What Counts as Creditable Coverage for Medicare?

Do I Need Medicare If I Already Have Insurance?

As people approach age 65, one of the most common questions I hear is, "Do I really need to sign up for Medicare if I already have insurance?" It's a fair question — and one that doesn't always have a simple yes-or-no answer.

The real issue isn't whether you have insurance, but whether that insurance is considered creditable coverage under Medicare rules. Understanding this distinction is important, because enrolling late without the right type of coverage can lead to penalties that last for the rest of your life.

Creditable coverage simply means health or prescription drug coverage that Medicare considers at least as good as what Medicare itself provides. When someone has creditable coverage at the time they first become eligible for Medicare, they may be able to delay enrolling in certain parts of Medicare without penalty. When they don't, the consequences can be costly and permanent.

Is Medicare Part A enough for hospital coverage?

Medicare Part A does cover hospital stays, but it’s usually not enough on its own. There are deductibles and costs you may still be responsible for, so most people add Part B and sometimes a supplement or Advantage plan to help with those gaps.When Employer Coverage Allows You to Delay Medicare

This comes up most often with people who are still working past 65 or who are covered under a spouse's employer plan. In many cases, employer-sponsored coverage can be considered creditable, but only under specific conditions. Generally, the coverage must be based on active employment and come from an employer with 20 or more employees. When those requirements are met, delaying Medicare Part B may be allowed.

Where people often get into trouble is assuming that all coverage counts. The following types of plans may provide real benefits, but Medicare does not treat them as creditable for enrollment purposes:

- COBRA

- Retiree health insurance

- Individual marketplace plans

- Short-term policies

- Veterans benefits as the only coverage in place

Relying on one of these plans instead of Medicare can result in unexpected penalties later.

What happens if I delay Medicare Part A enrollment because I'm still on my spouse's employer plan?

If covered under your spouse’s active employer plan, you can delay Medicare Part A without a penalty. When that coverage ends, you have a special enrollment window to sign up.Federal employees present another tricky scenario — FEHB coverage interacts with Medicare in ways that catch many early retirees off guard, particularly around Part B enrollment timing. For more on that and other edge cases, see unusual Medicare situations agents encounter in the field.

Medicare Penalties for Late Enrollment

If Medicare Part B is delayed without creditable coverage, Medicare applies a late enrollment penalty. That penalty increases the Part B premium by 10 percent for every full year someone was eligible but did not enroll. Once applied, that increase stays in place for life. In addition, enrollment may be limited to specific times of the year, which can leave gaps in coverage.

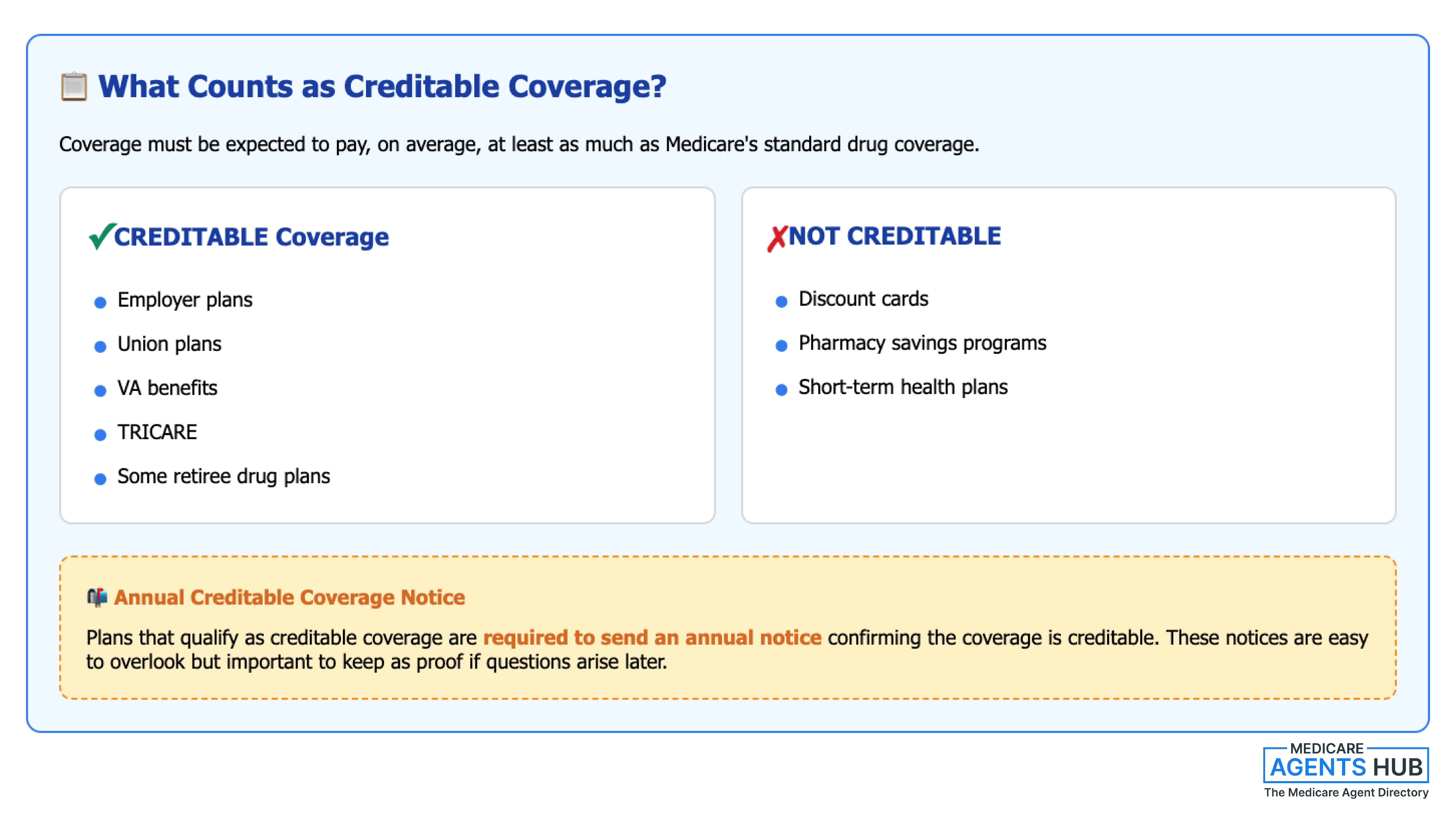

Prescription drug coverage has its own set of rules. Medicare Part D includes a separate late enrollment penalty, and this one can affect people even if they don't take medications when they first become eligible. For prescription coverage to be considered creditable, it must be expected to pay, on average, at least as much as Medicare's standard drug coverage.

Many plans meet this standard and do count as creditable drug coverage:

- Employer plans

- Union plans

- VA benefits

- TRICARE

- Some retiree drug plans

When they do, the plan is required to send a notice each year confirming that the coverage is creditable. These notices are easy to overlook, but they are important to keep, as they serve as proof if questions come up later.

On the other hand, the following do not count as creditable drug coverage:

- Discount cards

- Pharmacy savings programs

- Short-term health plans

If someone goes 63 days or more without creditable prescription coverage after becoming eligible for Medicare, a penalty may apply. Like the Part B penalty, this additional cost is typically permanent.

Timing, Special Enrollment Periods, and Avoiding Mistakes

Timing also matters when coverage ends. When someone loses employer coverage due to retirement or job loss, Medicare allows a limited window — known as a Special Enrollment Period — to enroll without penalties. These windows are strict and missing them can turn an otherwise smooth transition into an expensive mistake.

What makes this topic especially challenging is that Medicare rules don't apply the same way to everyone. Employer size, employment status, and the type of coverage all play a role. Advice that worked for a coworker or family member may not apply to another situation at all.

Am I eligible for a Special Enrollment Period if I lose employer coverage?

Yes. Losing employer coverage usually qualifies you for a Special Enrollment Period, allowing you to enroll in Medicare without penalties.The good news is that most Medicare penalties are avoidable. They usually happen not because people ignore Medicare, but because they don't realize how specific the rules are. Asking questions early and understanding whether current coverage is truly creditable can make all the difference.

About the Author: Heidi Wotton is a licensed Medicare Advisor who helps individuals understand Medicare rules, enrollment timelines, and how to avoid costly penalties by providing clear, educational guidance.