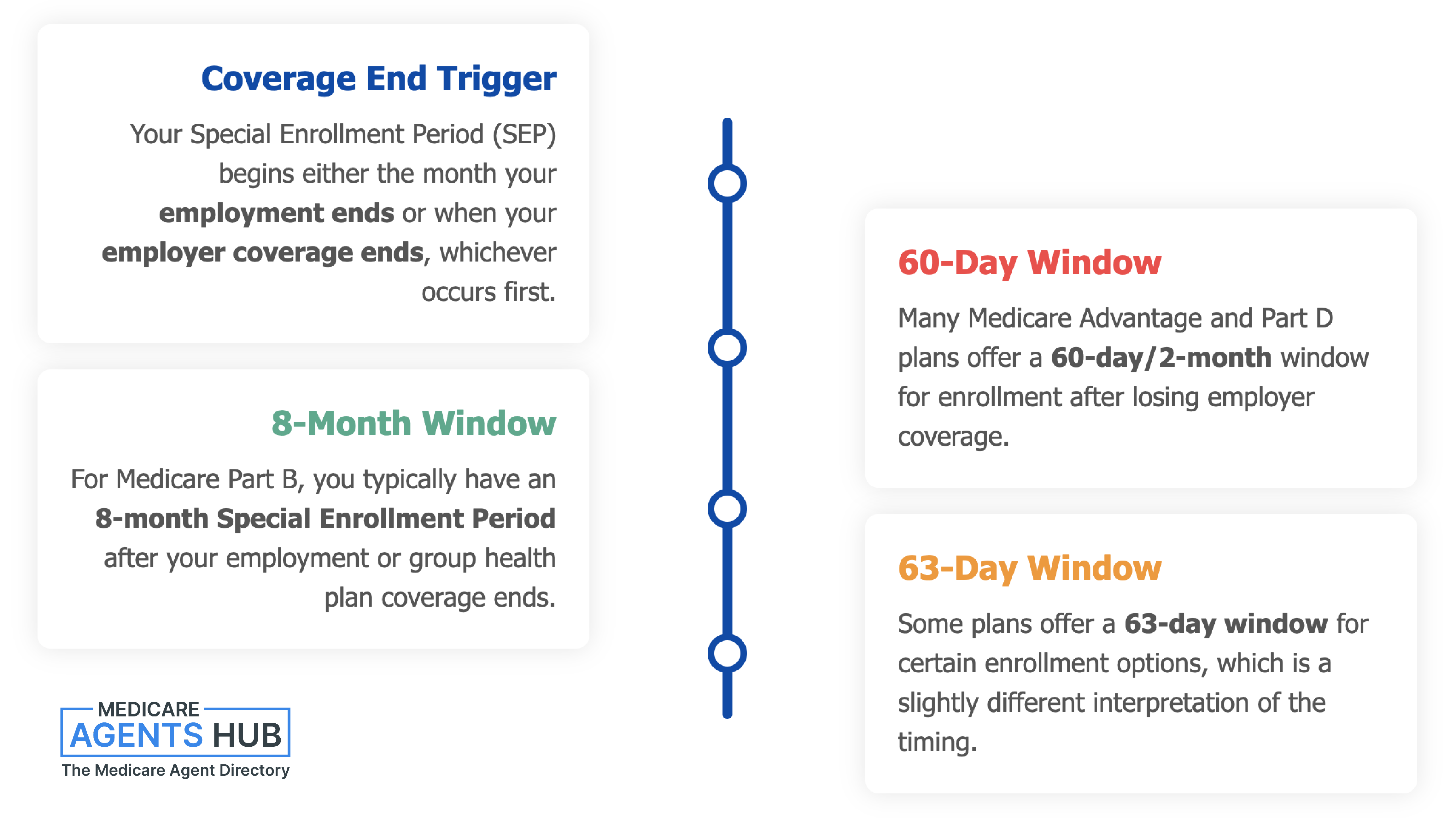

When you lose your employer-based health insurance, you don’t have unlimited time to act. The responses you provided included a few variations on the SEP time window, but all emphasized that there is a defined and limited period in which you can make your Medicare selections.

| Coverage Type | Enrollment Window |

|---|---|

| Medicare Part A & Part B | 8-month SEP |

| Medicare Advantage (Part C) | 63 days from coverage loss |

| Medicare Part D | 63 days from coverage loss |

| Medigap | 6-month open enrollment (from Part B effective date) |

Note: Your Medigap open enrollment window is tied to your Part B start date, not the date you lost your employer coverage. This is a one-time, federally protected period, so getting Part B active promptly matters if you want a Medigap plan without medical underwriting.

Despite the different timeframes for each part, all professionals highlighted the same core idea: you must act quickly to ensure continuous coverage and avoid any potential penalties or delays. Waiting too long could result in a gap in your healthcare or prescription drug coverage, and that can complicate matters significantly.

Some also noted that while Medicare does give you a few months to act, it’s best not to wait until the deadline approaches. Prompt coordination ensures you’re not left uncovered for any period of time.

I have Medicare Part A and B since 06/01/2006 because of disability. My husband retired on 4/1/2024, and I now have no other coverage except for Medicare Parts A and B because I missed open enrollment for insurance coverage. Note: SS dropped SSI and changed it to straight SS. Please help.

Got it — since we’re now in October 2025, your situation changes a bit, but there are still options.Here’s what’s happening:

Because your husband retired back in April 2024, your Special Enrollment Period (SEP) for losing employer coverage has already expired. (That SEP lasts 8 months after losing group coverage — so it would’ve ended around December 2024.)

But the good news is — you’re now in Medicare’s Annual Enrollment Period (AEP), which runs October 15 through December 7 every year. During this time, you can:

Enroll in a Medicare Advantage (Part C) plan, which combines hospital, medical, and often prescription coverage.

Or enroll in a standalone Part D (prescription drug) plan if you want to stay on Original Medicare.

Your new coverage would start January 1, 2026.

Since you mentioned you only have Parts A and B right now, you should definitely look into adding at least a Part D plan — otherwise, you could face a late enrollment penalty later on. You might also qualify for Extra Help or a Medicare Savings Program depending on your income, especially since your SSI changed to standard Social Security. Those programs can help lower your premiums and copays.

So right now, you’re in the perfect window to fix this — just make sure you act before December 7, 2025.

Would you like me to help you figure out what type of plan (Advantage or Supplement + Part D) might work best for your health needs and budget?

Enrollment Options During SEP

Once your Special Enrollment Period begins, you gain access to a range of Medicare options. Multiple responses described the variety of plans you can choose from, depending on your needs and situation.

You may choose to enroll in Original Medicare, which includes Part A (hospital insurance) and Part B (medical insurance). From there, you can add on a Part D plan for prescription drug coverage. Alternatively, you may opt for a Medicare Advantage Plan (Part C), which bundles coverage into one plan and often includes drug benefits.

Some noted that during this SEP, you're not limited to just enrolling in Medicare itself; you can also select a Medigap (supplement) plan to help cover out-of-pocket costs or change between Medicare Advantage plans if needed.

A few professionals clarified that even if you delayed Medicare Part B initially because you had employer coverage, this SEP allows you to activate it without facing a penalty. Several mentioned that decisions made during this period can determine the trajectory of your healthcare in retirement, reinforcing the importance of evaluating all available plan types.

Additionally, a couple of responses referred to the possibility of coordinating enrollment into multiple parts, such as Parts A, B, C, and D, all at once, depending on the needs of the individual. The takeaway was clear: this is a key window of opportunity to choose or change your Medicare path.

I've been on my employer's health plan but am retiring soon. What should I consider when moving to Medicare?

Timing is a big factor. Medicare plans only begin on the 1st of every month, so make sure your employer coverage extends to the end of the month before you start Medicare.Loss of Creditable Coverage: Why It Matters for Your SEP

A recurring concept throughout the responses is the importance of your previous employer coverage being creditable. This term came up several times and plays a critical role in determining your eligibility for a Special Enrollment Period and avoiding late penalties when transitioning into Medicare.

Creditable coverage essentially refers to employer-sponsored insurance that is considered at least as comprehensive as Medicare’s standard benefits. If the coverage you had through your job meets this standard, losing it will open the door to a SEP where you can sign up for Medicare Parts A and B, and make decisions about Advantage plans, Part D, or Medigap coverage. For a deeper explanation of how this works, read our full guide on what counts as creditable coverage for Medicare.

One insight clarified that the determination of creditable coverage is typically provided by the group insurance provider or your employer’s human resources department. This official confirmation helps ensure that you are eligible for the SEP and that you won’t be penalized for delayed Medicare enrollment. It’s a vital step in the process, especially for individuals who delayed enrolling in Medicare Part B while they were still working.

Several responses stressed that creditable coverage status must be clear at the time of losing your job-based plan. Without that confirmation, the ability to access SEP benefits could be compromised or delayed, leading to confusion or potential penalties. Therefore, verifying the creditable status of your previous coverage is one of the most important things to do immediately after leaving your job.

Can you explain what "creditable coverage" means and when it applies?

“Creditable coverage” means your other insurance is expected to pay, on average, at least as much as Medicare’s standard coverage, most commonly referring to prescription drug coverage (Part D). It matters because if you go 63 days or more without creditable drug coverage after becoming eligible for Medicare, you may face a late enrollment penalty when you enroll in Part D later.This often applies to employer or union plans, VA coverage, or certain retiree plans, which will notify you each year if your coverage is creditable. If your coverage is creditable, you can delay Part D without penalty.

Always keep the annual creditable coverage notice as proof in case Medicare asks later.

COBRA and Medicare: A Cautionary Note

While COBRA coverage might seem like a convenient extension of employer-sponsored insurance, it came up in multiple responses as a potential pitfall in the context of Medicare eligibility and SEP rules.

A few professionals cautioned that COBRA is not considered creditable coverage under Medicare. This distinction is crucial. If someone chooses COBRA instead of enrolling in Medicare during their SEP, they may unknowingly forfeit their right to penalty-free enrollment and could be left with gaps in coverage.

One contributor pointed out that Medicare does not view COBRA as a qualifying substitute, which means that relying on COBRA during this transition can prevent you from making full use of your SEP. Even if you still have access to healthcare through COBRA, Medicare may not consider you “covered” in the same way it does for employer-sponsored insurance, leading to complications down the line.

Additionally, it was noted that COBRA can be significantly more expensive than Medicare options. A few responses suggested that in most cases, it’s financially unnecessary to pay for COBRA when Medicare is available. There was also a strong suggestion to avoid overspending on COBRA, unless your situation clearly calls for it.

In summary, the general advice was to steer away from using COBRA as a bridge to Medicare. Instead, it's usually better to move directly into Medicare during your SEP to avoid penalties and simplify your coverage path.

I have Medicare A and B, which was secondary to my large group health plan. My spouse passed away in late June 2025, and his company is providing COBRA coverage for six months, through January. If I wait until then, will I still have guaranteed issue for a Medicare supplement, or do I have only 63 days from June 30 (until Sept 1) to enroll? I'm in CO

No, likely you will not have a guaranteed issue period for a Medicare Supplement (Medigap) plan if you wait until January 2026 for your COBRA to end, because COBRA is generally not considered "creditable coverage" for Medigap purposes. To qualify for guaranteed issue, you must enroll within 63 days of losing your employer's group health coverage. If you wait until January, more than six months will have passed, and you will likely lose your right to a guaranteed issue Medigap policy.SEP Rules Vary Based on Circumstances

While the focus here is on losing employer coverage, it's worth noting that several responses highlighted how Special Enrollment Period rules can vary depending on the situation. In other words, while losing job-based insurance is one well-known trigger, there are other life events that may qualify someone for a SEP as well.

A few responses mentioned other scenarios such as moving to a different location or experiencing a weather-related disaster. These events can also trigger a SEP, though the timing and options may be different based on individual factors and, in some cases, state-specific regulations.

Some noted that SEP windows differ slightly depending on what you’re enrolling in. For example, there may be separate timeframes for enrolling in Medicare Parts A and B versus Medicare Advantage or prescription drug plans. One explanation also pointed out that the window for enrolling in Part A and B might be longer than the one for Advantage or drug plans.

There were reminders that SEP eligibility isn't always the same across all circumstances, and some emphasized the importance of checking your specific situation to understand how long you have and what you’re allowed to do. SEP guidelines can be influenced by your location, plan availability, and other variables unique to your situation.

These nuances reinforce the value of personalized guidance during this transition. While losing employer coverage is a common SEP trigger, how you respond, and what rules apply, may vary based on the details of your life and benefits history.

I have Medicare Part A and B since 06/01/2006 because of disability. My husband retired on 4/1/2024, and I now have no other coverage except for Medicare Parts A and B because I missed open enrollment for insurance coverage. Note: SS dropped SSI and changed it to straight SS. Please help.

You might consider enrolling in a Medicare Supplement, depending on your age and the state you live in. This option provides an open network of doctors. The other option would be to evaluate special enrollment options for a Medicare Advantage or Part C plan. Certain chronic conditions, moving to a new service area, or natural disasters can all provide ways to enroll after open enrollment if you qualify. Contact me, and we can review your specific situation.Coordinating with Brokers for Seamless Transitions

Navigating Medicare enrollment during a SEP can be confusing, especially if you're dealing with deadlines, multiple plan options, and coverage transitions. Several responses recommended working with an experienced broker who can guide you through the steps and minimize the risk of a coverage gap.

Some contributors emphasized that brokers are skilled at helping individuals understand their SEP options and plan benefits, as well as making the process faster and more seamless. For example, coordinating plan start dates to ensure continuous care and medication coverage was mentioned as an area where expert help can be especially valuable.

There were insights suggesting that even though Medicare grants a SEP, it's not always easy to know what to do without assistance. The options (Original Medicare, Advantage plans, Medigap, drug plans) all come with their own enrollment rules and timelines. A broker can help you navigate those differences and avoid common enrollment mistakes.

A few responses also advised against trying to go through this transition alone, especially if you are unsure about plan compatibility, eligibility timing, or how to submit enrollment paperwork correctly. Support from someone who knows the ins and outs of Medicare can make a meaningful difference.

Ultimately, getting help from a broker isn’t just about saving time, it can also help ensure that your transition is smooth, strategic, and properly aligned with your healthcare goals.

What to Do Right After You Lose Employer Coverage

If you just lost job-based coverage, here's a practical order of operations:

- Confirm your prior coverage was creditable. Ask your former HR department or group insurance provider for written confirmation. This is what protects you from Part B and Part D late penalties.

- Mark your SEP deadlines on your calendar. You get 8 months for Part A & B, 63 days for Part D and Medicare Advantage, and 6 months for Medigap once Part B is active.

- Gather your paperwork. Request Form CMS-L564 from your former employer and have your Social Security and Medicare information ready before you apply.

- Compare your plan options. Weigh Original Medicare plus a Medigap and Part D plan against a Medicare Advantage plan based on your doctors, prescriptions, and budget.

- Talk to a local, licensed broker. A broker can coordinate start dates so you don't have a gap. You can find a Medicare agent in your area through our directory.

I have Medicare A and B, which was secondary to my large group health plan. My spouse passed away in late June 2025, and his company is providing COBRA coverage for six months, through January. If I wait until then, will I still have guaranteed issue for a Medicare supplement, or do I have only 63 days from June 30 (until Sept 1) to enroll? I'm in CO

You will have loss of creditable coverage. This will provide a special enrollment period. There will be a form you will need to have filled out by your husbands hr to verify that you had continuing coverage.Common Pitfalls to Avoid

A few mistakes come up over and over when people transition off employer coverage:

- Assuming COBRA counts as creditable coverage. It doesn't for Medicare purposes. Relying on it can cost you your SEP and trigger lifelong Part B and Part D penalties.

- Missing the Medigap window. Your 6-month Medigap open enrollment starts when Part B becomes active, and it's the only time you're guaranteed coverage without medical underwriting.

- Waiting until the last minute. Applications, ID verification, and paperwork all take time. Waiting until day 60 of a 63-day window is how gaps happen.

- Skipping the creditable coverage letter. Without written proof, Social Security may push back on your late Part B enrollment and apply penalties you shouldn't owe.

Can Your Employer Force You to Take Medicare?

No. If your company has 20 or more employees, your group health plan is required by federal law to keep offering you the same coverage it offers younger workers, whether or not you enroll in Medicare. Your employer can’t pressure you off the group plan or refuse to cover you because you turned 65.

The rules shift at smaller companies. If your employer has fewer than 20 employees, Medicare typically becomes your primary payer at 65, and the group plan pays second. In that case, most people enroll in Part A and B at 65 because the group plan assumes Medicare is picking up the majority of the bill. That’s not the employer forcing you onto Medicare, but it is a strong practical reason to enroll.

If you feel pressured to drop your group plan for Medicare at a company with 20+ employees, that may be a violation of Medicare Secondary Payer rules. When in doubt, talk to a licensed broker before signing anything.

Conclusion: You Get Access to Medicare Without Late Penalties

Losing your employer coverage is a major life transition and fortunately, it often opens the door to a Special Enrollment Period that gives you access to Medicare without late penalties. Every professional who weighed in agreed: this is a critical opportunity that must be acted on quickly and strategically.

Your SEP window may be as short as 63 days or extend to 8 months depending on what parts of Medicare you’re enrolling in. It's essential to confirm that your prior insurance was creditable, avoid leaning on COBRA unless necessary, and explore your plan options thoroughly. There’s also flexibility in the system. SEPs can vary based on your circumstances, and getting support from a knowledgeable broker can help you take full advantage of your options.

The choices you make during your SEP will shape your future healthcare experience. Taking informed, timely steps will set you up with the coverage you need, without unnecessary costs or delays.