Getting Sicker Won't Get You a New Medicare Plan: The SEP Myth and the Chronic Conditions That May Qualify

-

May 15, 2026

You just got a diagnosis you weren't expecting. Maybe it's a new cancer finding, a stroke, or a serious fall that changed everything overnight. Your first instinct is to call your insurance and switch to something better. That instinct makes total sense, and it's wrong.

Medicare does not grant a Special Enrollment Period (SEP) just because your health takes a turn for the worse. A cancer diagnosis, a stroke, a hospitalization, a rapid decline in mobility: none of these, by themselves, give you the right to change your Medicare Advantage or Part D plan outside the normal enrollment windows. This is one of the most persistent misunderstandings in Medicare, and agents across the country correct it constantly.

But there is a narrow exception that applies to a specific set of chronic conditions, and it works differently than most people expect.

Why Worsening Health Doesn't Qualify as a Special Enrollment Period

Medicare's enrollment rules are built around life events, not health events. The qualifying triggers for an SEP include things like moving out of your plan's service area, losing employer coverage, gaining Medicaid eligibility, or having your plan terminated by the carrier. Health status isn't on that list.

This trips people up because it feels backward. If you're sicker, shouldn't you be able to get better coverage? The logic is understandable, but CMS (the Centers for Medicare & Medicaid Services) designed the system so that plans can't be gamed by enrolling only when expensive care is needed and dropping afterward. The trade-off is that Medicare's enrollment periods are rigid by design, even when the timing feels cruel.

Dissatisfaction with your current plan's coverage after a health scare is not a qualifying event either. If your plan's network doesn't include the specialist you now need, or your out-of-pocket costs are higher than you anticipated, your next opportunity to switch is during the Annual Enrollment Period (AEP) from October 15 through December 7, or during the Medicare Advantage Open Enrollment Period (OEP) from January 1 through March 31 if you're already in an Advantage plan.

Do I qualify for SEP if my health dramatically gets worse out of nowhere?

Generally NO. There are two exceptions. One is being diagnosed with Kidney failure. The other is being diagnosed with ALS.A third is being diagnosed with Diabetes, Chronic heart failure or Cardio Vascular Disease.

The Exception: Chronic Condition Special Needs Plans (C-SNPs)

There is one path that connects a medical diagnosis to a plan change, and it runs through Chronic Condition Special Needs Plans, or C-SNPs. These are a specific type of Medicare Advantage plan built for people living with certain severe or chronic illnesses. If you're diagnosed with a qualifying condition and a C-SNP is available in your area, you can enroll at any time during the year using a special enrollment period.

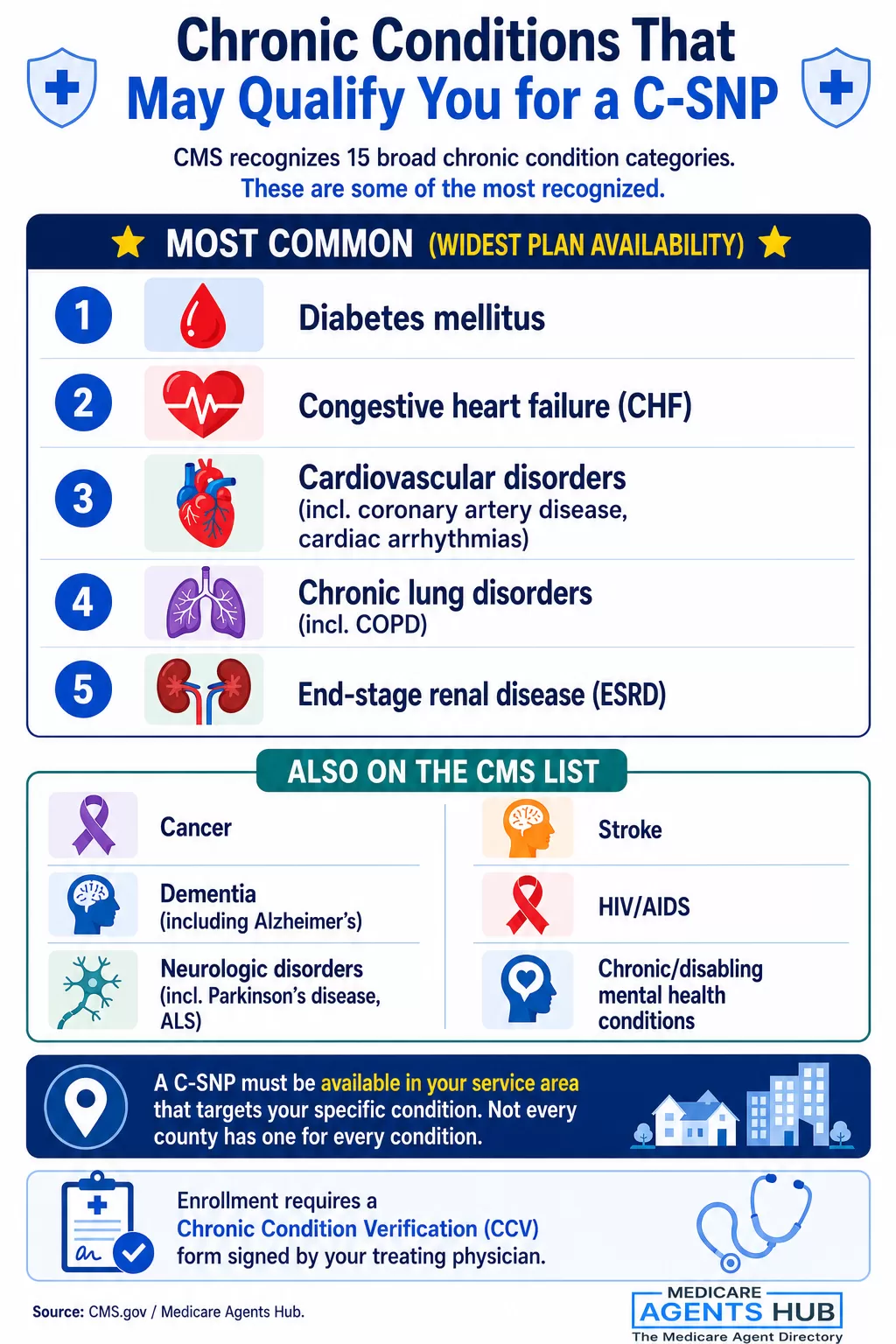

CMS recognizes 15 broad chronic condition categories that can qualify someone for C-SNP enrollment. The most common ones agents work with include:

- Diabetes mellitus

- Congestive heart failure (CHF)

- Cardiovascular disorders (including coronary artery disease and cardiac arrhythmias)

- Chronic lung disorders (including COPD and certain other respiratory conditions)

- End-stage renal disease (ESRD)

But the full CMS list also includes cancer, dementia (including Alzheimer's disease), neurologic disorders (including Parkinson's disease and ALS), stroke, HIV/AIDS, chronic/disabling mental health conditions, and several others. The complete list is broader than most people realize.

The catch is that a C-SNP must be available in your service area that targets your specific condition. Not every condition on the CMS list has an active plan in every county. The five conditions listed above are the ones with the widest plan availability nationwide, which is why agents bring them up most often. But if you've been diagnosed with cancer, dementia, Parkinson's, or another qualifying condition, it's worth checking whether a C-SNP exists near you.

Do I qualify for SEP if my health dramatically gets worse out of nowhere?

A sudden worsening of health, even with hospitalization, generally does not give you a Medicare Special Enrollment Period (SEP) to change coverage mid-year.What can create a Medicare SEP that sometimes relates to a health change is one of these situations:

- You qualify for a Chronic Condition Special Needs Plan (C‑SNP): If you are diagnosed with a qualifying chronic condition and a C‑SNP is available where you live, you may be able to join that plan using an SEP.

- You enter, live in, or leave an institution: If you are in a skilled nursing facility, nursing home, or similar facility, you may have an SEP to change Medicare Advantage/Part D coverage.

- You gain or lose Extra Help (LIS) or Medicaid: These programs can allow plan changes outside the usual enrollment periods.

- You move or lose other coverage: Moving out of your plan’s service area or losing creditable drug/employer coverage can trigger SEPs.

- Your plan changes materially: Certain plan terminations or other CMS-approved circumstances can trigger an SEP.

If none of those apply, your main options are usually:

- Annual Enrollment Period (AEP): Oct 15–Dec 7 (changes effective Jan 1).

- Medicare Advantage Open Enrollment Period (MA OEP): Jan 1–Mar 31 (only if you are already in a Medicare Advantage plan).

- State Medigap switching rules (where available): If you have a Medigap (supplement) policy, some states give extra opportunities to switch plans without medical underwriting, such as California and Oregon's “birthday rule,” which can allow a switch to a Medigap plan with equal or lesser benefits around your birthday (subject to state timing and requirements).

How C-SNP Enrollment Actually Works

Getting into a C-SNP isn't as simple as calling a plan and saying you have diabetes. There's a verification process that involves your doctor, and skipping it will get your enrollment denied.

Confirming Your Qualifying Condition

When you apply for a C-SNP, the insurance carrier must confirm that you have the qualifying chronic condition. This is typically done through a Chronic Condition Verification (CCV) form signed by your treating physician, or through a CMS-approved pre-enrollment assessment tool, depending on the plan. The form or assessment confirms your diagnosis and verifies that you meet the plan's clinical criteria.

If the carrier doesn't receive confirmation within the required timeframe, you can be disenrolled from the plan. Your agent and your doctor both need to be in the loop from the beginning so this doesn't slip through the cracks.

This Isn't an Unlimited Pass to Keep Switching

The C-SNP special enrollment period is available while you have the qualifying condition and ends once you're enrolled in the chronic care SNP. It's not an open-ended window that lets you keep switching plans mid-year. After enrollment, changes generally have to go through another applicable election period like AEP or OEP, just like any other Medicare Advantage plan.

C-SNPs are Medicare Advantage plans, so they come with the same structural features: provider networks, prior authorization requirements, and annual plan changes. They're designed to coordinate care around your specific condition, often with lower copays for related services and medications, dedicated care management teams, and formularies tailored to your treatment needs.

What’s the best time of year to change my Medicare plan if I develop a new diagnosis?

If you are diagnosed by a doctor with a chronic illness such as diabetes, heart failure, cardiovascular disease, COPD, end stage renal disease and among others listed by insurance carriers, you can change immediately.SEPs That Get Confused With Health-Based Enrollment

Part of the confusion around "health changes = plan changes" comes from SEPs that look health-related but are actually triggered by something else. These are worth knowing about, because one of them might apply to your situation even if the C-SNP path doesn't.

Institutionalization

If you move into, currently reside in, or are discharged from a skilled nursing facility, long-term care facility, or similar institution, you have an SEP to change your Medicare Advantage or Part D coverage. This one feels health-related because the reason you're in a facility is usually a health event. But the trigger is the institutional status, not the diagnosis.

Gaining Medicaid or Extra Help (LIS)

A serious health event can sometimes push your income down or your expenses up enough to qualify for Medicaid or the Low-Income Subsidy (Extra Help) program. If you newly qualify, that creates an SEP allowing plan changes. Again, the trigger isn't the diagnosis itself, but the resulting change in financial eligibility.

Plan Termination or Service Area Change

If your Medicare Advantage plan exits your county or terminates entirely, you get an SEP and often guaranteed-issue rights into a new plan. This has been happening more frequently as carriers restructure their networks, especially in rural areas. It's not a health trigger, but it sometimes coincides with a health crisis if you're losing access to providers mid-treatment.

The 5-Star SEP

If a Medicare Advantage plan in your area carries a 5-star quality rating from CMS, you can enroll in that specific plan once per year outside of AEP. This is rarely discussed and even more rarely used, but it exists as an option regardless of your health status.

What to Do When You Don't Qualify for a C-SNP

If your diagnosis doesn't match the C-SNP list, no C-SNP is available in your area for your condition, and none of the adjacent SEPs apply, your options are more limited, but they're not zero.

Review your current plan immediately. Most Medicare Advantage plans cover a wider range of services than people realize. Check whether your plan has a care management program, a nurse hotline, or disease-specific support services you haven't activated. Your plan may already cover what you need, just not in the way you expected.

Use the next enrollment window strategically. If you're between enrollment periods, start researching now. Compare Medicare Advantage plans versus Medigap options based on your new medical reality. Look at out-of-pocket maximums, specialist copays, and drug formularies with your actual prescriptions and treatment plan in hand. An agent can run this comparison for you at no cost.

Consider whether Medigap is the long-term play. If you're currently on Medicare Advantage and your health has gotten more complex, you may want to evaluate switching to Original Medicare with a Medigap supplement during the next AEP. The catch: in most states, switching from Medicare Advantage back to Original Medicare means you'll face medical underwriting for Medigap, and a recent serious diagnosis could make that difficult or expensive. This is a conversation to have with a licensed agent who knows your state's rules.

Talk to a local Medicare agent. The intersection of enrollment rules, plan availability, and your specific health situation is exactly the kind of problem a local Medicare broker handles every day. Agents don't charge you for their help, and they can identify options you might not know exist, including C-SNP availability in your area, state-specific guaranteed-issue rules, and whether any of the adjacent SEPs apply to your circumstances.

How can my Medicare plan still meet my needs if my health changes?

We have a deep understanding of the qualifying health changes or life events that would trigger a Special Enrollment Period. Based on your coverage, we can also provide guidance on your ability to make changes during the Annual Enrollment Period (Oct. 15–Dec. 7) and the Medicare Advantage Open Enrollment Period (Jan. 1–Mar. 31).The Bottom Line on Health Changes and Medicare Enrollment

Medicare's enrollment system wasn't built to respond to individual health crises. That's a hard reality to accept when you're the one in the hospital bed. But understanding the rules as they actually work, rather than how they should work, puts you in a better position to make the right move at the right time.

If you've been diagnosed with a condition on CMS's C-SNP qualifying list, including diabetes, heart failure, cardiovascular disease, chronic lung disorders, cancer, dementia, stroke, or other recognized chronic conditions, you may have a C-SNP enrollment window available right now. Talk to your doctor about condition verification and connect with an agent who can check plan availability in your zip code.

For everyone else, the Annual Enrollment Period from October 15 through December 7 is your next opportunity to make changes. Start planning before October, not after, so you're comparing plans with your current treatment needs front and center.