I Chose the Wrong Medicare Plan During AEP… Now What?

-

January 12, 2026

Let me start by stating this directly, because I have this conversation every single January. If you are thinking, “I picked the wrong Medicare plan during Annual Enrollment,” you are absolutely not alone.

I have been a Medicare agent for a long time, and every year, once the calendar flips to January, my phone rings with the same worried questions. My doctor is not in network. My prescriptions are more expensive than I expected. This plan sounded great in October, but now it feels like a mistake.

Take a breath. Choosing the wrong plan does not mean you failed or that you are stuck forever. Medicare has rules, yes, but it also has options. The key is understanding what can still be fixed and what simply needs a smarter plan going forward.

First, Take a Breath and Get Clear on What Is Not Working

Before making any changes, I always tell my clients to slow down and name the problem. Medicare plans are complex, and frustration can make everything feel broken when it is really just one or two issues.

Here are the most common problems I hear about:

- Prescription drug costs are much higher than expected

- Doctors or hospitals are no longer in the plan’s network

- Referrals and prior authorizations feel restrictive or confusing

- Copays are adding up faster than planned

- Extra benefits sounded good but are hard to use in real life

Not every issue requires switching plans. Sometimes a simple pharmacy change can lower drug costs. Other times, a formulary exception or a better understanding of how referrals and network types work can make a big difference. But when core needs like doctors or medications are not lining up, that is when we look at bigger changes.

I changed my plan during Open Enrollment and now I can't see my regular specialist. Isn't this what the whole review period is supposed to prevent?

I will best answer this based upon what information is in the question. If you changed to another medicare advantage plan during AEP and you found out after that you can’t see your specialist—out of network I’m guessing, then you can always change an MA Plan during the Medicare Advantage Open Enrollment period of January 1st - March 31st. But if that timeline has passed then you can see if you qualify for a SEP (Special Enrollment period) so that you can change your plan. This SEP would be based upon that you received inaccurate information. You can call 1-800-Medicare to explain your situation and ask about a SEP.If You Chose Medicare Advantage, You May Still Have a Window

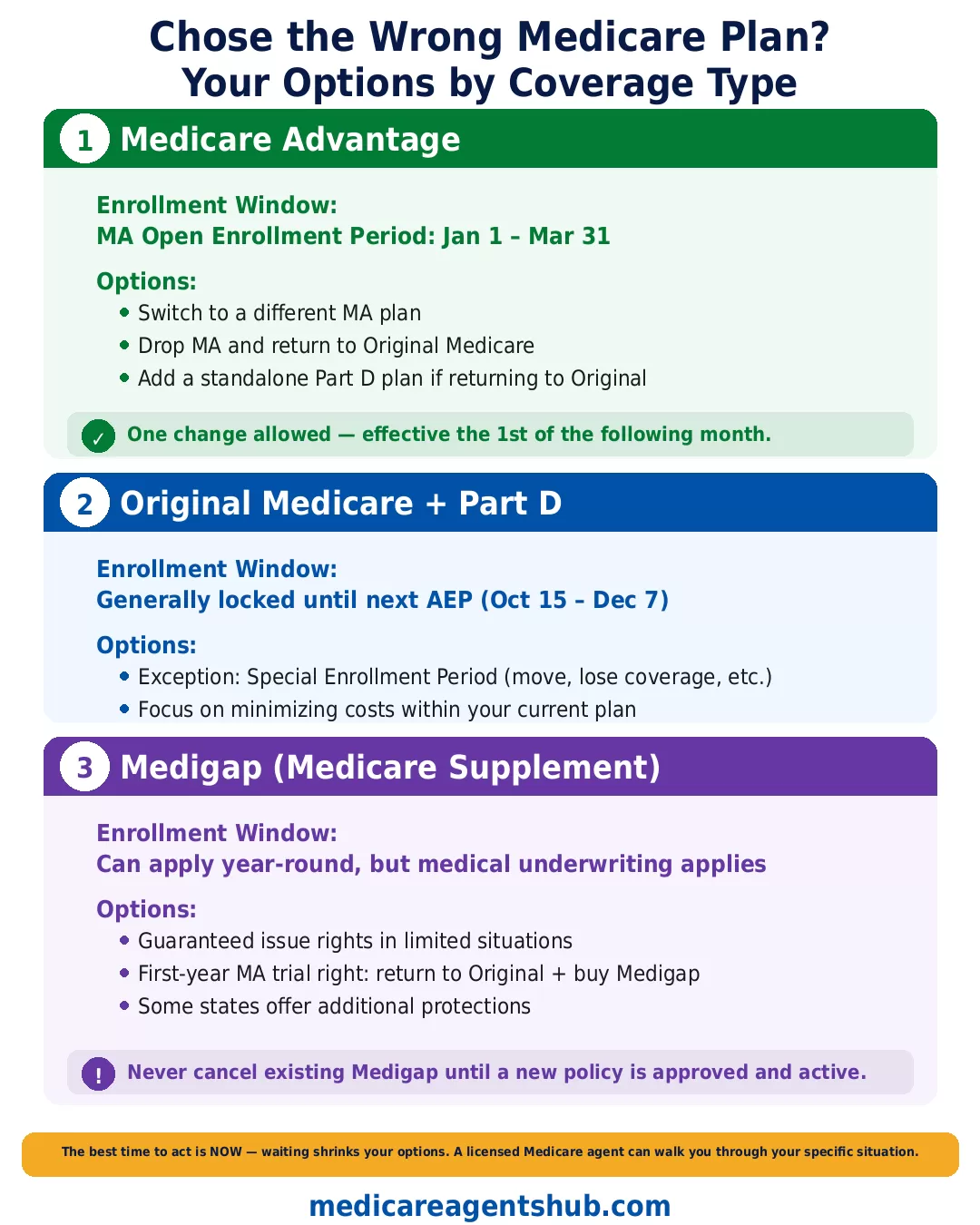

If you are enrolled in a Medicare Advantage plan, there is an important enrollment period many people do not realize exists. It is called the Medicare Advantage Open Enrollment Period, and it runs from January 1 through March 31 each year.

During this time, you are allowed to make one change if your current Medicare Advantage plan is not working for you.

You can:

- Switch to a different Medicare Advantage plan

- Drop Medicare Advantage and return to Original Medicare

- Enroll in a standalone Part D prescription drug plan if you return to Original Medicare

Any change you make usually starts the first day of the month after the plan receives your request. This is a one-time opportunity, so it is important to review your OEP options carefully rather than rushing into another decision out of frustration.

If we choose a Medicare Advantage plan and later regret it, can we go back to Original Medicare without penalties?

Yes, you can go back to Original Medicare, but there are a few rules.If you try a Medicare Advantage plan for the first time and don’t like it, you get one year to change your mind. During that first year, you can switch back to Original Medicare or back to a Medigap (supplement) plan with no problem. This is called trial rights.

If you’ve been in a Medicare Advantage plan for more than a year, you can still go back, to original medicare but only during certain times each year, like October 15 to December 7 or January 1 to March 31.

You won’t pay a penalty for switching back, but you might not be guaranteed to get a Medigap plan again if you had that previously. You may have to go through underwriting, some insurance companies might say no or charge more.

So yes, you can go back without penalties.

Any other questions feel free to reach out.

Thanks

What If You Have Original Medicare With a Drug Plan?

If you are on Original Medicare and only changed your Part D prescription drug plan during AEP, the rules are tighter. In most cases, you cannot switch drug plans again until the next Annual Enrollment Period unless you qualify for a Special Enrollment Period.

Special Enrollment Periods are triggered by specific life events. These include moving out of your plan’s service area, losing other creditable coverage, or your plan leaving Medicare. If none of these apply, you may need to stay put for now and focus on minimizing your prescription costs where you can.

This is one of the hardest conversations I have with clients, but it is also where planning ahead becomes incredibly valuable.

Medigap Changes Require Extra Care

If your regret involves a Medicare Supplement, also called Medigap, please move slowly. Medigap rules are very different from Medicare Advantage.

In most states, you can apply for a Medigap plan year-round, but once you are past your initial six-month Medigap enrollment window, insurance companies are usually allowed to use medical underwriting. That means they can deny your application or charge more based on your health.

There are a few important exceptions:

- If you are in your first year of Medicare Advantage and decide to return to Original Medicare, you may have a trial right to buy certain Medigap plans without underwriting

- Some states offer additional consumer protections that allow limited plan changes

- Certain situations create guaranteed issue rights, such as your plan ending coverage

This is why I always tell people not to cancel an existing Medigap policy until a new one is approved and active. Once you give up a supplement, getting it back is not always guaranteed.

I missed my Medigap window by a few months and now no one will cover me without underwriting. Why isn't this rule more well known?

Most people simply are not told about it.When you first enroll in Medicare Part B, you get a one time Medigap open enrollment period where you can buy a Supplement plan with no health questions. After that window closes, insurance companies can ask health questions and can decline you.

This rule is buried in Medicare materials and rarely explained clearly, so many people assume they can sign up anytime.

This is one of the biggest reasons working with a Medicare agent matters. An agent makes sure you understand these deadlines before they pass so you do not lose guaranteed options.

Why Waiting Often Makes Things Worse

I completely understand the urge to ignore the problem and hope it sorts itself out. Unfortunately, with Medicare, waiting usually makes things harder.

Delaying action can lead to:

- Higher out-of-pocket costs that quietly add up

- Delays in care because of network or authorization issues

- Missed enrollment windows that limit future choices

Medicare is very structured. Once certain windows close, flexibility drops. Acting early gives you more control and more peace of mind.

How to Make a Smarter Correction

If you think you chose the wrong plan, here is the same checklist I walk through with my own clients:

- Write down exactly what is not working and why

- Confirm whether you are on Medicare Advantage, Original Medicare, or a supplement

- Check if you qualify for the Medicare Advantage Open Enrollment Period or a Special Enrollment Period

- Compare plans based on doctors, prescriptions, and total yearly costs, not just premiums

- Get help if you feel overwhelmed

Licensed Medicare agents, SHIP counselors, and Medicare.gov tools exist for a reason. Medicare is not meant to be figured out alone, and asking for help now is far better than paying for a costly Medicare mistake all year long.

Preparing for the Next Annual Enrollment Period

Even if you cannot make a change right now, this experience is valuable. Pay attention to how you use your coverage throughout the year. Track your prescriptions, doctor visits, and unexpected costs. When your plan’s Annual Notice of Change arrives in the fall, read it carefully.

The best Medicare decisions are made before deadlines, not during them.

When is a good time to start preparing for AEP?

A good time to start preparing for (AEP) or Annual Enrollment Period is late August/September. This allows you to review your current coverage what you currently like and dislike about it. You can also look for any upcoming changes from your current plan, compare new options, and gather medications or provider lists, this helps with not having to rush through the process of renewal after the October 15th start date.The Bottom Line

Choosing the wrong Medicare plan during AEP is frustrating, but it is also very common. In many cases, it is fixable. The most important thing is understanding which rules apply to your situation and acting within the right timeframes.

Medicare is not one-size-fits-all, and adjusting your coverage is part of the learning curve. If something feels off, trust that feeling and explore your options with a Medicare advisor. Taking action now can save you money, stress, and a lot of unnecessary worry later in the year.