Critical Medicare Mistakes to Avoid (and How to Protect Yourself)

")

-

Last Updated July 22, 2026

Written by Robert Vaughan, R.Ph., MBA

Medicare Broker Licensed in CA, AZ, ID, NM, NV & TX

Navigating Medicare can be one of the most important, and confusing, milestones in your healthcare journey. While Medicare provides essential health coverage for millions of Americans aged 65 and older, making the wrong decision (or delaying the right one) can result in costly consequences.

Whether you are approaching eligibility or helping a loved one manage their transition into Medicare, it is essential to understand what not to do. Avoiding common mistakes can save you thousands of dollars in penalties, help you access the care you need when you need it, and give you peace of mind for the future.

In this article, we will explore three of the most critical Medicare mistakes to avoid:

- Missing Enrollment Periods and Incurring Penalties

- Enrolling in Medicare Part B Before You Are Ready

- Delaying the Coverage You May Need in a Health Crisis

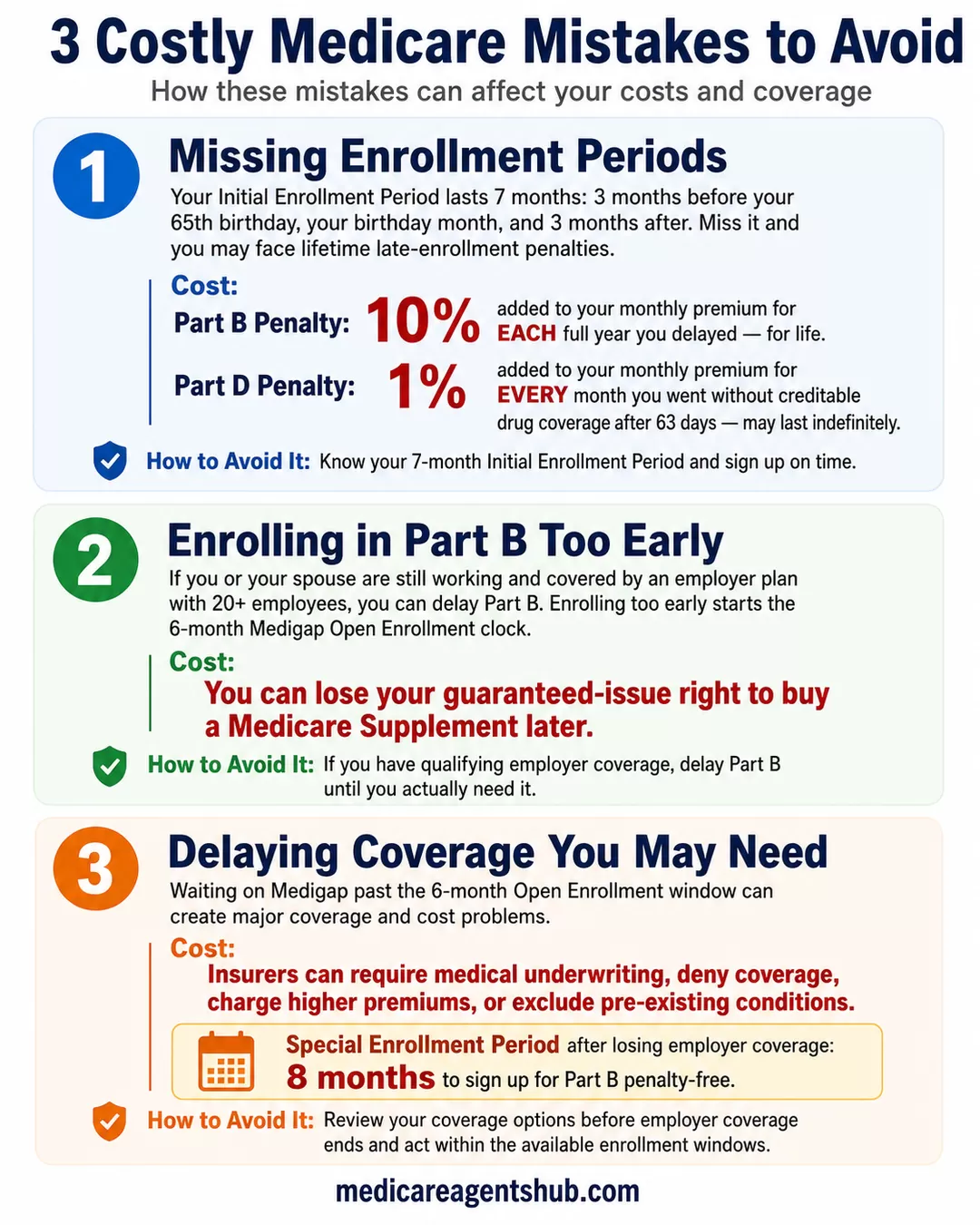

Mistake #1: Missing Enrollment Periods and Incurring Penalties

The most common and financially damaging Medicare mistake is failing to enroll on time.

When you first become eligible for Medicare (typically at age 65), you are given a 7-month Initial Enrollment Period (IEP). This window begins three months before your 65th birthday, includes the month of your birthday, and ends three months after.

If you miss this window and do not have other creditable coverage (like employer-based insurance), you could face lifetime late-enrollment penalties.

The Cost of Delay:

- Part B Penalty: If you delay enrolling in Part B and do not have other creditable coverage, you will pay a 10% premium penalty for each full year you could have had Part B but did not. This penalty is added to your monthly premium for life.

- Part D Penalty: If you go without creditable prescription drug coverage for more than 63 consecutive days, you will pay a 1% penalty for every month you are late. Like the Part B penalty, this is added to your monthly premium and may last indefinitely.

How to Avoid It:

- Mark your calendar when you are approaching 65.

- Understand whether your current health insurance qualifies as creditable coverage. If it does not, you’ll need to sign up for Medicare during your IEP to avoid penalties.

- If you miss your IEP, you can enroll during the General Enrollment Period (January 1–March 31), but coverage will not start until the first of the month following enrollment, and penalties may apply.

Missing your enrollment window can create lasting financial strain, especially if you are living on a fixed income. Planning ahead and understanding your eligibility timeline is your first defense.

Why am I paying more for Medicare Part B and D than my friends? What is IRMAA and how is it calculated?

You are paying more for your Medicare Part B and Part D premiums due to the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA is a surcharge added to Part B and Part D premiums for those with higher incomes, based on their Modified Adjusted Gross Income (MAGI) from two years prior. You can find your MAGI on line 11 of your IRS Form 1040. The Social Security Administration (SSA) determines IRMAA amounts based on income brackets, and these brackets are adjusted annually for inflation.If you disagree with the Income-Related Monthly Adjustment Amount (IRMAA) that the Social Security Administration (SSA) has determined you need to pay for your Medicare Part B and/or Part D premiums, you have the right to appeal.

How to Request a Reconsideration:

Complete and submit Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount - Life-Changing Event).

Provide supporting documentation: This may include tax returns, marriage/divorce certificates, employer statements, and other evidence relevant to your specific situation.

You can contact the SSA for assistance with the reconsideration process and documentation requirements.

Mistake #2: Enrolling in Medicare Part B Before You Are Ready

While missing enrollment can be costly, enrolling too early can also be a problem, particularly when it comes to Medicare Part B.

Part B covers outpatient services like doctor visits, preventive care, and durable medical equipment. Unlike Part A (which is often premium-free), Part B comes with a monthly premium, and you do not want to pay it before you need to.

When It Is Okay to Delay Part B:

If you or your spouse are still working (active employment) and have employer-sponsored health insurance, you may be able to delay Part B without penalty. The key factor is the size of the employer:

- If the employer has 20 or more employees, the employer plan is the primary payer, and you can delay Part B until you retire or lose that coverage.

- Once you stop working or lose that coverage, you will have an 8-month Special Enrollment Period (SEP) to sign up for Part B without a penalty.

Why Enrolling Too Early Can Hurt:

- You will start paying Part B premiums even if you are still fully covered by your employer plan.

- Signing up for Medicare Part B too soon could eliminate your guaranteed issue right for a Medicare Supplement policy. The Medicare Supplement Open Enrollment Period is a six-month window that begins the month you are enrolled in Medicare Part B. During this window, you have a guaranteed right to buy any Medicare Supplement plan sold in your state. After this period, you may have to undergo medical underwriting and the insurance company can deny coverage, charge higher premiums, or exclude coverage for existing health conditions.

How to Avoid It:

- Confirm whether your employer coverage is creditable and whether it is primary or secondary.

- Delay Part B enrollment only if your employer plan is considered creditable.

- Document your coverage and understand your SEP rights to avoid penalties when you do need to enroll.

Making sure you are not paying for unnecessary coverage, while still avoiding penalties, is a delicate balance, but one that can keep more money in your pocket.

Mistake #3: Delaying the Coverage You May Need in a Health Crisis

The third common mistake? Choosing minimal coverage now, thinking you can upgrade later if your health changes. Unfortunately, it is not always that easy.

Many Medicare beneficiaries choose the lowest-cost plan available, especially when they are healthy. But what happens when you get sick or injured and suddenly face mounting medical bills?

The Risk:

- Original Medicare (Parts A and B) does not cover everything. You are responsible for 20% of most outpatient costs, with no out-of-pocket maximum.

- If you skip adding a Medigap plan or do not choose a robust Medicare Advantage plan, you could be stuck with high out-of-pocket costs.

- Switching plans later is not always guaranteed. In many states, after your one-time Medicare Supplement Open Enrollment Period (6 months after enrolling in Part B), insurers can deny you coverage or charge more based on your health.

Real-World Example:

Imagine you choose Original Medicare and a basic Part D drug plan at 65, thinking you are healthy and do not need more. At 67, you are diagnosed with a chronic condition that requires frequent doctor visits and expensive medications.

Now, when you try to apply for a Medicare Supplement plan to help cover your costs, you are subject to medical underwriting and may be denied or charged significantly higher premiums.

How to Avoid It:

- Choose a plan that meets your current and future health risks.

- Consider a Medicare Advantage plan that includes additional coverage (like dental, vision, hearing, and a cap on out-of-pocket costs), or a Medicare Supplement plan to pair with Original Medicare.

- Reevaluate your plan each year during the Annual Enrollment Period (Oct. 15–Dec. 7) to ensure your coverage continues to meet your needs.

When you are healthy, it is easy to underestimate your need for coverage, but health issues can arise suddenly. Protecting yourself with the right plan before you need it can save you thousands and give you access to timely, quality care.

Can I switch from a Medicare Advantage plan to Original Medicare with a Medigap plan mid-year if I’m diagnosed with a serious illness?

No, not mid-year. You can use the Medicare Advantage Open Enrollment Period (MA OEP), which runs from January 1 to March 31 each year, to return to Original Medicare and apply for a Medicare Supplement (Medigap) plan. The issue here is serious illness, which would likely disqualify you from Medicare Supplement plans. You have 6 months from your Medicare Part B effective date to enroll in a Medicare Supplement plan without going through underwriting. Insurance companies can deny your application for a Medicare Supplement if submitted outside of this 6 month window.Final Thoughts: Stay Informed, Plan Ahead, and Get Help When You Need It

Medicare is not one-size-fits-all, and the choices you make today can significantly impact your financial and physical well-being tomorrow. Here is a quick recap of the three most important things to avoid:

- Do not miss your Initial Enrollment Period. Penalties and delays can be long-lasting.

- Do not enroll in Medicare Part B prematurely if you have employer coverage that allows you to delay enrollment.

- Do not wait to get adequate coverage. Protect yourself from surprise medical bills when health issues arise.

Part of avoiding surprises is knowing what Medicare actually covers. Some of the answers are not what people expect, as our guide on 8 surprising Medicare coverage answers reveals. It is also worth understanding what Medicare fraud is and why you should care, since scams targeting beneficiaries can lead to costly mistakes that are entirely outside your control.

The good news? You do not have to navigate Medicare alone. A licensed independent Medicare agent or advisor can help you:

- Understand your eligibility and deadlines

- Evaluate and compare plan options

- Determine the best time to enroll based on your situation

- Reassess your coverage annually as your needs change

Medicare is too important, and too complex, to leave to guesswork. For a closer look at what can go wrong, see 10 real frustrations seniors have with Medicare and how licensed agents respond. With a little preparation and the right guidance, you can avoid costly mistakes and make confident choices that support your health and your wallet.

Need Help with Medicare? Reach out to a licensed independent Medicare agent today to get personalized, unbiased guidance and answers to your most pressing questions. It could be the most valuable healthcare decision you make all year.

How to know if a Medicare agent is legitimate?

Your first step should always be verifying their insurance license information on the state’s Department of Insurance (DOI) website. Beware of door-to-door sales; Medicare agents cannot solicit business at your home without an appointment and Medicare will never send an agent to your home to enroll you into a plan. A legitimate Medicare agent will take the time needed to understand your specific needs and recommend products to meet those needs. Look for an agent that represents multiple private insurance companies. They should lay out all your coverage options (Medicare Supplement plans, Medicare Pharmacy (Part D) plans, and Medicare Advantage plans) and provide unbiased guidance. You can also search the internet (Google) to see if they have any reviews or ask for client references.About the Author: Robert Vaughan is a Medicare Health Plan specialist licensed in CA, NV, AZ, NM, and TX with over 35 years of healthcare and insurance experience. He is the founder of Robert Vaughan Insurance Solutions based in Oakdale, CA.