Creditable Coverage and Medicare

-

September 8, 2025

If you're approaching Medicare eligibility or already enrolled, creditable coverage is one of the most important terms to understand. Get it wrong, and you could face permanent penalties on your Medicare premiums for the rest of your life. Get it right, and you'll have the flexibility to transition into Medicare on your own timeline without unnecessary costs.

This article breaks down the basics of creditable coverage, explains why it matters, and shows how a local Medicare agent can make the process much easier.

What Is Creditable Coverage?

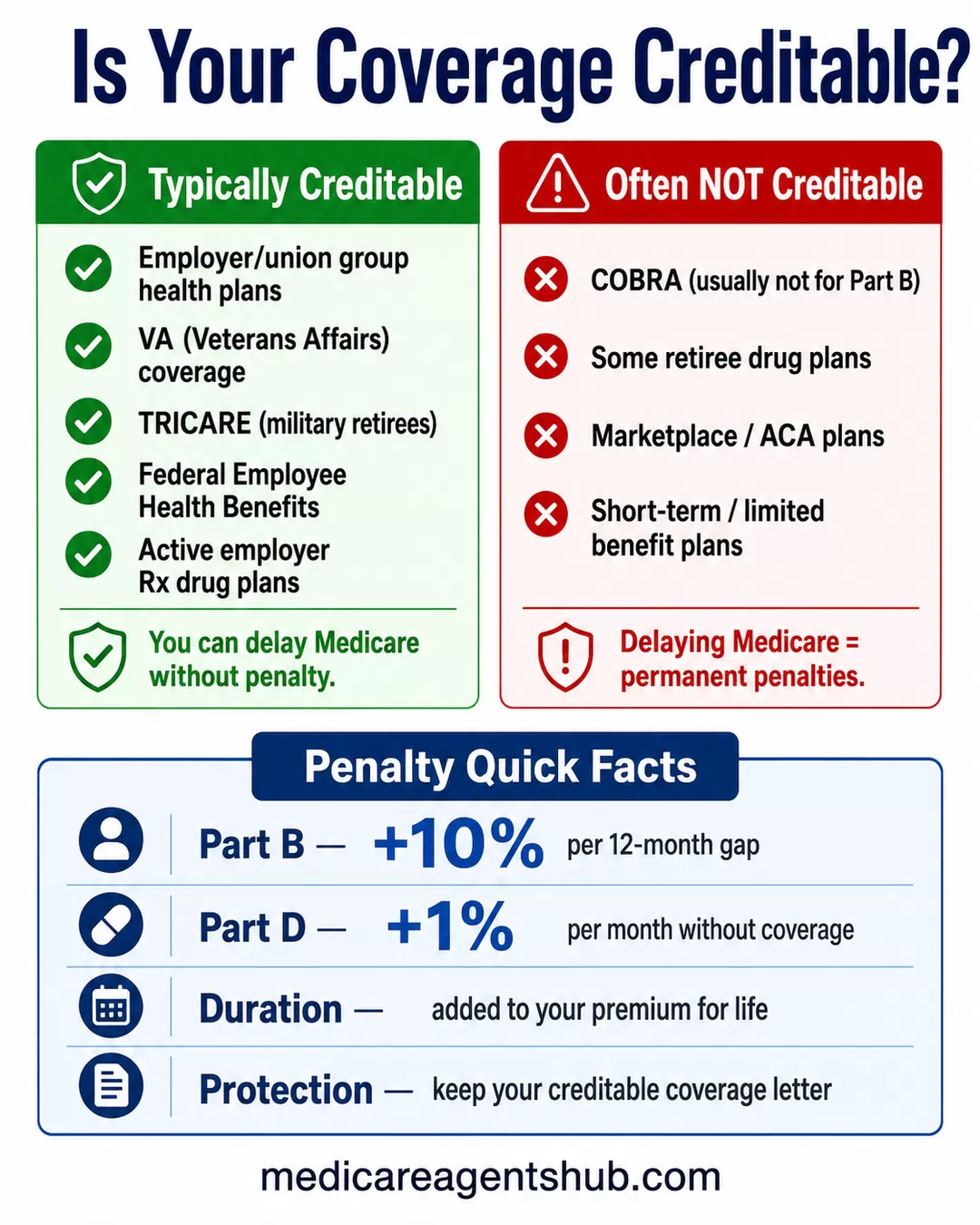

Creditable coverage is health or prescription drug insurance that Medicare considers at least as good as its own standard benefits. If you have it, you can delay enrolling in certain parts of Medicare (like Part B or Part D) without paying late enrollment penalties later.

A quick note on spelling: a lot of people search for "credible coverage" or "credible insurance." The correct term is creditable - as in something that earns you credit toward Medicare's coverage requirements. Same thing, different spelling.

Examples of plans that are often considered creditable coverage include:

-

Employer or union group health insurance (if you or your spouse is still working)

-

Veterans Affairs (VA) coverage

-

Certain retiree health plans (confirm with your plan administrator and get the notice in writing before assuming)

-

Some COBRA plans (though not always, it's important to double-check)

Each year, your insurance provider should send you a notice stating whether or not your coverage is creditable. Keep this letter - it's proof you'll need if you decide to delay Medicare.

Can you explain what "creditable coverage" means and when it applies?

Credible coverage refers to health insurance that is considered as good as or better than Medicare, particularly for part B and part D. It’s most commonly relevant when someone is delaying Medicare because they’re still working and have an employer sponsored coverage. As long as that coverage is deemed credible, you can delay enrolling in Medicare without facing late enrollment penalties. When you do retire or lose that coverage, you’ll get a special enrollment period to sign up for Medicare without penaltyWhy Does Creditable Coverage Matter?

The biggest reason creditable coverage matters is penalties. If you don't sign up for Medicare Part B or Part D when you're first eligible (and you don't have creditable coverage) you'll likely pay a permanent penalty on top of your monthly premiums. Medicare's own guidance on how to avoid late enrollment penalties is worth reading before you make any decision to delay.

Here are two common scenarios:

-

Part B (Medical Insurance): If you delay enrolling without creditable coverage, your premium increases by 10% for every 12-month period you were eligible but didn't sign up.

-

Part D (Prescription Drug Coverage): If you go without Part D or creditable prescription coverage for 63 days or more, you'll pay an extra penalty added to your Part D premium for life.

For many people, these penalties add up to thousands of dollars over time. Understanding whether you have creditable coverage can help you avoid these unnecessary costs.

If a senior is turning 65 but still working, should they enroll in Medicare or delay it?

It depends largely on the size of the employer, often referred to as the Medicare “rule of 20.”If the employer has 20 or more employees, their group coverage is typically considered primary, and the senior can delay enrolling in Medicare Part B without penalty as long as they maintain that creditable employer coverage.

If the employer has fewer than 20 employees, Medicare generally becomes primary at age 65, and delaying Part B could lead to gaps in coverage and potential late enrollment penalties.

Because of this rule, it’s important to review the employer size and coverage details before deciding whether to enroll or delay Medicare.

Creditable Prescription Drug Coverage

The rules for creditable prescription drug coverage are a little different from the rules for medical coverage, and this is where a lot of people trip up. A drug plan is considered creditable if it pays out, on average, at least as much as a standard Medicare Part D plan would.

Plans that commonly qualify as creditable drug coverage include:

-

Most employer or union group prescription drug plans

-

Some retiree drug plans (but not all - always check the notice)

-

TRICARE prescription benefits

-

VA prescription coverage

Plans that usually do not qualify:

-

Prescription discount cards (these aren't insurance)

-

Some limited-benefit or high-deductible plans that don't meet Medicare's actuarial standard

-

Indian Health Service coverage (not creditable for Part D)

Every plan sponsor is required to send you a Notice of Creditable Coverage each year, usually in September or October before the Annual Enrollment Period. If your drug plan is not creditable and you don't sign up for Part D within 63 days of losing it, the Part D late enrollment penalty follows you for as long as you have Medicare.

Certificate of Creditable Coverage: How to Get Proof

The only way to know for sure whether your plan qualifies is to get it in writing. Each fall, insurance providers are required to send out a Notice of Creditable Coverage (sometimes called a certificate or letter of creditable coverage). This document states whether your current health or drug plan meets Medicare's standard. You can read the official CMS guidance on creditable coverage notices if you want to see exactly what plan sponsors are required to disclose.

If you don't receive a notice, ask your HR department, insurance company, or benefits administrator to send you one. If you're proving creditable coverage to delay Medicare Part B, you may also need Form CMS-L564 (Request for Employment Information) filled out by your employer. Never assume your plan qualifies - it's better to double-check than to face a penalty later. For a deeper breakdown, see what counts as creditable coverage for Medicare.

If you're still working past 65 with employer coverage, your situation is especially worth reviewing. The rules around employer plan size, active employment status, and spouse coverage all affect whether you can safely delay enrollment.

Common Misunderstandings About Creditable Coverage

Many people make costly mistakes because they assume their coverage is creditable when it isn't. Here are a few common misunderstandings:

-

"I have COBRA, so I'm covered." - COBRA is not considered creditable coverage for Medicare Part B. It may qualify as creditable for Part D, but only if the notice from your plan says so. Always check the letter before relying on it.

-

"My retiree plan is always creditable." - Not always. Some retiree drug plans don't meet Medicare's standards, and Indian Health Service coverage generally isn't considered creditable for either Part B or Part D. Don't assume - get the notice in writing from your plan administrator before making any decision to delay.

-

"I can keep contributing to my HSA as long as I have employer coverage." - Once you enroll in any part of Medicare, including premium-free Part A, you lose your eligibility to contribute to a Health Savings Account. Making contributions after enrollment can trigger tax penalties. If you plan to keep funding an HSA past 65, you need to delay both Part A and Part B, not just Part B.

-

"I'll just sign up later if I need to." - Without proof of creditable coverage, signing up later usually means paying penalties for life.

These are the kinds of details that can trip people up. When you're transitioning off employer coverage, it's especially important to understand the timing rules so you don't end up in a gap.

I'm turning 65 in three months but still working with employer coverage. Do I need to sign up for Medicare right now or can I wait?

Before you decide, please find out if your employer coverage is considered to be creditable. If it is, you can delay your medicare, or at least, your part B and continue through with your employer coverage for as long as you qualify for it without having to worry about a penalty. Important detail, there are two separate penalties if your coverage was not creditable. One is for medical or part B, another one is for part D. If your coverage is credible those penalties do not apply and you can turn your part B on when you are ready to leave your employer plan.Why a Local Medicare Agent Is So Valuable

Sorting through Medicare rules on your own can feel like a full-time job. That's where a local Medicare agent comes in. Here's why working with one can make a big difference:

-

Personalized guidance: A local agent can look at your specific situation - your work status, current coverage, prescriptions, and doctors - and explain whether you have creditable coverage.

-

Clarity on penalties: They can walk you through the risks of delaying Medicare and how to avoid unnecessary costs.

-

Plan comparisons: Instead of spending hours online, a local agent can compare Medicare Advantage, Medigap, and Part D plans in your area, showing you which ones fit your needs.

-

Ongoing support: Medicare isn't "set it and forget it." Agents can review your plan each year during open enrollment to make sure you still have the right coverage.

Best of all, working with a Medicare agent costs you nothing - their services are free to you, as they are paid by the insurance companies.

For many beneficiaries, the peace of mind that comes with having a trusted local advisor outweighs the confusion and risk of going it alone. If you'd rather start with a non-commercial resource, you can also call 1-800-MEDICARE or reach out to your state's SHIP (State Health Insurance Assistance Program) counselor for free, unbiased help.

Key Takeaways

-

Creditable coverage means your insurance is as good as or better than Medicare.

-

If you have creditable coverage, you can delay Medicare enrollment without penalties.

-

Always keep proof of your creditable coverage in case Medicare asks for it.

-

Not all coverage counts. COBRA and some retiree plans may leave you exposed to penalties.

-

Enrolling in any part of Medicare, even premium-free Part A, ends your ability to contribute to an HSA.

-

A local Medicare advisor can save you time, stress, and money by helping you make the right choices.

Medicare is too important (and too complex) to leave to chance. Understanding creditable coverage ensures you don't face surprise penalties or gaps in your healthcare. If you're unsure about your situation, reaching out to a Medicare broker or agent is one of the smartest moves you can make. They can simplify the process, explain your options clearly, and help you feel confident in your Medicare decisions.